Adding my drivers license to my Apple Wallet was revelational; the screen was less a convenience and more a necessity. Then it got me thinking: loyalty, visibility, transactional power, and identity. The Apple Wallet is one of the most significant pieces of digital real estate for brands – DTC, enterprise, and everything in between.

With the recent announcement that California residents will soon be able to add their driver’s licenses and state I.D.s (joining Arizona, Maryland, Colorado, Georgia, and Ohio) to Apple Wallet, the implications for both consumers and brands are profound. This move signals a shift towards a future where the Apple Wallet screen—especially the area above the fold—becomes an essential touchpoint for brands aiming to deepen their relationships with consumers. It becomes a loyalty play, an engine to allow them to remain top-of-mind. This space’s high visibility and frequent usage will make it invaluable for brand engagement, particularly among high-earners-not-rich-yet (H.E.N.R.Y.s) who are known for their discerning tastes and desire to signal brand affinity and status. This is a psychographic that I will use to denote key consumers in the Gen Z and Millennial demographics.

The Apple Wallet as Prime Digital Real Estate

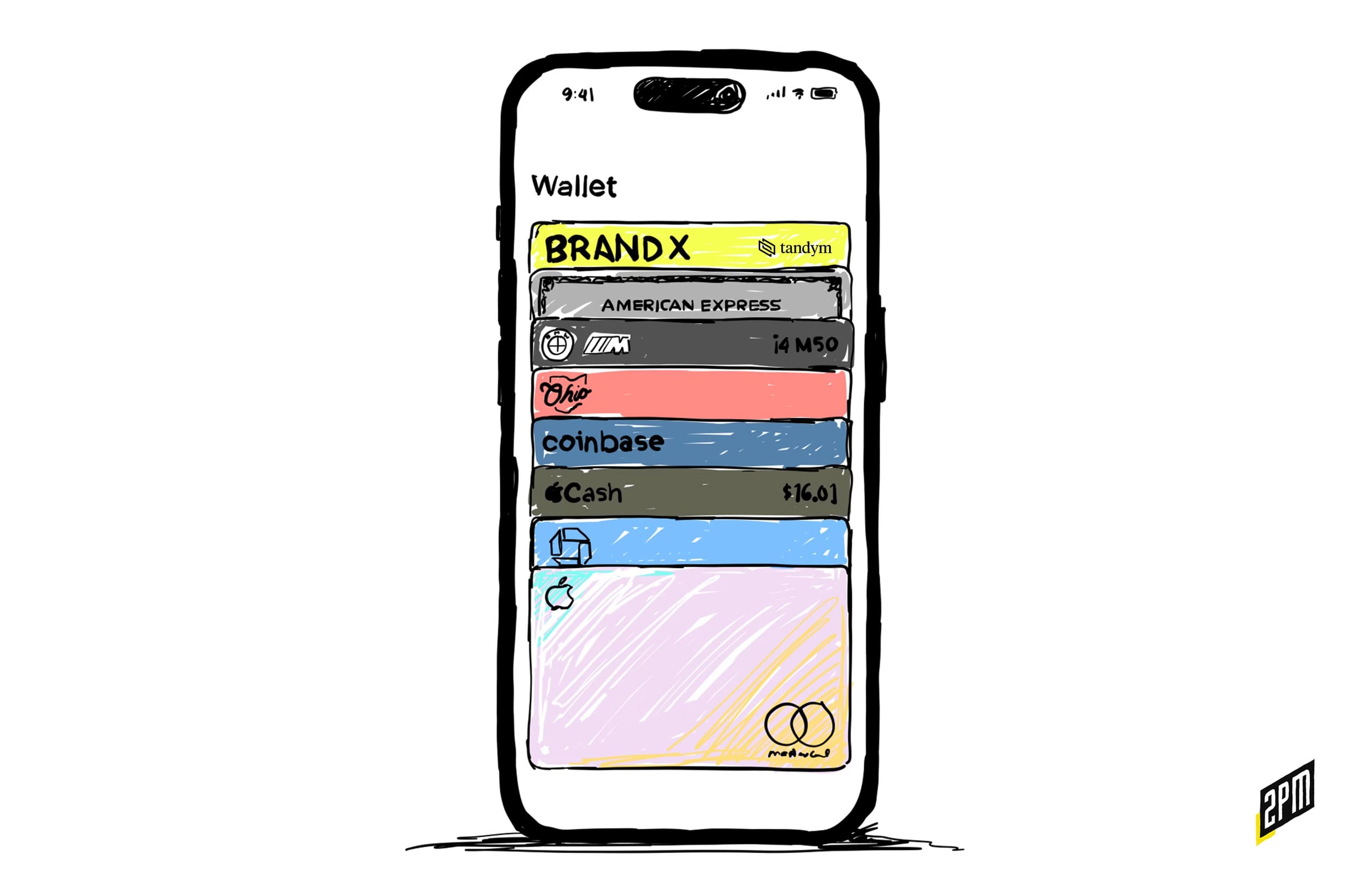

The Apple Wallet is waiting for the first co-branded credit card; a DTC powerhouse and the card’s provider. Which brand would you want to see in your wallet every day? I can name a few.

It’s no longer just a convenient app for storing credit cards and boarding passes. It is quickly becoming a central hub for all forms of identification and access. The Wallet’s role in daily life is expanding. As The Verge reported, this fall, some California residents will be able to participate in a pilot program allowing them to add their driver’s licenses and state I.D.s to Apple Wallet. This pilot is part of a broader trend where digital I.D.s are becoming more commonplace. What happens when Apple authorizes every state in the union?

This expansion of digital I.D.s within Apple Wallet means that users will interact with the app more frequently. Whether they’re going through airport security, purchasing age-restricted products, or simply proving their identity, users will open their Apple Wallet multiple times a day. This increased usage transforms the Wallet screen into prime digital real estate, particularly the area above the fold, which is the first thing users see when they open the app. Brands that secure a presence in this space can achieve daily consumer interaction, making it a powerful tool for brand reinforcement and customer loyalty. And, as of yet, Apple cannot control it.

Above the Fold: A New Battleground for Brand Visibility

The concept of “above the fold” originates from the newspaper industry, where the most important stories were placed on the upper half of the front page, above the literal fold, to attract attention. In the digital age, this concept has been adapted to websites, where the most crucial content is placed at the top of the page before users scroll. With the increasing significance of the Apple Wallet, the “above the fold” area of the Wallet screen is becoming one of the most coveted spaces for brands.

When a user opens their Apple Wallet, the first cards they see are those that reside above the fold. These cards are likely to include their most frequently used payment methods, co-branded credit cards, digital car keys, and digital I.D.s. For brands, being visible in this area resembles having prime billboard space in the busiest part of town. Every time a user opens their Wallet, they are exposed to the brand’s presence, reinforcing brand recognition and fostering a sense of familiarity.

For H.E.N.R.Y.s, who are often on the cutting edge of technology adoption, the Apple Wallet’s above-the-fold section becomes a digital expression of their lifestyle and values. These consumers will likely curate their Wallet to reflect their brand affinities and status, keeping certain cards or I.D.s in prominent positions as a subtle signal of their preferences and social standing.

H.E.N.R.Y.s and the Power of Brand Affinity

H.E.N.R.Y.s (“High Earners, Not Rich Yet“) represent a unique consumer segment characterized by their substantial disposable income, yet they are not typically classified as wealthy. This demographic is particularly attractive to brands because they have the financial means to make aspirational purchases and are highly brand-conscious. For H.E.N.R.Y.s, the brands they choose to associate with are more than just providers of goods and services; they are extensions of their identity.

The Apple Wallet offers H.E.N.R.Y.s a powerful platform to signal their brand affinities. For instance, having a premium credit card or a membership to an exclusive club stored in a prominent position in their Wallet can serve as a potent status symbol, visible each time they use their device. This is akin to how physical wallets once displayed gold or platinum cards as indicators of financial success, but in a more digital and dynamic form.

Brands targeting H.E.N.R.Y.s must recognize the potential of the Apple Wallet as a status-signaling tool. By offering digital cards that convey exclusivity or prestige, brands can deepen their relationships with this demographic. For example, a luxury brand could offer a co-branded, digital loyalty card that provides rewards and features exclusive design elements or limited-time offers that appeal to the H.E.N.R.Y.’s desire for unique, high-status experiences.

Privacy and Security: A Key Consideration

While the Apple Wallet presents a significant opportunity for brands, it is also essential to address the privacy and security concerns that come with storing sensitive information in a digital format. As The Verge recently noted, state-run mobile I.D. programs have sparked debates about potential security risks, including the possibility of third parties accessing users’ information or law enforcement using mobile I.D.s as a pretext to seize phones.

Apple has made assurances that I.D.s stored in Apple Wallet are secure and cannot be accessed by third parties, including Apple itself. According to Apple’s press release, driver’s license information added to Apple Wallet is only stored on the user’s device and is not accessible unless the user chooses to present it. This level of security is crucial for maintaining consumer trust, especially for H.E.N.R.Y.s, who are likely to be highly aware of the importance of data privacy.

The Future of Brand Engagement in the Apple Wallet

As the Apple Wallet continues to evolve beyond movie passes and debit cards, it is poised to become one of the most important digital platforms for brand engagement. The integration of the above mentioned categories of cards means that the Wallet will be a frequent touchpoint in users’ daily lives. For brands, particularly those targeting H.E.N.R.Y.s, securing a presence in the above-the-fold section of the Apple Wallet offers an unparalleled opportunity to deepen relationships with consumers. This trend is likely to continue, making the Apple Wallet a key platform for brand engagement in the future.

The Apple Wallet’s transformation into a central hub for digital identity and access is not just a convenience for users; it is a strategic opportunity for brands. By understanding the importance of this digital real estate and how it can signal brand affinity and status, brands can position themselves to engage with consumers meaningfully and meaningfully. As digital I.D.s become more common and the Wallet’s role in daily life expands, this screen will become as valuable as the traditional home page, if not more so, for brands aiming to connect with today’s discerning consumers.

Research and Writing by Web Smith