This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.

No. 339: In Defense of Tim Armstrong

Tim Armstrong is not wrong. The “DTX” in DTX Company is short for “Direct to Everything”; the fund hopes to provide a proverbial spark to this age of online retail. Formerly the CEO of Oath, Tim Armstrong announced the launch of his latest venture with the following mission statement:

We invest in mission-driven founders who are leaders in the direct-brand economy. We are building the infrastructure for the direct brand economy by creating experiences, designing platforms, and investing in founders and talent. [1]

DTX is part venture fund and part amplifier for DTC brands. The fund has already invested in six well-established digitally-natives with an investment thesis that is focused on their appeal to influential, millennial DTC consumers. I’ll come back to the importance of influence at the end.

On November 6, his DTX Company contacted 120 direct-to-consumer brands, making the invitation to join DTX as official partners on the inaugural DTC Friday, the latest man made retail event. Armstrong joins Jack Ma and Jeff Bezos in this respect. The one-day event featured DTX’s portfolio companies and an additional 110 or so that Armstrong recruited. Just seven days later, the day was announced and on the following Friday, Oath’s former CEO took to CNBC to explain his vision for digitally-native brands.

It’s really about having an alternative to the [FAANG] platforms. […] We want to move everything out to the edges.

The retail event’s promise was simple enough, DTX would advertise to 150 million potential consumers. However, it didn’t work out for many of the brand partners. Fred Perrotta of Tortuga backpacks reported:

As of 10 AM Pacific Time, dtcfriday.com has sent us 14 visitors, almost as many as Duck Duck Go.We had better results back when Bitcoin Black Friday was still active.

And led by co-founder and CEO Matt Bahr, Enquire is a SaaS company that powers attribution surveys for hundreds of Shopify stores. Bahr’s platform works with 15 of the 120 brands that partnered with DTX Company. In total, those brands earned ten sales attributed to DTX Company’s efforts.

We analyzed anonymous survey response and UTM parameter data for DTC Friday’s brands that we work with. Several were highlighted on the DTC Friday website and we found that less than a dozen orders were attributed to the campaign. From our experience working with direct-to-consumer brands, this isn’t too surprising. The blanketed media approach is not typically effective in driving conversions in such short-term time-windows.

Nik Sharma, one of AdWeek’s 29 “Young Influentials in branding” also works with a selection of brands featured by DTX. In his words: “I didn’t have any brands that achieved any surge.” There was positive feedback, however. According to Andie founder Melanie Travis, “[DTX Company] had asked me not to share any numbers yet but I’m definitely excited by the early results.” According to Google Trends, Andie Swim’s search interest was at a seven day low on DTC Friday.

For those who are tracking DTX Company’s trajectory, there has been an abundance of skepticism. I’ve mentioned Armstrong’s team’s makeup. Of the 29 employees, zero of them have been former founders of digitally-native brands. There is little to no practical experience within the walls of a company tasked with revolutionizing customer acquisition for DTC. There is little of the instinct that’s driven certain brands to outsized valuations and exits.

In contrast, to prepare Away-competitor Rimowa for the DTC era, LVMH hired former Raden founder Josh Udashkin shortly after his luggage brand shuttered. His practical experience has informed the Rimowa’s tactical decisions for over two years. It’s this lack of practical experienced that convinced Lean Luxe founder Paul Munford to provide this scathing comment:

From what I understand anecdotally, DTC Friday was a bust. Am I shocked? No. I cringed when I heard it was coming, and it certainly doesn’t seem to fit the spirit of the DNVB space. There seems to be a great deal if hubris here to think that just by decreeing this a new holiday, that it would instantly become something massive event like the Black Friday for DNVBs, which is an awful motivation alone.

I understand the need now for a centralized marketplace for the space. And I believe that DTC Friday was meant to play that role. But execution seemed off, there didn’t seem to be a cohesive effort at launch, and I’ve just heard conflicting feedback from folks who participated.

By my estimation, it wasn’t a bust. Despite the poor feedback from a number of brand operators, DTC Friday likely its purpose. Tim Armstrong is not wrong, he’s early. DTX’s effort to launch DTC Friday 2019 wasn’t designed to prioritize the advertising brands. The goal was to advertise Flowcode, a reportedly advanced rebrand of the QR code concept that was dismissed in the United States, several years ago. The star of each of the retail holiday’s TV ads, street posters, and influencer whitelisting efforts wasn’t swimwear, technical fabric menswear, children’s clothes, or a relaxing drink. Nor were the stars the founders, themselves.

In each case, the most prominent property on each ad was Armstrong’s Flowcode – an easier way to link visual marketing to an online property. DTX was discriminate in its advertising investments. While some brands experienced little to no lift, there is evidence that leads me to conclude that a selection of brands were given the royal treatment. And they benefited from it. Andie’s request for silence makes more sense, with this as the context.

Armstrong’s estimated spend on Rockets of Awesome: $35,000

Armstrong’s estimated spend on Andie: $45,000

Armstrong’s estimated spend on Rhone: $27,000

Armstrong’s estimated spend on Recess: $65,000

Flowcode, QR culture, and online retail penetration

Commerce has been democratized and thanks to platforms like Facebook and Google, attention has become centralized. According to the President and COO of Loop Returns:

As attention decentralizes, brands will have an opportunity to build DTC communication channels with consumers. DTX and Flowcode looks like an early experiment in this genre. It may not (will likely not) be right but that doesn’t mean they’re wrong.

It’s worthwhile to mention that when Tim Armstrong made the comments (below), it was misinterpreted by many.

The distribution structure of social, search, YouTube and their ad formats allow these companies to put everything in their product catalog directly in front of consumers. The payments space, though complicated now, is on the verge of getting a lot easier. And the systems getting built now are allowing companies to get real-time, direct relationships built with consumers.

Armstrong maintains a notable disdain for FAANG’s influence on media and commerce, a fact that comes through in every sound bite or article on his work with DTX. His solutions are sound, they are just early. While we’ve seen vast improvements to payment systems in North America with the adoption of Apple Pay, Android Pay, Square Cash, Venmo, the advent of Amazon Go, and the expansion of other digital-first solutions: the U.S. continues to lag behind China and other Asian countries.

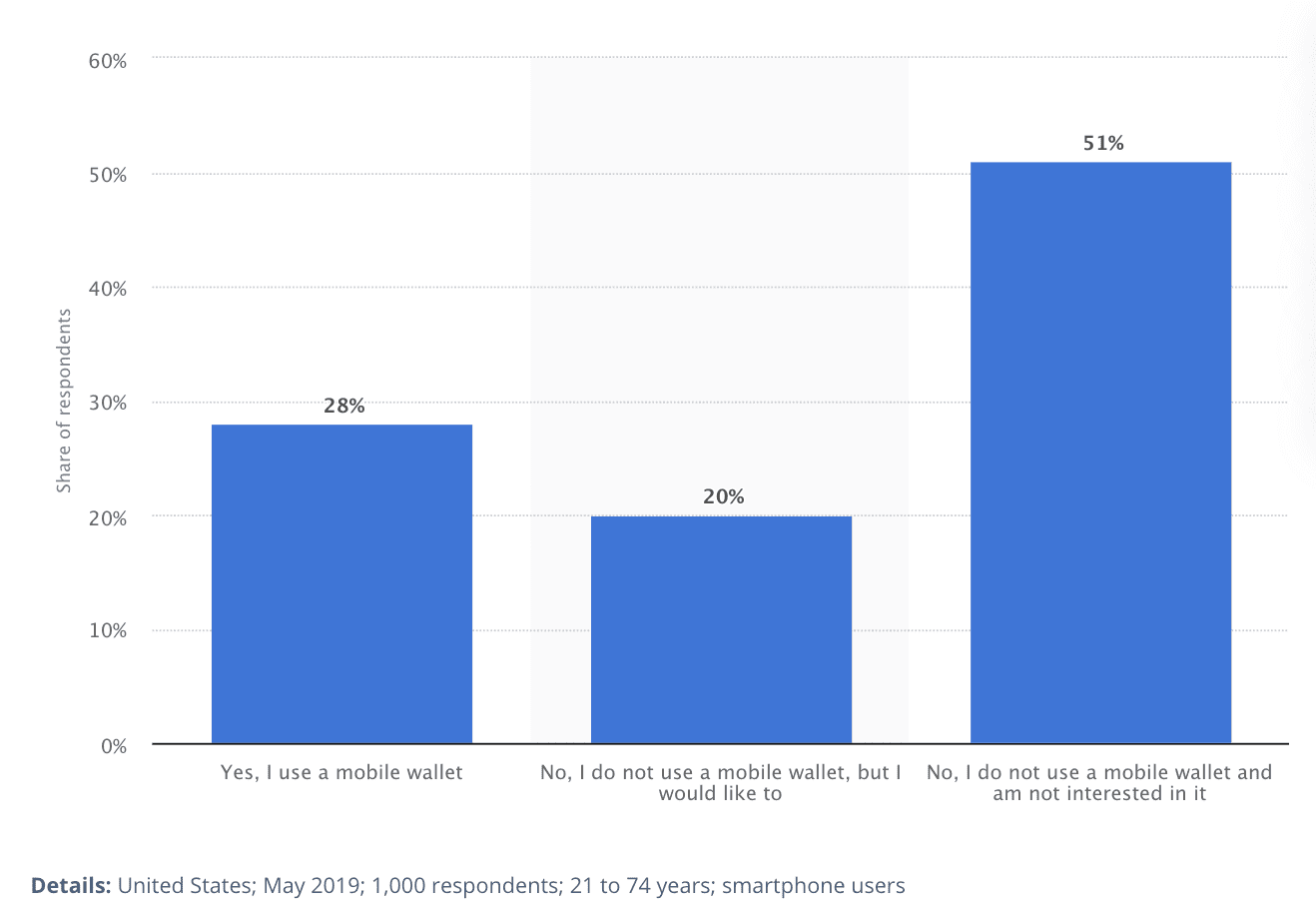

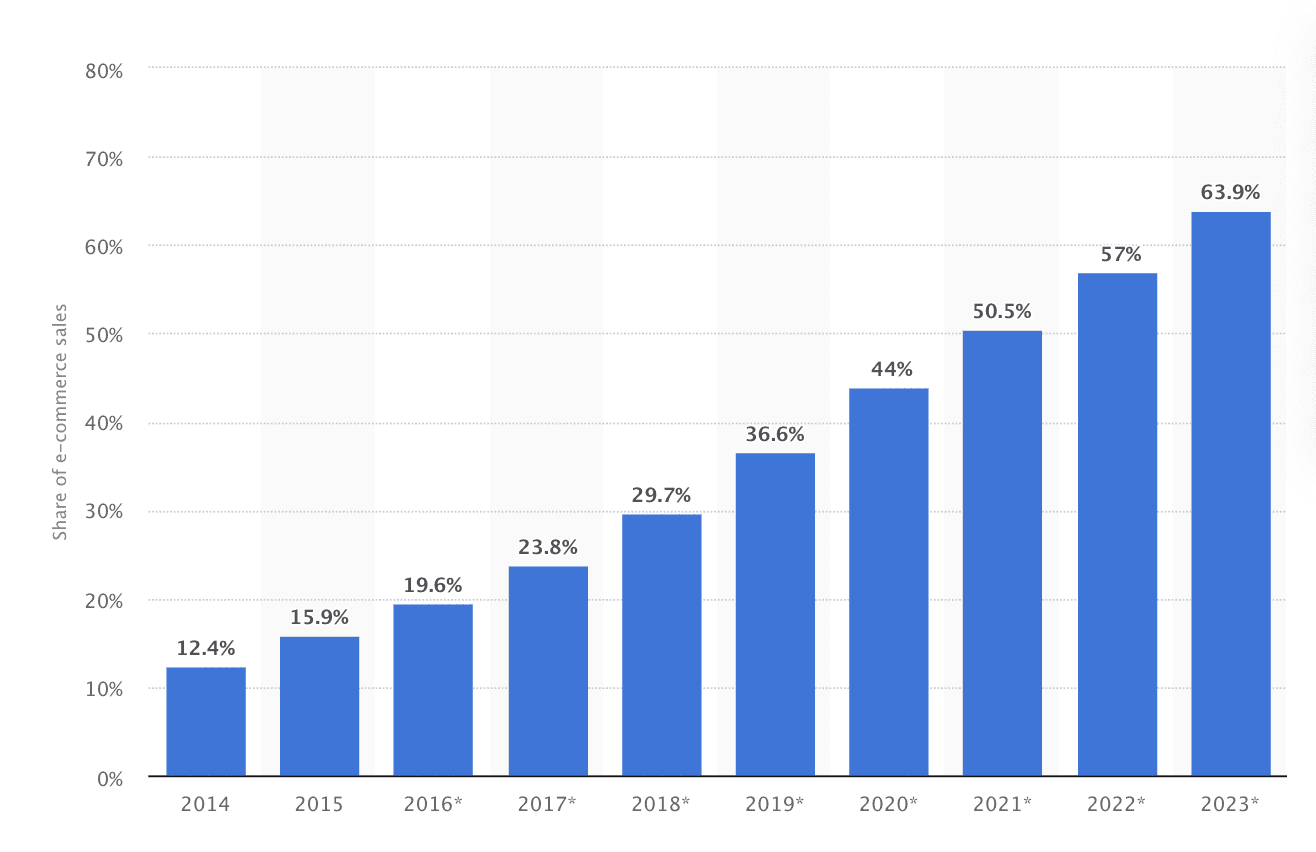

A lagging indicator, eCommerce is still at a lowly 12% of all retail in the United States. By comparison, this number borders on 39% in China. The primary difference between the two penetration rates can be chalked up to mobile wallet adoption. In China, nearly every citizen uses mobile payments for day to day life. In country, WeChat Pay and AliPay are so prevalent, it can be difficult for tourists to transact without them.

Travelers have had more luck on Alipay, which introduced a seven-step process last week that requires visitors to submit passport and visa information to Alipay, before loading money using an overseas card onto a prepaid card. [2]

And here is why the data is important. Offline-to-online attribution has been difficult for marketers. In the United States, offline attribution is mostly manual for billboards, brochures, mailers, and physical activations. Brands issue surveys or ask for attribution data. In China, however, QR codes fuel sales and attribution at scale. [3] Given the flow of retail innovations from China to the United States, it’s clear to see that when Armstrong discusses payments “getting easier”, he anticipates an adoption of mobile wallets and streamlined payments systems. Why? The prevalence of these systems correlated with a mass adoption of QR code usage in China.

At the start of this decade, most Chinese people were still carrying cash everywhere and credit cards were rarely used outside of the big cities. But as people began to earn more, it was clear they needed a new way to pay without carrying wads of cash. [3]

DTC Friday may not have been a successful sales day by most standards but it was an effective way to recruit popular brands to market a concept that America laughed at just a few years prior.

In the United States, there are barriers to the future that Armstrong imagines. Here, America is over-retailed. There are more brick and mortar stores, per capita, than anywhere else on Earth. The real estate development industry is so prevalent that the brick and mortar has become eCommerce’s greatest hindrance. We are less likely to adopt mobile payments and when we can use debit cards in most physical stores.

So, in the meantime – digitally native brands are best served leveraging the methods of traditional retailers to achieve scale. But eventually, Armstrong’s hypothesis will prove correct. Time will tell if it’s DTX Company that lives to take the credit for this shift in consumer behavior. The diffusion of innovation curve does not favor Armstrong. It will be up to DTX and its band of DTC loyals like Andie, Recess, Rockets of Awesome, and Rhone to persuade savvy millennials to shift their shopping behaviors. If not, Armstrong’s Flowcode could be the Webvan to another innovator’s DoorDash or UberEats. Time and adoption velocity will determine who gets the credit for the sale. And that may be one attribution problem that even Armstrong cannot solve for.

Research and Report by Web Smith | About 2PM

No. 329: The MLM-ification of DTC

On Mavely and the unspoken opportunity ahead for the DTC industry. When Greats Brand was reportedly acquired by Steve Madden after their most recent year that saw $13 million in earnings, it was a shock to many in the industry. Revenues seemed lower than what many expected but inline with the realties of buildng an omnichannel brand with an often-costly means of customer acquisition. It’s likely that profitability was an issue. This begs the question, how would things have been different if Greats’ customer acquisition model was one built on profitability and value? The venture-dependent, high growth model may elevate a select few brands in the ecosystem but it seems to be depressing the exit optionality of the majority of them.

Percentage of ad spend is a fine tool for aligning incentives. The problem is not with tested and vetted agencies. It’s with bad ones using it to pad income before providing value.

Founded by Ryan Babenzien, Greats was considered a well-respected, independent shoe company with great propects to become a brand as promising as Allbirds. Babenzien’s marketing team had command over several types of outreach. Greats employed several methods to include performance marketing, direct mail, strategic partnerships, and even text-based promotion. But in the end, the brand never achieved profitability. It was a stark reminder that we may be turning a corner in the DTC space; there seems to be an added weight to the importance of earning profits. A rebuke of the SaaS multiple model that many tech companies can adopt to grow in value. At the intersection of growth and profitability, its the street named ‘Profitability’ that DTC brands should run along.

Greats, which still sells most of its shoes through its eCommerce site, opened a 500-square-foot location on Crosby Street last year. The brand also inked a wholesale partnership with Nordstrom and unveiled a buzzy collaboration with men’s fashion authority Nick Wooster.[1]

The company seems to have done everything right and yet, Greats reportedly sold for no more than two times the previous year’s revenues (June 30, 2018 – June 30, 2019). Greats raised $13 million in funding and sold for around a reported $26 million. It became abundantly clear that an absent path to profitability became the issue that drove the wedge. Steve Madden’s supply chain and organization will be a great fit for this reason, the company drove north of $410 million in the previous year. And they did so while maintaining profitability.

We want to build a profitable business and we’re one of the few digitally-native brands that hasn’t raised an ungodly amount of money that makes it challenging to build a profitable business and exit where everybody wins. We weren’t trying to build the company that had the biggest valuation in round one. We’re trying to build the company that had the biggest valuation at the end. [2]

The news of this acquisition served as a wakeup call for many in the direct to consumer space. What else can be done to improve the viability of DTC brands? Is an early-stage path profitability that crucial? If there is one thing that’s clear, the days of optimizing for ‘at any cost’ growth may be over. As customer acquisition costs continue to skyrocket, retail media has begun reporting on several marketing alternatives. Of them is Mavely, a relatively new platform that launched with a unique approach to reducing CAC for these brands. Mavely’s big idea: turn these DTC brands into multi-level marketing companies.

Mavely is trying to put a new spin on the multilevel-marketing model, in which companies recruit people to sell for them but which has gotten a bad rap for leading a lot of people to actually lose money. Wray said Mavely has no cost to join, no inventory requirements that consumers must maintain, and no minimum follower count that users need to recommend products. [3]

Founded by Evan Wray, Peggy O’Flaherty, and Sean O’Brien, the Chicago-based company has raised $1 million and is reportedly profitable “on a per user basis.” The app-based service has 10,000 users and currently operates as a glorified, peer-to-peer affiliate model. But while it may eventually and significantly supplement organic and paid growth for brands, that timeline is likely to be longer than Mavely would care to admit. Critical mass for this type of service means that Mavely will have to earn tens of millions of users. It will be interesting to observe whether or not Wray’s company can remain committed to growing the way that they’re preaching to their DTC partners: cost-effectively, perhaps a bit slowly, and by one customer (down-line) at a time. In the meantime, the performance marketing industry may be due for an evolution of its own.

Web Smith on Twitter

I’m not sure that a lot of DTC brand owners realize that they’re building companies valued at 1 – 1.5x revenues.

In a recent conversation on the merits of percentage of ad spend as a profit center for media buying agencies, agency owner David Hermann provided his perspective on how business should be pursued between DTC brands and agency partners.

This is why we do percentage of revenue tied to ROAS that’s based on their margins and what the break even point is after costs associated with our fees and expenses. Trust is key, we lay everything out before we get started so they never are in dark on anything. [4]

It presented a worthwhile question. As institutional investors continue to pour more and more venture capital into the DTC space, the approach to marketing should evolve with the volume. CAC has risen as a result of an influx of capital spent on performance marketing. This cycle has led to an unintended result; larger but largely unprofitable businesses. Perhaps the math of success or failure should be reconsidered by investors and founders, alike. What Hermann suggests is correct, agencies should consider a new model for compensation – one that emphasizes healthy contribution margins for these retailers.

Hermann went on:

[My firm is] dealing with one client’s margins right now. [We’re] helping them find a better supply chain. They needed a 2.15x margin just to break even after fees and expenses, so I am now helping on their margin-side. As I always say, media buying is just one side of the job now.

There is an opportunity for a new style of performance marketing agency. Agencies equipped with brand-side, practical expertise could build acquisition strategies around healthy margins, paving the way for percentage of profits as the key performance indicator shared between DTC brands and their agency partners. This solves several problems. Of those concerns, this model accounts for: (1) sustainability, (2) efficient paths to profitability, (3) longer-term relationships between agencies and brands, and (4) decreased dependence on institutional capital. Rather than media buyers being compensated for what they spend, agencies should consider compensation on the profits that they earn for brands.

It’s acquisition vehicles like Mavely, BrandBox, DTX Company’s Unbox, and Showfields that may influence this shift in the agency business model by providing meaningful opportunities for CAC diversification. And if so, the DTC era may finally begin to solve its profitability problem. This could be the first step towards improving valuation multiples and exit optionality for an industry in need of another feather in its cap.

Report by Web Smith | About 2PM