Este informe está destinado exclusivamente a Miembros ejecutivos, para facilitarle la afiliación, puede hacer clic a continuación y acceder a cientos de informes, a nuestra lista DTC Power List y a otras herramientas que le ayudarán a tomar decisiones de alto nivel.

Resumen para miembros: El efecto Huberman

Desbloqueado temporalmente para el "Chat de optimización" de HBS. En 1964, una expedición financiada por Canadá y dirigida por el médico de Montreal Stanley Skoryna navegó a Rapa Nui (Isla de Pascua) para realizar un estudio ecológico sin precedentes de su biosfera que condujo al descubrimiento de la rapamicina, lanzando un campo perdurable de investigación biomédica. Conocida por la comunidad científica como un fármaco que altera y prolonga la vida, "la rapamicina es el agente preventivo del cáncer más eficaz que se conoce en ratones. Incluso se ha sugerido que la rapamicina alarga la vida previniendo el cáncer".(NLM)

Se sabe que el fármaco imita la restricción calórica. Funciona inhibiendo mTOR, que envía señales a las células que afectan al crecimiento, el metabolismo y la autofagia (un proceso que elimina las células viejas en favor de las nuevas). ¿Cómo sé todo esto? ¿Y por qué me importa? Desde luego, no soy el único.

Pregunte a diez estudiantes universitarios con las mejores puntuaciones en el ACT en qué piensan especializarse y es posible que oiga "neurociencia" o cualquier otra ciencia biológica. Supongo que oiría esto más que hace una década, cuando ese mismo estudiante podría haber contestado "informática" o "ingeniería".

Llamémoslo efecto Huberman.

Los albores del siglo XXI han sido testigos de una atención cada vez mayor al bienestar y la optimización personales. Esta tendencia, alimentada por la innovación tecnológica, un renovado interés por los alimentos hipersaludables y una afluencia de marcas digitales de salud y bienestar, está transformando la industria de la salud. Empresas como Whoop, Eight Sleep, Apollo Neuro, Base, Oura Ring y Apple, con su exitosa versión "Ultra", han allanado el camino para esta nueva era de optimización humana.

Puede que también haya oído hablar de Brian Johnson. Es el empresario que vendió su empresa Braintree a Paypal por 800 millones de dólares y después dedicó su vida, a los 45 años, a varios métodos de inversión de la edad, intentando reducir su edad biológica a 18 años. Es rico, obsesivo, motivado y está especialmente centrado en su propio cuerpo. No es el único (aunque sus métodos sean extremos). De un artículo de Bloomberg BusinessWeek de enero de 2023 sobre el pionero del antienvejecimiento:

Este año va camino de gastarse al menos 2 millones de dólares en su cuerpo. Quiere tener el cerebro, el corazón, los pulmones, el hígado, los riñones, los tendones, los dientes, la piel, el pelo, la vejiga, el pene y el recto de un joven de 18 años.

Hay un conjunto de datos que sugieren que la moda de la "Medicina 3.0" ha proporcionado vientos de cola a una serie de empresas centradas en la salud. La medicina 3.0 es una fase de sofisticación altamente personalizada de la atención sanitaria hacia la que nos dirigimos rápidamente. Se basa en directrices "basadas en la evidencia" en lugar de "basadas en la evidencia" sobre medidas preventivas para enfermedades crónicas, que son ahora "la principal fuente de morbilidad y mortalidad".

El crecimiento de Restore Hyper Wellness es un testimonio de esta tendencia. Fundada con la misión de hacer más asequibles y accesibles los tratamientos de bienestar, la empresa se ha expandido rápidamente, ofreciendo una amplia gama de servicios, como crioterapia, terapia intravenosa por goteo y oxigenoterapia hiperbárica. Han democratizado el acceso a los tratamientos de bienestar, normalmente reservados a los atletas profesionales y a los ricos, para el público en general. Este cambio ha sido decisivo para que las personas puedan tomar las riendas de su bienestar.

Paralelamente, ha surgido una nueva generación de educadores y personas influyentes, con podcasts y plataformas digitales para difundir la concienciación y el conocimiento sobre la optimización de la salud personal. Lex Fridman, investigador de IA en el MIT, presenta un podcast conocido por sus conversaciones profundas y sugerentes sobre IA, atención plena y potencial humano. El Dr. Andrew Huberman, neurocientífico y profesor titular de la Facultad de Medicina de la Universidad de Stanford, comparte sus profundos conocimientos sobre el cerebro y su impacto en nuestro comportamiento y bienestar. El Dr. David Sinclair, profesor del Departamento de Genética y codirector del Centro Paul F. Glenn para la Biología del Envejecimiento de la Facultad de Medicina de Harvard, explora la ciencia del envejecimiento y la longevidad. Por último, el Dr. Peter Attia, antiguo becario de oncología quirúrgica en el Hospital Johns Hopkins, se centra en la ciencia de la longevidad, la bioquímica nutricional y la fisiología del ejercicio. Su influencia colectiva ha sido decisiva para impulsar un cambio cultural hacia una salud proactiva y preventiva.

Al mismo tiempo, estamos asistiendo a un resurgimiento del interés por los minoristas de bienes de consumo envasados hipersaludables. Esta tendencia no tiene que ver con las dietas de moda, sino con la adopción de alimentos integrales y ricos en nutrientes que contribuyan a una función humana óptima. Empresas como Heart & Soil, Force of Nature y ButcherBox están a la cabeza en este ámbito, distribuyendo directamente a los consumidores carnes y vísceras de alta calidad alimentadas con pasto, conocidas por sus densos perfiles nutricionales. La popularidad de estas marcas refleja un cambio social más amplio hacia la transparencia, la sostenibilidad y la densidad de nutrientes en nuestras elecciones alimentarias.

En el frente de la rendición de cuentas, la tecnología para llevar puesta, como Whoop, Eight Sleep y Apple Ultra, está desempeñando un papel crucial. Estos dispositivos proporcionan datos en tiempo real sobre una serie de indicadores de salud, como la calidad del sueño, la variabilidad de la frecuencia cardiaca y la actividad física. Estos datos personalizados permiten a las personas tomar decisiones informadas sobre su estilo de vida y sus hábitos, lo que refuerza una cultura de rendición de cuentas y responsabilidad personal sobre la salud. Whoop, por ejemplo, ofrece información sobre la recuperación, el esfuerzo y el sueño, lo que permite a los usuarios optimizar sus rutinas diarias para rendir al máximo. El wearable Ultra de Apple va un paso más allá, integrando el seguimiento de la salud con un ecosistema más amplio de aplicaciones y servicios diseñados para contribuir al bienestar general.

La proliferación de marcas de comercio electrónico en este espacio es otro aspecto crítico de esta industria emergente. Empresas como Thrive Market y Misfits Market no solo venden productos, sino también un estilo de vida. Proporcionan a los consumidores la información que necesitan para tomar el control de su salud, ya se trate de alimentos de alta calidad y ricos en nutrientes, suplementos o productos de bienestar. Estas empresas prosperan porque se alinean con los valores y prioridades de un segmento creciente de la población que busca activamente formas de optimizar su salud y rendimiento.

La optimización humana ya no es un nicho de interés, sino una tendencia cultural y económica en toda regla. Al entrar en esta nueva era, vemos la intersección de la tecnología, la educación, la responsabilidad personal y un renovado interés por la calidad de los alimentos que consumimos.

La información basada en datos que ofrece la tecnología para llevar puesta no sólo está cambiando nuestra forma de enfocar el ejercicio físico y la salud, sino también nuestra percepción de lo que es posible. Con estas herramientas, ya no somos receptores pasivos de consejos sobre salud, sino participantes activos en nuestro camino hacia el bienestar. Este es uno de los principios básicos de la prevención que defiende el Dr. Peter Attia al referirse a la Medicina 3.0. Para profundizar en el tema, lea su nuevo libro Outlive. Hay un sinfín de pepitas de oro como ésta:

El efecto promotor de la autofagia [de la rapamicina] es sólo una de las razones por las que la rapamicina puede tener futuro como fármaco para la longevidad, según Matt Kaeberlein, investigador de la Universidad de Washington. Kaeberlein, que lleva un par de décadas estudiando la rapamicina y el mTOR, cree que los beneficios del fármaco son mucho más amplios y que la rapamicina y sus derivados tienen un enorme potencial para su uso en humanos, con el fin de prolongar la esperanza de vida y la salud.

Resumen

La educación impartida por figuras influyentes en el ámbito de la salud y el bienestar está democratizando conocimientos que antes estaban confinados a los círculos académicos y clínicos. Los podcasts de Lex Fridman, el Dr. Andrew Huberman, el Dr. David Sinclair y el Dr. Peter Attia han puesto al alcance de las masas conceptos complejos sobre salud, forma física y longevidad, despertando un interés generalizado por la optimización personal.

El resurgimiento de los alimentos hipersaludables subraya una reevaluación colectiva de nuestras elecciones dietéticas. Este cambio no es solo un rechazo de los alimentos procesados y pobres en nutrientes, sino una aceptación de aquellos que nos aportan los nutrientes que nuestro cuerpo necesita para funcionar de forma óptima.

Y el éxito de las marcas de comercio electrónico en este espacio refleja una creciente demanda de productos y servicios que apoyen este estilo de vida centrado en la optimización. Estas marcas no se limitan a vender productos, sino que proporcionan las herramientas, los recursos y la comunidad necesarios para que las personas tomen las riendas de su salud.

La aparición de la optimización humana como gran industria subraya un profundo cambio en los valores y prioridades de la sociedad. Habla de un deseo colectivo no sólo de vivir más, sino de vivir mejor. A medida que más personas se esfuerzan por alcanzar su máximo potencial, más empresas, educadores, marcas y servicios se alzan para satisfacer esta demanda, allanando el camino hacia un futuro más saludable para un mayor porcentaje de nuestros ciudadanos. Este cambio de paradigma, impulsado por la innovación tecnológica, la educación y un renovado interés por la nutrición de calidad, es sólo el principio de lo que promete ser un viaje transformador hacia la optimización de la salud y el bienestar. Y pensar que este resurgimiento del interés por los métodos antienvejecimiento puede haber comenzado con las visitas a la misteriosa Isla de Pascua. No, no la de 1964. Aquellas en las que el Dr. Peter Attia se unió a Tim Ferris y a un grupo rotativo de colegas amantes de la ciencia.

Por Web Smith | Editado por Hilary Milnes con arte de Christina Williams

Memo: El nuevo evangelismo del acceso preferente

Si creciste con una nevera vacía con frecuencia, Amazon Prime es una bendición. Como adulto: te levantas, miras la nevera, tus recuerdos te llevan a una respuesta irracional y abres innecesariamente una aplicación para llenar los espacios vacíos de tu despensa o cámara frigorífica. En dos horas, el problema está resuelto y tus estanterías ya no provocan pensamientos de inseguridad alimentaria. Amazon se queda con el negocio, los gastos de envío y los datos. Que se joda Costco. No puedo ser la única persona que hace esto habitualmente.

El mercado para este comportamiento de consumo va a crecer. Amazon Prime, que normalmente tiene una cuota anual de 139 dólares, tiene una opción más barata para aquellos que lo necesiten y vas a oír hablar más de ella. Prime Access, aunque está disponible desde 2017, fue impulsado recientemente por Amazon (Amazon amplió este programa en octubre de 2022). Probablemente como solución a un problema doble:

- efectos inflacionistas restantes(4,9%)

- la caída de los ingresos de los socios minoristas

Muy pronto, la aplicación podrá reflejar opciones de compra más económicas. Más sobre esto en un momento.

Amazon ha estado a menudo a la vanguardia de la evolución del comercio electrónico, desde su origen como librería digital hasta su estatus actual como colosal conglomerado multisectorial. Su evangelización en abril de 2023 de Prime Access (un programa con seis años de antigüedad) y destinado a democratizar Amazon Prime para los usuarios con menos ingresos, es otro testimonio de la necesidad de la empresa de ajustarse a la evolución del comercio minorista.

Prime Access es el programa de descuentos de Amazon para programas gubernamentales. Los clientes de Estados Unidos que cumplan los requisitos y se inscriban recibirán todos los privilegios de Amazon Prime con un descuento de alrededor del 50% sobre el precio de una suscripción normal.

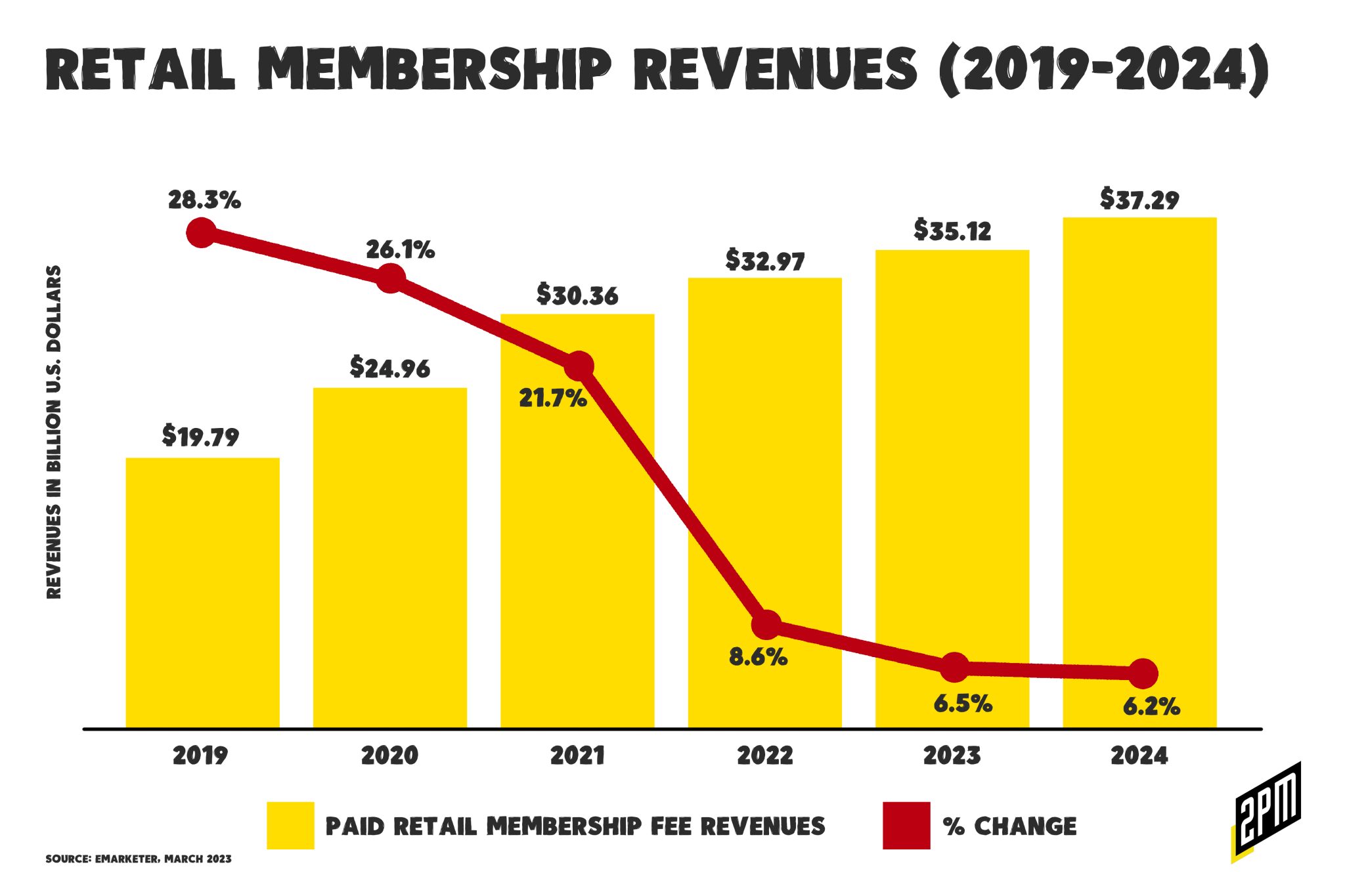

Prime Access podría afectar significativamente al crecimiento potencial de Amazon en un contexto de descenso de los ingresos por afiliación en todo el sector. Según la startup de afiliación Inveterate, que gestiona los programas de fidelización de las siguientes empresas: Liquid IV, Fresh Clean Tees, Lashify, Fly by Jing, Flamingo Estate y muchas otras:

Un estudio de Deloitte reveló que el 67% de los consumidores se uniría a un programa de fidelización de pago si ofreciera ventajas significativas (frente a sólo el 33% que dijo lo mismo de los programas gratuitos basados en puntos).

Amazon espera captar, o incluso mejorar, el crecimiento restante apelando a un público más amplio que pueda estar interesado en programas de fidelización de pago. En la actualidad, Amazon Prime sigue siendo el programa de fidelización mejor valorado, según una encuesta realizada por Activate en octubre de 2022. Esto incluye CostCo, Sam's Club, Walmart+ e Instacart+. Pero el crecimiento se ha ralentizado como era de esperar.

Tradicionalmente, Amazon Prime se ha percibido como un bien adyacente al lujo, destinado predominantemente a los hogares con mayores ingresos. Sin embargo, esta nueva iniciativa representa una ampliación significativa del mercado objetivo de Amazon. Aprovechando una serie de programas gubernamentales, Amazon está haciendo accesibles sus servicios premium a un grupo demográfico más amplio, ampliando así su base potencial de usuarios y sus fuentes de ingresos. Este movimiento demuestra el poder del comercio electrónico basado en aplicaciones y orientado a los miembros: al reducir la barrera de entrada, Amazon puede acceder a un mercado menos atendido (pero en crecimiento), impulsando su potencial de crecimiento. Este podría ser el antídoto.

Nunca se insistirá lo suficiente en el poder de la simplicidad en el comercio, especialmente en el contexto de las compras repetidas con un solo clic en mercados basados en aplicaciones como Amazon Prime (aquí hay un artículo reciente sobre este tema). El modelo de Amazon ha destacado por ofrecer una experiencia de compra fluida y sin fricciones. Cuantos menos pasos tenga que dar un consumidor para completar una compra, mayor será la probabilidad de conversión. Al simplificar al máximo el proceso de compra, Amazon anima a los usuarios a repetir las compras, fomentando la fidelidad de los clientes e impulsando las ventas. En el contexto de la democratización del comercio, creo que existe un motivo de preocupación.

En línea con el principio de simplicidad, Prime Access también sirve para democratizar el comercio electrónico. Según Amazon, puedes aportar pruebas de elegibilidad o participación de los siguientes programas:

- SNAP EBT

- Medicaid

- Programa para Mujeres, Bebés y Niños (WIC)

- Seguridad de Ingreso Suplementario (SSI)

- Tarjeta de débito Direct Express (DE)

- Ayuda Temporal para Familias Necesitadas (TANF)

- Programa Nacional de Almuerzos Escolares (NSLP)

- Programa de Asistencia Energética para Hogares con Ingresos Bajos (LIHEAP)

- Carta de elegibilidad para asistencia tribal (TTANF)

- Programa de Asistencia Nutricional (PAN)

Tradicionalmente, las compras en línea se han inclinado hacia quienes disponen de mayores ingresos y acceso a tarjetas de crédito. Al permitir el acceso a los beneficios Prime a través de la participación en diversos programas de ayuda gubernamental, Amazon está ampliando el alcance del mercado minorista en línea. Este movimiento democratiza el mercado del comercio al ofrecer las mismas comodidades y ventajas de las compras en línea a un grupo demográfico que sólo recientemente se ha convertido en el centro de atención de las empresas minoristas:

Es la nueva venta directa al consumidor. El envío de los pedidos directamente desde sus fábricas de origen mantiene los precios bajos. Shein, el gigante chino de la moda ultrarrápida, ha tomado el mundo por asalto y sigue creciendo en magnitud, empequeñeciendo el recuento de SKU y el volumen de ventas de competidores como Zara, H&M y Boohoo. La ropa es barata, desechable y adictiva. Temu podría satisfacer un deseo similar de productos "baratos pero suficientemente buenos", sobre todo ahora que la histórica racha inflacionista de Estados Unidos sigue inclinando al alza los precios al consumo.

Empresas chinas de comercio transfronterizo como Shein y Temu se centran en este segmento demográfico, pero pocas llegan a él como Amazon. Es la facilidad de compra, la disponibilidad del producto, la transparencia de precios y la proximidad al consumidor. En relación con este tema, se rumorea que Amazon podría adquirir 500 establecimientos de los que Albertsons y Kroger planean desprenderse. Estas tiendas permitirían a Amazon ampliar su opción Amazon Fresh, una fuente de productos más económica que la que suele encontrarse en Whole Foods. En resumen, Whole Foods solo puede crecer hasta cierto punto.

En una carta a los accionistas a principios de abril, el CEO de Amazon, Andy Jassy, dijo que el negocio de comestibles, que ha luchado por despegar, necesita ser un punto focal de la estrategia de la compañía. Ya en 2017 Amazon pagó 13.700 millones de dólares por la cadena Whole Foods, pero eso ha venido con golpes y magulladuras. Amazon también se ha visto obligada a cerrar locales de Amazon Go y Amazon Fresh, y ha despedido a miles de trabajadores. En febrero, Amazon anunció una pausa en el despliegue de sus tiendas Amazon Fresh mientras reevaluaba la economía del concepto.

La concienciación sobre este programa y la posterior democratización no está exenta de posibles inconvenientes. Uno de ellos son las implicaciones de que Amazon permita realizar compras impulsivas, durante periodos de gran incertidumbre económica, de productos básicos como alimentos y artículos para el hogar con una tarjeta de crédito. Con la comodidad de las compras con un solo clic y la tentación de una amplia gama de productos, los consumidores pueden verse obligados a gastar por encima de sus posibilidades, lo que podría conducir a mayores niveles de endeudamiento.

Aunque se trata de un riesgo potencial, es importante tener en cuenta que la comodidad de las compras en línea, sobre todo de productos básicos, también puede servir como herramienta de planificación financiera. Por ejemplo, la posibilidad de comparar precios y productos puede ayudar a los compradores a tomar decisiones más informadas, con el consiguiente ahorro de dinero a largo plazo. Además, la comodidad de la entrega a domicilio puede ahorrar gastos de transporte, sobre todo para quienes viven en zonas desérticas o con acceso limitado a las tiendas.

La promoción de Amazon de Prime Access subraya el poder transformador del comercio electrónico basado en aplicaciones y orientado a los miembros en productos de alimentación y del hogar. Al anunciar un acceso democratizado a sus servicios Prime, Amazon no solo está ampliando su crecimiento potencial, sino también allanando el camino para un comercio más inclusivo. Al mismo tiempo, este desarrollo pone de relieve la necesidad de educar a los consumidores para mitigar el potencial de aumento de la deuda. A medida que el mercado del comercio electrónico sigue evolucionando, es crucial que los avances en comodidad y accesibilidad se equilibren con medidas que promuevan el gasto responsable.

Por Web Smith | Editado por Hilary Milnes con arte de Alex Remy y Christina Williams