Быстрее: H&M. Быстрее: Zara. Быстрее всех: Shein. Эта прогрессия изменила потребительский стиль, ускорила производство текстиля и одновременно нанесла ущерб экономике. Zara нарушила работу H&M, а затем Shein вытеснила их обоих. Теперь H&M перешел в наступление, пытаясь вернуть себе былые преимущества.

Мы надеемся вернуть миллионы потребителей, которые ушли от Zara и Shein. Все сводится к осям x и y двух конкурирующих идей: экономики и воздействия на окружающую среду.

У фаст-фэшн и athleisure есть последствия; пластик не был предназначен для того, чтобы его безнаказанно носили и выбрасывали.

Разговоры о будущем моды - это сплошное противоречие: молодое поколение покупателей говорит, что хочет сохранить окружающую среду. Сопоставьте этот идеал с тем, что они покупают на самом деле, и вы увидите, что в их коллективной философии "спасения планеты" есть трещины. Представителей поколения Z часто называют наиболее сознательным и экологически ориентированным сегментом потребителей. Они также способствовали росту Shein, крупнейшей в истории компании быстрой моды. По сравнению с ними Zara и H&M были маленькими ритейлерами. В исследовании Гарвардской школы бизнеса 2021 года рассказывается о том, как Inditex, материнская компания Zara, внедряла инновации для повышения эффективности цепочки поставок, чтобы быстрее выпускать продукцию, которая в большей степени соответствовала тенденциям.

Zara - старейший и крупнейший бренд Группы, на долю которого приходится около 69 % продаж, или 18 млрд евро в 2018 году. В основе успеха Zara лежит инновационная бизнес-модель, основанная на очень оперативной цепочке поставок и быстрой оборачиваемости товаров. Zara разрабатывает, производит и доставляет новые товары в магазины менее чем за три недели, что позволяет ей постоянно обновлять свои коллекции и адаптироваться к меняющимся вкусам покупателей.

Всего через два года после написания этого дела Zara обращает свой взор на бренд для новорожденных: Shein - это Zara на стероидах. И поколение Z это любит. Shein стал фаворитом на TikTok, где пользователи делятся покупками платьев за 15 долларов, шорт за 10 долларов и топов за 5 долларов. Одежда дешевая и модная, рассчитанная на одноразовое ношение, которую выкладывают в социальные сети и выбрасывают. Концепция не нова, но с тенденцией к экологичности она должна была выйти из моды. Вместо этого идея стала еще более сильной.

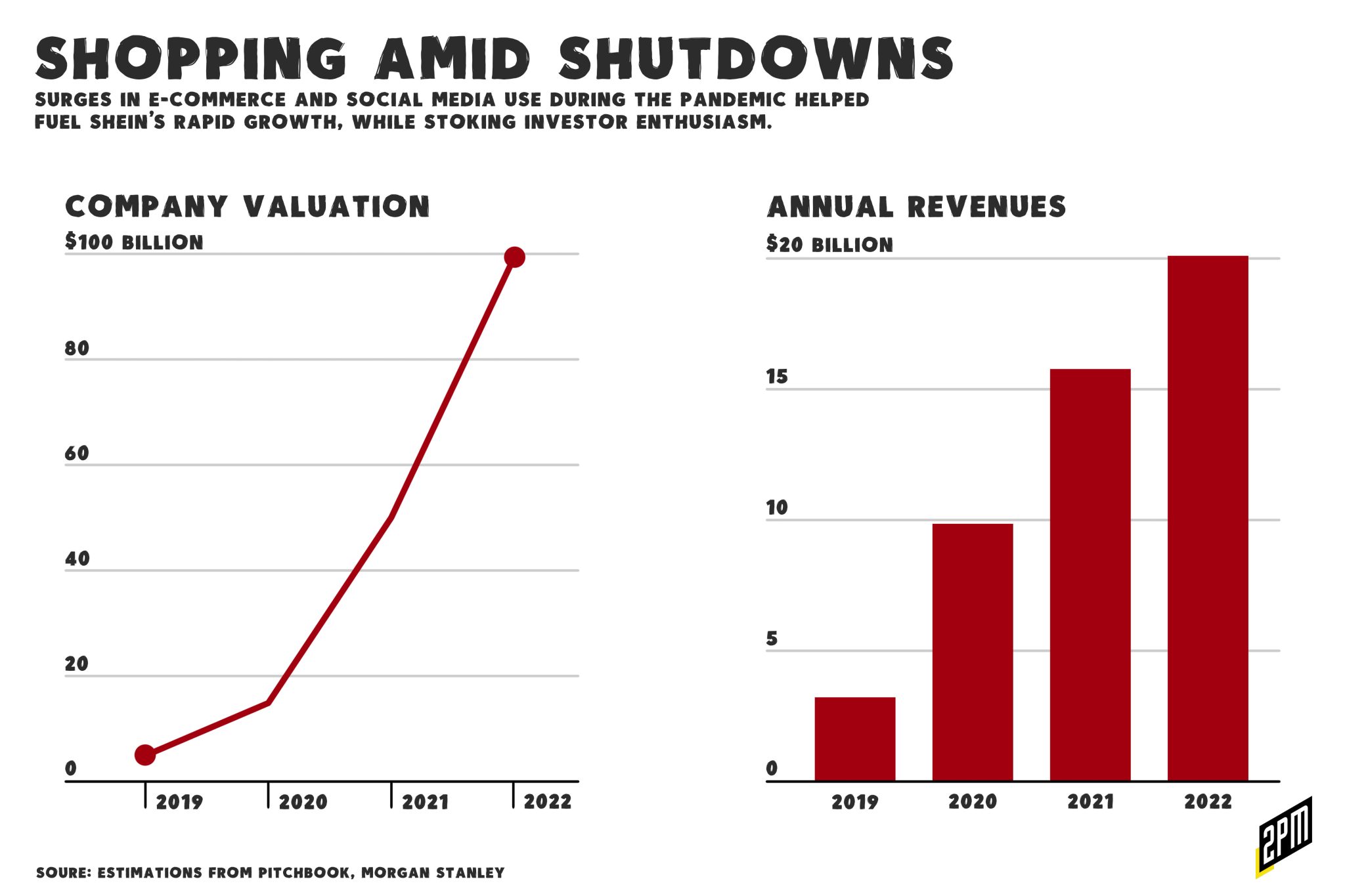

Масштабы Шейна трудно осознать. Эта операция более секретна, чем большинство других, но очевидно, что мы как никогда осознаем ее последствия. У фаст-фэшн и athleisure есть весьма ощутимые отрицательные стороны; пластик не был предназначен для того, чтобы его безнаказанно носили и выбрасывали. 31 мая Fortune написал глубокую статью о Шеине, в которой изложил суть дела:

Глобальные инвесторы, для которых становится все более модным отстаивать высокие стандарты в области экологии, социальной сферы и управления (ESG), также поражены. Они подняли стоимость Shein до 100 миллиардов долларов, сделав ее третьим по стоимости стартапом в мире после ByteDance, китайского производителя TikTok, и SpaceX Элона Маска. По данным Bloomberg, Shein сейчас стоит больше, чем H&M и Inditex, материнская компания Zara, вместе взятые.

Но хотя инновационная бизнес-модель Shein может снизить цены для потребителей, наблюдатели ворчат, что Shein построила свою империю одежды на дешевой рабочей силе, поддельных товарах и программном обеспечении для дизайна, управляемом А.И., которое побуждает потребителей выбрасывать старые наряды с вредными для планеты темпами. Эти жалобы, а также недавнее замедление темпов роста электронной коммерции делают дальнейшее господство компании далеко не однозначным.

Позиция Fortune, согласно которой, выражаясь многословно: "воздействие компании Shein на окружающую среду в конечном итоге приведет к ее гибели", в лучшем случае ошибочна. Почему? У целевого рынка быстрой моды существует когнитивный диссонанс. Можно ли спасти планету, покупая платья за 13 долларов для Instagram? До сих пор компании быстрой моды теряли свое господство только тогда, когда им на смену приходили более быстрые компании, способные повторять тренды по более низким ценам. Неважно, не видят ли покупатели гнусной практики Shein или намеренно игнорируют ее, в конечном итоге это не имеет значения. Покупатели, которых привлекает одежда по доступной цене, как правило, не те, кто останавливается, чтобы спросить, почему вещь стоит так мало. Важно лишь то, что, сталкиваясь с дешевыми вариантами, молодые потребители выбирают быструю моду.

За подъемом Shein стоит сочетание нескольких факторов. Социальные сети ускорили циклы модных тенденций. Экологически чистая мода стоит непомерно дорого, а меняющиеся приливы и отливы консьюмеризма для многих определили, что мода - это не инвестиции, по крайней мере, не в плане трендов. Потребителей часто считают ответственными за то, что они "голосуют своими долларами", когда речь идет о том, чтобы побудить корпорации быть более устойчивыми, но это никогда не было полной правдой. Покупатели будут покупать то, что легко и доступно, особенно в молодости.

Сама компания Shein - это черный ящик. О том, как она добывает и производит свою одежду, мало что известно, но цифры и ценники говорят сами за себя. Компания начала рассказывать о своих усилиях по защите окружающей среды. Vogue называет это "зеленым промыванием":

Каждую неделю на рынок Кантаманто поступает 15 миллионов единиц одежды из стран Глобального Севера, что приводит в упадок местную текстильную промышленность.

Компания наняла главу глобального отдела ESG и недавно объявила о создании фонда в размере 50 миллионов долларов, который будет направлен на компенсацию воздействия на окружающую среду и решение проблемы отходов. Это капля в море на 50 миллионов долларов, которая едва ли сможет исправить хоть что-то из того, что Шейн выплеснул на рынок TikTok, Snapchat, Instagram и поклонников Кардашьян. На этой неделе компания получила похвалу за партнерство с фондом OR Foundation, которому она выделит 15 миллионов долларов в течение трех лет на борьбу с отходами одежды в Аккре, Гана, где в итоге оказывается много выброшенной одежды.

Это не более чем отвлечение от реальности воздействия на свалки. То, что Шеин называет отходы отходами и жертвует средства, чтобы привлечь внимание к этой проблеме, может быть воспринято как неискренность. К счастью для них, H&M делает нечто подобное, выделив 250 миллионов долларов вместе с Lululemon в пользу новой организации, которая стала преемницей Aii:

"Мы пытаемся показать, что это центр притяжения для всей климатической работы, и все - от Textile Exchange до Fashion for Good и многих других, - кто работает над снижением выбросов углерода, придумывает решения и внедряет их в производство, - все являются бенефициарами этого", - сказал он. "Это коллективное "мы". Это не передача средств Aii, и они не пойдут на другие климатические работы. Это создание центрального фонда, с помощью которого мы все сможем начать рассматривать более консолидированный подход в противовес фрагментации проектов, которые не взаимодействуют друг с другом и дублируют усилия".

Проблему Шейна в моде решат не пожертвования, не связи с общественностью и не признание вины. Более плодотворным решением будет отказ социальных сетей от быстрой моды в пользу экологичности. Но нельзя полагаться на покупателей поколения Z, чтобы решить эту проблему. Пора признать, что никакие благонамеренные покупатели не смогут остановить машину розничной торговли, которую хотят видеть миллионы, поскольку появляются новые тенденции, а TikTok транслирует их для подражания.

Команда 2PM