With a new Apple partnership, Stripe just secured more power in Silicon Valley. The running joke is that any advancement by Stripe is indicative of its “mob boss” mentality, a reference to the recently viral thread by the founder of Bolt. In actuality, Stripe is showing just how much of a positive-sum mentality it’s using by building more dynamism into American retail and entrepreneurship.

Much has happened since this pre-pandemic report on “falling American dynamism,” a term that I prescribe to suggest that entrepreneurship was falling in popularity. In that report, I explained:

The more that conglomerates exist, the more we’ll see dynamism collapse. As a number of those companies begin to succumb to antitrust scrutiny, dynamism will be called upon to close the gap between the age of conglomeration and the need for new, high-growth businesses.

The idea behind that essay was that companies like Google, Facebook, and Apple were so powerful that it was beginning to make tech employment more popular than self-starting entrepreneurship. Of course, the flip side of this argument is that most businesses cannot survive without using Google, Facebook, or Apple. In the essay, I assigned special value to Jack Dorsey’s two companies, Twitter and Square (now Block), and their positive value to dynamism (word of mouth marketing and ease of transaction). Apple builds on that positive impact with its latest project and I believe that the entire fintech ecosystem will benefit along with the advancement of the end user.

In most media reports, the Apple Pay x Stripe partnership is positioned as competitive with Dorsey’s company. I’d argue that Stripe has no interest in competing with Block, a nod to the positive-sum mentality of Stripe’s founders. In fact, I can see a future where they partner with Dorsey’s hardware/ financial services. But not everyone thinks this way about Stripe.

Days after former Bolt CEO Ryan Breslow compared the company to the mob boss of the tech world (and was retweeted 1,600 times), it was announced that Stripe would be the launch partner for Apple’s upcoming Tap to Pay technology. Tap to Pay turns Apple devices into payment hardware, making credit card swipe attachments essentially unnecessary. (That’s a separate lesson for hardware companies that have built their businesses on being middlemen for Apple and payment services.) This product partnership is the result of a 2020 Apple acquisition of Mobeeweave, an NFC innovation that enabled iPhones and other devices to operate as pay terminals without additional hardware. Apple Pay’s partnership with Stripe is expected to operate with Mobeeweave’s technology.

Whether or not Apple will approach this opportunity to monopolize payments and take on competitors like Block and Venmo is the next debate. Pointed out by NextWeb, Block is more than just a payments portal – it helps small businesses manage inventory and analytics. Shopify’s stake in Stripe boosted its positioning as the payments manager of choice for entrepreneurs and small-and-medium sized businesses. Apple’s Tap to Pay appears to only facilitate payments, but if it were to move beyond the point of sale to the backend management of inventory and data, that would give it a bigger role in the space where Block and Shopify currently operate. Or, Apple could choose to open up Tap to Pay to more partners, widening its reach in assisting payments despite the platform the seller uses. This is the most likely play, in my opinion.

It’s important to consider Apple’s ambitions in fintech. With Apple Pay standing tall as the most adopted technology, Tap to Pay seems like the extension of a strategy that’s just getting started. From Next Web:

Over the last few years, Apple has been focused on expanding its services business — especially financial offerings. In 2019, it launched the Apple Card, and plans to expand it to more countries. Last July, a Bloomberg report noted that the company is exploring a “buy now, pay later” product with Goldman Sachs. If Apple starts accepting payment on a seller’s behalf, it can explore more financial products, ranging from loans to management services. Really, this news shows how serious Apple is about getting its services to reach a $1.5 trillion valuation alone. And, at this stage, who would bet against it?

Two years later and dynamism is on the rise. The “great resignation” has led to 47.4 million American voluntarily leaving their jobs in 2021, according to CNN data. ADP Chief Economist Nela Richardson was recently quoted:

We’re seeing a lot of churn in the jobs market. But one thing we are seeing is that hires are higher. They’re not leaving the jobs market, they’re leaving for other jobs in the same industry.

But to the earlier point of dynamism, it’s not all corporate upward mobility, the pandemic has influenced a boom in dynamism. An August 2021 report in the New York Times began:

After waning for decades, applications to start businesses surged last year. If the rebound proves durable, it could provide a more resilient economy.

So it is through this lens that I see the positive sum game that the Collison brothers are playing with Apple. Will it have an impact on Block’s hardware business? Yes. But that does not mean that Apple won’t partner with Block in the future. Block sells full point of sale systems for readers; this new Apple / Stripe partnership will only impact Block’s dongle business.

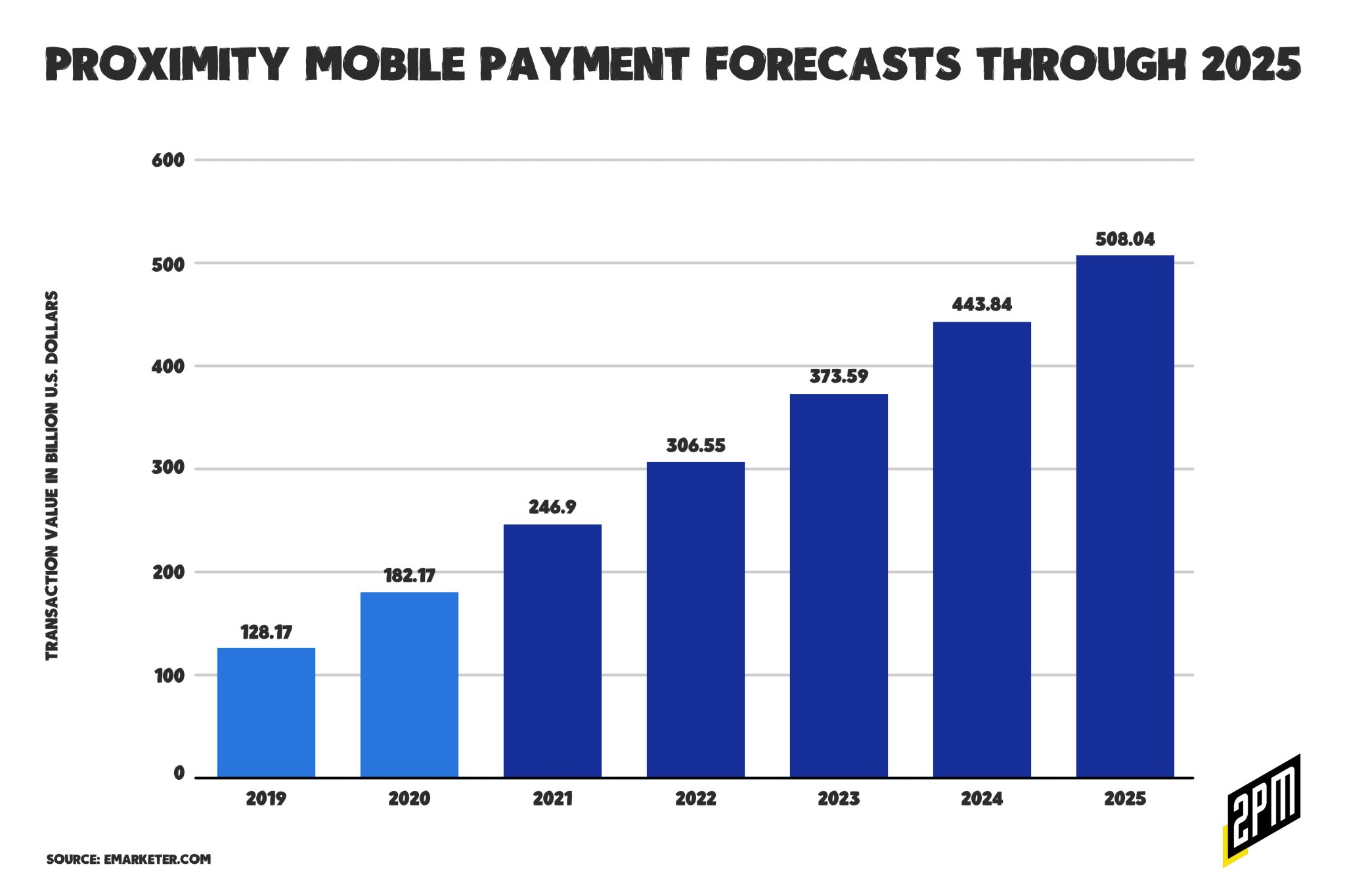

Viewed this way, Apple’s Tap to Pay could be helpful to Block as it removes the need for the dongle, giving users more and easier ways to pay, without making the dongle obsolete. Protocol makes the argument that Block is then freed up to focus on other services that are more profitable than a hardware business, including banking, payroll and other financial services. By making it easier for anyone to accept payments via iPhone, smaller business owners and entrepreneurs who aren’t looking for full POS machines can start selling, widening Block’s pool of potential customers in the long run. Then, more can win as the market for proximity payments expects to double over the next four years:

A positive-sum mentality and dynamism go hand in hand. Lost in the news cycle on the Apple Pay x Stripe partnership is that the same technology will be powering Shopify’s similar solution in the coming months. Stripe will be offering the Tap to Pay solution for iPhone users through a new Shopify app, as well.

Dynamism is defined as a theory or philosophy that explains something in terms of great energy or force. In the context of entrepreneurship, it goes hand and hand with payments technology, specifically the way that we use our phones. It is easier to pit one company against the other than it is to understand the bigger picture here. The United States is currently in eighth place behind China, South Korea, Vietnam, Norway, the United Kingdom, India, and Spain with respect to mobile payment adoption. China’s penetration was 39.5% to America’s 17.7% (as of August 2021). With an emphasis on making peer to peer transactions easier, businesses of all kinds can grow in sophistication and in reach.

And in doing so, Apple will achieve its goal for Apple Pay. It wants the payment technology to no longer be bound by the hardware that launched it. As Stripe has become the processing layer beneath much of commerce, Apple likely has aspirations to do the same for the transactions layer. And it won’t care if the trade is happening on iOS, Android or through Block, Shopify, or even Bolt. Dynamism is about agility and reach and it seems to be on its way back.

By Web Smith | Edited by Hilary Milnes with art by Alex Remy and Christina Williams

Disclaimer: 2PM is an investor in Fast, a competitor to Bolt. To Ryan’s Breslow’s point, Stripe is an investor in Fast. But Bolt has been noted as better positioned with more money raised, more enterprise clients, and a higher GMV. Stripe has been noted as being competitive with Fast in a few of its recent initiatives. Ok, I am tired.