तेज़: एच एंड एम। उससे भी तेज़: ज़ारा। सबसे तेज़: शीन। यह एक ऐसी प्रगति है जिसने उपभोक्तावाद को बदला है, कपड़ा उत्पादन को गति दी है, और ऐसा करते हुए अर्थव्यवस्था को भी नुकसान पहुँचाया है। ज़ारा ने एच एंड एम को तहस-नहस कर दिया और फिर शीन ने उन दोनों को बेदखल कर दिया। अब, एच एंड एम अपनी पुरानी बढ़त वापस पाने के लिए आक्रामक हो गया है।

उम्मीद है कि ज़ारा और शीन की राह पर चल पड़े लाखों उपभोक्ताओं को वापस लाया जा सकेगा। यह सब दो प्रतिस्पर्धी विचारों के x और y अक्षों पर निर्भर करता है: आर्थिक और पर्यावरणीय प्रभाव।

फास्ट-फैशन और एथलीजर के अपने परिणाम हैं; प्लास्टिक को पहनने और बेखौफ फेंक देने के लिए नहीं बनाया गया है।

फ़ैशन के भविष्य को लेकर चल रही चर्चाएँ एकदम विरोधाभासी हैं: खरीदारों की एक युवा पीढ़ी कहती है कि वे पर्यावरण को संरक्षित करना चाहते हैं। इस आदर्श को उनकी वास्तविक खरीदारी के साथ जोड़कर देखें, तो आप पाएँगे कि उनके सामूहिक "ग्रह बचाओ" के दर्शन में खामियाँ हैं। जेन ज़ेड को अक्सर सबसे स्थायी रूप से जागरूक, पर्यावरण के प्रति जागरूक उपभोक्ता वर्ग के रूप में जाना जाता है। वे इतिहास की सबसे बड़ी फ़ास्ट फ़ैशन कंपनी, शीन के उदय को भी बढ़ावा दे रहे हैं। इसकी तुलना में ज़ारा और एच एंड एम छोटे खुदरा विक्रेता थे। 2021 के हार्वर्ड बिज़नेस स्कूल के एक केस स्टडी में बताया गया है कि कैसे ज़ारा की मूल कंपनी, इंडिटेक्स ने आपूर्ति श्रृंखला दक्षता के इर्द-गिर्द नवाचार किया ताकि ऐसे तेज़ उत्पाद तैयार किए जा सकें जो रुझानों के ज़्यादा अनुरूप हों।

ज़ारा समूह का सबसे पुराना और सबसे बड़ा ब्रांड था, जिसकी 2018 में लगभग 69% बिक्री, यानी €18 बिलियन थी। ज़ारा की सफलता का मूल एक बेहद संवेदनशील आपूर्ति श्रृंखला और तेज़ी से माल की आपूर्ति पर आधारित एक अभिनव व्यावसायिक मॉडल था। ज़ारा ने तीन हफ़्तों से भी कम समय में नए उत्पादों को डिज़ाइन, निर्मित और स्टोर्स तक पहुँचाया, जिससे उसे अपने संग्रह को लगातार अपडेट करने और ग्राहकों की बदलती पसंद के अनुसार ढलने में मदद मिली।

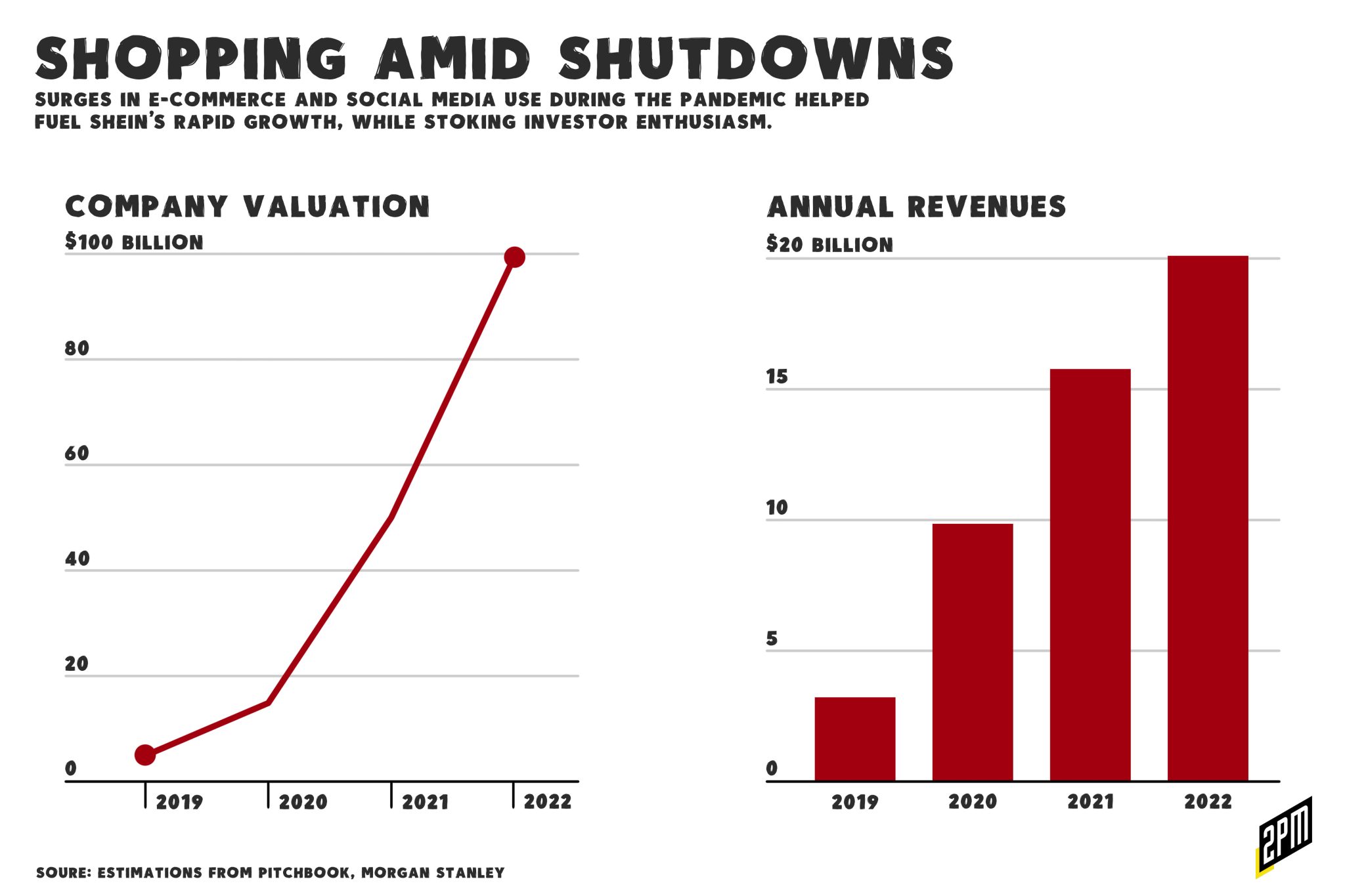

इस मामले के लिखे जाने के सिर्फ़ दो साल बाद, ज़ारा अब एक नए ब्रांड की ओर देख रही है: शीन, ज़ारा का स्टेरॉयड है। और जेनरेशन ज़ेड इसे पसंद करती है। शीन टिकटॉक पर एक पसंदीदा ब्रांड बन गया है, जहाँ यूज़र्स इस ब्रांड के 15 डॉलर के ड्रेस, 10 डॉलर के शॉर्ट्स और 5 डॉलर के टॉप शेयर करते हैं। ये कपड़े सस्ते और ट्रेंडी हैं, जिन्हें सिर्फ़ एक बार पहनने के लिए डिज़ाइन किया गया है, सोशल मीडिया पर पोस्ट करके फेंक दिया जाता है। यह कॉन्सेप्ट नया नहीं है, लेकिन सस्टेनेबिलिटी की ओर बढ़ते रुझान के साथ, इसे चलन से बाहर होना चाहिए था। लेकिन, यह आइडिया ज़्यादा प्रभावशाली है।

शीन के पैमाने को समझना मुश्किल है। यह काम ज़्यादातर कंपनियों की तुलना में ज़्यादा गोपनीय है, लेकिन यह साफ़ है कि हम इसके परिणामों के बारे में पहले से कहीं ज़्यादा जागरूक हैं। फ़ास्ट-फ़ैशन और एथलीज़र के कुछ ठोस नकारात्मक पहलू भी हैं; प्लास्टिक को बेख़ौफ़ होकर पहनने और फेंकने के लिए नहीं बनाया गया था। फ़ॉर्च्यून ने 31 मई को शीन पर एक गहन लेख लिखा, जिसमें कहानी को स्पष्ट किया गया:

वैश्विक निवेशक, जिनके लिए पर्यावरण, सामाजिक और शासन (ईएसजी) मामलों में उच्च मानकों को बढ़ावा देना तेज़ी से प्रचलन में है, भी इसी तरह प्रभावित हैं। उन्होंने शीन का मूल्यांकन $100 बिलियन तक बढ़ा दिया है, जिससे यह टिकटॉक की चीनी मूल कंपनी बाइटडांस और एलन मस्क की स्पेसएक्स के बाद दुनिया का तीसरा सबसे मूल्यवान स्टार्टअप बन गया है। ब्लूमबर्ग के अनुसार, शीन की कीमत अब एचएंडएम और ज़ारा की मूल कंपनी इंडिटेक्स की संयुक्त कीमत से भी ज़्यादा है।

हालाँकि शीन का अभिनव व्यावसायिक मॉडल उपभोक्ताओं के लिए कीमतें कम कर सकता है, लेकिन नियामकों का कहना है कि शीन ने सस्ते श्रम, नकली सामान और कृत्रिम बुद्धिमत्ता (एआई) से प्रेरित डिज़ाइन सॉफ़्टवेयर के दम पर अपना परिधान साम्राज्य खड़ा किया है, जो उपभोक्ताओं को पुराने कपड़े त्यागने के लिए प्रोत्साहित करता है और ऐसी कीमतों पर बेचता है जो दुनिया के लिए हानिकारक हैं। ये शिकायतें, और हाल ही में ई-कॉमर्स में आई मंदी, कंपनी के प्रभुत्व को और भी अनिश्चित बना देती हैं।

फॉर्च्यून का यह कहना कि, कई शब्दों में कहें तो: "शीन का पर्यावरण पर प्रभाव अंततः उसे बर्बाद कर देगा," पूरी तरह से गलत है। क्यों? फ़ास्ट फ़ैशन के लक्षित बाज़ार में एक संज्ञानात्मक असंगति है। क्या कोई इंस्टाग्राम के लिए $13 के कपड़े खरीदकर ग्रह को बचा सकता है? अब तक, फ़ास्ट फ़ैशन कंपनियों ने अपना प्रभुत्व तभी खोया है जब उनकी जगह तेज़ कंपनियों ने ले ली है जो कम दामों पर नए ट्रेंड्स ला सकती हैं। चाहे शीन की नापाक हरकतें ग्राहकों को समझ न आएँ या जानबूझकर नज़रअंदाज़ कर दी जाएँ, अंततः इससे कोई फ़र्क़ नहीं पड़ता। जो ग्राहक कपड़ों की सस्ती कीमतों के कारण उनकी ओर आकर्षित होते हैं, वे आमतौर पर वही नहीं होते जो यह पूछने के लिए रुकेंगे कि किसी कपड़े की कीमत इतनी कम क्यों है। जो मायने रखता है वह यह है कि सस्ते विकल्पों के सामने, युवा उपभोक्ता फ़ास्ट फ़ैशन की खरीदारी करेंगे।

शीन के उदय के पीछे कई कारक काम कर रहे हैं। सोशल मीडिया ने फ़ैशन के ट्रेंड चक्र को तेज़ कर दिया है। टिकाऊ फ़ैशन बेहद महँगा है और उपभोक्तावाद के बदलते चलन ने, कई लोगों के लिए, यह तय कर दिया है कि फ़ैशन कोई निवेश नहीं है, कम से कम ट्रेंड के लिहाज़ से तो नहीं। जब कंपनियों को ज़्यादा टिकाऊ बनने के लिए प्रोत्साहित करने की बात आती है, तो अक्सर उपभोक्ताओं को "अपने पैसे से वोट देने" के लिए ज़िम्मेदार ठहराया जाता है, लेकिन यह कभी भी पूरी तरह सच नहीं रहा है। ग्राहक वही खरीदेंगे जो आसानी से और किफ़ायती तौर पर उपलब्ध हो, खासकर जब वे युवा हों।

शीन खुद एक ब्लैक बॉक्स है। यह अपने कपड़ों की सोर्सिंग और निर्माण कैसे करता है, इसके बारे में बहुत कम जानकारी सार्वजनिक की जाती है, लेकिन आंकड़े और कीमतें खुद ही सब कुछ बयां कर देती हैं। कंपनी ने अपने टिकाऊपन प्रयासों के बारे में खुलकर बोलना शुरू कर दिया है। वोग इसे ग्रीनवाशिंग कहता है:

प्रत्येक सप्ताह, वैश्विक उत्तरी देशों से कांटामांटो बाजार में 15 मिलियन वस्त्र आते हैं, जिससे वहां का स्थानीय वस्त्र उद्योग नष्ट हो जाता है।

इसने ESG के एक वैश्विक प्रमुख को नियुक्त किया है और हाल ही में 50 मिलियन डॉलर के फंड की घोषणा की है जो इसके पर्यावरणीय प्रभाव को कम करने और कचरे की समस्या से निपटने के लिए इस्तेमाल किया जाएगा। यह 50 मिलियन डॉलर की एक बूंद के बराबर है जो टिकटॉक, स्नैपचैट, इंस्टाग्राम और कार्दशियन के वफादारों के बाज़ार पर शीन द्वारा किए गए कहर को कम नहीं कर पाएगा। इस हफ़्ते, इसे OR फ़ाउंडेशन के साथ साझेदारी के लिए प्रशंसा मिली, जिसे यह अकरा, घाना में कपड़ों के कचरे से निपटने के लिए तीन वर्षों में 15 मिलियन डॉलर देगा, जहाँ बहुत सारे बेकार कपड़े फेंके जाते हैं।

यह लैंडफिल पर पड़ने वाले प्रभाव की वास्तविकता से ध्यान भटकाने के अलावा और कुछ नहीं है। शीन द्वारा कचरे को उजागर करना और इस मुद्दे पर ध्यान आकर्षित करने के लिए धन दान करना कपटपूर्ण माना जा सकता है। सौभाग्य से, एच एंड एम भी कुछ ऐसा ही कर रहा है, और एआईआई के उत्तराधिकारी नए संगठन की ओर से लुलुलेमन के साथ मिलकर 250 मिलियन डॉलर देने का वादा कर रहा है।

उन्होंने कहा, "हम यह दर्शाने की कोशिश कर रहे हैं कि यह जलवायु परिवर्तन से जुड़े सभी कार्यों का केंद्रबिंदु है और टेक्सटाइल एक्सचेंज से लेकर फ़ैशन फ़ॉर गुड और कई अन्य सभी संगठन, जो कार्बन उत्सर्जन कम करने, समाधान ढूंढने और उन्हें पायलट प्रोजेक्ट में लाने के लिए काम कर रहे हैं, इसके सभी लाभार्थी हैं।" "यह एक सामूहिक 'हम' है। यह एआई को नहीं दिया जा रहा है, और न ही यह अन्य जलवायु कार्यों में जाएगा। यह एक केंद्रीय निधि का निर्माण कर रहा है जिससे हम सभी एक अधिक समेकित दृष्टिकोण अपना सकते हैं, बजाय परियोजना कार्य के विखंडन के, जो एक-दूसरे से बात नहीं करता और प्रयासों को दोहराता है।"

फैशन की शीन समस्या का समाधान दान, जनसंपर्क या गलत कामों की स्वीकृति से नहीं होगा। ज़्यादा कारगर समाधान सोशल मीडिया का तेज़ फ़ैशन से दूर होकर स्थिरता की ओर रुझान बढ़ाना होगा। लेकिन इस समस्या के समाधान के लिए जेनरेशन ज़ेड ग्राहकों पर निर्भर रहना उचित नहीं है। अब यह स्वीकार करने का समय आ गया है कि कोई भी नेकदिल ग्राहक लाखों लोगों की पसंदीदा रिटेल मशीन को नहीं रोक सकता, क्योंकि नए ट्रेंड आते रहते हैं और टिकटॉक उन्हें सभी के अनुकरण के लिए प्रसारित करता है।

2PM टीम द्वारा