Cada semana aparece un nuevo minorista en apuros. Es hora de plantearse hasta qué punto la economía minorista estadounidense se construyó sobre una clase de consumidores que nunca fue tan estática como se creyó: la clase media.

Muchas marcas minoristas, mercados y grandes almacenes heredados se encuentran en un callejón sin salida. Durante décadas, se dirigieron con éxito a un grupo de estadounidenses que ni subía ni bajaba de su posición económica. Cuando esa cohorte de consumidores se enfrentaba a pérdidas de empleo u otras incertidumbres financieras, los minoristas respondían ofreciendo promociones para atraerlos a sus tiendas. En la década anterior, esos esfuerzos promocionales no cejaron. Pocos ejecutivos del comercio minorista parecían tener en cuenta las tendencias sociológicas a más largo plazo que influyen en la clase social y la confianza de los consumidores.

Pensemos en las dificultades actuales de Ralph Lauren Corporation (RL). Según un informe de Credit Suisse, las ventas digitales del minorista crecieron sólo un 3% en el segundo trimestre de 2020. Esto se produjo en un contexto de crecimiento histórico del comercio minorista en línea. Las acciones cotizan actualmente cerca de mínimos de cinco años; gran parte puede atribuirse a su pobre estrategia promocional y a la falta de inversión en el negocio directo al consumidor. Según Retail Dive:

La marca también señaló en sus reuniones con Credit Suisse que planea tomarse la pandemia como un momento para pasar agresivamente de los clientes en línea de bajo valor y buscar clientes de mayor margen, un grupo demográfico que la empresa cree que será más complaciente con sus recientes aumentos de precios, la reducción de promociones y la selección de productos de gama más alta. [3]

Ralph Lauren y sus colegas, un producto de los años 80, asumieron que algunas cosas nunca cambiarían. Pero no fue así.

Del extremo sur a la costa norte

Como muchos niños de los 80, devoraba películas como The Breakfast Club, Sixteen Candles, Ferris Bueller's Day Off y Uncle Buck. Las películas eran idílicas. Desde las imágenes de prosperidad económica hasta la confianza de los personajes, todo me atraía. No fue hasta que fui adulto cuando me di cuenta de las implicaciones culturales que servían de telón de fondo a la obra de John Hughes: la propia ciudad fracturada.

El Sr. Hughes, cuyo padre era vendedor de tejados, utilizó estas comunidades para explorar cuestiones de clase, estatus y consumismo, así como la tensión y atracción entre suburbio y ciudad en la América de los 80. [1]

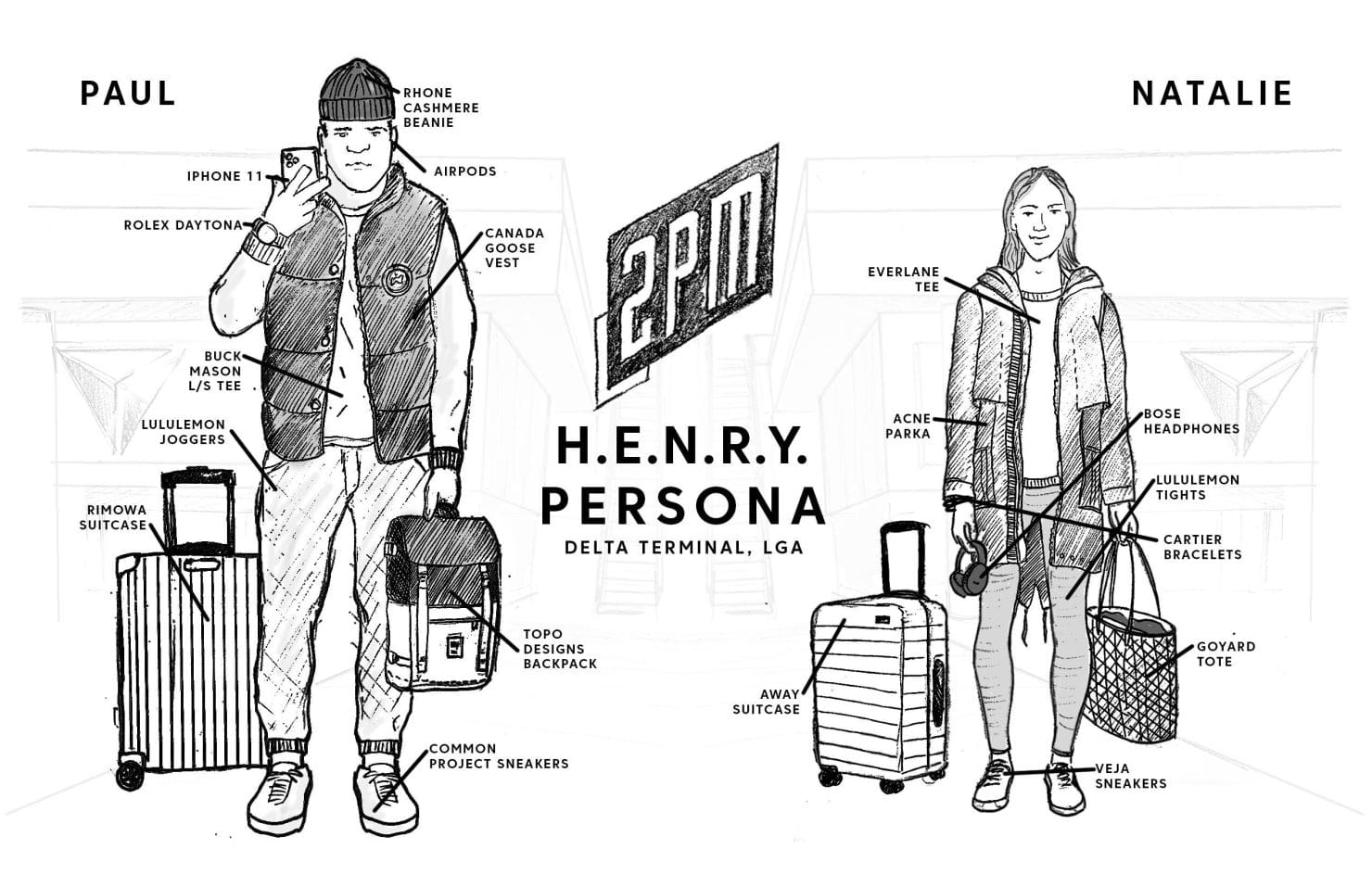

La base del informe Regarding HENRY de 2PM fue el libro de Lisa Birnbach de los años ochenta, The Official Preppy Handbook. Ese libro, junto con la obra de Hughes, proyectó una imagen de riqueza ascendente, facilidad y seguridad a toda una generación de consumidores.

El libro fue escrito para lo que entonces se llamaba Yuppies: una persona joven con un trabajo bien pagado y un estilo de vida a la moda. Publicado originalmente en octubre de 1980, el libro fue coescrito y editado por Lisa Birnbach e ilustrado por Oliver Williams. El manuscrito pasó a un segundo plano tras las ya icónicas ilustraciones, que sirvieron de guía a consumidores y marcas durante casi dos décadas. Era algo más que una estrella del norte para saber dónde ir a la escuela, o de fiesta los fines de semana, o a qué clubes sólo para socios había que apuntarse.[2PM, 2]

Al igual que en la obra de Hughes, la costa norte de Chicago está omnipresente en la sátira de Birnbach sobre la riqueza y la clase social en Estados Unidos. Mi fascinación juvenil por el Chicago de Hughes fue sustituida por otra más inquisitiva cuando empecé a visitar la ciudad entre los 20 y los 30 años.

Estados Unidos se está bifurcando social, política y económicamente. En estos escenarios, las masas se mueven hacia uno de los dos polos proverbiales. En muchas ciudades, no puede haber uno sin el otro. En Chicago, los polos son también literales. A lo largo de las décadas -con una atención cada vez menor a la consecución de una clase media estable- algunos recursos se desplazaron de la clase trabajadora hacia el crecimiento de la clase alta. La mayoría de los recursos se malgastaron en otros lugares, lo que agravó la desventaja de la clase trabajadora. En tan sólo 45 minutos en coche por el Gran Chicago, se pueden observar dos mundos distintos de atributos diametralmente opuestos: guerra frente a paz, lucha frente a facilidad, escasez frente a abundancia.

Esta parte de la región del Medio Oeste, a lo largo del lago Michigan, es un ejemplo vivo de la Doctrina del Flujo y la Unidad de los Opuestos de Heráclito[5]. Heráclito, filósofo griego que vivió alrededor del año 500 a.C., afirmaba que cada opuesto es inseparable. Los opuestos dependen el uno del otro; esta dependencia forma la identidad de cada opuesto. Si uno de los dos desaparece, también lo hará el otro, según el filósofo.

Imagina dos mundos opuestos separados por 25 millas y empezarás a entender las disparidades de Chicago. El diseño de la ciudad ha reforzado esta división. Hay barreras físicas, puentes que se pueden levantar y una tensión silenciosa entre los que tienen y los que no tienen. Desde hace poco, la tensión ha crecido más allá de lo silencioso y de las fronteras artificiales. Un ciudadano que vive en el extremo sur de la ciudad tiene un salario medio de 26.400 dólares, según un artículo de 2018 en The Atlantic. Sin embargo, una asombrosa cuarta parte de los ciudadanos de la ciudad ganan por encima de los 100.000 dólares. Según Redfin, el precio medio de la vivienda en la zona de North Shore de Winnetka es de 1,28 millones de dólares. Las tasas de desempleo respectivas de las zonas norte y sur son del 4,7% y el 16%, según el mismo informe. Uno no puede existir sin el otro; ambos lados aprietan el medio.

La última vez que visité Chicago, lo vi con mis propios ojos. En agosto, conduje desde el aeropuerto O'Hare hacia el bloque 100 de la calle 132 Este para visitar a la abuela de un viejo amigo. Me quedé en su casa unos 45 minutos, pero la impresión fue duradera. Todas las personas con las que me encontré deseaban la movilidad literal y figurada que muchos de los que lean esto darán por sentada. En la semana siguiente, seis vecinos de la zona morirían a menos de un kilómetro y medio del porche donde me senté. El barrio de Eden Garden de Chicago tiene una intensidad que no se comprende hasta que se está allí.

Me dirigí desde la calle 132 Este y a lo largo de la Ruta 41. Una carretera junto al lago me condujo desde el South Side de la ciudad hasta Evanston, una de las zonas más notables de la North Shore y sede de la Northwestern University. Este es el Chicago de John Hughes y Lisa Birnbach. La experiencia fue diametralmente opuesta a mis 45 minutos en otro lugar: paz, tranquilidad y abundancia. Me sentí lo suficientemente cómodo en ambos mundos como para poder evaluar su impacto en el otro.

En todas las ciudades se encuentran estas líneas de demarcación, aunque pocas son tan claras como las de Chicago. La pandemia ha acelerado la remodelación de los grupos definidos por estas líneas.

Por un lado, el trabajo a distancia es práctico y deseable. El acceso al capital permite ganancias a corto plazo en el mercado de valores. Las cuentas de ahorro y las bajas tasas de desempleo garantizan la continuación de la vida dentro de la nueva normalidad. Es como si este periodo de dificultades económicas no hubiera existido en absoluto.

En el South Side, el trabajo asalariado y los ingresos exigen una presencia física y una tolerancia al riesgo para la salud. Estos son los dignos trabajadores por hora que hacen que nuestra economía se mueva, aunque no reciben ningún reconocimiento por ello. Su acceso al capital es escaso o nulo; no pueden aprovecharse de las ganancias récord del mercado durante los máximos históricos del desempleo. Ni siquiera hay acceso WiFi capaz para muchos. Para estos ciudadanos, nada es igual que antes del cierre. Los asuntos encontraron la manera de involucionar aún más. Y para un subconjunto de ellos, las circunstancias imposiblemente duras han empeorado. El aprendizaje a distancia es obligatorio para las familias que no pueden trabajar desde casa o mantener la infraestructura necesaria para aprender a distancia.

Este es el telón de fondo. Los minoristas estadounidenses sufrieron porque no previeron la bifurcación de riqueza, acceso y humanidad que se les venía encima. Cuando se revisa una lista de quiebras y cierres, se observa que se inclinan hacia empresas que han construido estrategias en torno a una clase media perpetua. Pero en mi viaje por la Ruta 41, no había clase media que observar. Para que nuestra economía de consumo (que da empleo a casi 30 millones de estadounidenses) recupere su forma, las empresas minoristas tendrán que entender el mensaje central de "HENRY". La clase media nunca fue realmente estática.

HENRY revisitado

La denominación HENRY es la abreviatura de "high earners not rich yet" (personas con altos ingresos que aún no son ricas). El sistema de identificación por acrónimos se ha hecho popular entre los analistas, sin embargo, esta clasificación de consumidores ha sido ignorada en gran medida por las empresas minoristas.

Con siglas o sin ellas, la pandemia ha sido testigo de este fenómeno. El acceso a escapadas suburbanas, las ventajas del trabajo o la educación a distancia y el volumen de transacciones diarias fueron sólo algunos de los signos reveladores. En Nueva York y Brooklyn, los residentes huyeron a Nueva Inglaterra y los Hamptons. En el Medio Oeste, la península superior de Michigan fue un punto caliente para este grupo psicográfico. En la costa oeste, los alquileres en los suburbios de la zona de la bahía crecieron mientras los alquileres en la ciudad caían hasta un 15%.

Cuando Ralph Lauren Corporation cita una estrategia para modernizar su negocio mediante la creación de "perfiles de cliente inteligentes", es a la designación HENRY a la que se refiere la marca.

Los HENRY son avanzados, no necesariamente quienes han superado el listón de la riqueza para acceder a la élite estadounidense. De hecho, muchos trabajan para abandonar la clase media como si fuera una mancha en sus ambiciones personales. En este sentido, el término es más inclusivo que el apelativo yuppie de antaño. También es un síntoma de nuestra economía actual, en la que el coste de la vida puede empezar a erosionar las inversiones a largo plazo, como los bienes inmuebles, los fondos del mercado monetario u otras acciones.[2PM, 2]

Como escribió Heráclito, "la vida es flujo". La atención a la identificación temprana de los ascendentes es algo que se convertirá en habitual en el marketing y la creación de marcas. Mientras que las métricas de objetivos como el coste de adquisición del cliente (CAC) y el valor del ciclo de vida (LTV) dominan el comercio electrónico, yo diría que surgirá otra: la duración de la fidelidad (DOL). Las marcas identificarán pronto a determinados clientes y los seguirán a lo largo de su formación y su carrera, una estrategia que se practica habitualmente en el sector del automóvil.

A medida que las empresas minoristas como Ralph Lauren empiecen a dirigirse de forma inteligente a la clase media, los días de esfuerzos promocionales superficiales darán paso a la noción de flujo. Al dirigirse adecuadamente a estos clientes, la esperanza es que muchos se mantengan fieles a medida que ascienden a mayores ingresos discrecionales y mayor consumo.

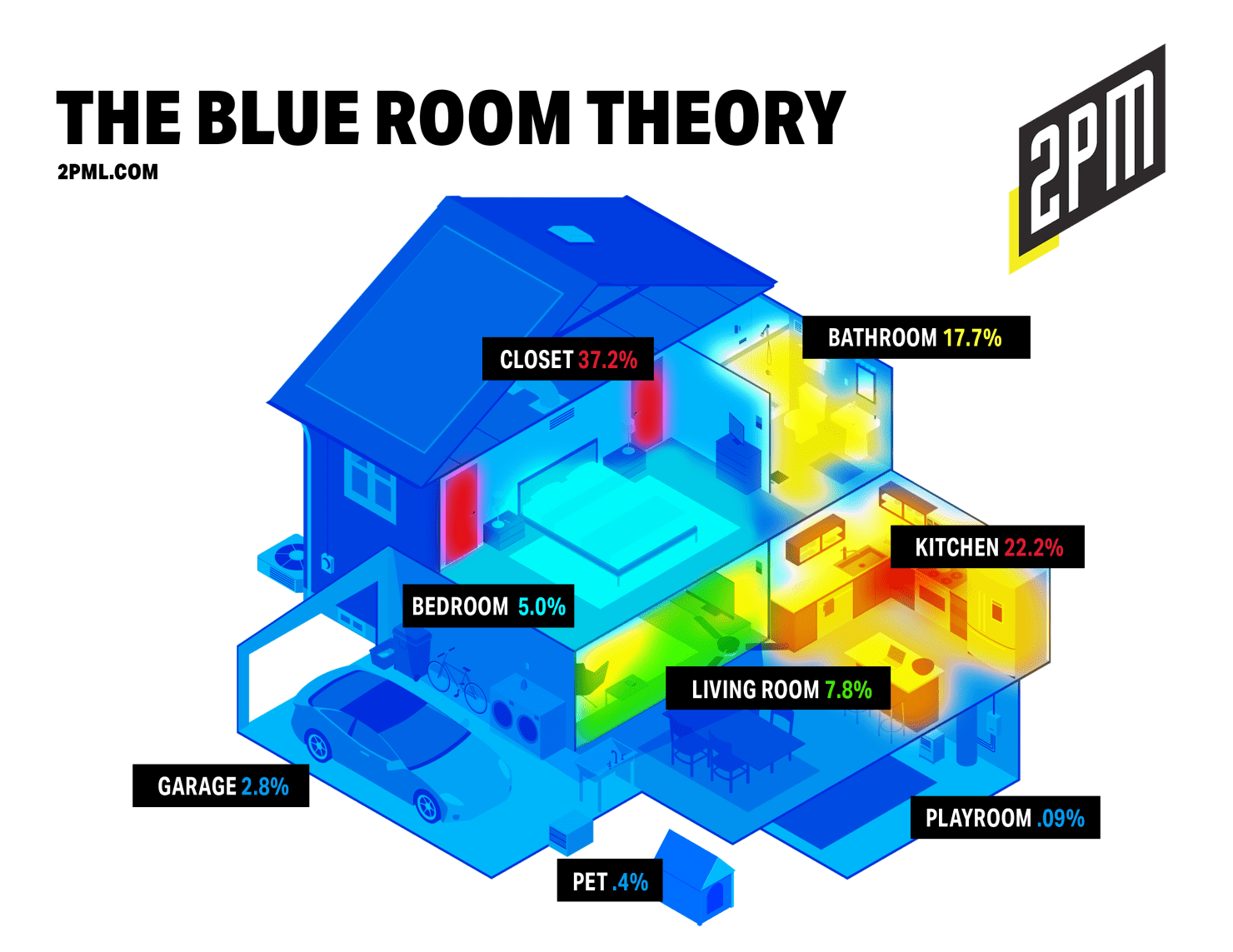

En Sanitized Urbanization, 2PM analizó la tendencia general de los urbanitas a trasladarse a zonas suburbanas. En todo Estados Unidos, las personas con movilidad ascendente buscaban la paz, la facilidad y la abundancia exurbanas. Algunos buscaban un traslado permanente. En teoría, estas zonas ofrecían un ritmo más tranquilo, aire más limpio y comercios locales que funcionaban. Eran cosas que antes se consideraban esenciales, hoy son lujos. En estas zonas, servicios como parques y playas proporcionaban una sensación de normalidad.

La urbanización saneada elimina los riesgos percibidos de vivir en zonas urbanas al tiempo que añade el valor de -lo que suele ser- infraestructuras mejoradas, mejores escuelas y bases impositivas más bajas. Es probable que se convierta en una cuestión politizada una vez que los municipios urbanos empiecen a sufrir toda la fuerza de la migración lejos de los centros urbanos.[2PM, 4]

Como muchos otros fenómenos, la pandemia aceleró las tendencias existentes: urbanización desinfectada, trabajo a distancia, venta al por menor en línea, fitness en casa y una dependencia cada vez menor de los vehículos personales. Para los profesionales que se sentían cómodos con esta economía cambiante, muchos de ellos lograron avances financieros a pesar de la vulnerabilidad de la economía. La vulnerabilidad nunca se ha distribuido por igual. Uno de los últimos bastiones de la movilidad económica son los más de 29 millones de empleos en el comercio minorista de Estados Unidos. Para proteger lo que queda de ellos, los minoristas deben empezar a ver el mercado de esta manera. Los estirados ejecutivos de la industria minorista parecen carecer de la capacidad y la previsión para hacerlo.

Esta cohorte de profesionales es una muestra representativa de raza, etnia y sexo, aunque muchos comparten rasgos similares en cuanto a calidad de la educación, carrera profesional y posición social. Este grupo psicográfico se convertirá en el estudio clave en los próximos cinco a diez años del desarrollo del marketing y la comunicación en el comercio minorista. HENRY está empezando a hacer honor a su nombre. Hay una nueva guardia de líderes creativos, capitalistas en solitario y ejecutivos ascendentes que lo demuestran.

Por Web Smith | Redacción: Hilary Milnes | Arte: Alex Remy | About 2PM

Informe original: Sobre H.E.N.R.Y.