Both companies set out to take on Nike and Adidas. The eventual divergence of their paths can be attributed to a number of differences in decisions: funding methods, geographies, early adopters, and design philosophies. But what ultimately set one shoe brand up for international dominance ($8+ billion market cap) and the other into survival mode ($100 million market cap) came down to this: comfort.

It can be easy to forget that Allbirds, at one time, seemed to be on the same trajectory as On. Wrote Rachel Syme in 2018 for the New Yorker:

In their initial wave of popularity, Allbirds became an essential part of the daily uniform of Bay Area tech entrepreneurs. But in the past year Allbirds have travelled outside the clean hallways of Silicon Valley headquarters and tipped into the mainstream. Mila Kunis wears Allbirds. So does Jennifer Garner. So do Park Slope dads and modern dancers and trendy teen-agers and kooky aunts and registered nurses and bartenders and pretty much every overworked, weary thirtysomething you see on the New York subway.”

The cascading effects of comfort as a variable would take volumes of essays to explain but here I will try to simplify as best I can. I wrote this about Allbirds in February of 2022 when it was still a $1.5 billion company.

Allbirds is cozying up to wholesale. It’s an interesting paradox in omnichannel strategy that takes brand awareness and unit economics into consideration. The brands with sales velocity and stature to own their distribution can and will move towards an owned-store / DTC model. Brands working to reach profitability and scale are moving towards third-party retail wholesale partnerships.

In that essay entitled “Omnichannel Nirvana“, I opined that the strongest brands are pursuing DTC strategies while brands in need of sales growth are highly reliant on wholesale partnerships. The irony of the timing of this new report is that Allbirds is still pursuing wholesale and On Running is shifting in the opposite direction, according to this report in WWD.

The Swiss sports brand reported the strongest quarter in its history Tuesday morning with a jump of 46.5 percent in net sales to 480.5 million Swiss francs, driven in large part by its direct-to-consumer business.

As a result, the company will focus primarily on its own DTC efforts going forward and stick with the wholesale partners it already has without significantly adding to its stable. DTC accounts for 35 percent of overall sales.

The journey from performance to fashion statement encapsulates the evolving dynamics of consumer preferences and market trends. Nike, Adidas, and Reebok followed this pattern. Today, it is On Running. And I suspect that it will tilt the brand’s trajectory even higher.

Phil Knight, the visionary behind Nike, initially believed that running shoes were solely meant for sports. He found out that he was wrong. Over time, basketball shoes, epitomized by brands like Nike and Adidas, became the casual footwear of choice, transcending their functional roots to become fashion staples. Without many exceptions, the trend has pivoted away from basketball and returned to running shoes as the primary exhibitor of daily wear (and fashion in some cases).

Today, brands like Hoka and On Running, renowned for their exceptionally comfortable soles, are worn casually by the executive classes, a demographic that Allbirds once firmly held thanks to the early adoption by west coast venture capitalists alluded to in the introduction. This transition from performance to casual wear reflects the changing landscape of the athletic footwear industry and consumer priorities. The great contrast between the two brands began with comfort. People wear Hoka and On because it feels good to wear the shoe. Eventually, enough people wore them that their appearance became more socially acceptable outside of running circles. Like Hoka, On shoes have a particular look that was more unconventional than their counterparts at Nike and Adidas.

Good Steps and Missteps

The rise of On Running is noteworthy and generational. Founded in 2010 by Swiss Ironman champion Olivier Bernhard, On has experienced a meteoric rise in popularity, especially in the last few years. A significant boost in its profile came in 2019 when Swiss tennis great Roger Federer became a shareholder. In 2023, On announced $490 million in net sales in the second quarter, marking its sixth consecutive best-ever quarter. The brand’s appeal transcends its athletic origins, finding favor among various consumer segments, from tech workers to boomer parents and the athleisure crowd. Keys to its growth:

- Product Innovation: On Running’s unique cloud-like cushioning technology has appealed to both serious athletes and casual wearers. Its focus on technological innovation in footwear has set it apart in terms of performance and comfort.

- Market Positioning: On Running has successfully positioned itself across multiple segments, catering to both high-performance athletes and consumers looking for comfortable, stylish footwear. This dual appeal has broadened its customer base significantly.

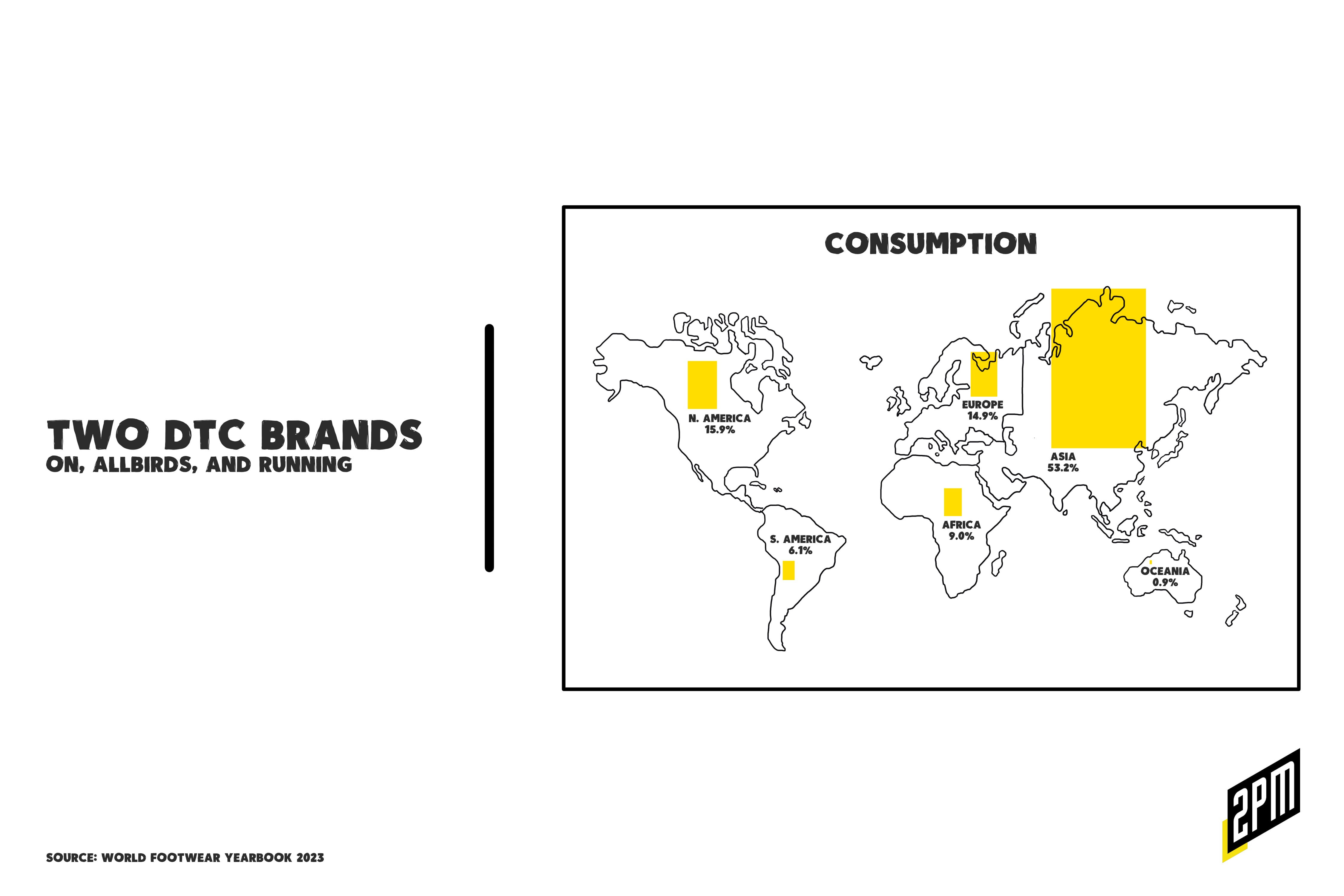

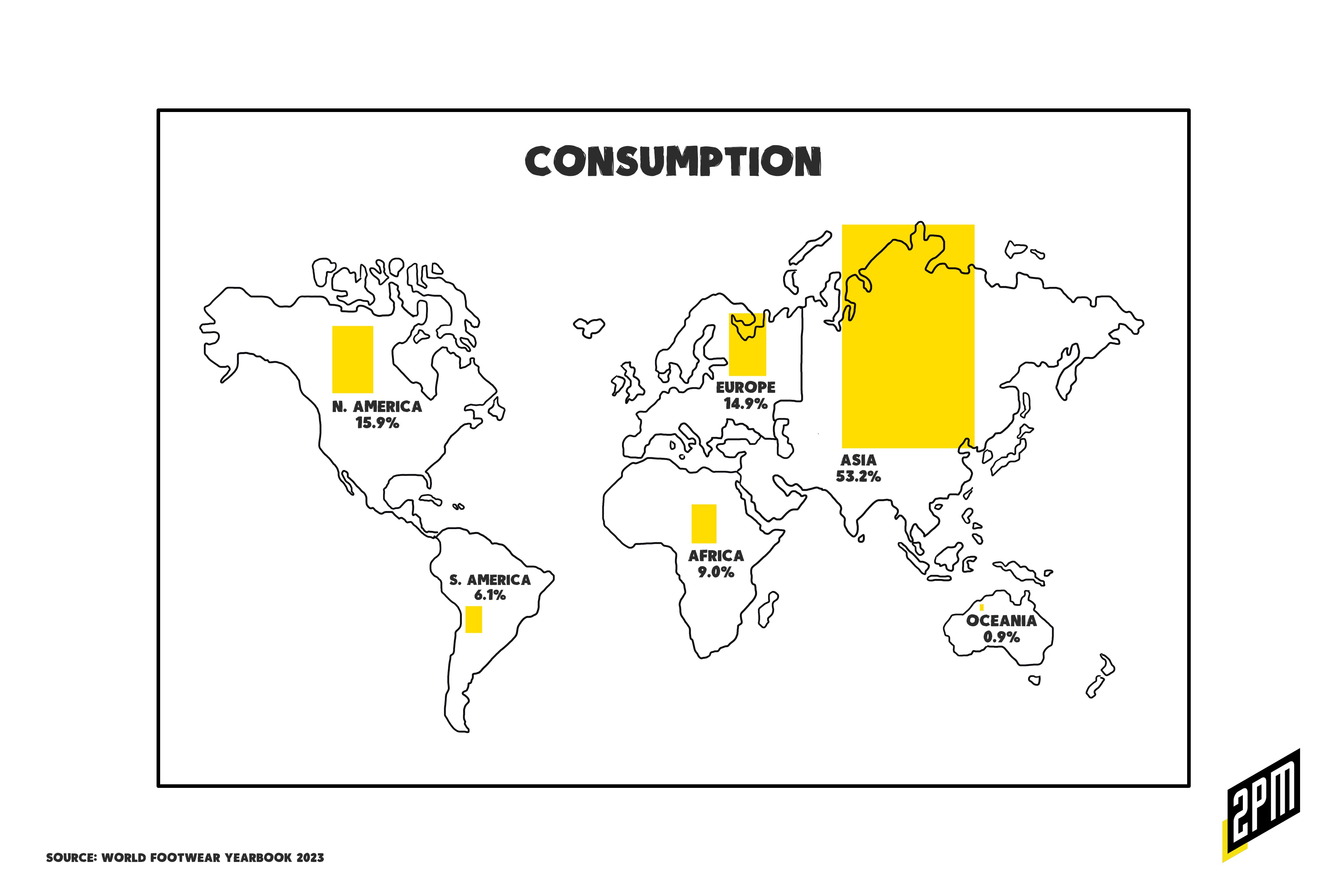

- Global Expansion: On Running has expanded its market reach globally, making significant inroads in Europe, North America, and Asia. This global presence has contributed to its growing revenue.

- Brand Partnerships: The involvement of high-profile figures like Roger Federer has boosted On Running’s brand visibility and appeal. These partnerships have helped the brand gain credibility and attract a diverse range of consumers.

On’s shoes, known for their patented CloudTec soles, have historically been relatively firm, catering to a different runner preference than the traditionally softer American market. However, their recent models like the Cloudmonster and partnerships with athletes like Kristian Blummenfelt indicate a renewed focus on athletic performance.

Allbirds, on the other hand, initially captivated the market with its sustainable Wool Runner shoes. Founded in 2016 with a sustainability bend, Allbirds quickly gained popularity, especially in tech hubs like Silicon Valley. However, as the company tried to expand rapidly into new market segments and product lines, like running shoes and apparel, it faced significant challenges. The materials used in its running shoes were not well-suited for intensive activity, leading to durability issues. Its apparel line, made entirely of merino wool, was criticized for being too warm and uncomfortable. Furthermore, Allbirds’ expansion into younger consumer demographics and other product categories without sufficient market research diluted its brand image and confused consumers about what the brand stood for. Keys to its struggles:

- Segmentation Missteps: Allbirds’ expansion into running shoes and apparel was not well-received. The materials used in their products, while sustainable, did not meet the performance and comfort expectations of the new segments they targeted, particularly in the athletic footwear market.

- Brand Dilution: The rapid expansion into various product lines and market segments diluted Allbirds’ core brand image. This lack of focus led to confusion about the brand’s identity and diminished its appeal to its original customer base.

- Pricing and Product Quality: The higher price points of Allbirds’ new products, combined with quality issues, especially in terms of durability and suitability for athletic use, led to customer dissatisfaction and lower sales.

Looking ahead, for Allbirds to reemerge successfully, a pivot in strategy may be crucial. Transitioning from a sustainability-focused brand to one that emphasizes comfort could open new avenues. Developing and patenting exceptional soles, akin to On Running’s CloudTec, could help Allbirds regain a foothold in the market. This focus on comfort, combined with its existing commitment to sustainability, could potentially redefine its brand identity and appeal to a broader consumer base. This strategic shift requires not only technological innovation but also a deep understanding of consumer preferences and market trends.

Asia As The Next Emerging Market For Running

Asia’s burgeoning market for running and athletic footwear presents significant growth opportunities for brands like On Running and Allbirds. The impact of this growth on comfort categories can be substantial, offering new avenues for market expansion and product innovation. Here are a few key points:

Rising Health Consciousness: In many Asian countries, there’s a growing trend towards health and wellness. This shift is driving an increase in activities like running, which in turn boosts the demand for high-quality running shoes. Brands that can tap into this health-conscious market with products that offer both performance and comfort are likely to see success.

Expanding Middle Class: Asia’s expanding middle class is fueling consumer spending on lifestyle and wellness products, including athletic footwear. This demographic is not only looking for functional products but also values comfort and style, blending their needs for athletic and casual footwear.

Urbanization and Lifestyle Changes: Rapid urbanization across Asia has led to lifestyle changes that blend fitness activities with daily life. As a result, there’s a growing preference for versatile footwear that serves both athletic and casual purposes, which is where the comfort category can greatly benefit.

Online Retail and Digital Engagement: The superiority of eCommerce platforms in Asia offers brands an effective channel to reach a broader audience. These platforms also provide valuable consumer data, enabling brands to tailor their products and marketing strategies to local preferences, including comfort-oriented features.

Cultural Trends and Brand Perception: In many Asian markets, Western brands are often perceived as status symbols. Brands like On Running and Allbirds can leverage this perception, emphasizing their unique value propositions in comfort and sustainability to appeal to a wide range of consumers.

Influence on Comfort Categories: The emphasis on running and athletic footwear in Asia is likely to have a trickle-down effect on comfort categories. Consumers who prioritize performance in their athletic wear also seek comfort in their everyday footwear. This overlap creates opportunities for brands to develop products that cater to both needs.

Asia’s growing market for running and athletic footwear is the key area for future growth in this segment, with significant implications for the comfort category. Both can effectively tap into this market by balancing performance, comfort, and style, and adapting to local preferences, stand to gain a significant competitive advantage in this rapidly evolving market landscape.

Allbirds will need to refocus on its core strengths while also innovating in product comfort and performance. Developing and patenting new technologies for soles, similar to On Running’s approach, could help turn it around. This strategic shift should be accompanied by a renewed focus on understanding and catering to its target segments’ needs, particularly around comfort, sustainability, and performance.

The stories of On Running and Allbirds in the athletic footwear industry offer valuable lessons in brand positioning, market segmentation, and the importance of aligning product offerings with consumer expectations. While On Running has successfully navigated these challenges, Allbirds has faced hurdles. However, with the strategic pivot mentioned above, Allbirds could potentially reclaim its position in the market. In the same New Yorker article, Syme wrote: “I have never been the kind of person who selects my shoes based on their orthopedic function.” The irony for high flying running shoe brands like Hoka and On is that this was their appeal before appeal was their appeal. And with that, more consumers prioritized comfort over appearance. Even Adidas and Nike have taken note.

Over four years, emerging sportswear companies Hoka and On Running spent the equivalent of what Nike spends in two weeks to grow their market shares — and added $3 billion worth of revenue over that period, according to TD Cowen. (Business Insider, 2023)

Allbirds can learn from this. Nike is focused on China to continue growing market share. The athletic footwear industry continues to evolve, and brands that can adapt to changing consumer preferences while maintaining a clear and consistent brand identity are likely to succeed in this competitive landscape. This is the tale of the two DTCs.

By Web Smith | Edited by Hilary Milnes with art by Alex Remy and Christina Williams