This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.

Memo: On DTC Ideas Taking Shape

Deep generalism is at the core of how 2PM curates and publishes. Deep generalists excel in multiple fields and are able to identify connections between them. They are capable of analysis and adept at information synthesis. A 2018 report by Harvard Business Review stated it best:

One view is that the key to creative breakthroughs is being able to combine or leverage different areas of expertise. After all, every innovation somehow recombines or reimagines things that already exist. Many studies have found that the best ideas emerge from combining insights from fields that don’t seem connected. [14]

There has been tremendous change over the past months. While some of these changes seemingly happened overnight, many were long in the making. With Monday letters, member briefs, and weekly reports written over four years: 2PM has prided itself on publishing forward-thinking analyses, principles, and ideas. These essays were synthesized from many of the same reports, articles, white papers, and features that are included in the thrice-weekly letters that have published nearly 600 times since the newsletter’s start.

Since the beginning of 2020: eCommerce adoption has doubled, we’ve come to terms with our condition of over-retail, malls are shuttering, Hollywood has gone direct, DTC brands have found a second life, acquisition costs have fallen, total addressable market has grown, the American consumer has bifurcated, and The Law of Linear Commerce has become a prevailing strategy, and Generation Z’s tools of the trade have taken the spotlight.

Here are ten ideas that are now taking shape.

The Law of Linear Commerce

Linear Commerce is the prioritization of audience. Product manufacturers typically seek to outsource demand generation. Brands, that are ahead of the curve, emphasize their audience’s depth and engagement. Likewise, digital media publishers that follow linear commerce principles prioritize organic and loyal audience growth over SEO or PPC-driven commodity clicks.

No. 333: Food52 and Linear Commerce

The most viable companies across the digital ecosystem will share a common trait: established, organic audiences. Content and community are core to that outcome. For the well-executed linear commerce brands, retention rates will be high and CAC will be low. The road map is there for the brands looking for a sustainable advantage and improved optionality. Perhaps, the public and private markets will reward more of them. [1]

No. 314: On Linear Commerce

DTC linear commerce concepts are akin to those fabled pro shops at Augusta National. And for challenger brands looking toward sustainability, there is a lot to learn from these examples. Audience-driven businesses have figured out how to monetize their visitors by providing value that captures attention. The alternative is paying the audience to show up at your party – a cost that is rising by the year. [2]

The Bifurcation of the American Consumer

Per capita, America is over-retailed; it always has been. But for nearly 60 years of suburban retail expansion, it seemed as though the industry would never contract. According to Randal Konik, an analyst with Jefferies: “There are about 1,350 enclosed malls in the United States but only 200 to 400 are needed.” But while retail stores shutter, sales are expected to grow 3.5% to $3.7 trillion. According to reports by UBS, it may take ten years to reach the equilibrium (1,350 to 200). The investment bank forecasts 75,000 additional stores closing in that time.

No. 327: The Gilded Age 2.0

More closures are to come. Of them: GAP and L Brands will accelerate closures, further diminishing middle class retail. Not only are we witnessing a polarization of American wealth at a dizzying pace, it is now reflecting in retail real estate. The institutions for the affluent have remained steady, in some cases contributing to a growing retail sector. The institutions for the economically-distressed are also doing quite well. Historically, off-price and luxury retail were at the periphery. If these trends continue, these two cohorts may become the collective majority. [3]

America and Over-retail

The original vision for the American mall was not the suburban dwelling that you recognize today. In Gruen’s opinion, today’s typical mall would promote social isolation rather than a community sensation that it was designed for. In fact, Gruen was a proponent of walkability. An Austrian by birth, he opposed America’s reliance on cars.

His designs would later be amended, however. Gone were the multifunctional social centers – an emblem of urban lifestyles and walkability. The shopping centers that resulted over a period between 1970 – 2000 were diametrically opposed to Gruen’s initial vision for them.

No. 319: Mall Retail and 1954

Shortly after this Supreme Court decision [Brown vs. Board of Education], Eisenhower enacted the “Accelerated Depreciation” (AD) program. This allowed the owners of commercial real estate developments to deduct building costs from their tax burdens. This new form of tax deduction enabled builders to extract wealth from their developments 10x faster than the year before. Thomas Hanchett’s “U.S. Tax Policy and the Shopping-Center Boom of the 1950’s and 1960’s” notes that there was one regional mall in 1953. No less than 25 were approved, immediately after this decision in 1954. America went from one mall to 25 in one year. [4]

Between 1955 and 1975, shopping mall development exploded. Though, development was no longer tied to demand. Many were built as extractable retail assets only to be flipped for massive profits. This meant that development was no longer tied to population growth.

For more: Ep. 008 with Derek Thompson of The Atlantic. In this episode, we discuss the future of cities and the changes to come.

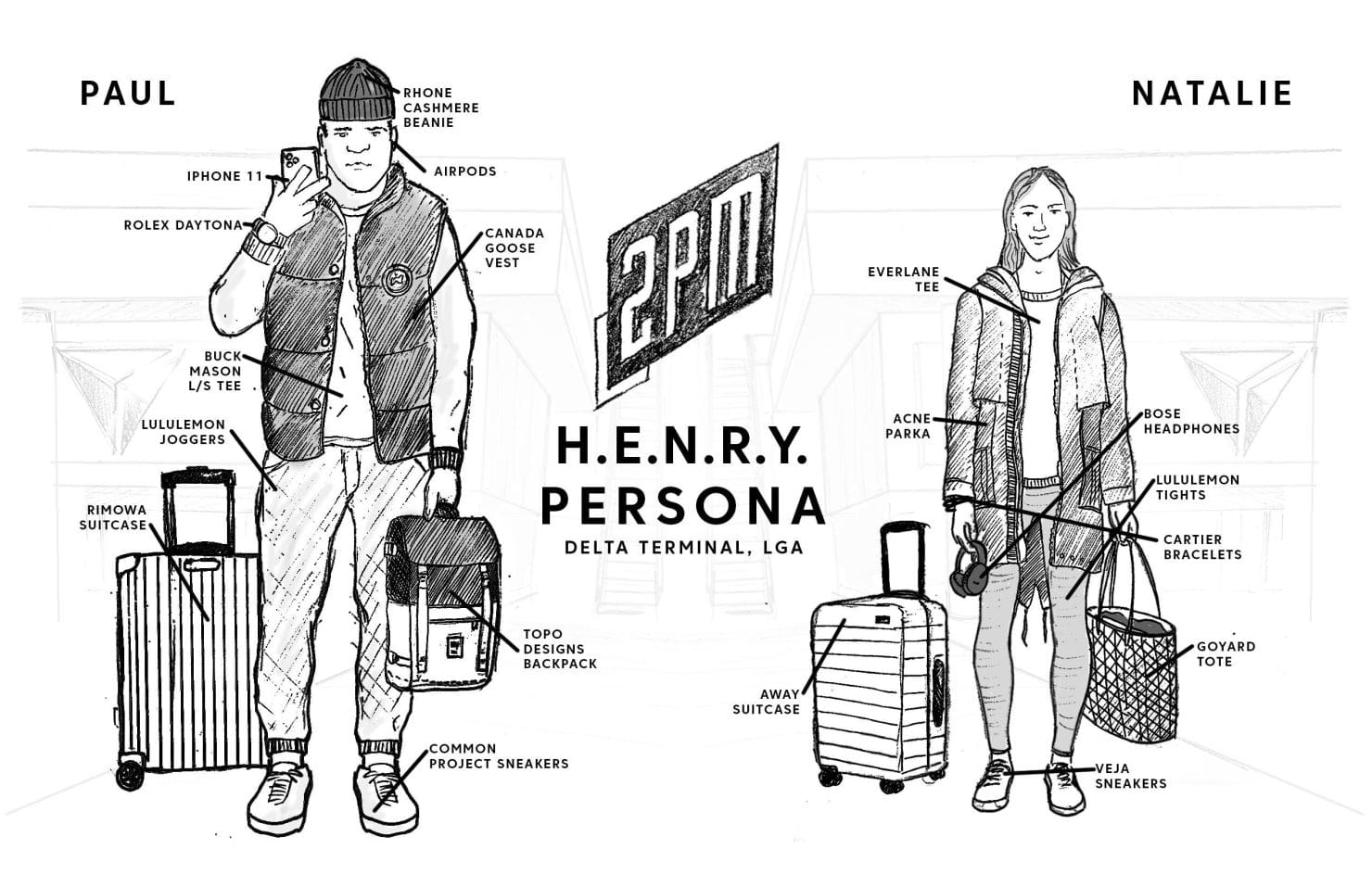

HENRY is equipped to hold steady

Successful brands and services have accounted for consumer bifurcation by maintaining price integrity and adjusting their total addressable market (TAM) to reflect a growing HENRY cohort that is adding to the population of luxury consumers. Short for high earners, not rich yet, HENRY is a designator that will influence TAM for many luxury manufacturers.

Member Brief: Regarding HENRY

The HENRYs are advancers, not necessarily those who have cleared the wealth bar to America’s elite class. In fact, many are working to leave the middle-class as if it’s a blemish on their personal ambitions. In this way, the term is more inclusive than the yuppie moniker of yesteryear. It’s also a symptom of our current economy, one where the cost of living can begin to erode long-term investments like real estate, money market funds, or other equities. Unlike the traditional middle-class, HENRYs have the inclination to believe that they are on the path to the liquidity. A liquidity and safety net that is necessary for investing in long-term assets. HENRY is a transitional cohort, not a class. A cohort that can no longer be ignored. [5]

Gen Z Arbitrage Steadies eCom Penetration

In America, Generation Z is awaiting the opportunity to buy with the frequency of Millennials and Generation X. The data suggests that their consumer activity will trump that of previous generations. While Millennials prefer DTC brands by a margin of just 4% over traditional retailers, Generation Z prefers these online-born brands to their legacy counterparts by over 40-45%.

No. 330: Gen Z Arbitrage

From time to time, there are technological and economic advantages that lift the brands that are prepared for the moment. For direct to consumer brands, a category of brands that Gen Z prefers over traditional retail, there is an opportunity to shorten the marketing funnel by appealing to a generation of consumers that have been written off by the incumbents in retail. Traditional brands are marketing to the parents of America’s youth rather than directly communicating to a demographic that could benefit them. The data suggests that as Apple Pay’s adoption rates continue to improve, Gen Z will become the primary consumers of the goods that have, so far, been marketed to Millennials and Gen X members. [6]

Live Streaming + Headless Commerce

Pioneered by Taobao and introduced to America through companies like ShopShops, live streaming is due to become the next great acquisition channel. It’s an amalgam of television’s push and social media’s pull. And though native platforms have risen to the challenge, it’s Instagram that stands to benefit. On the livestream-friendly platform, media companies and brands are due to to test influencer and media partnerships before committing to cross-border commerce. A growth tactic that helped MVMT grow to nearly $100 million + in annual revenue. Thus far, Instagram is the only platform with the capacity and the architecture for experimentation.

Member Brief: Headless Commerce

By reconsidering their commerce architecture, brands can manufacture experiences that meet the sociological as well as the consumer needs of the consumer. Headless commerce emphasizes community and it enables creators and brands to build a service funnel. This evolution of online retail gives brands control over their consumer experience, allowing depth of identity and relationship. By allowing creators to build end-to-end solutions, headless commerce may change the definition of customer acquisition altogether. This means more predictability and sustainable growth for media creators or brands willing to take the chance on owning their commerce outcomes. [7]

No. 304: In-App Audiences

Gaming platforms like Epic Games‘ Fortnite and PUBG have captivated audiences while storing their payment methods for ease of purchase. And services like Netflix and Spotify are learning that they can do the same. The monetization of audiences through innovative, exclusive partnerships will continue to build a foundation for how media companies address a metaverse-driven economy. By reclassifying app downloads as the beginning of a sales funnel (rather than its end), digital content communities can reframe the value of their content. [8]

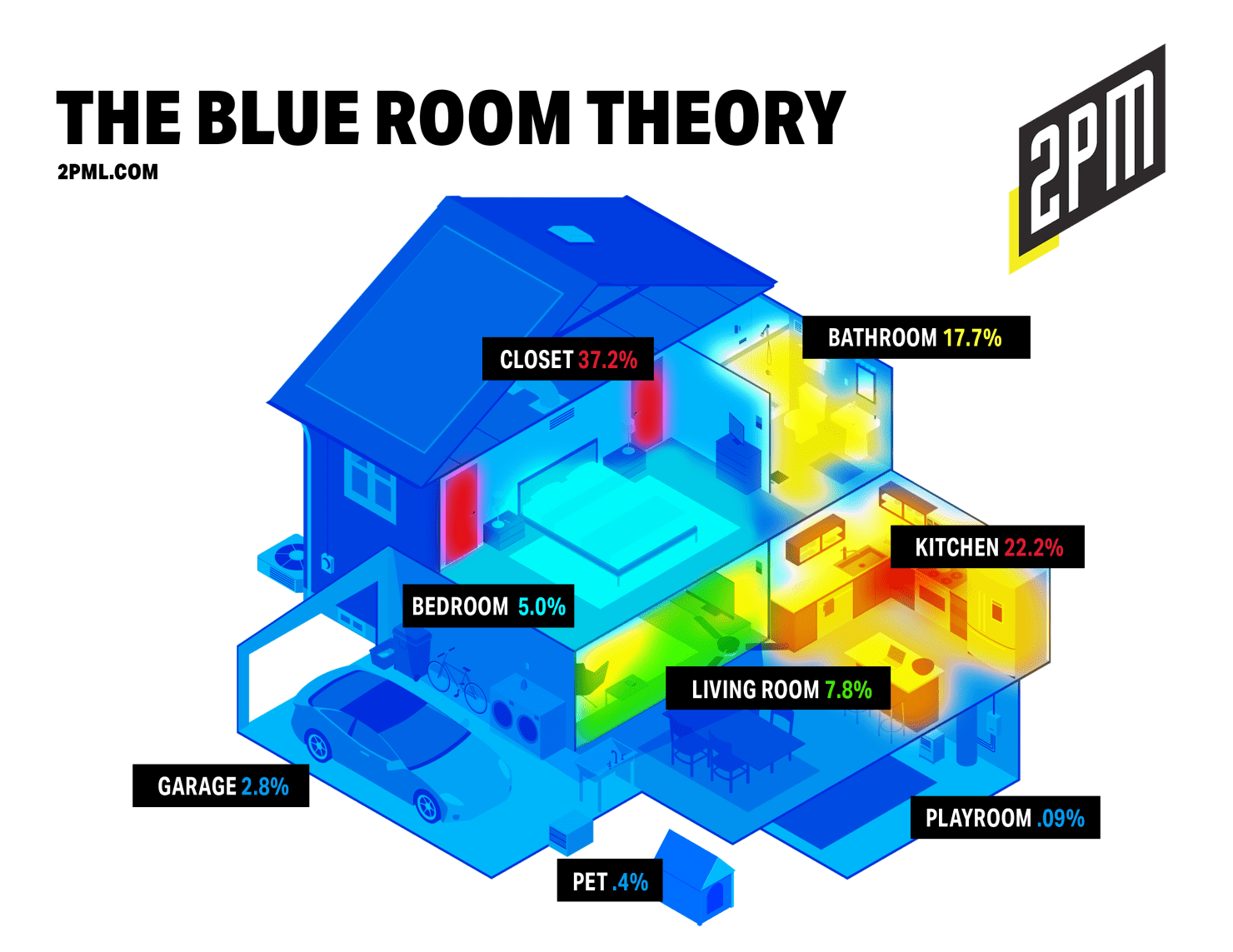

New Zones

The Blue Room Theory serves as a more useful interpretation of DTC brand density. It identifies opportunity zones throughout the home rather than by category. As (1) millennial home ownership continues to rise and (2) as DTC brands grow in preference vs. traditional counterparts and (3) as HENRY-esque [4] millennials begin to leave major urban centers for second-tier metropolitan areas: each 1,800+ square foot home represents a new canvas . Of the 729 growing, private companies that we studied, the vast majority were concentrated in three areas of the home: the closet, the kitchen, and the bathroom.

Member Brief: The Blue Room Theory

The Blue Room Theory is a new framework for product launch, early traction, and hyper-growth in consumer retail. It relies on a basic understanding of Red Ocean vs. Blue Ocean strategies. It’s here that Jen Rubio and Steph Korey made a wonderful key decision, very early on. Rather than view their product through the lens of category, they positioned specific real estate as the constraint. Away didn’t market their products in the context of storage capacity or durable plastics. Rather, they focused on owning a domain: the airport. [9]

Modern Luxury Holds Steady

With eCommerce at less than 11% of all retail sales in America, eCommerce continues to skew towards wealthier American. Until that domestic eCommerce figure grows, online retail’s adoption will continue to benefit the brands, services, and platforms appeal to the upper-middle class and beyond. This is reflected heavily by the growth of companies like Peloton, Equinox, SoulCycle, and the boom of meditation-based hardware. Additionally, the gig economy continues to thrive. Last mile workers have taken the form of a servant class, serving the upper-class. Time is the ultimate luxury, you know.

Member Brief: The Modern Luxury Thesis

The DTC retailers with the most promise to grow throughout this period of economic uncertainty can be broken down into two distinct groups: (1) off-price retail and (2) modern luxury. These two groups can operate independently of a dwindling middle class. Both nos. 1 and 2 are less likely to spend disproportionately on customer acquisition as the consumers in each of the respective wealth class tend to be more receptive as consumers. While CAC continues to rise on platforms like Facebook, this can be disproportionately attributed to increased competition for the attention of the a dwindling middle-class consumer cohort. [10]

Streaming and Bundles

The next twelve months will be pivotal in determining the viability of each of more than a dozen SVOD brands but one thing is apparent, streaming services are drilling down on their strengths. For Walt Disney Corporation, this means the ownership and operation of valuable intellectual property. For Netflix, Showtime, HBO, and others: this means adopting other mediums to amplify top funnel awareness.

No. 325: Consolidation and Cable 2.0

Streaming services will be bundled. It’s likely that we’re near the point of OTT carriers marketing the opportunity for consumers to purchase pre-negotiated, economically-friendly bundles of streaming services packaged. With no-login, one collective price, and less of a fear of missing out – the past has become the present. Disney’s streaming offering may be the sole victor here; their value and reach may outlast a shift back consolidation. For all others, the fracturing market of streaming video on demand (SVOD) has begun to cannibalize the direct to consumer opportunity that was the initial appeal. [11]

The DTC-fication of Hollywood

Disney will be able to command a fee that is more lucrative than traditional day and date releases and at margins far greater than their streaming competitors (Netflix), marketplace vendors (Apple’s iTunes) or cinema competitors (AMC Theaters). Before Walt Disney Studios’ 100th anniversary, you will be able to rent a blockbuster premiere through your Disney app. With respect to the overturning of the Paramount Decrees of 1948, this is Walt Disney’s end game.

Member Brief: The Netflix Report

Direct-to-consumer strategies have been influential across physical product industry over the last decade. Hastings seems to be applying this DTC strategy to streaming media. It’s clear that the Netflix team understands that they must play in the traditional space to eventually overtake tradition. [12]

Member Brief: Disney+ and Antitrust

Whether or not DOJ’s ruling on the 1948 Paramount Decrees is overturned, Disney has found a way forward. When Disney+ achieves its desired scale, it will redefine how consumers interact with blockbuster, box office films. Either you’ll watch it in the theaters that you always have. Or you’ll view them in the comfort of your own home – on the day of the film’s premiere. When that time comes, Disney+ will offer their blockbuster debuts for a premium price. And consumers will pay up. The data proves as much. Disney’s intellectual property is responsible for nine of the top ten highest grossing films over the trailing twelve months, a pace that is sure to continue. And to think, it all began with a negotiation over distribution rights with Paramount. [13]

There is an incredible trove of data and insights throughout the 2PM family of categories: weekly reports, member briefs, daily data, and more. But the core of 2PM is the thrice-weekly letters available to Executive Members. The collection of stories, insights, and short analyses provide a window into the why’s, when’s, and how’s of shifts throughout a number of industries that impact one another. If that interests you, you can join at the top of the site. 2PM readers can anticipate the curve; our Executive Members are ahead of it.

By Web Smith | About 2PM

Member Brief: NBC and Linear Commerce

This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.