Этот краткий обзор предназначен исключительно для Исполнительные членыЧтобы упростить членство, вы можете нажать на кнопку ниже и получить доступ к сотням отчетов, нашему списку DTC Power List и другим инструментам, которые помогут вам принимать решения на высоком уровне.

No. 339: In Defense of Tim Armstrong

Tim Armstrong is not wrong. The “DTX” in DTX Company is short for “Direct to Everything”; the fund hopes to provide a proverbial spark to this age of online retail. Formerly the CEO of Oath, Tim Armstrong announced the launch of his latest venture with the following mission statement:

We invest in mission-driven founders who are leaders in the direct-brand economy. We are building the infrastructure for the direct brand economy by creating experiences, designing platforms, and investing in founders and talent. [1]

DTX is part venture fund and part amplifier for DTC brands. The fund has already invested in six well-established digitally-natives with an investment thesis that is focused on their appeal to influential, millennial DTC consumers. I’ll come back to the importance of influence at the end.

On November 6, his DTX Company contacted 120 direct-to-consumer brands, making the invitation to join DTX as official partners on the inaugural DTC Friday, the latest man made retail event. Armstrong joins Jack Ma and Jeff Bezos in this respect. The one-day event featured DTX’s portfolio companies and an additional 110 or so that Armstrong recruited. Just seven days later, the day was announced and on the following Friday, Oath’s former CEO took to CNBC to explain his vision for digitally-native brands.

It’s really about having an alternative to the [FAANG] platforms. […] We want to move everything out to the edges.

The retail event’s promise was simple enough, DTX would advertise to 150 million potential consumers. However, it didn’t work out for many of the brand partners. Fred Perrotta of Tortuga backpacks reported:

As of 10 AM Pacific Time, dtcfriday.com has sent us 14 visitors, almost as many as Duck Duck Go.We had better results back when Bitcoin Black Friday was still active.

And led by co-founder and CEO Matt Bahr, Enquire is a SaaS company that powers attribution surveys for hundreds of Shopify stores. Bahr’s platform works with 15 of the 120 brands that partnered with DTX Company. In total, those brands earned ten sales attributed to DTX Company’s efforts.

We analyzed anonymous survey response and UTM parameter data for DTC Friday’s brands that we work with. Several were highlighted on the DTC Friday website and we found that less than a dozen orders were attributed to the campaign. From our experience working with direct-to-consumer brands, this isn’t too surprising. The blanketed media approach is not typically effective in driving conversions in such short-term time-windows.

Nik Sharma, one of AdWeek’s 29 “Young Influentials in branding” also works with a selection of brands featured by DTX. In his words: “I didn’t have any brands that achieved any surge.” There was positive feedback, however. According to Andie founder Melanie Travis, “[DTX Company] had asked me not to share any numbers yet but I’m definitely excited by the early results.” According to Google Trends, Andie Swim’s search interest was at a seven day low on DTC Friday.

For those who are tracking DTX Company’s trajectory, there has been an abundance of skepticism. I’ve mentioned Armstrong’s team’s makeup. Of the 29 employees, zero of them have been former founders of digitally-native brands. There is little to no practical experience within the walls of a company tasked with revolutionizing customer acquisition for DTC. There is little of the instinct that’s driven certain brands to outsized valuations and exits.

In contrast, to prepare Away-competitor Rimowa for the DTC era, LVMH hired former Raden founder Josh Udashkin shortly after his luggage brand shuttered. His practical experience has informed the Rimowa’s tactical decisions for over two years. It’s this lack of practical experienced that convinced Lean Luxe founder Paul Munford to provide this scathing comment:

From what I understand anecdotally, DTC Friday was a bust. Am I shocked? No. I cringed when I heard it was coming, and it certainly doesn’t seem to fit the spirit of the DNVB space. There seems to be a great deal if hubris here to think that just by decreeing this a new holiday, that it would instantly become something massive event like the Black Friday for DNVBs, which is an awful motivation alone.

I understand the need now for a centralized marketplace for the space. And I believe that DTC Friday was meant to play that role. But execution seemed off, there didn’t seem to be a cohesive effort at launch, and I’ve just heard conflicting feedback from folks who participated.

By my estimation, it wasn’t a bust. Despite the poor feedback from a number of brand operators, DTC Friday likely its purpose. Tim Armstrong is not wrong, he’s early. DTX’s effort to launch DTC Friday 2019 wasn’t designed to prioritize the advertising brands. The goal was to advertise Flowcode, a reportedly advanced rebrand of the QR code concept that was dismissed in the United States, several years ago. The star of each of the retail holiday’s TV ads, street posters, and influencer whitelisting efforts wasn’t swimwear, technical fabric menswear, children’s clothes, or a relaxing drink. Nor were the stars the founders, themselves.

In each case, the most prominent property on each ad was Armstrong’s Flowcode – an easier way to link visual marketing to an online property. DTX was discriminate in its advertising investments. While some brands experienced little to no lift, there is evidence that leads me to conclude that a selection of brands were given the royal treatment. And they benefited from it. Andie’s request for silence makes more sense, with this as the context.

Armstrong’s estimated spend on Rockets of Awesome: $35,000

Armstrong’s estimated spend on Andie: $45,000

Armstrong’s estimated spend on Rhone: $27,000

Armstrong’s estimated spend on Recess: $65,000

Flowcode, QR culture, and online retail penetration

Commerce has been democratized and thanks to platforms like Facebook and Google, attention has become centralized. According to the President and COO of Loop Returns:

As attention decentralizes, brands will have an opportunity to build DTC communication channels with consumers. DTX and Flowcode looks like an early experiment in this genre. It may not (will likely not) be right but that doesn’t mean they’re wrong.

It’s worthwhile to mention that when Tim Armstrong made the comments (below), it was misinterpreted by many.

The distribution structure of social, search, YouTube and their ad formats allow these companies to put everything in their product catalog directly in front of consumers. The payments space, though complicated now, is on the verge of getting a lot easier. And the systems getting built now are allowing companies to get real-time, direct relationships built with consumers.

Armstrong maintains a notable disdain for FAANG’s influence on media and commerce, a fact that comes through in every sound bite or article on his work with DTX. His solutions are sound, they are just early. While we’ve seen vast improvements to payment systems in North America with the adoption of Apple Pay, Android Pay, Square Cash, Venmo, the advent of Amazon Go, and the expansion of other digital-first solutions: the U.S. continues to lag behind China and other Asian countries.

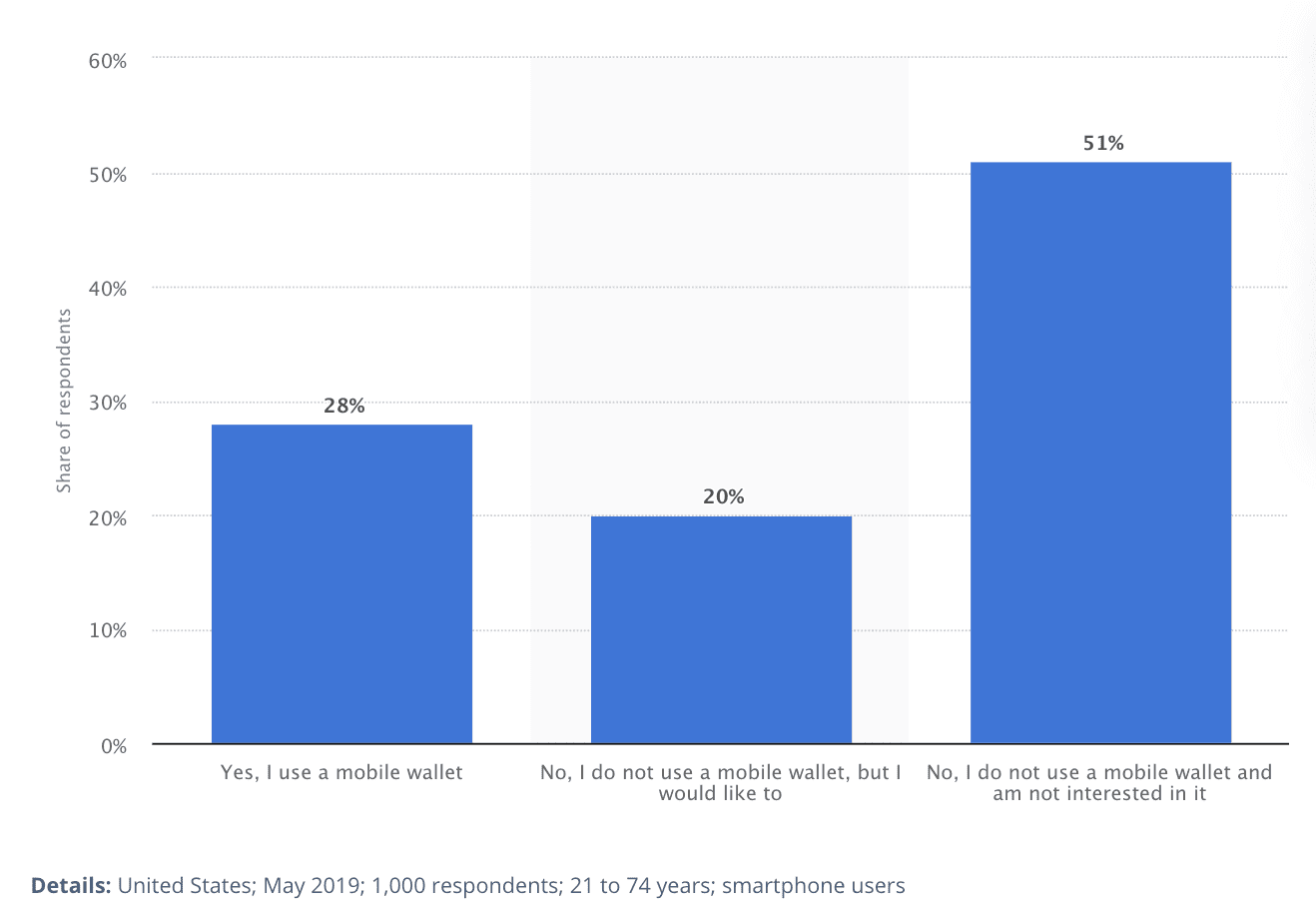

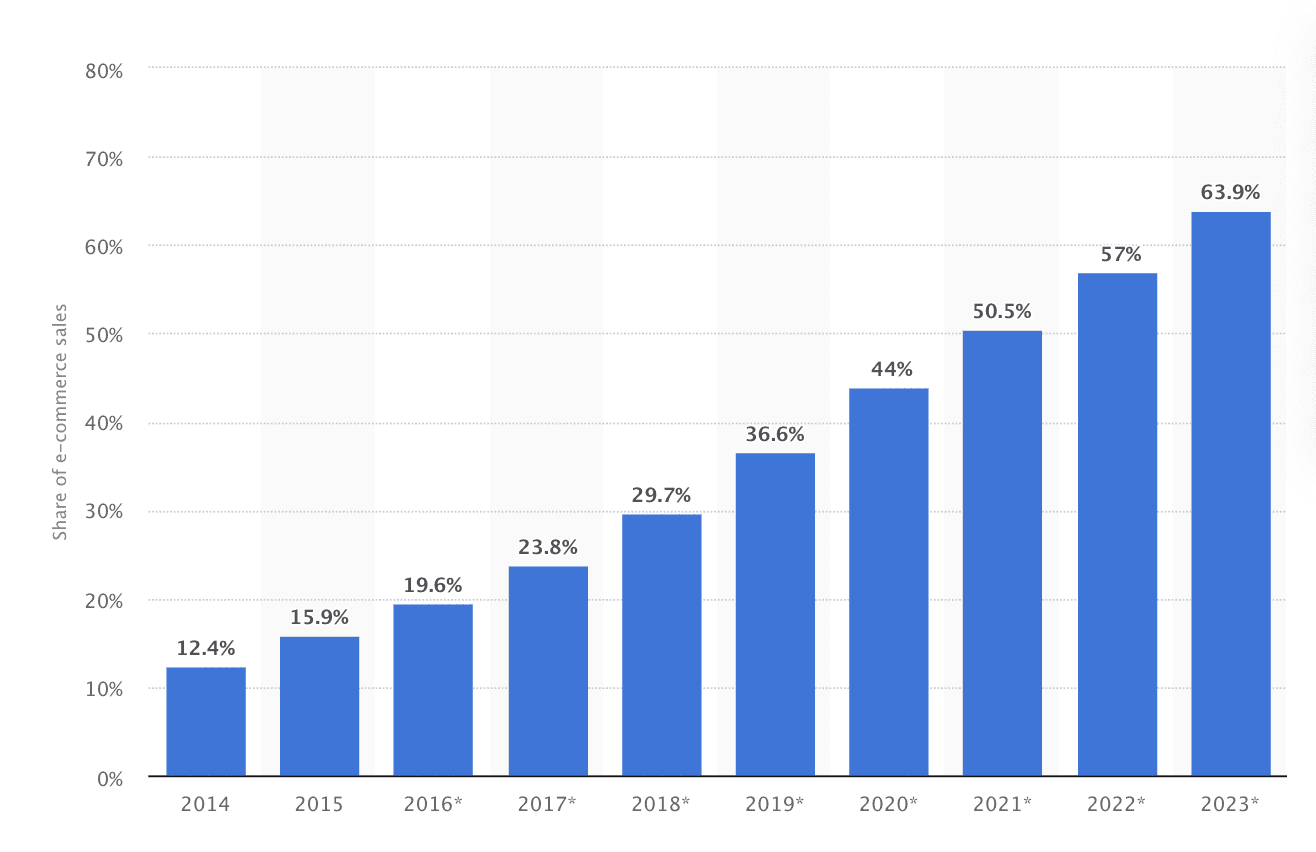

A lagging indicator, eCommerce is still at a lowly 12% of all retail in the United States. By comparison, this number borders on 39% in China. The primary difference between the two penetration rates can be chalked up to mobile wallet adoption. In China, nearly every citizen uses mobile payments for day to day life. In country, WeChat Pay and AliPay are so prevalent, it can be difficult for tourists to transact without them.

Travelers have had more luck on Alipay, which introduced a seven-step process last week that requires visitors to submit passport and visa information to Alipay, before loading money using an overseas card onto a prepaid card. [2]

And here is why the data is important. Offline-to-online attribution has been difficult for marketers. In the United States, offline attribution is mostly manual for billboards, brochures, mailers, and physical activations. Brands issue surveys or ask for attribution data. In China, however, QR codes fuel sales and attribution at scale. [3] Given the flow of retail innovations from China to the United States, it’s clear to see that when Armstrong discusses payments “getting easier”, he anticipates an adoption of mobile wallets and streamlined payments systems. Why? The prevalence of these systems correlated with a mass adoption of QR code usage in China.

At the start of this decade, most Chinese people were still carrying cash everywhere and credit cards were rarely used outside of the big cities. But as people began to earn more, it was clear they needed a new way to pay without carrying wads of cash. [3]

DTC Friday may not have been a successful sales day by most standards but it was an effective way to recruit popular brands to market a concept that America laughed at just a few years prior.

In the United States, there are barriers to the future that Armstrong imagines. Here, America is over-retailed. There are more brick and mortar stores, per capita, than anywhere else on Earth. The real estate development industry is so prevalent that the brick and mortar has become eCommerce’s greatest hindrance. We are less likely to adopt mobile payments and when we can use debit cards in most physical stores.

So, in the meantime – digitally native brands are best served leveraging the methods of traditional retailers to achieve scale. But eventually, Armstrong’s hypothesis will prove correct. Time will tell if it’s DTX Company that lives to take the credit for this shift in consumer behavior. The diffusion of innovation curve does not favor Armstrong. It will be up to DTX and its band of DTC loyals like Andie, Recess, Rockets of Awesome, and Rhone to persuade savvy millennials to shift their shopping behaviors. If not, Armstrong’s Flowcode could be the Webvan to another innovator’s DoorDash or UberEats. Time and adoption velocity will determine who gets the credit for the sale. And that may be one attribution problem that even Armstrong cannot solve for.

Исследование и отчет Веба Смита | Около 2PM

№ 329: MLM-фикация DTC

О компании Mavely и негласных возможностях, открывающихся перед индустрией DTC. Когда компания Greats Brand была приобретена Steve Madden после последнего года, когда ее прибыль составила 13 миллионов долларов, это стало шоком для многих в отрасли. Доходы оказались ниже, чем многие ожидали, но это соответствовало реалиям создания омниканального бренда с часто дорогостоящим способом привлечения клиентов. Вполне вероятно, что рентабельность была проблемой. В связи с этим возникает вопрос, как бы все изменилось, если бы модель привлечения клиентов Greats была построена на прибыльности и ценности? Зависимая от венчурных инвестиций модель быстрого роста может возвысить несколько избранных брендов в экосистеме, но, похоже, она угнетает возможность выхода большинства из них.

Процент от рекламных расходов - прекрасный инструмент для выравнивания стимулов. Проблема не в проверенных агентствах. Проблема в плохих агентствах, которые используют этот инструмент для повышения доходов, а не для создания ценности.

Компания Greats, основанная Райаном Бабензиеном, считалась уважаемой независимой обувной компанией с большими перспективами стать таким же перспективным брендом, как Allbirds. Маркетинговая команда Бабензиена контролировала несколько видов работы с клиентами. Greats использовала несколько методов, включая перфоманс-маркетинг, прямую почтовую рассылку, стратегическое партнерство и даже текстовое продвижение. Но в итоге бренд так и не вышел на прибыльность. Это было суровое напоминание о том, что мы, возможно, поворачиваем за угол в DTC-пространстве; похоже, важность получения прибыли приобретает дополнительный вес. Это упрек в адрес многократной модели SaaS, которую многие технологические компании могут перенять, чтобы расти в цене. На пересечении роста и прибыльности находится улица под названием "Прибыльность", по которой должны двигаться бренды DTC.

Greats, который по-прежнему продает большую часть своей обуви через сайт электронной коммерции, в прошлом году открыл помещение площадью 500 квадратных футов на Кросби-стрит. Бренд также заключил оптовое партнерство с Nordstrom и представил нашумевшую коллаборацию с авторитетом мужской моды Ником Вустером[1].

Компания вроде бы все делала правильно, но Greats, как сообщается, была продана не более чем в два раза дороже, чем выручка за предыдущий год (30 июня 2018 - 30 июня 2019). Greats привлекла 13 миллионов долларов финансирования и продала их за 26 миллионов долларов. Стало совершенно ясно, что отсутствие пути к прибыльности стало проблемой, которая вбила клин. Цепочка поставок и организация Steve Madden отлично подойдут для этой цели, ведь в прошлом году компания заработала более 410 миллионов долларов. И это при сохранении рентабельности.

Мы хотим построить прибыльный бизнес и являемся одним из немногих цифровых брендов, которые не привлекли немереное количество денег, что затрудняет построение прибыльного бизнеса и выход из него с выигрышем для всех. Мы не пытались создать компанию с самой большой оценкой в первом раунде. Мы пытаемся создать компанию, которая будет иметь самую большую оценку в конце".[2]

Новость об этом приобретении послужила тревожным звонком для многих представителей сферы прямых продаж. Что еще можно сделать для повышения жизнеспособности брендов DTC? Так ли важна рентабельность на ранних этапах? Ясно одно: времена оптимизации роста "любой ценой", возможно, прошли. Поскольку стоимость привлечения клиентов продолжает стремительно расти, розничные СМИ начали сообщать о нескольких альтернативных маркетинговых решениях. Среди них - Mavely, относительно новая платформа, которая запустила уникальный подход к снижению CAC для брендов. Главная идея Mavely: превратить эти DTC-бренды в компании многоуровневого маркетинга.

Mavely пытается по-новому взглянуть на модель многоуровневого маркетинга, в рамках которой компании набирают людей для продаж, но которая получила дурную славу из-за того, что многие люди фактически теряют деньги. По словам Врея, в Mavely нет стоимости участия, нет требований к запасам, которые должны поддерживать потребители, и нет минимального количества последователей, которые должны быть у пользователей, чтобы рекомендовать продукты.[3]

Основанная Эваном Врэем, Пегги О'Флаэрти и Шоном О'Брайеном, компания из Чикаго привлекла 1 миллион долларов и, как сообщается, является прибыльной "в расчете на одного пользователя". Сервис, основанный на приложении, насчитывает 10 000 пользователей и в настоящее время работает как прославленная, одноранговая партнерская модель. Но хотя в конечном счете он может существенно дополнить органический и платный рост брендов, этот срок, скорее всего, будет более долгим, чем Mavely хочет признать. Критическая масса для такого рода услуг означает, что Mavely придется набрать десятки миллионов пользователей. Будет интересно понаблюдать, сможет ли компания Врея сохранить приверженность росту так, как они проповедуют своим DTC-партнерам: экономически эффективно, возможно, немного медленно, и по одному клиенту (down-line) за раз. Тем временем, возможно, индустрия перфоманс-маркетинга должна пройти свою собственную эволюцию.

Веб Смит в Twitter

Я не уверен, что многие владельцы DTC-брендов осознают, что они строят компании, оцениваемые в 1-1,5 раза больше выручки.

В ходе недавнего разговора о преимуществах процента от рекламных расходов как центра прибыли для медиабаинговых агентств владелец агентства Дэвид Херманн высказал свою точку зрения на то, как должен вестись бизнес между DTC-брендами и партнерами агентства.

Именно поэтому мы устанавливаем процент от выручки, привязанный к ROAS, который основан на их марже и точке безубыточности после затрат, связанных с нашими комиссионными и расходами. Доверие - ключевой момент, мы рассказываем обо всем до начала работы, чтобы они никогда не оставались в неведении".[4]

В связи с этим возникает интересный вопрос. Поскольку институциональные инвесторы продолжают вливать все больше и больше венчурного капитала в DTC-пространство, подход к маркетингу должен меняться вместе с объемами. CAC вырос в результате притока капитала, потраченного на результативный маркетинг. Этот цикл привел к непреднамеренному результату - увеличению масштабов бизнеса, но его убыточности. Возможно, инвесторам и основателям следует пересмотреть математику успеха или неудачи. То, что предлагает Герман, верно: агентствам следует рассмотреть новую модель вознаграждения - такую, которая подчеркивает здоровый уровень прибыли для этих ритейлеров.

Герман продолжил:

[Моя фирма сейчас занимается маржой одного клиента. [Мы помогаем им найти лучшую цепочку поставок. Им нужна была маржа в 2,15 раза, чтобы выйти на безубыточность после комиссий и расходов, поэтому сейчас я помогаю им с маржой. Как я всегда говорю, медиабаинг - это только одна сторона работы.

Появилась возможность создать новый стиль агентства performance-маркетинга. Агентства, обладающие практическим опытом работы с брендами, могли бы строить стратегии привлечения клиентов на основе здоровой маржи, прокладывая путь к проценту прибыли как ключевому показателю эффективности, разделяемому между DTC-брендами и их партнерами-агентствами. Это решает несколько проблем. Из этих проблем данная модель учитывает: (1) устойчивость, (2) эффективные пути к прибыльности, (3) долгосрочные отношения между агентствами и брендами и (4) снижение зависимости от институционального капитала. Вместо того чтобы вознаграждать медиабайеров за то, что они тратят, агентствам следует подумать о вознаграждении за прибыль, которую они зарабатывают для брендов.

Именно такие приобретения, как Mavely, BrandBox, DTX Company's Unbox и Showfields, могут повлиять на изменение бизнес-модели агентства, предоставив значимые возможности для диверсификации CAC. И если это так, то эра DTC, возможно, наконец-то начнет решать проблему рентабельности. Это может стать первым шагом к повышению мультипликаторов оценки и возможности выхода для отрасли, нуждающейся в еще одном перышке в шапке.

Доклад Веба Смита | Около 2 часов дня