快:H&M。更快Zara。最快Shein。这一进步改变了消费主义,加速了纺织品的生产,同时也损害了经济。Zara 打乱了 H&M 的阵脚,随后,Shein 又将两者赶下台。现在,H&M 开始进攻,试图重新夺回曾经的优势。

我们的希望是,重新挽回数以百万计被 Zara 和 Shein 抛弃的消费者。这一切都取决于两个相互竞争的理念:经济和环境影响。

快速时尚和运动休闲是有后果的;塑料制品并不是可以肆无忌惮地穿戴和丢弃的。

关于未来时尚的讨论充满了矛盾:年轻一代的购物者说他们想要保护环境。将这一理想与他们实际购买的商品相比较,你会发现他们 "拯救地球 "的集体理念中存在着裂痕。Z 世代通常被称为最具可持续发展意识和环保意识的消费群体。他们还推动了历史上最大的快速时尚公司 Shein 的崛起。相比之下,Zara 和 H&M 只是小零售商。哈佛商学院 2021 年的一份案例研究解释了 Zara 的母公司 Inditex 如何围绕供应链效率进行创新,以更快的速度生产出更符合潮流的产品。

Zara 是集团历史最悠久、规模最大的品牌,在 2018 年的销售额中约占 69%,即 180 亿欧元。Zara 成功的核心是基于反应迅速的供应链和快速商品周转的创新商业模式。Zara 在不到三周的时间内设计、生产并向商店交付新商品,从而能够不断更新产品系列,适应不断变化的顾客口味。

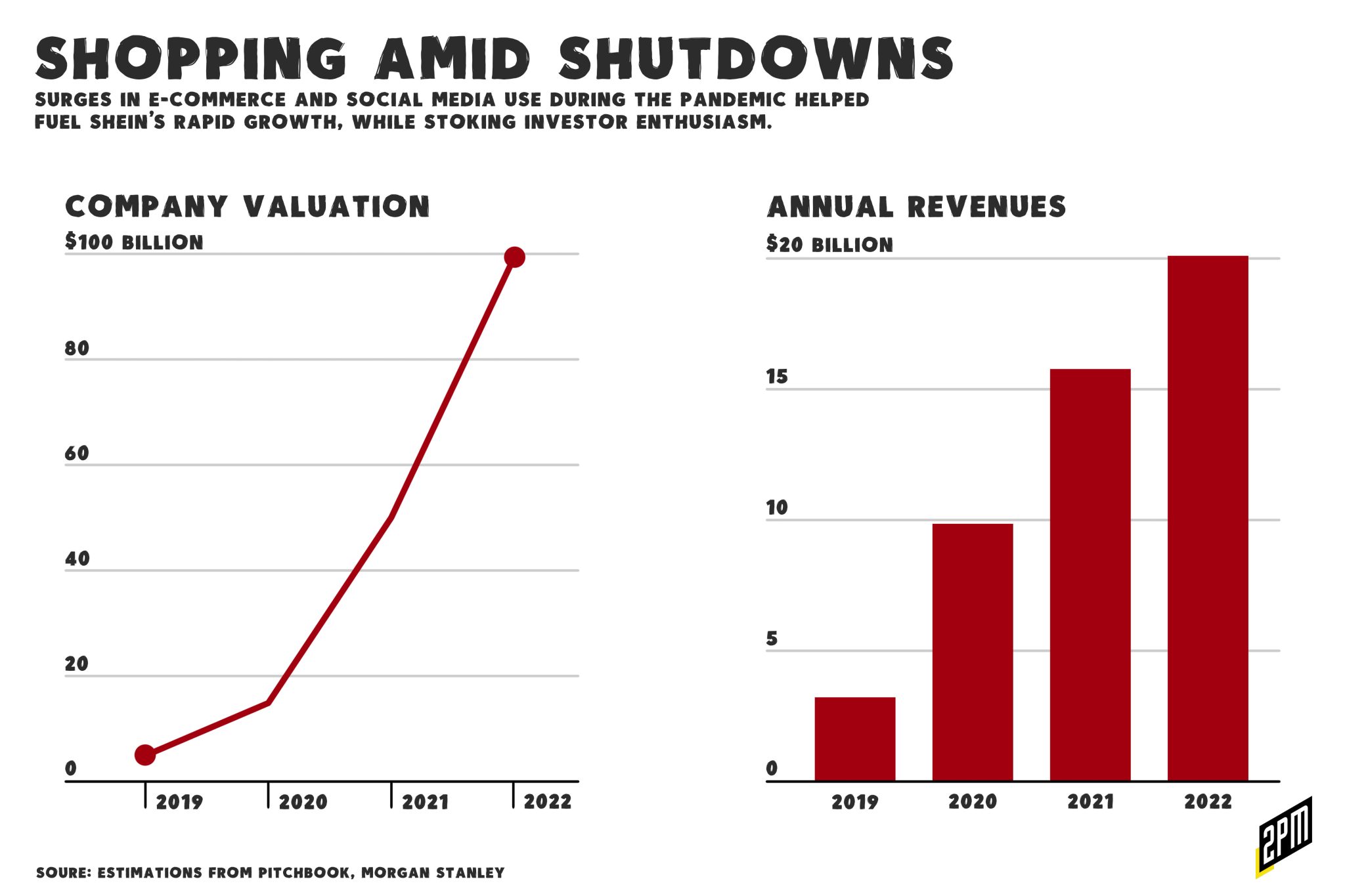

就在撰写本案例的两年后,Zara 现在又开始关注一个婴儿品牌:Shein 是打了类固醇的 Zara。Z 世代非常喜欢它。Shein已成为TikTok上的宠儿,用户们在那里分享从该品牌淘来的15美元连衣裙、10美元短裤和5美元上衣。这些衣服既便宜又时髦,专为一次性穿着而设计,在社交媒体上发布后就会被丢弃。这个概念并不新鲜,但在可持续发展的趋势下,它应该会过时。相反,这个想法却更有力量。

谢因的规模难以把握。该公司的运作比大多数公司都要隐秘,但显而易见的是,我们比以往任何时候都更清楚后果的严重性。快速时尚和运动休闲有非常明显的负面影响;塑料制品并不是用来随意穿戴和丢弃的。财富》杂志于5月31日撰文对Shein进行了深度报道,对其进行了叙述:

对全球投资者来说,倡导环境、社会和治理(ESG)方面的高标准越来越时髦,他们也同样为之倾倒。他们将 Shein 的估值抬高到 1000 亿美元,使其成为全球第三大最有价值的初创企业,仅次于字节跳动、TikTok 的中国母公司和埃隆-马斯克的 SpaceX。据彭博社报道,Shein 现在的价值超过了 H&M 和 Zara 母公司 Inditex 的总和。

尽管Shein创新的商业模式可能会降低消费者的价格,但观察家们抱怨说,Shein是在廉价劳动力、山寨商品和人工智能设计软件的支持下建立起自己的服装帝国的,这些软件鼓励消费者以对地球有害的速度抛弃旧服装。这些抱怨,再加上最近电子商务的放缓,使得该公司能否继续保持主导地位还很难说。

用《财富》杂志的话来说"Shein对环境的影响最终将导致其灭亡 "的说法充其量只是错误的。为什么?快速时尚的目标市场存在认知偏差。人们能在为 Instagram 购买 13 美元裙子的同时拯救地球吗?迄今为止,快时尚公司只是在被更快的公司取代后才失去了主导地位,这些公司能以更低的价格重复流行趋势。至于 Shein 的恶行是被顾客遗忘,还是被故意忽略,最终并不重要。因为价格实惠而被服装吸引的顾客,通常不会停下来问一件衣服为什么这么便宜。重要的是,底线证据表明,面对廉价的选择,年轻消费者会选择快速时尚。

Shein 的崛起是多种因素共同作用的结果。社交媒体加速了时尚的潮流周期。可持续时装价格昂贵,而消费主义浪潮的变化也让许多人认为时装不是一种投资,至少在潮流方面不是。在鼓励企业更加注重可持续发展的问题上,消费者经常被认为有责任 "用他们的钱投票",但这从来都不是完全正确的。顾客会购买容易买得起的东西,尤其是在他们年轻的时候。

Shein 本身就是一个黑盒子。关于它如何采购和生产服装的信息很少公开,但数字和价格标签却不言而喻。该公司已经开始公开其在可持续发展方面所做的努力。Vogue 将此称为 "洗绿":

每周都有令人震惊的 1500 万件服装从全球北方国家运抵坎塔曼托市场,使当地的纺织业遭受重创。

该公司聘请了一位全球环境、社会和治理主管,最近还宣布成立一个 5000 万美元的基金,用于抵消对环境的影响和处理废物问题。这不过是杯水车薪的 5000 万美元,对 Shein 在 TikTok、Snapchat、Instagram 和卡戴珊的忠实拥护者市场上所造成的影响来说,几乎是杯水车薪。本周,Shein 因与 OR 基金会合作而备受赞誉,该基金会将在三年内捐赠 1500 万美元,用于在加纳阿克拉解决服装浪费问题,那里是许多废弃服装的最终归宿。

这不过是在转移人们对垃圾填埋场的现实影响的注意力。Shein抨击浪费并捐献资金以引起人们对这一事业的关注可能会被认为是不真诚的。幸运的是,H&M 也在做类似的事情,它与 Lululemon 一起为接替Aii 的新组织捐款 2.5 亿美元:

"他说:"我们试图证明的是,这是所有气候工作的重心,从纺织品交易所到时尚公益组织,再到其他许多致力于降低碳排放、提出解决方案并将其付诸试点的组织,都是这一工作的受益者。"这是一个集体的'我们'。这不是把钱交给 Aii,也不会用于其他气候工作。这是在创建一个中央集合基金,让我们都能开始考虑一个更综合的方法,而不是分散的项目工作,彼此不交流,重复工作。

要解决时尚界的 Shein 问题,靠的不是捐款、公共关系或承认错误。更有效的解决办法是在社交媒体上掀起一股远离快速时尚、追求可持续发展的潮流。但是,不能依靠 Z 世代的顾客来解决这个问题。随着新潮流的出现和 TikTok 的传播,让所有人都能效仿,现在是时候接受这样的事实:任何好心的顾客都无法阻止数百万人所希望的零售机器。

由 2PM 团队提供