Fast: H&M. Faster: Zara. Fastest: Shein. It’s a progression that has changed consumerism, accelerated textile production, and hurt the economy while doing so. Zara disrupted H&M and then Shein unseated them both. Now, H&M has gone on the offensive in an effort to regain the advantage it once had.

The hope is to regain the millions of consumers who’ve gone the way of Zara and Shein. It all comes down to the x and y axes of two competing ideas: economics and environmental impact.

There are consequences to fast-fashion and athleisure; plastics weren’t intended to be worn and discarded with impunity.

The chatter around the future of fashion is one of pure contradiction: a young generation of shoppers say they want to preserve the environment. Juxtapose this ideal atop of what they actually buy and you’ll find that there are cracks in their collective “save the planet” philosophy. Gen Z is often referred to as the most sustainably conscious, environmentally-minded consumer segment. They’re also fuelling the rise of Shein, the biggest fast fashion company in history. Zara and H&M were small retailers in comparison. A 2021 Harvard Business School case study explained how Inditex, the parent company of Zara, innovated around supply chain efficiency to produce faster products that were more in-line with trends.

Zara was the Group’s oldest and largest brand, representing around 69% of sales, or €18 billion in 2018. At the core of Zara’s success was an innovative business model based on a very responsive supply chain and quick merchandise turnaround. Zara designed, produced and delivered new items to stores in less than three weeks, allowing it to constantly update its collections and adapt to changing customer tastes.

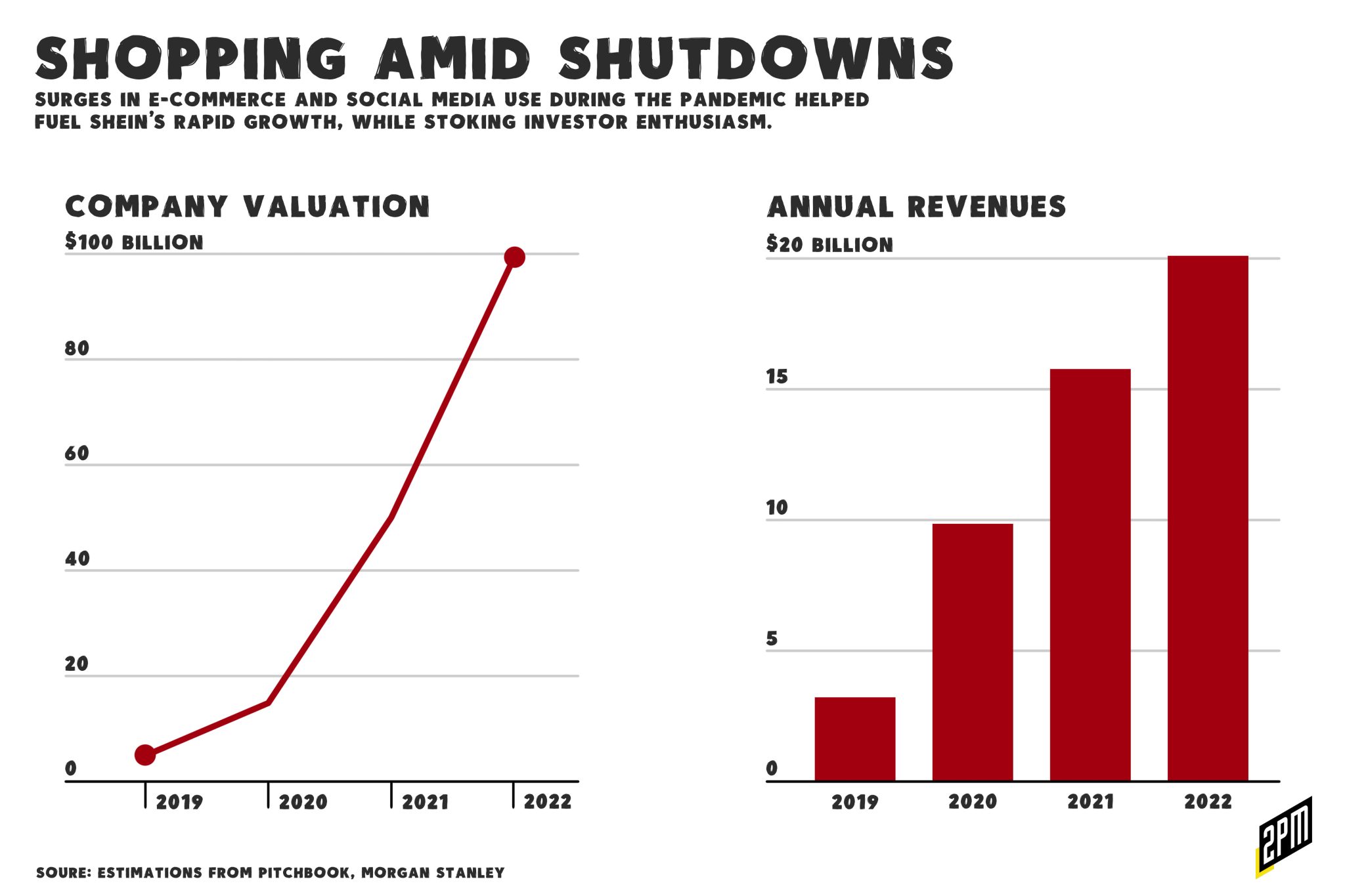

Just two years after this case was written, Zara is now looking upwards at an infant brand: Shein is Zara on steroids. And Gen Z loves it. Shein has become a favorite on TikTok, where users share hauls from the brand of $15 dresses, $10 shorts and $5 tops. The clothes are cheap and trendy, designed for one-time wears posted on social media and discarded. The concept is not new but with the trend toward sustainability, it was supposed to be going out of style. Instead, the idea is more powerful.

Shein’s scale is difficult to grasp. The operation is more secretive than most but what is evident is that we are more aware than ever of the consequences. There are very tangible negatives to fast-fashion and athleisure; plastics weren’t intended to be worn and discarded with impunity. Fortune wrote a deep-dive on Shein on May 31, laying bear the narrative:

Global investors, for whom it is increasingly fashionable to champion high standards on environmental, social, and governance (ESG) matters, are similarly smitten. They have pumped Shein’s valuation up to $100 billion, making it the world’s third most valuable startup behind ByteDance, the Chinese parent of TikTok, and Elon Musk’s SpaceX. Shein is now worth more than H&M and Inditex, Zara’s parent company, combined, according to Bloomberg.

But while Shein’s innovative business model might lower prices for consumers, watchdogs grumble that Shein has built its clothing empire on the back of cheap labor, knockoff goods, and A.I.-driven design software that encourages consumers to ditch old outfits at rates that are bad for the planet. Those complaints, along with a recent e-commerce slowdown, make the company’s continued dominance far from certain.

Fortune’s position that, in so many words: “Shein’s impact on the environment will eventually lead to its undoing” is faulty at best. Why? There is a cognitive dissonance in fast fashion’s target market. Can one save the planet while buying $13 dresses for Instagram? So far, fast fashion companies have only lost dominance when they’ve been replaced by faster companies that can regurgitate trends at lower prices. Whether Shein’s nefarious practices are lost on customers or willfully ignored doesn’t ultimately matter. Customers who are drawn to clothing because of their affordable price are typically not the same ones who will stop to ask why a piece of clothing costs so little. What does matter is the bottom-line evidence that faced with cheap options, young consumers will shop for fast fashion.

At play behind the rise of Shein is a combination of factors. Social media has accelerated the trend cycles of fashion. Sustainable fashion is prohibitively expensive and the shifting tides of consumerism have, for many, determined that fashion is not an investment, at least not in terms of trends. Consumers are often held responsible for “voting with their dollars” when it comes to encouraging corporations to be more sustainable but this has never been completely true. Customers will buy what is easily and affordably available, particularly when they’re young.

Shein itself is a black box. Little is made public about how it sources and manufactures its clothing but the numbers and price tags speak for themselves. The company has started speaking up about – of all things – its sustainability efforts. Vogue calls this greenwashing:

Each week, a shocking 15 million garments arrive at Kantamanto Market from countries in the Global North, decimating the local textiles industry there.

It hired a global head of ESG and recently announced a $50 million fund that will go toward offsetting its environmental impact and handling its waste problem. That is a $50 million drop in the bucket that will barely undo a stitch of what Shein has unleashed on the market of TikTok, Snapchat, Instagram, and Kardashian loyalists. This week, it received praise for partnering with the OR Foundation, which it will give $15 million over three years in order to combat clothing waste in Accra, Ghana, where many discarded clothing ends up.

It’s nothing more than a diversion from the reality of the impact on landfills. Shein calling out waste and donating funds to bring attention to the cause may be perceived as disingenuous. Luckily for them, H&M is doing something similar, committing $250 million alongside Lululemon on behalf of the new organization that succeeded Aii:

“What we’re trying to demonstrate is that this is the center of gravity for all of climate work and everyone from Textile Exchange to Fashion for Good to many others — that are working in lowering carbon and coming up with solutions and getting them to pilot — are all beneficiaries of this,” he said. “This is a collective ‘we.’ This is not giving it to Aii, and it’s not going to go into other climate work. This is creating a central pooled fund whereby we all can begin to look at a more consolidated approach as opposed to fragmentation of project work that’s not talking to each other and duplicating efforts.”

What will solve fashion’s Shein problem is not donations, public relations, or acknowledgements of wrong-doing. The more fruitful solution will be social media trending away from fast fashion and towards sustainability. But there’s no relying on Gen Z customers to fix this problem. It is time to accept that no well meaning customer can stop the retail machine desired by millions, as new trends come along and TikTok broadcasts them for all to emulate.

By The 2PM Team