This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.

Memo: The New Evangelism of Prime Access

If you grew up with a frequently empty-ish refrigerator, Amazon Prime is a godsend. As an adult: you wake up, look at your refrigerator, your memories drive an irrational response, and you needlessly open an app to fill the empty spaces in your pantry or cold storage. Within two hours, the problem is solved and your shelves no longer trigger thoughts of food insecurity. Amazon gets the business, the delivery fees, and the data. Costco be damned. I can’t be the only person who routinely does this.

The market for this consumer behavior is due to grow. Amazon Prime, which typically comes with a $139 annual fee, has a cheaper option for those in need and you’re going to hear more about it. Prime Access, while available since 2017, was recently pushed by Amazon (Amazon expanded upon this program in October 2022). Likely as a solution for a two-pronged problem:

- remaining inflationary effects (4.9%)

- the fall in retail membership revenues

Soon enough, the app may reflect grocery options that may be more economical. More on that in a moment.

Amazon has often been at the forefront of eCommerce evolution, from its origin as a digital bookstore to its current status as a colossal multi-industry conglomerate. Its April 2023 evangelism of Prime Access (a six year old program) and one designed to democratize Amazon Prime for lower-income users, is another testament to the company’s need to adjust to retail’s evolution.

Prime Access is Amazon’s discounted membership program for qualifying government programs. Eligible customers in the U.S. who sign up receive all of the privileges of Amazon Prime at around 50% off of the typical membership.

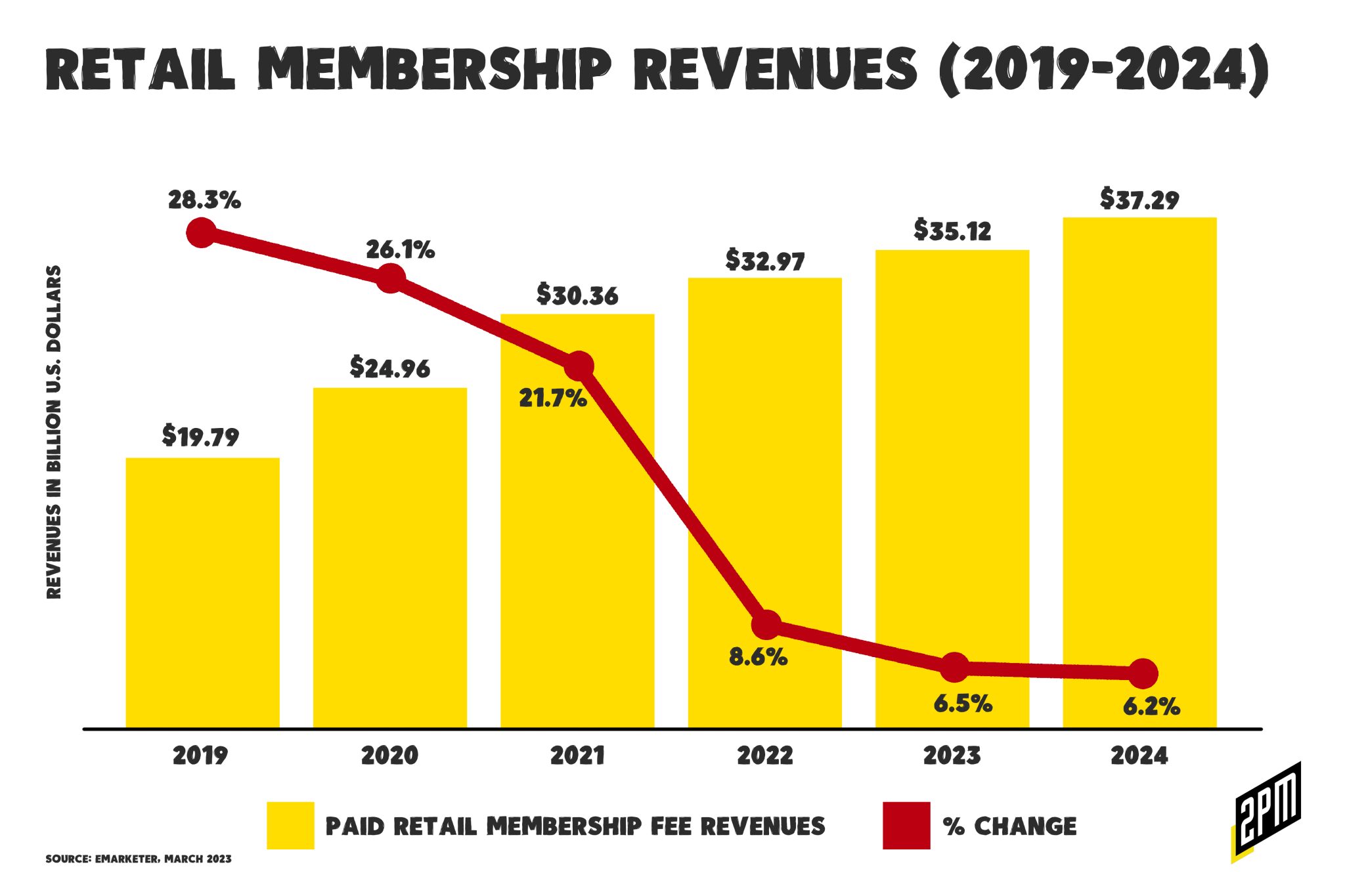

Prime Access could significantly impact Amazon’s potential growth against the backdrop of declining industry-wide membership revenue growth. According to membership startup Inveterate who powers the following companies’ membership loyalty programs: Liquid IV, Fresh Clean Tees, Lashify, Fly by Jing, Flamingo Estate, and a number of others:

A study by Deloitte found that 67% of consumers would join a paid loyalty program if it offered significant benefits (compared to just 33% who said the same for free points-based programs).

Amazon is hoping to capture, or even improve, the remaining growth by appealing to a larger audience who may be interested in paid loyalty programs. As it stands, Amazon Prime remains the highest-rated loyalty program according to an October 2022 survey by Activate. This includes CostCo, Sam’s Club, Walmart+, and Instacart+. But growth has predictably slowed.

Traditionally, Amazon Prime has been perceived as a luxury-adjacent good, predominantly catering to higher-income households. However, this new initiative represents a significant expansion of Amazon’s target market. By leveraging a range of government programs, Amazon is making its premium services accessible to a broader demographic, thereby widening its potential user base and revenue streams. This move demonstrates the power of membership-driven, app-based eCommerce: by lowering the barrier to entry, Amazon can tap into a lesser-served (but growing) market, boosting its growth potential. This could be the antidote.

The power of simplicity in commerce, especially in the context of one-click, repeat purchases in app-based marketplaces like Amazon Prime, cannot be overstated (here is a recent deep dive on that topic). The Amazon model has excelled by offering a seamless, frictionless shopping experience. The fewer the steps a consumer has to take to complete a purchase, the higher the likelihood of conversion. By making the purchasing process as simple as possible, Amazon encourages users to make repeat purchases, fostering customer loyalty and driving sales. In the context of democratizing commerce, I believe that there is a cause for concern.

In line with the principle of simplicity, Prime Access also serves to democratize eCommerce. According to Amazon, you can provide proof of eligibility or participation from the following programs:

- SNAP EBT

- Medicaid

- Woman, Infants, and Children Program (WIC)

- Supplemental Security Income (SSI)

- Direct Express Debit Card (DE)

- Temporary Assistance for Needy Families (TANF)

- National School Lunch Program (NSLP)

- Low Income Home Energy Assistance Program (LIHEAP)

- Tribal Assistance Eligibility Letter (TTANF)

- Nutrition Assistance Program (NAP)

Traditionally, online shopping has been skewed towards those with higher disposable incomes and access to credit cards. By allowing access to Prime benefits through participation in various government assistance programs, Amazon is broadening the scope of the online retail market. This move democratizes the market for commerce by offering the same conveniences and advantages of online shopping to a demographic that has only recently become the focus of enterprise retailers:

Consider it the new direct-to-consumer retail. Shipping orders directly from their origin factories keeps prices low. Shein, the Chinese ultra-fast-fashion giant, has taken the world by storm and continues to grow in magnitude, dwarfing the SKU counts and volume of sales of competitors like Zara, H&M and Boohoo. The clothes are cheap, disposable, and addicting. Temu could fulfill a similar desire for “cheap yet good-enough” products – especially as America’s historic run of inflation continues to tilt consumer prices upward.

Chinese-owned, cross-border commerce companies like Shein and Temu are laser-focused on this demographic but few can reach them like Amazon. It’s the ease of purchase, the product availability, the pricing transparency, and the proximity to consumer. Relevant to this conversation, there’s rumor that Amazon may acquire 500 locations that Albertsons and Kroger plan to divest. These stores would enable Amazon to grow its Amazon Fresh option, a more economical source of goods than what’s commonly found at Whole Foods. In short, Whole Foods can only scale so much.

In a letter to shareholders in early April, Amazon CEO Andy Jassy said the grocery business, which has struggled to get off the ground, needs to be a focal point of the company’s strategy. Back in 2017 Amazon paid $13.7 billion for the Whole Foods chain, but that has come with bumps and bruises. Amazon also has been forced to close Amazon Go and Amazon Fresh locations, and has laid off thousands of workers. Amazon announced in February it was pausing the rollout of its Amazon Fresh stores while it re-evaluated the concept’s economics.

The awareness of this program and the further democratization to follow is not without its potential downsides. One such concern lies in the implications of Amazon enabling impulse purchases, during periods of great economic uncertainty, for essentials such as groceries and in-home needs with a credit card. With the convenience of one-click purchases and the temptation of a vast array of products, consumers may find themselves spending beyond their means, which could lead to increased levels of debt.

While this is a potential risk, it’s important to note that the convenience of online shopping, particularly for essentials, can also serve as a financial planning tool. For example, the ability to compare prices and products can help shoppers make more informed decisions, potentially saving money in the long run. Additionally, the convenience of home delivery can save on transportation costs, especially for those living in food deserts or areas with limited access to stores.

Amazon’s evangelism of Prime Access underscores the transformative power of membership-driven, app-based eCommerce in grocery and household goods. By advertising democratized access to its Prime services, Amazon is not only expanding its potential growth but also paving the way for more inclusive commerce. At the same time, this development highlights the need for consumer education to mitigate the potential for increased debt. As the eCommerce market continues to evolve, it’s crucial that advancements in convenience and accessibility are balanced with measures to promote responsible spending.

By Web Smith | Edited by Hilary Milnes with art by Alex Remy and Christina Williams

Memo: Redefining The Revenue Model in CPG

It’s been a boom season for consumer packaged goods and perishable foods brands. This growth skewed heavily towards those properly positioned to benefit from omnichannel distribution and it punished many who rely solely on direct-to-consumer and subscription models.

This week – after sitting with executives at one of America’s most prominent grocers, I was left thinking about all of the changes in how we consume the consumer packaged goods that we love. Here is what I concluded after those conversations:

You have a subscription to products that you like, you repeat purchase the products that you love. More often than not, those repeat purchases exceed the volume of the product that you’d consume if you subscribed to a monthly shipment from the same company.

Olipop and Poppi need no subscription box – they have Amazon Prime Now and DoorDash. I would venture to guess that the enthusiastic Olipop fan buys 4-5 cases of four per month ($50) through various channels. Wild Planet needs no subscription box, nor does Primal Kitchen, Bar Harbor, Organic Girl, Brad’s products, Dave’s Killer Bread, Waterloo water, Bare Bones bone broth, Bulletproof, or Force of Nature meats. Prime Now basically advertises these brands at no cost to them. Whether perishables or not, brands are losing volume to those positioned to help consumers with immediacy.

The subscription model in the food industry has been a popular trend, particularly in the past decade, with businesses offering curated boxes of ingredients, snacks, or specialty products to consumers on a regular basis. However, by 2022, the landscape had changed, with subscription box sales diminishing post-pandemic. For a deep dive on that, start here at The Subscription Crash:

Winc, Birchbox, and Blue Apron’s shrinking markets tell the story of what happens when a subscription model falls out of favor with consumers. Each company’s current concerns teach a different lesson: Winc’s DTC-only strategy diminished growth, Birchbox’s acquisition partners failed at every turn, and Blue Apron can’t seem to turn a profit. In each case, these subscription companies learned that the novelty of subscription wears off.

As a result of recessionary effects in 2021 and 2022 and the move towards retail media networks, the emphasis has shifted towards making consumer packaged goods, both perishable and non-perishable, available for immediate purchase and consumption through services like Amazon Prime Now, DoorDash, Instacart, and Thrive Market. Three of these platforms have robust retail media networks and those three (Prime Now, DoorDash, Instacart) allow for instantaneous availability of goods.

Grocery delivery is set to become a $1 trillion market by 2027 fueled by this model. What’s not included in this figure is the subscription box model. The subscription model in food has now become a form of down-side protection – which aims to “reduce the frequency and/or magnitude of capital losses, resulting from significant asset market declines” for brands looking to maximize revenue. It’s a model that protects a nonsensical (at this point) dependency on aging digital customer acquisition channels (Meta, et. al.)

As the market for grocery shifts to marketplace, this change impacts the consumer’s purchasing behavior and the CPG retailers. Traditional subscription models may actually slow sales velocity and overall volume for the best brands.

Down-Side Protection and Maximizing Revenue

In the current market landscape, the subscription model serves as a way to offer predictable (but increasingly less-reliable) steady stream of revenue through the commitment of customers to receive products periodically. This model, however, does not maximize revenue potential as it limits the frequency and volume of purchases made by consumers. For product-based brands that are truly indispensable, with high loyalty and affinity, a study of consumer behavior suggests that buyers prefer purchasing these products as needed throughout the days, weeks, or months.

Brands with a loyal customer base have a greater potential for revenue generation by catering to the convenience of purchasing products as and when required, rather than committing to a fixed subscription. This trend is particularly evident among the major grocers who benefit from buyers’ repeat purchases throughout the week, as opposed to stocking up through bulk purchases at stores like Costco or relying on traditional subscription models. By focusing on immediate purchase and consumption, brands can maximize revenue while providing a more tailored and flexible service to their customers.

Dynamic Shelf Space, Cooking Schedules, and Refrigerator Capacity

I have two subscription services that see more trash can time than freezer or refrigerator time. In fact, it’s time to cancel those subscriptions. If I cannot get them through Prime Now, DoorDash, or a like-service, I will just find a substitute. This is likely a shared consumer mindset as more products are available through grocery delivery services.

One of the key advantages of this shift towards immediate purchase and consumption is the increased flexibility it offers to consumers in terms of their shelf space, cooking schedules, and refrigerator capacity. Traditional subscription models often require consumers to plan their meal schedules around the arrival of their subscription boxes, leading to potential food waste and inefficiencies in meal preparation. By purchasing products as needed, consumers can adapt their cooking schedules to their daily routines, dietary requirements, and preferences.

Additionally, this approach allows users to be more dynamic in their shelf space and refrigerator capacity management. Traditional subscription models may result in overcrowded shelves or refrigerators, as consumers must accommodate the bulk delivery of food items. On the other hand, purchasing products as needed allows consumers to optimize their storage space, avoid clutter, and reduce food waste due to spoilage or expiration.

Rewarding CPG Retailers with Significant Brand Equity, Product Loyalty, and Affinity

The shift towards immediate purchase and consumption of CPGs not only benefits consumers but also rewards the retailers who have developed significant brand equity, product loyalty, and overall affinity. These retailers have invested in building strong relationships with their customers, ensuring high-quality products, and providing excellent customer service.

By offering products for immediate purchase, these retailers can capitalize on their brand’s reputation and loyalty to drive sales and increase revenue. This approach further strengthens the relationship between the retailer and the consumer, as it demonstrates the retailer’s understanding of their customers’ preferences and their ability to adapt to the changing market landscape.

The move towards retail media networks, as often discussed here, has also created new opportunities for CPG retailers to target their marketing efforts and engage with their audience more effectively. By leveraging these platforms, retailers can further enhance their brand presence, drive consumer engagement, and foster long-term relationships with their customers.

The decline of the subscription model is a headwind facing many companies that have relied solely on this mechanism as a second-order effect of measuring paid advertising spend (with LTV or lifetime value as the holy grail of marketing efficacy) has paved the way for a more dynamic and flexible approach to purchasing and consuming consumer packaged goods. By focusing on immediate purchase and consumption, brands can maximize their revenue potential while providing a more convenient and adaptable service to their customers.

Out: monthly recurring revenue (MRR)

The value of a customer was viewed through two lenses: lifetime value and as a unit in a larger monthly recurring revenue rate. I would argue a new measure will become accountable.

In: monthly repeat rate (MRR)

Thanks to data from platforms like Amazon Prime Now, DoorDash, or Instacart, a product retailer can measure a customer based on how often that customer buys the same product throughout the month and how that frequency of purchases lends itself to overall volume.

Summary

While subscription models can provide a predictable and steady stream of revenue for brands, they may not always be the most effective method for maximizing sales. The sales performance of brands through subscription models or Amazon Prime Now can vary depending on the specific brand, product, target market, and consumer preferences.

Brands can better understand the product’s performance by constantly assessing repeat sales (MRR) through delivery systems. The data will better assess competitive landscape and promote a better understanding of seasonal sales trends. This shift has enabled brands to capitalize on their strong relationships with customers and leverage retail media networks to further enhance their marketing efforts and brand presence.

The changing landscape of the food industry highlights the need for brands and retailers to adapt their business models to better serve the evolving preferences and needs of their customers. By embracing the shift towards immediate purchase and consumption, brands can not only maximize revenue but also foster stronger relationships with their customers, ensuring sustainability and continued growth in a highly competitive market.

By Web Smith | Edited by Hilary Milnes with art by Alex Remy and Christina Williams