Think symbiosis.

Lending and brand equity go hand in hand. Buy Now, Pay Later (BNPL) providers and the retailers that they serve are key to each other’s operations; they are mutually beneficial, they work in tandem. Affirm, Klarna, and countless others are key products for many retailers. Without these services, gross merchandising volume (GMV) would have been considerably lower for many, over recent years. Consumer Packaged Goods (CPG) lenders like Ampla served brands by lending to them; this allowed them to acquire inventory or pay for marketing services that helped them grow top-line revenues. As their portfolio of lending customers grew, so did their valuation – at least for a time.

And then, there are companies like Tandym, a financial services company that works with merchants to create their own private-label digital credit cards and rewards programs. Tandym charges a processing fee of just 0.5%, a substantial savings compared to the typical 1.5% to 3% fees imposed by major credit card providers. Tandym provides the capital necessary to extend credit directly to a retailer’s customers, offering businesses a seamless and cost-effective way to grow and engage their customer bases. A retailer doesn’t need to be worth trillions or even billions to access such technologies. At almost any level, credit lending and retail brands can achieve symbiosis.

****

When it comes to credit / brand symbiosis, Apple has once again set the standard at the enterprise level. This marks the fourth consecutive year that Apple Card, in partnership with Goldman Sachs, has achieved the top ranking, a testament to its user-centric design, loyalty rewards, and commitment to financial health. With innovative features like daily cash rewards and integration with Apple Wallet, it’s become a favorite among consumers.

As Apple continues to dominate the U.S. market with its top-rated card, Amazon is making its significant move in the loyalty-driven economy with the launch of a new co-branded credit card in partnership with Barclays. The Amazon Barclaycard will aim to capture consumer loyalty by offering rewards on everyday purchases, which can be redeemed for Amazon gift cards. With no annual fee and additional perks for Amazon Prime members, this new card is designed to strengthen Amazon’s ecosystem while providing customers with valuable benefits tailored to their shopping habits.

Together, these developments underscore the growing importance of branded credit cards in fostering customer loyalty and delivering value in today’s competitive financial landscape.

The consumer credit landscape is rapidly changing, with branded credit cards standing out as the most attractive option in an increasingly strained economy. Driven by rising interest rates, diminishing brand loyalty, and growing revolving debt, branded credit cards are becoming a go-to tool for brands that aim to shore up their value.

The shift toward value-oriented credit cards

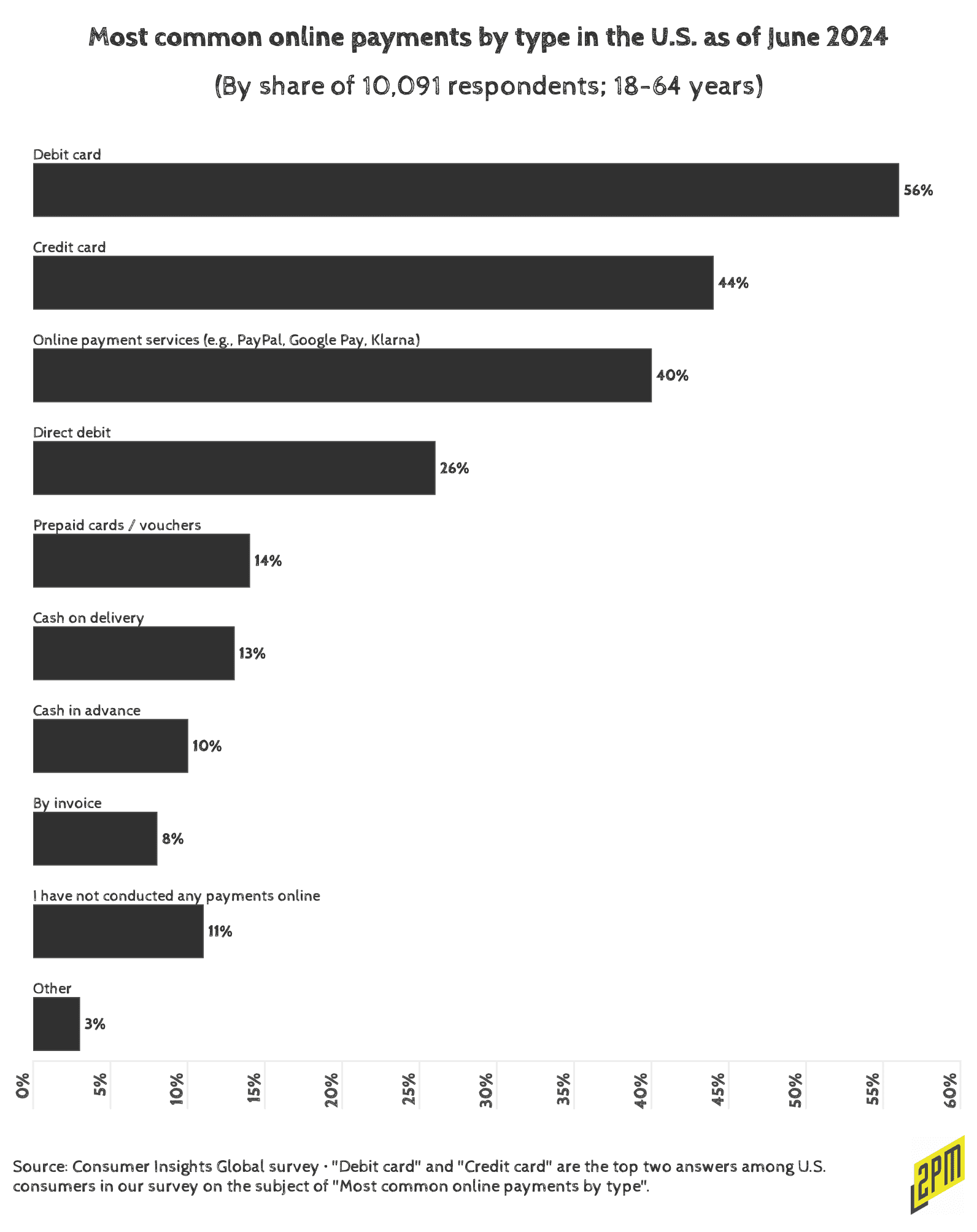

The recent J.D. Power 2024 U.S. Credit Card Satisfaction Study communicates a shift in consumer preferences and revelations worth noting here. The study reveals that over half of U.S. credit card customers are financially unhealthy, with 51% carrying revolving debt as interest rates climb. This is buoyed by the rise in Buy Now Pay Later transactions, which Apple chose to end in June of 2024. But, when juxtaposed on the data shared below, it illustrates just how important credit card usage is to the retail industry: 44% of transactions are through credit cards, another 40% are through “Brand Pay” systems and BNPL technologies: Google Pay, Apple Pay, Paypal, Klarna, Affirm, and so on.

Given the growing strains caused by economic distress, the appeal of traditional points and air miles cards is diminishing, with many consumers opting for cash back cards that offer more tangible benefits. As such, cash back cards now dominate the market, used by 58% of cardholders, compared to 31% who still favor points and miles cards.

60% of co-branded cardholders primarily use cards affiliated with major retailers like Amazon, Costco, or Target. This shows the strong appeal of cards offering rewards on everyday purchases. (The Financial Brand)

This trend can be seen as a direct response to mounting pressures. Cashback cards, which often come with lower or no annual fees, provide a more accessible way for consumers to derive value from their spending without the complexity and long-term commitment associated with points and miles programs. As financial health declines, so does the attractiveness of credit cards that promise rewards in the distant future. Consumers are looking for immediate benefits, and cashback cards deliver just that.

Regulatory pressures and the rise of BNPL

At the same time, regulatory pressures are disrupting the Buy Now, Pay Later (BNPL) services that reshaped the broader credit landscape. The Consumer Financial Protection Bureau (CFPB) has been scrutinizing BNPL products, proposing new regulations subjecting them to similar rules as traditional credit cards. Companies like Affirm have responded by advocating for a regulatory framework tailored specifically to BNPL, arguing that applying credit card regulations to these products could create confusion and unnecessary compliance burdens.

As BNPL products have grown in popularity, they’ve posed a potential threat to traditional credit cards, particularly those that rely on high-interest revolving debt for profitability. However, recent months have stressed the importance of innovation and adaptability in the credit market. One of those innovations is the rise of the co-branded credit card.

Co-branded credit cards: a strategic advantage

Co-branded credit cards are emerging as a strategic advantage for both issuers and partner brands. The recent partnership between Amazon and Barclays to launch a co-branded credit car in the U.K. is a prime example of the continuation of this trend. The Amazon Barclaycard will offer customers rewards on everyday spending, which can be redeemed for Amazon gift cards, with additional perks for Amazon Prime members. This card strengthens customer loyalty to Amazon and provides Barclays with a valuable touchpoint for engaging with a broad customer base. Here are six top examples of co-branded credit cards:

Apple Card (Goldman Sachs):

The Apple Card stands out for its seamless integration with Apple Wallet and its commitment to transparency. With no fees, not even for late payments, and a straightforward cashback program that offers up to 3% Daily Cash on purchases, it’s designed for users who value simplicity and financial health.

Amazon Prime Rewards Visa Signature Card:

Tailored for the avid Amazon shopper, this card delivers substantial rewards—5% back on Amazon and Whole Foods purchases. Beyond Amazon, it also offers 2% back at restaurants, gas stations, and drugstores, making it a versatile tool for everyday spending. There’s no annual fee for Prime members, adding to its appeal.

Chase Sapphire Reserve:

Known for its travel perks, the Chase Sapphire Reserve is a premium card that provides 3x points on travel and dining worldwide. Cardholders enjoy an annual $300 travel credit, access to over 1,000 airport lounges through Priority Pass, and valuable travel insurance, making it a top choice for those who are often on the go.

Hilton Honors American Express Aspire Card:

This card is a powerhouse for Hilton enthusiasts, offering 14x points on stays at Hilton properties. Cardholders receive automatic Hilton Diamond status, which includes room upgrades and late checkouts, along with a free weekend night every year. It’s the ultimate companion for frequent Hilton guests.

Southwest Rapid Rewards Premier Credit Card:

This card is tailored for those who frequently fly Southwest Airlines. It rewards users with 2x points on Southwest purchases and anniversary bonus points each year. With no foreign transaction fees and the ability to earn towards Companion Pass status, it’s a strong contender for domestic travelers.

Costco Anywhere Visa® Card by Citi:

A go-to for Costco shoppers, this card offers impressive rewards, including 4% cash back on gas, 3% on restaurants and travel, and 2% on Costco purchases. Its broad rewards categories make it a versatile option for those who do most of their shopping at Costco.

Co-branded credit cards offer several key benefits. First, they align the interests of the issuer and partner brands, creating a mutually beneficial relationship that can drive customer engagement and retention. For brands like Amazon, co-branded cards enhance the shopping experience by offering rewards directly tied to their ecosystem.

The role of branded credit cards in the loyalty economy

These cards are playing an increasingly important role in the loyalty-driven economy. They offer consumers a way to earn rewards and benefits that align with their spending habits and financial goals. As the financial health of many consumers deteriorates, these cards provide a valuable tool for managing expenses and maximizing the value of everyday spending.

Best Buy listed its credit card as the second-largest driver of customer loyalty and repeat action. (eMarketer)

The success of branded credit cards depends on their ability to adapt to the changing needs and preferences of consumers. Issuers must navigate a complex landscape, balancing the need for profitability with the demand for accessible and valuable rewards. This requires a deep understanding of consumer behavior and a willingness to innovate and respond to regulatory challenges.

In all, branded credit cards represent a bright spot in an economy under increasing pressure from revolving debt and financial instability. By offering tailored rewards, lower fees, and partnerships with famous brands, these cards are helping consumers navigate a challenging financial landscape while providing issuers with a valuable tool for building customer loyalty. Co-branded credit cards offer a compelling growth opportunity for financial institutions and their retail partners. By tackling existing challenges and capitalizing on new market trends, these tailored financial products can seize a greater portion of the credit card market while delivering distinct advantages to a diverse range of consumers. Success in this space hinges on crafting strong value propositions, clearly conveying these benefits to prospective cardholders, and persistently innovating to keep pace with the shifting demands and preferences of consumers.

As the credit market continues to evolve, branded credit cards are likely to become even more important, serving as a critical driver of consumer satisfaction, financial resilience, and brand value.

Research, Data, and Writing by Web Smith