This week, NOBULL began its time as the title sponsorship of the CrossFit Games. The event was associated with Reebok for ten year. There are a number of narratives here – the founding team at NOBULL were once Reebok employees. It’s a story with endless examples of rivalry but the main one is one oft seen in retail. The generational brand gave way to the challenger. They’ve earned their time in the spotlight. Now, we will see what NOBULL does with the opportunity.

Direct-to-consumer startups are designed to be disruptive by nature. Their purpose is to see the opportunities that larger corporations have gotten too big to identify themselves, improving on process and product in doing so. At CrossFit, the changeover in sponsor is giving a DTC challenger the chance to go toe-to-toe where an incumbent left shoes to fill. CrossFit CEO Eric Roza sought out NOBULL to take over as CrossFit’s main sponsor, letting Reebok’s time lapse. The brand pulled out following the former CEO’s remarks.

Roza had a choice to make. As he recently told Footwear News, he could have given the company more time to recover before seeing who else he might have to choose from on the market. But he was a NOBULL fan, in large part due to the brand’s DTC spirit. He said in the interview:

I love their nimbleness and that I had a friendship with the founders, not just a business relationship. When I met them, I had an interest in investing in them, so they knew I was a bit of a fanboy. I loved that they were a direct-to-consumer play, they were e-commerce forward. The fact that they were digitally-native, really good at direct marketing and native to CrossFit with styling I really liked, made it the right decision for us.

NOBULL’s nimbleness, digitally-native and eCommerce forward traits made it the most attractive partner to CrossFit, proving that DTC challengers have real potential in shaking up the markets they’re in. That’s especially true when it comes to partnerships with brands who are looking to borrow some of that DTC spirit.

Reebok is making its own moves. The brand last week launched a Bonus Program that offers prize money to athletes who take first or second place in a CrossFit event wearing a Reebok shoe – directly incentivizing athletes to disregard the new sponsor’s shoes with a financial bonus. According to Reebok, nearly 200 athletes have taken them up on the challenge. NOBULL, in response, reminded Reebok who had the title sponsor spot. CMO Todd Meleney told Morning Chalk Up, “Since the beginning we’ve been in favor of anything that supports the athletes and the CrossFit community. As the title sponsor of the CrossFit Games, that’s the case now more than ever.”

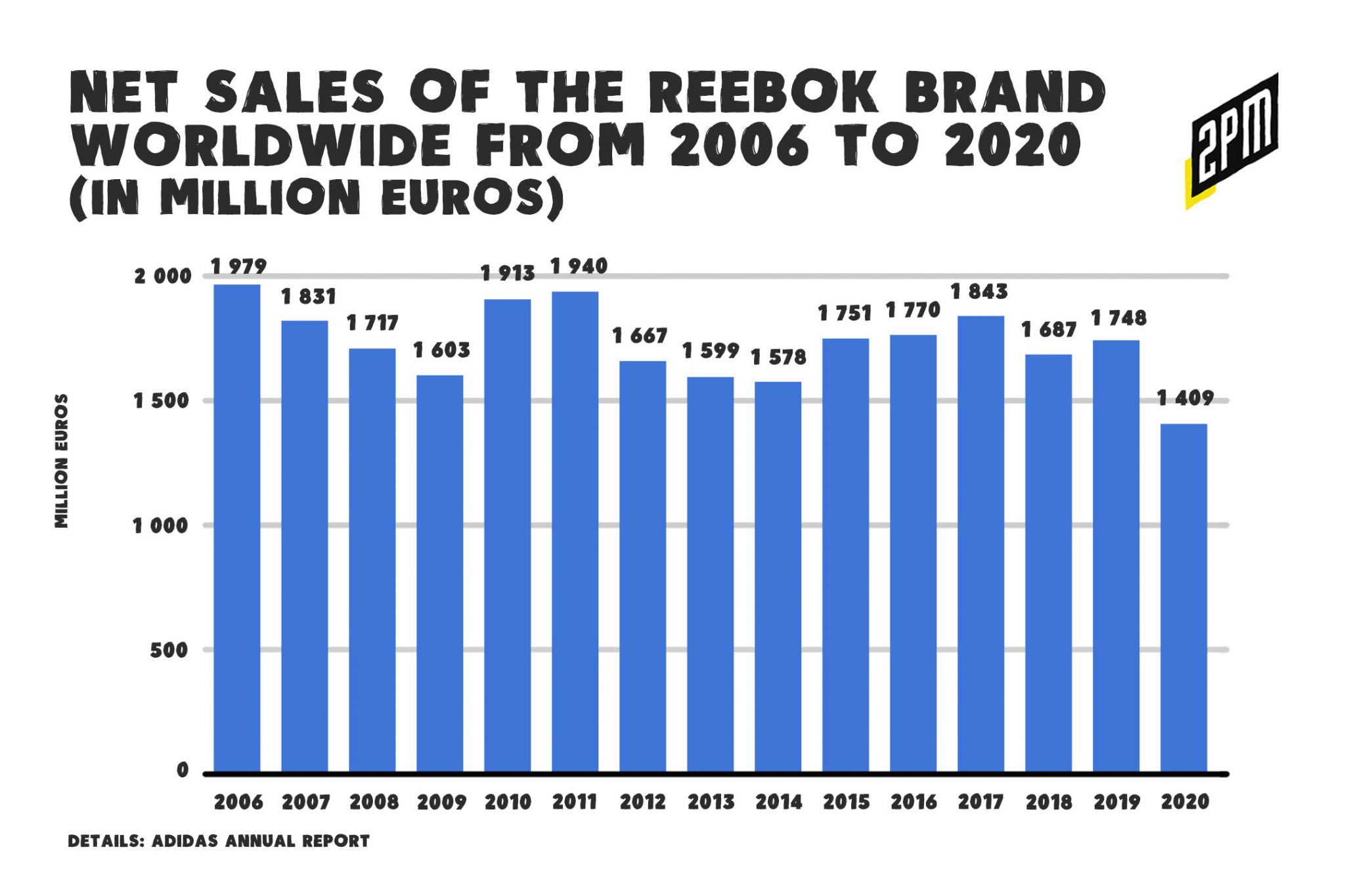

In all, this is as much a story about Reebok’s failure (the company is looking for a buyer) as it is NOBULLs rise as an enterprise-level brand. Click on the above graph to read Retail Dive’s narration of Reebok’s rise and fall. Reebok’s sales fell to a 15 year low, meanwhile Nike and Puma (who suffered similar pandemic struggles) only fell to three and five year lows respectively. Meanwhile, at No. 109, 2PM estimates NOBULL’s revenue to be well into the nine figures just seven years into their life cycle.

By Web Smith | Editor: Hilary Milnes | Art: Christina Williams and Alex Remy

One side has the advantage of distribution, the other side has the advantage of brand equity. I believe that the holding company trend will favor brand equity in the long run.

One side has the advantage of distribution, the other side has the advantage of brand equity. I believe that the holding company trend will favor brand equity in the long run.