Este resumo para membros foi elaborado exclusivamente para Membros executivosPara facilitar a associação, você pode clicar abaixo e obter acesso a centenas de relatórios, à nossa DTC Power List e a outras ferramentas para ajudá-lo a tomar decisões de alto nível.

Resumo para membros: O efeito Huberman

Desbloqueado temporariamente para o "Chat de otimização" da HBS. Em 1964, uma expedição financiada pelo Canadá e liderada pelo médico de Montreal Stanley Skoryna navegou até Rapa Nui (Ilha de Páscoa) para realizar um levantamento ecológico sem precedentes de sua biosfera, o que levou à descoberta da rapamicina, lançando um campo duradouro de pesquisa biomédica. Conhecida pela comunidade científica como uma droga que altera e prolonga a vida, "a rapamicina é o agente preventivo de câncer mais eficaz conhecido em camundongos. Foi até sugerido que a rapamicina prolonga a vida útil ao prevenir o câncer."(NLM)

O medicamento é conhecido por imitar a restrição calórica. O mTOR envia sinais às células que afetam o crescimento, o metabolismo e a autofagia (um processo que elimina as células velhas em favor das novas). Como posso saber tudo isso? E por que eu me importo? Certamente não estou sozinho.

Pergunte a dez alunos que estão prestes a entrar na faculdade com as melhores pontuações no ACT o que eles planejam fazer e você poderá ouvir "neurociência" ou qualquer outra ciência biológica. Eu diria que você ouviria isso mais do que ouviria há uma década, quando o mesmo aluno poderia ter respondido "ciência da computação" ou "engenharia".

Vamos chamá-lo de efeito Huberman.

O início do século XXI testemunhou um foco cada vez maior no bem-estar e na otimização pessoal. Essa tendência, impulsionada pela inovação tecnológica, um interesse renovado em alimentos hipersaudáveis e um influxo de marcas digitais de saúde e bem-estar, está transformando o setor de saúde. Empresas como Whoop, Eight Sleep, Apollo Neuro, Base, Oura Ring e Apple, com sua versão "Ultra" de grande sucesso, abriram o caminho para essa nova era de otimização humana.

Talvez você também já tenha ouvido falar de Brian Johnson. Ele é o empresário que vendeu sua empresa Braintree para o Paypal por US$ 800 milhões e, aos 45 anos, dedicou sua vida a vários métodos de reversão de idade, tentando reduzir sua idade biológica para 18 anos. Ele é rico, obsessivo, motivado e tem um foco exclusivo em seu próprio corpo. Ele não é o único (embora seus métodos possam ser extremos). De um artigo da Bloomberg BusinessWeek de janeiro de 2023 sobre o pioneiro do antienvelhecimento:

Este ano, ele está no caminho certo para gastar pelo menos US$ 2 milhões em seu corpo. Ele quer ter o cérebro, o coração, os pulmões, o fígado, os rins, os tendões, os dentes, a pele, o cabelo, a bexiga, o pênis e o reto de um jovem de 18 anos.

Há um conjunto de dados que sugerem que a mania da "Medicina 3.0" proporcionou ventos favoráveis para uma série de empresas voltadas para a saúde. A Medicina 3.0 é um estágio altamente personalizado de sofisticação na área da saúde para o qual estamos nos acelerando. Ela se baseia em diretrizes "informadas por evidências" em vez de "baseadas em evidências" sobre medidas preventivas para condições crônicas, que agora são "a fonte dominante de morbidade e mortalidade".

O crescimento da Restore Hyper Wellness é um testemunho dessa tendência. Fundada com a missão de tornar os tratamentos de bem-estar mais acessíveis e baratos, a empresa expandiu-se rapidamente, oferecendo uma ampla gama de serviços, incluindo crioterapia, terapia de gotejamento intravenoso e terapia de oxigênio hiperbárico. A empresa democratizou o acesso a tratamentos de bem-estar, normalmente reservados a atletas profissionais e pessoas ricas, para o público em geral. Essa mudança foi fundamental para capacitar as pessoas a assumir o controle de sua jornada de bem-estar.

Paralelamente, surgiu uma nova geração de educadores e influenciadores, com podcasts e plataformas digitais para disseminar a conscientização e o conhecimento sobre a otimização da saúde pessoal. Lex Fridman, pesquisador de IA do MIT, apresenta um podcast conhecido por conversas profundas e instigantes sobre IA, atenção plena e potencial humano. O Dr. Andrew Huberman, neurocientista e professor titular da Faculdade de Medicina da Universidade de Stanford, compartilha seu profundo conhecimento sobre o cérebro e seu impacto em nosso comportamento e bem-estar. O Dr. David Sinclair, professor do Departamento de Genética e codiretor do Paul F. Glenn Center for the Biology of Aging da Harvard Medical School, explora a ciência do envelhecimento e da longevidade. Por fim, o Dr. Peter Attia, ex-bolsista de oncologia cirúrgica do Johns Hopkins Hospital, concentra-se na ciência da longevidade, bioquímica nutricional e fisiologia do exercício. Sua influência coletiva tem sido fundamental para promover uma mudança cultural em direção à saúde proativa e preventiva.

Simultaneamente, estamos vendo um ressurgimento do interesse em varejistas de bens de consumo embalados hipersaudáveis. Essa tendência não tem a ver com dietas da moda, mas sim com a adoção de alimentos integrais e ricos em nutrientes que apoiam a função humana ideal. Empresas como Heart & Soil, Force of Nature e ButcherBox estão liderando esse espaço, fornecendo carnes de alta qualidade, alimentadas com capim e carnes de órgãos, conhecidas por seus densos perfis de nutrientes, diretamente na porta dos consumidores. A popularidade dessas marcas reflete uma mudança social mais ampla em direção à transparência, sustentabilidade e densidade de nutrientes em nossas escolhas alimentares.

No que se refere à responsabilidade, a tecnologia vestível, como Whoop, Eight Sleep e Apple Ultra, está desempenhando um papel fundamental. Esses dispositivos fornecem dados em tempo real sobre uma série de indicadores de saúde, incluindo a qualidade do sono, a variabilidade da frequência cardíaca e a atividade física. Esses dados personalizados permitem que os indivíduos tomem decisões informadas sobre seu estilo de vida e seus hábitos, reforçando uma cultura de responsabilidade e responsabilidade pessoal pela saúde. O Whoop, por exemplo, oferece insights sobre recuperação, esforço e sono, permitindo que os usuários otimizem suas rotinas diárias para obter o máximo desempenho. O wearable Ultra da Apple vai além, integrando o rastreamento da saúde a um ecossistema mais amplo de aplicativos e serviços criados para apoiar o bem-estar geral.

A proliferação de marcas de comércio eletrônico nesse espaço é outro aspecto fundamental desse setor emergente. Empresas como a Thrive Market e a Misfits Market não estão apenas vendendo produtos; elas estão vendendo um estilo de vida. Elas fornecem aos consumidores os insights de que precisam para assumir o controle de sua saúde, seja com alimentos de alta qualidade e ricos em nutrientes, suplementos ou produtos de bem-estar. Essas empresas estão prosperando porque se alinham com os valores e as prioridades de um segmento crescente da população que está buscando ativamente maneiras de otimizar sua saúde e seu desempenho.

A otimização humana não é mais um interesse de nicho, mas uma tendência cultural e econômica completa. Ao entrarmos nessa nova era, vemos a interseção de tecnologia, educação, responsabilidade pessoal e um foco renovado na qualidade dos alimentos que consumimos.

Os insights orientados por dados oferecidos pela tecnologia vestível não estão apenas mudando a maneira como abordamos o condicionamento físico e a saúde; eles estão alterando nossa percepção do que é possível. Com essas ferramentas, não somos mais receptores passivos de conselhos de saúde, mas participantes ativos em nossas jornadas de bem-estar. Esse é um dos princípios fundamentais da prevenção que o Dr. Peter Attia defende quando se refere à Medicina 3.0. Para um mergulho profundo, leia seu novo livro Outlive. Há inúmeras dicas como esta:

O efeito promotor de autofagia [da rapamicina] é apenas um dos motivos pelos quais a rapamicina pode ter futuro como medicamento para a longevidade, de acordo com Matt Kaeberlein, pesquisador da Universidade de Washington. Kaeberlein, que vem estudando a rapamicina e o mTOR há algumas décadas, acredita que os benefícios da droga são muito mais abrangentes e que a rapamicina e seus derivados têm um enorme potencial para uso em seres humanos, com o objetivo de prolongar o tempo de vida e a saúde.

Resumo

A educação fornecida por figuras influentes no campo da saúde e do bem-estar está democratizando o conhecimento que antes estava confinado aos círculos acadêmicos e clínicos. Os podcasts de Lex Fridman, Dr. Andrew Huberman, Dr. David Sinclair e Dr. Peter Attia tornaram conceitos complexos de saúde, condicionamento físico e longevidade acessíveis às massas, despertando um interesse generalizado na otimização pessoal.

O ressurgimento de alimentos hipersaudáveis ressalta uma reavaliação coletiva de nossas escolhas dietéticas. Essa mudança não é apenas uma rejeição de alimentos processados e pobres em nutrientes, mas uma aceitação daqueles que nos fornecem os nutrientes de que nosso corpo precisa para funcionar de maneira ideal.

E o sucesso das marcas de comércio eletrônico nesse espaço reflete a crescente demanda por produtos e serviços que apoiam esse estilo de vida focado na otimização. Essas marcas não estão apenas vendendo produtos; elas estão fornecendo as ferramentas, os recursos e a comunidade necessários para que as pessoas assumam o controle de sua saúde.

O surgimento da otimização humana como um setor importante ressalta uma mudança profunda nos valores e nas prioridades da sociedade. Ele fala de um desejo coletivo de não apenas viver mais, mas de viver melhor. À medida que mais pessoas se esforçam para atingir seu potencial máximo, empresas, educadores, marcas e serviços estão surgindo para atender a essa demanda, abrindo caminho para um futuro mais saudável para uma porcentagem maior de nossos cidadãos. Essa mudança de paradigma, impulsionada pela inovação tecnológica, educação e um foco renovado em nutrição de qualidade, é apenas o começo do que promete ser uma jornada transformadora rumo à saúde e ao bem-estar otimizados. E pensar que esse interesse ressurgente em métodos antienvelhecimento pode ter começado com visitas à misteriosa Ilha de Páscoa. Não, não aquela de 1964. Aquelas em que o Dr. Peter Attia se juntou a Tim Ferris e a um grupo rotativo de amigos amantes da ciência.

Por Web Smith | Editado por Hilary Milnes com arte de Christina Williams

Memorando: O novo evangelismo do Prime Access

Se você cresceu com uma geladeira frequentemente vazia, o Amazon Prime é uma dádiva de Deus. Como adulto: você acorda, olha para a geladeira, suas lembranças provocam uma reação irracional e você abre desnecessariamente um aplicativo para preencher os espaços vazios na despensa ou na câmara fria. Em duas horas, o problema está resolvido e suas prateleiras não provocam mais pensamentos de insegurança alimentar. A Amazon fica com o negócio, as taxas de entrega e os dados. A Costco que se dane. Não posso ser a única pessoa que faz isso rotineiramente.

O mercado para esse comportamento do consumidor está crescendo. O Amazon Prime, que normalmente vem com uma taxa anual de US$ 139, tem uma opção mais barata para aqueles que precisam e você vai ouvir falar mais sobre isso. O Prime Access, embora disponível desde 2017, foi recentemente promovido pela Amazon (a Amazon expandiu esse programa em outubro de 2022). Provavelmente como uma solução para um problema de duas vertentes:

- efeitos inflacionários remanescentes(4,9%)

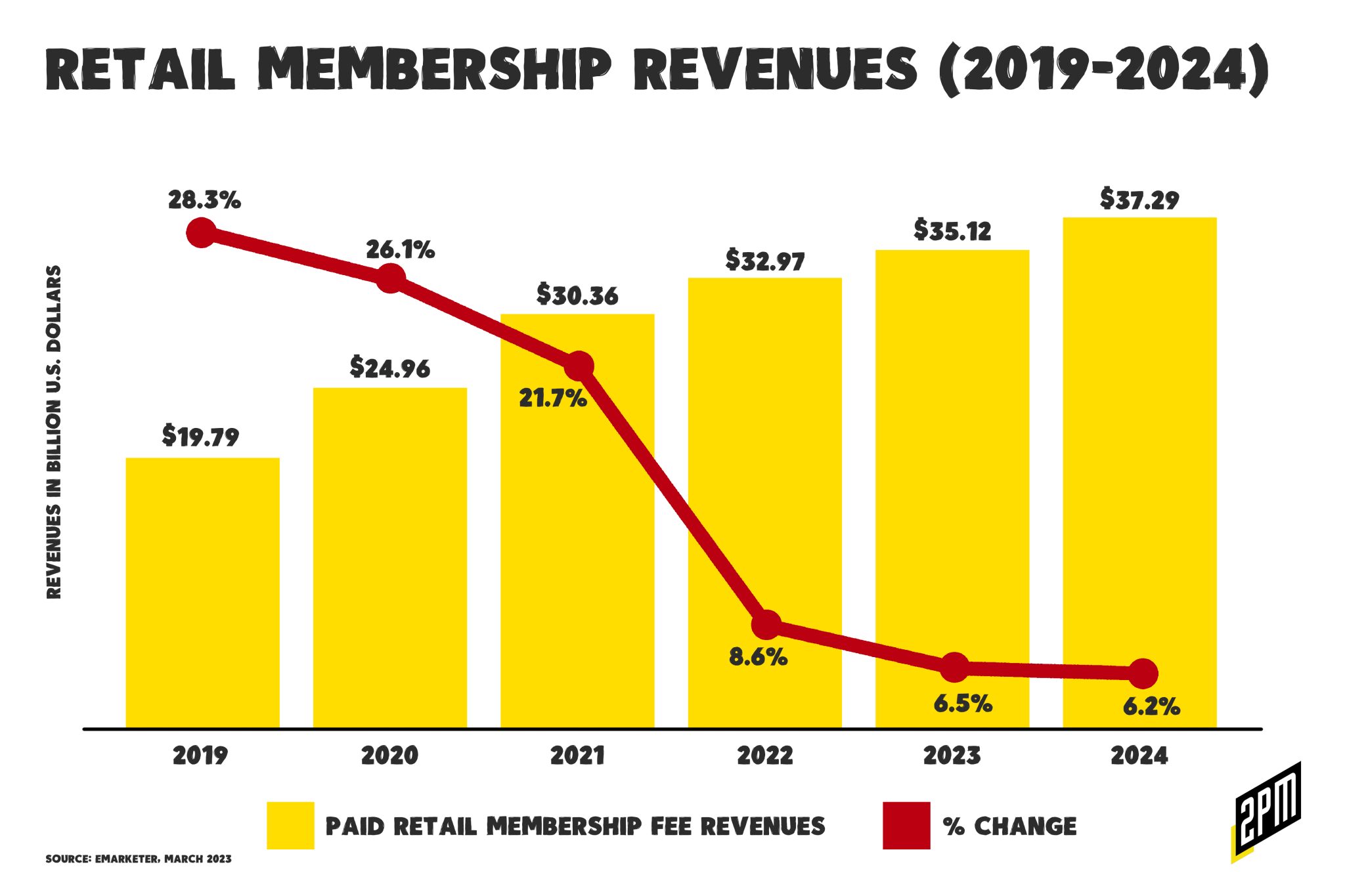

- a queda nas receitas de associação de varejo

Em breve, o aplicativo poderá refletir opções de compras que podem ser mais econômicas. Falaremos mais sobre isso em breve.

A Amazon sempre esteve na vanguarda da evolução do comércio eletrônico, desde sua origem como livraria digital até seu status atual como um colossal conglomerado multissetorial. Seu evangelismo de abril de 2023 do Prime Access (um programa de seis anos de idade) e um programa projetado para democratizar o Amazon Prime para usuários de baixa renda, é outro testemunho da necessidade da empresa de se ajustar à evolução do varejo.

Acesso Prime é o programa de associação com desconto da Amazon para programas governamentais qualificados. Os clientes qualificados nos EUA que se inscreverem recebem todos os privilégios do Amazon Prime com cerca de 50% de desconto em relação à associação típica.

O Prime Access poderia afetar significativamente o crescimento potencial da Amazon em um cenário de declínio do crescimento da receita de assinaturas em todo o setor. De acordo com a startup de filiação Inveterate, que controla os programas de fidelidade de filiação das seguintes empresas: Liquid IV, Fresh Clean Tees, Lashify, Fly by Jing, Flamingo Estate e várias outras:

Um estudo da Deloitte constatou que 67% dos consumidores adeririam a um programa de fidelidade pago se ele oferecesse benefícios significativos (em comparação com apenas 33% que disseram o mesmo para programas gratuitos baseados em pontos).

A Amazon espera capturar, ou até mesmo melhorar, o crescimento restante apelando para um público maior que possa estar interessado em programas de fidelidade pagos. No momento, o Amazon Prime continua sendo o programa de fidelidade mais bem avaliado, de acordo com uma pesquisa realizada em outubro de 2022 pela Activate. Isso inclui CostCo, Sam's Club, Walmart+ e Instacart+. Mas, previsivelmente, o crescimento diminuiu.

Tradicionalmente, o Amazon Prime tem sido visto como um bem de luxo, atendendo predominantemente a famílias de alta renda. No entanto, essa nova iniciativa representa uma expansão significativa do mercado-alvo da Amazon. Ao alavancar uma série de programas governamentais, a Amazon está tornando seus serviços premium acessíveis a um grupo demográfico mais amplo, ampliando assim sua base potencial de usuários e fluxos de receita. Essa medida demonstra o poder do comércio eletrônico baseado em aplicativos e orientado por membros: ao reduzir a barreira de entrada, a Amazon pode explorar um mercado menos atendido (mas em crescimento), aumentando seu potencial de crescimento. Esse pode ser o antídoto.

O poder da simplicidade no comércio, especialmente no contexto de compras repetidas com um clique em mercados baseados em aplicativos como o Amazon Prime, não pode ser exagerado (aqui está um mergulho profundo recente nesse tópico). O modelo da Amazon tem se destacado por oferecer uma experiência de compra perfeita e sem atritos. Quanto menos etapas o consumidor tiver que seguir para concluir uma compra, maior será a probabilidade de conversão. Ao tornar o processo de compra o mais simples possível, a Amazon incentiva os usuários a fazer compras repetidas, promovendo a fidelidade do cliente e impulsionando as vendas. No contexto da democratização do comércio, acredito que há um motivo de preocupação.

De acordo com o princípio da simplicidade, o Prime Access também serve para democratizar o comércio eletrônico. De acordo com a Amazon, você pode fornecer prova de elegibilidade ou participação nos seguintes programas:

- SNAP EBT

- Medicaid

- Programa para Mulheres, Bebês e Crianças (WIC)

- Renda de segurança suplementar (SSI)

- Cartão de débito Direct Express (DE)

- Assistência Temporária para Famílias Carentes (TANF)

- Programa Nacional de Merenda Escolar (NSLP)

- Programa de Assistência à Energia Residencial de Baixa Renda (LIHEAP)

- Carta de elegibilidade para assistência tribal (TTANF)

- Programa de Assistência Nutricional (NAP)

Tradicionalmente, as compras on-line são direcionadas àqueles com maior renda disponível e acesso a cartões de crédito. Ao permitir o acesso aos benefícios do Prime por meio da participação em vários programas de assistência governamental, a Amazon está ampliando o escopo do mercado de varejo on-line. Essa medida democratiza o mercado de comércio ao oferecer as mesmas conveniências e vantagens das compras on-line a um grupo demográfico que só recentemente se tornou o foco dos varejistas corporativos:

Considere isso como o novo varejo direto ao consumidor. O envio de pedidos diretamente de suas fábricas de origem mantém os preços baixos. A Shein, gigante chinesa da moda ultrarrápida, tomou o mundo de assalto e continua a crescer em magnitude, superando o número de SKUs e o volume de vendas de concorrentes como Zara, H&M e Boohoo. As roupas são baratas, descartáveis e viciantes. A Temu poderia atender a um desejo semelhante de produtos "baratos, porém bons o suficiente", especialmente porque a série histórica de inflação dos Estados Unidos continua a aumentar os preços ao consumidor.

Empresas chinesas de comércio internacional, como a Shein e a Temu, estão focadas nesse grupo demográfico, mas poucas conseguem atingi-lo como a Amazon. É a facilidade de compra, a disponibilidade do produto, a transparência dos preços e a proximidade com o consumidor. Relevante para essa conversa, há rumores de que a Amazon pode adquirir 500 locais que a Albertsons e a Kroger planejam alienar. Essas lojas permitiriam que a Amazon aumentasse sua opção Amazon Fresh, uma fonte de produtos mais econômica do que a encontrada normalmente na Whole Foods. Em suma, a Whole Foods não pode se expandir tanto.

Em uma carta aos acionistas no início de abril, o CEO da Amazon, Andy Jassy, disse que o negócio de mercearia, que tem lutado para decolar, precisa ser um ponto focal da estratégia da empresa. Em 2017, a Amazon pagou 13,7 bilhões de dólares pela cadeia Whole Foods, mas isso veio com solavancos e contusões. A Amazon também foi forçada a fechar as lojas Amazon Go e Amazon Fresh, e demitiu milhares de funcionários. A Amazon anunciou em fevereiro que estava pausando o lançamento de suas lojas Amazon Fresh enquanto reavaliava a economia do conceito.

A conscientização desse programa e a maior democratização que se seguirá têm suas possíveis desvantagens. Uma dessas preocupações está nas implicações de a Amazon permitir compras por impulso, durante períodos de grande incerteza econômica, para itens essenciais, como mantimentos e necessidades domésticas, com um cartão de crédito. Com a conveniência das compras com um clique e a tentação de uma vasta gama de produtos, os consumidores podem acabar gastando além de suas possibilidades, o que poderia levar a um aumento dos níveis de endividamento.

Embora esse seja um risco em potencial, é importante observar que a conveniência das compras on-line, principalmente de produtos essenciais, também pode servir como uma ferramenta de planejamento financeiro. Por exemplo, a possibilidade de comparar preços e produtos pode ajudar os compradores a tomar decisões mais bem informadas, o que pode economizar dinheiro a longo prazo. Além disso, a conveniência da entrega em domicílio pode economizar nos custos de transporte, especialmente para aqueles que vivem em desertos alimentares ou em áreas com acesso limitado a lojas.

O evangelismo da Amazon sobre o Prime Access ressalta o poder transformador do comércio eletrônico baseado em aplicativos e orientado por membros em produtos alimentícios e domésticos. Ao anunciar o acesso democratizado aos seus serviços Prime, a Amazon não está apenas expandindo seu crescimento potencial, mas também abrindo caminho para um comércio mais inclusivo. Ao mesmo tempo, esse desenvolvimento destaca a necessidade de educação do consumidor para mitigar o potencial de aumento de dívidas. Como o mercado de comércio eletrônico continua a evoluir, é fundamental que os avanços em conveniência e acessibilidade sejam equilibrados com medidas para promover gastos responsáveis.

Por Web Smith | Editado por Hilary Milnes com arte de Alex Remy e Christina Williams