Every week, there is a new retailer in distress. It’s time to consider how much of America’s retail economy was built on a class of consumers that was never as static as once believed: the middle class.

Many legacy retail brands, marketplaces, and department stores are at an impasse. For decades, they successfully marketed to a group of Americans that would neither rise nor fall from their economic standing. When that consumer cohort faced job losses or other financial uncertainties, retailers responded by offering promotions to attract them to their stores. In the previous decade, those promotional efforts haven’t let up. Few retail executives seemed to consider the longer-term sociological trends that impact class and consumer confidence.

Consider Ralph Lauren Corporation’s (RL) current struggles. According to a Credit Suisse report, the retailer grew digital sales just 3% in Q2 of 2020. This was against the backdrop of historic online retail growth for retailers. The stock is currently trading near five-year lows; much can be attributed to their poor promotional strategy and a lack of investment into direct-to-consumer business. According to Retail Dive:

The brand also noted in its meetings with Credit Suisse that it plans to take the pandemic as a time to aggressively pivot from low-value online customers and pursue higher-margin customers, a demographic which the company believes to be more accommodating of its recent price increases, reduced promotions and higher-end selection of products. [3]

A product of the 1980s, Ralph Lauren and its peers assumed that some things would never change. That didn’t hold true.

From the Far South to the North Shore

Like many children of the ’80s, I devoured films like The Breakfast Club, Sixteen Candles, Ferris Bueller’s Day Off, and Uncle Buck. The films were idyllic. From the images of economic prosperity to the confidence of the characters, I was drawn to it all. It wasn’t until I was an adult that I realized the cultural implications that served as the backdrop of John Hughes’ work – the fractured city, itself.

Mr. Hughes, whose father was a roofing salesman, used these communities to explore issues of class, status and consumerism as well as the tension and attraction between suburb and city in ’80s America. [1]

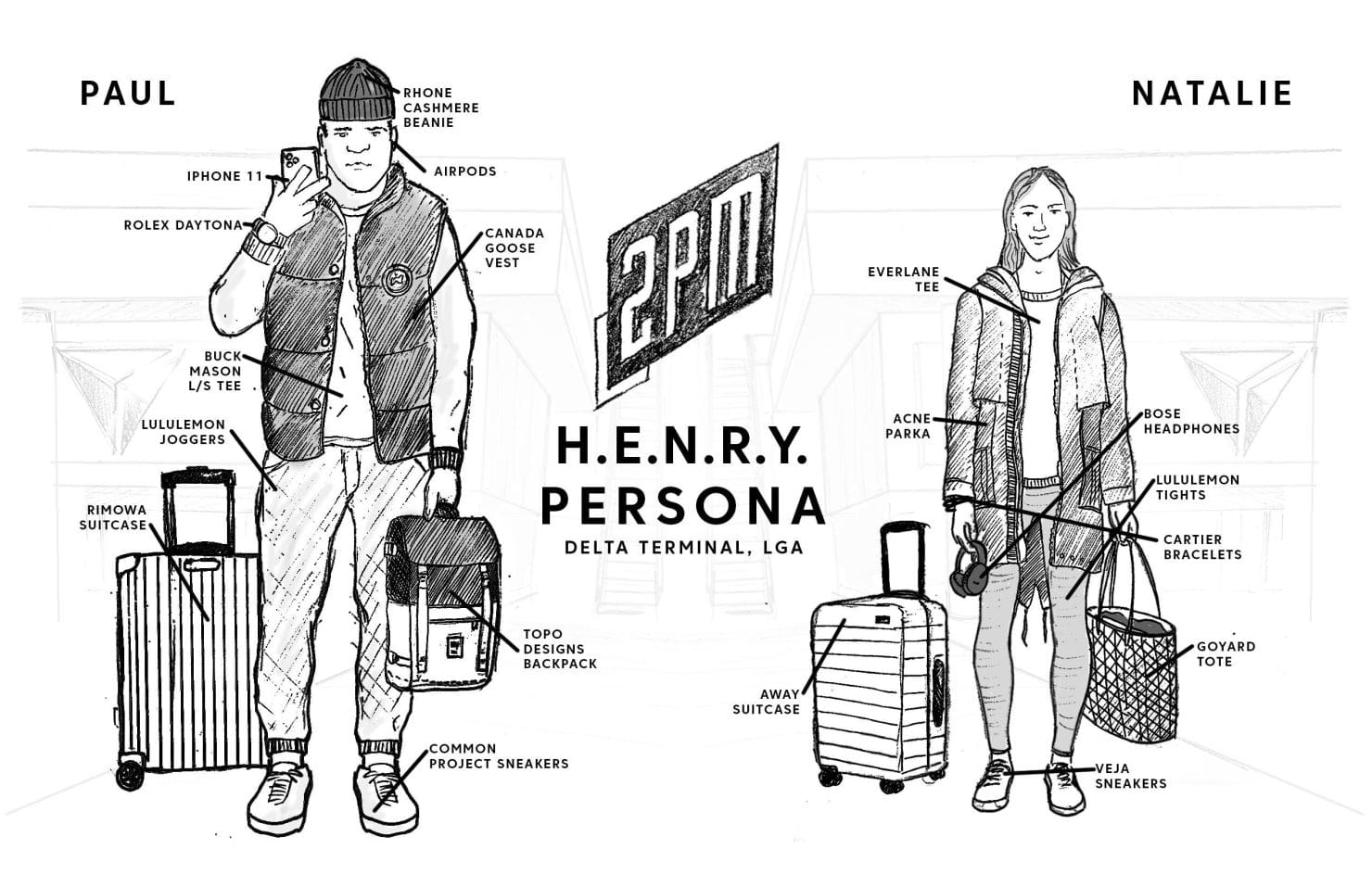

The basis of 2PM’s Regarding HENRY report was the 1980s Lisa Birnbach book, The Official Preppy Handbook. That book, along with Hughes’ work, projected an image of ascendant wealth, ease, and certainty to an entire generation of consumers.

The book was written for what was then called Yuppies: a young person with a well-paid job and a fashionable lifestyle. Originally published in October of 1980, the book was co-authored and edited by Lisa Birnbach and illustrated by Oliver Williams. The manuscript played second fiddle to the now-iconic illustrations, ones that served as a guide for consumers and brands for nearly two decades. It was more than a north star for where to go to school, or party on weekends, or which members-only clubs to apply to. [2PM, 2]

Like Hughes’ work, Chicago’s North Shore is omnipresent throughout Birnbach’s satirical take on wealth and class in America. My youthful fascination with Hughes’ Chicago was replaced by a newer, more inquisitive one as I began to visit the city in my 20s and 30s.

America is bifurcating socially, politically, and economically. In these scenarios, the masses move towards one of two proverbial poles. In many cities, there cannot be one without the other. In Chicago, the poles are also literal. Over decades – with a diminished focus on achieving a steady middle class – some resources shifted away from the working class and towards growing the upper class. Most of the resources were misspent elsewhere, furthering the disadvantage of the working class. In just a 45 minute drive through Greater Chicago, you can observe two distinct worlds of diametrically opposed attributes: war versus peace, struggle versus ease, shortfall versus abundance.

This part of the Midwest region along Lake Michigan is a living example of Heraclitus’ Doctrine of Flux and the Unity of Opposites [5]. A Greek philosopher who lived around 500 B.C., Heraclitus claimed that each opposite is inseparable. The opposites depend on one another; this dependence forms the identity of each opposite. If one of the pair disappears so will the other, according to the philosopher.

Imagine two contrasting worlds separated by 25 miles and you’ll begin to understand Chicago’s disparities. The design of the city has bolstered this divide. There are physical barriers, bridges that can be lifted, and a quiet tension between the haves and the have nots. As of recently, the tension has grown beyond quiet and beyond the artificial borders. A citizen who lives in the city’s far South Side has a median wage of $26,400, according to a 2018 article in The Atlantic. However, an astonishing one-fourth of the city’s citizens earn north of $100,000. According to Redfin, the average home price in the North Shore area of Winnetka is $1.28 million. The respective unemployment rates of the North and South Sides are 4.7% and 16%, according to the same report. One cannot exist without the other; both sides squeeze the middle.

When I last visited Chicago, I saw it for myself. In August, I drove from O’Hare Airport towards the 100-block of East 132nd Street to visit an old friend’s grandmother. I stayed at her home for 45 minutes or so, but the impression was lasting. Everyone that I encountered wanted the literal and figurative mobility that many who read this will take for granted. In the week that followed, six local residents would die within one-fourth of a mile from the porch where I sat. The Eden Garden neighborhood of Chicago has an intensity that you won’t quite understand until you’re there for yourself.

I made my way from East 132nd street and along Route 41. One lakeside road ushered me from the city’s South Side to Evanston, one of the most noteworthy areas along the city’s North Shore and the home of Northwestern University. This is John Hughes’ and Lisa Birnbach’s Chicago. The experience was diametrically opposed to my 45 minutes elsewhere: peace, ease, and abundance. I was comfortable enough in both worlds to be able to assess their impact on the other.

In every city, you will find these lines of demarcation, though few are as clear as Chicago’s. The pandemic has accelerated the reshaping of the groups defined by these lines.

On one side, remote work is practical and desirable. Access to capital allows for short-term gains in the stock market. Savings accounts and low unemployment rates ensure a continuation of life within the new normal. It’s as if this period of economic distress hasn’t existed at all.

On the South Side, wage work and income require a physical presence and a tolerance for health risk. These are the dignified hourly workers that make our economy move, though they receive no credit for doing so. There is little to no access to capital on their side; there is no taking advantage of record market gains during record highs in unemployment. There isn’t even capable WiFi access for many. For these citizens, nothing is the same as it was before the lockdown. Matters found a way to further devolve. And for a subset of them, impossibly hard circumstances have worsened. Remote learning is mandated for families whom cannot work from home or support the infrastructure required to learn remotely.

This is the backdrop. American retailers suffered because they didn’t foresee the bifurcation of wealth, access, and humanity that was staring back at them. When you review a list of bankruptcies and closures, you will notice that they will skew towards companies that have built strategies around a perpetual middle class. But in my trip along Route 41, there was no middle class to observe. For our consumer economy (one that employs nearly 30 million Americans) to return to form, enterprise retailers will have to understand the core message of “HENRY.” The middle was never really static at all.

HENRY Revisited

The HENRY designation is short for “high earners not rich yet.” The acronym system of identification has become popular with analysts, however, this consumer classification has gone largely ignored by enterprise retailers.

Whether by acronym or not, the pandemic has been witness to this phenomenon. Access to suburban escapes, remote work or educational benefits, and day-trading volume were but a few of the tell-tale signs. In New York and Brooklyn, residents fled to New England and the Hamptons. In the Midwest, the upper peninsula of Michigan was a hot spot for this psychographic. On the West Coast, rents in the Bay Area’s suburbs grew as rents in the city fell as much as 15%.

When Ralph Lauren Corporation cites a strategy to modernize its business by creating “smart customer profiles,” it is the HENRY designation that the brand is speaking of.

The HENRYs are advancers, not necessarily those who have cleared the wealth bar to America’s elite class. In fact, many are working to leave the middle class as if it’s a blemish on their personal ambitions. In this way, the term is more inclusive than the yuppie moniker of yesteryear. It’s also a symptom of our current economy, one where the cost of living can begin to erode long-term investments like real estate, money market funds, or other equities. [2PM, 2]

As Heraclitus wrote, “life is flux.” The focus on early identification of the upwardly mobile is one that will become commonplace in marketing and branding. As target metrics like customer acquisition cost (CAC) and lifetime value (LTV) dominate eCommerce-first retail, I’d argue that there is another that will arise: duration of loyalty (DOL). Brands will identify certain customers early and follow them throughout their education and careers, a strategy commonly practiced in the automobile industry.

As enterprise retailers like Ralph Lauren begin to smart-target the middle class, the days of shallow promotional efforts will give way to the notion of flux. By targeting these customers appropriately, the hope is that many will remain loyal as they ascend to greater discretionary income and higher consumption.

In Sanitized Urbanization, 2PM explored the larger trend of urbanites moving to suburban areas. Across America, the upwardly mobile pursued exurban peace, ease, and abundance. Some sought permanent moves. In theory, these areas brought a calmer pace, cleaner air, and functioning local retailers. These were things that were once considered essential, today they are luxuries. In these areas, amenities like parks and beaches provided a sense of normalcy.

Sanitized urbanization removes the perceived risks of living in urban areas while adding the value of – what’s often – upgraded infrastructure, improved schools, and lower tax bases. It is likely to become a politicized issue once urban municipalities begin to suffer the full force of the migration away from city centers. [2PM, 4]

Like many phenomena, the pandemic accelerated existing trends: sanitized urbanization, remote work, online retail, in-home fitness, and a decreasing dependence on personal vehicles. For the professionals who were comfortable with this shifting economy, a great many of them achieved financial breakthroughs despite the economy’s vulnerability. The vulnerability has never been equally distributed. One of the last bastions of economic mobility is America’s 29+ million retail jobs. To protect what’s left of them, retailers must begin to see the market this way. The industry’s stodgy retail executives seem to lack the ability and foresight to do so.

This cohort of professionals is a cross-section of race, ethnicity, and gender though many share similar traits in quality of education, career, and social standing. This psychographic is due to become the key study in the next five to 10 years of retail marketing and communications development. HENRY is beginning to live up to its name. There is a new guard of creative leaders, solo capitalists, and ascendant executives to show for it.

作者:Web Smith | 编辑:Hilary Milnes | 艺术:亚历克斯-雷米 |关于 2PM

Original Report: Regarding H.E.N.R.Y.