After many years of struggles, Sears Holding Corp followed through on their anticipated Chapter 11 bankruptcy after missing a crucial debt payment of $134 million.

2PM, Inc. on Twitter

News: @Sears to file for bankruptcy after 12 PM EST. 150 anchor stores at Tier B / C malls will be closed and nearly 19,000 jobs will be lost.

History. Sears has a story that dates back 132 years. For over a century, that history was rich and awe-inspiring. From a mail order catalogue (that sold everything) to one of the largest retailers and land holders in the world – only to be surpassed by Walmart in 1987. For a long time, Sears met consumers where they were.

It wasn’t just that Sears failed to improve its in-store experience and merchandising strategy. Lampert also failed to see how digital could boost the overall business. According to Dennis, the e-commerce business was positioned as a separate play, distinctly different from physical stores. Using stores as digital assets with technology like buy online, pick up in store is a common shield retailers like Nordstrom and Kohl’s use to protect themselves from Amazon.

How Sears’ cost-cutting strategy sealed its fate

While Walmart has evolved to compete in the online-first economy, Sears has not. Of two of the top reasons that Sears’ century of good fortune began to crumble: they incurred massive debts and suffered from severe corporate mismanagement issues.

Web Smith on Twitter

TIL: @Sears used to sell cocaine, codeine, and opium. They were profitable then.

But that doesn’t tell the entire story. Here is a great quote from today’s CNBC article on the matter:

A separate survey of U.S. consumers by Cowen & Co. found the average Sears shopper today is about 45 years old and makes a little more than $59,000 each year. The average Kmart shopper, meanwhile, is a little more than 43 years old and makes about $53,000 annually. That makes Walmart ($55,200), Burlington Coat Factory ($59,100), J.C. Penney ($61,000) and Ross Stores($61,400) the most comparable retailers for Sears and Kmart shoppers when looking at household income, the firm said.

J.C. Penney and Walmart set to benefit

Economics. In a recent study by the Pew Research Center, the middle class is defined as a household with two-thirds to double the national median income. This metric currently includes about half of American households. However, from 2000 to 2014, families that were considered “middle class” decreased in 203 of 229 studied metropolitan areas. This decrease has only accelerated in the past four years. Sears was built for middle-class mall goer. It’s been the thesis of 2PM, Inc. that retailers who’ve built their businesses for this American demo will continue to struggle until the American middle class rebounds.

JC Penney is another retailer that is facing these troubles. Whereas companies like Walmart, Target, Amazon, Dollar General, or Kohl’s have achieved growth by appealing to the upper middle class or economy shoppers. Straddled in debt, and with little to no visionary leadership, Sears failed to execute this pivot. The results have been tragic. Mall owners and commercial real estate developers will have to adopt new strategies to prevent the negative cycles that have occured in the past when anchor stores are abandoned.

But the real economic shift will be felt in exurban, lower-to-middle class areas. These areas are more dependent on shopping malls and the associated commercial real estate developments to fill their open swaths of land. This is where these communities go to shop, eat, and work. This is also where a sizable amount of tax revenue is generated. Without anchor stores or foot traffic for smaller businesses, exurban commercial real estate is nothing more than a house of cards. Next generation retail will not be there. And neither will appreciating homes.

2PM Data

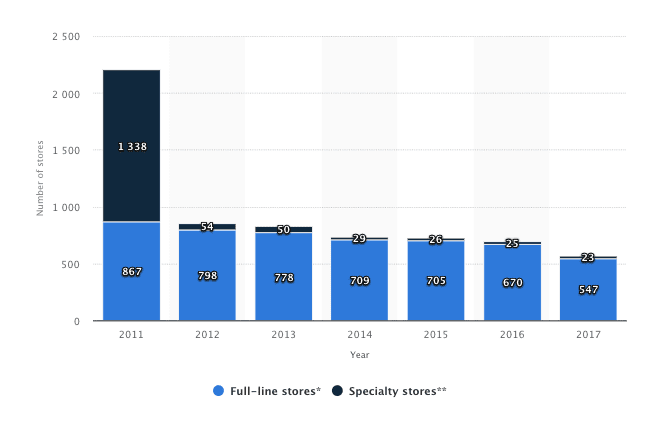

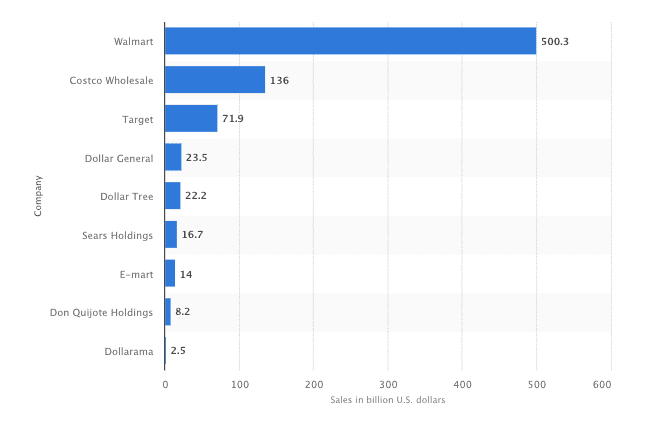

The top 100 retailers are listed below. A common misconception is that Sears was a forgotten retailer. In this recent dataset by Statista, Sears is currently in the top 40 stores in America.

[table id=29 /]

Here is a look several data points that will influence commercial real estate for years to come.

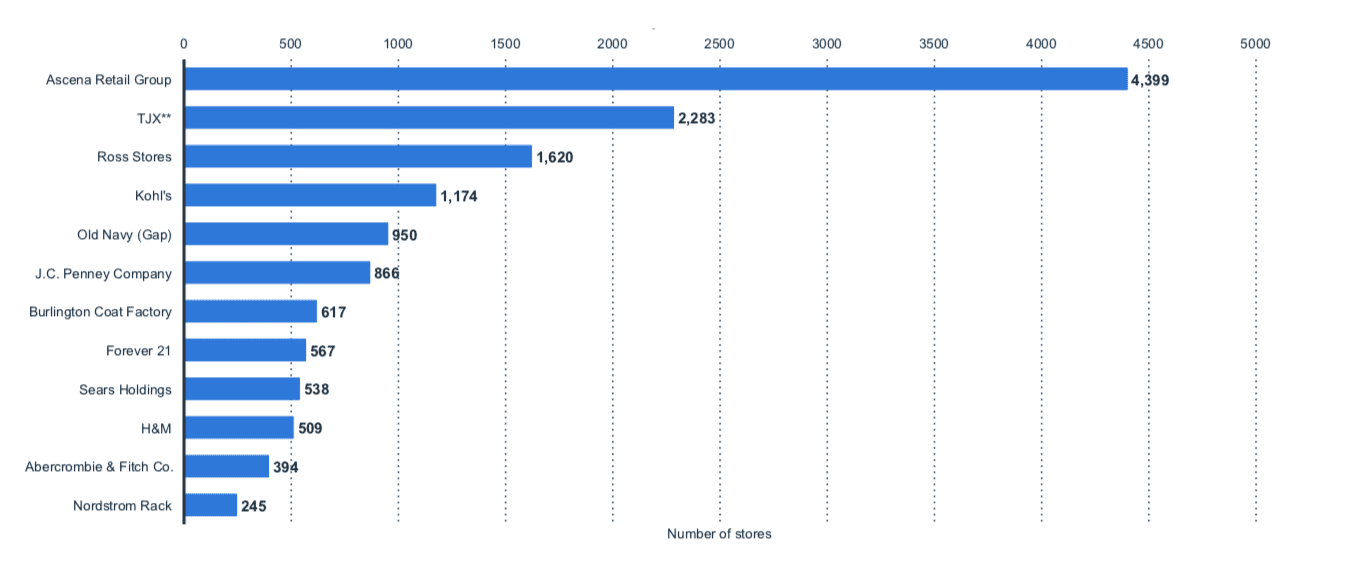

The Sears bankruptcy should be viewed as a warning shot for companies like: J.C. Penney, Burlington Coat Factory, and Ascena Retail Group – a conglomerate of middle class retail brands. Ascena is currently operating 4,400 stores in North America and trading at 25% of its historical highs. Retailers that have been dependent on debt and brick and mortar foot traffic are overdue for an evolution of their approach to reaching a) existing customers in a dwindling demo or b) finding innovative ways to reach new customers in growing demos: economy and up market.

The death of retail as we now know it is greatly exaggerated. Retail isn’t dying; it’s evolving. Just like it has done before. There has always been disruption in the retail sector. A major disruption occurred in the late 1800s when Sears introduced the catalog and brought the entire store into the homes of U.S. consumers. This gave Sears the same advantage over brick and mortar stores that eCommerce sites have today. Sears was simply responding to the needs of its customer since 60 percent of the U.S. population lived in rural areas at the time and didn’t have convenient access to stores. Sears would bring the store right to them.

Nearly 111 million square feet of retail space will be lost in this bankruptcy. For the Tier A malls that will be affected by Sears’ closings, consumers will see new consumer or events spaces in place of the historic retailer. But for Tier B/C malls, Sears’ closing will become another eyesore that will influence aspirational consumers to shop elsewhere. Sears once thrived on the principles meeting customers where they were. Evolving customer needs requires leadership that understands where consumer mindshare and dollars are going.

Read the curation here.

By Web Smith | About 2PM