On the heels of Elliott Management’s plan to remove Jack Dorsey from his chief executive role at Twitter, this report looks at: dynamism, corporate conglomeration, and a model for outside-of-the-box thinking that new entrepreneurs can learn from. Twitter isn’t behind the curve, it may be ahead of its time.

A defense of Jack Dorsey’s leadership is a defense of polymathic thinkers in business. The public markets have rewarded the type of deep-specialization that Dorsey shuns. However, those same markets are beginning to reflect the American economy’s falling rates of dynamism. In a 2012 article by Harvard Business Review, entrepreneur Kyle Wiens wrote:

We live in an age where deep-specialization is highly encouraged — the era of what tech analyst Vinnie Mirchandani calls the “monomath.” Doctors specialize, lawyers specialize, academics specialize, mechanics specialize … just about everyone professionally specializes. The more deeply you specialize, the more money you’re likely to make. And that’s fine. Except when it’s not. [4]

One can infer from a number of employment data sources that the United States is approaching a new period of job market revision, though deep specialization will always remain common in professions such as medicine and academia. Being able to view a problem from a number of angles, avoiding narrow analysis, is re-emerging as a high professional value. Polymathory is a personality trait that Dorsey identifies with. But more importantly, his helming of Twitter and Square is one of the few remaining pillars that addresses diminishing paths to middle-class entrepreneurship.

Audience and Commerce. In a unscientific 2PM poll (n=632, take home income: $42,000 – $98,000), the following tools were selected out of nearly thirty options. Each was noted for their value to middle-class, early-stage entrepreneurs: Twitter (27.1%), Reddit 17.8%) Gumroad (11.1%), Patreon (22.9%), Substack (7.3%), Shopify (31.1%), and Square (29.4%).

The more focused the company, the more aligned with early-stage entrepreneurship they appear to be. This comes at a cost, however. Critics question Twitter’s eschewed advertising potential, a growth that comes by conglomerating the business. Academia and public markets generally conclude that corporations that are polymathic in nature (companies that operate seamlessly in three or more distinguished industries) are valued at a premium. There are a number of companies that come to mind: AT&T, Facebook, Amazon, Comcast, and Google. For decades, these corporations have been allowed to operate new verticals with minimal government oversight. The polymathic corporation is relatively new to the American imagination but the polymathic individual has been long discouraged.

The age of conglomeration can be directly tied to the diminishing number of startups launched in the United States. After Reagan’s Antitrust Explosion of 1982, elements of the law began to shift from structuralism and toward consumer welfare. That year, AT&T and IBM faced antitrust litigation that forced changes in each company by 1984. [1] This period would eventually manifest in ways that are just now becoming scrutinized; it’s led to a new form of anti-competitive behavior. This meant that new companies would launch, only to be snuffed out by the faster-moving, well-capitalized companies like Facebook, Google, or Amazon.

The market rewards these companies and rightfully so; they are nearly immovable. The media landscape would have readers believe that entrepreneurship is at an all-time high. However, this couldn’t be farther from the truth. The American economy is ossifying. In The Complacent Class, Tyler Cowen writes:

These days Americans are less likely to switch jobs, less likely to move around the country, and, on a given day, less likely to go outside the house at all […] the economy is more ossified, more controlled, and growing at lower rates.

A defense of Jack Dorsey is a reminder that Twitter is one of the few major media platforms with little risk of antitrust action. A pivot towards a Facebook or Google-like model of conglomeration is a reward with a proverbial expiration date. A chief argument by activist investor Elliott Management is that, unlike Facebook or Google’s expansive catalogue of audience and advertising products, Twitter has hesitated to innovate. I believe that this has been by design.

Investors have complained that Twitter has failed to come up with innovative new products. Though its core social network remains prominent — it is one of President Trump’s primary bullhorns — upstart rivals including, most recently, TikTok, have seized the public’s imagination and eyeballs. [6]

Consider the campaign trail where candidates on both sides of the line of demarcation are comfortable critiquing anti-competitive behavior. It’s common to see Twitter’s contemporaries to be mentioned. From Senator Warren’s platform [2]:

America’s big tech companies provide valuable products but also wield enormous power over our digital lives. Nearly half of all e-commerce goes through Amazon. More than 70% of all Internet referral traffic goes through sites owned or operated by Google or Facebook.

Specialization vs. Deep Generalism

To land one of America’s most coveted and secure jobs, it would be best to mask one’s multi-disciplinary interests. If Jack Dorsey didn’t start a company, it’s unlikely that his varied interests would appeal to the typical executive recruiter. And this is despite a superior track record as a software engineer.

This wave of career-specialization was a response to a trend of industry conglomeration that’s influenced public markets for decades. Executive recruiters cited certain benefits to building resumes of this sort: increased value proposition, shortened learning curve, “perception of authority”, higher conversion, and superior networking.

The rise of the corporate conglomerate coincided with an emphasis on post-collegiate specialization, a trend that was influenced by hiring practices and job security of coastal technology companies. Rufus Franck, founder of Consultants 500 explained [3]:

When you take a look at the Fortune 1000 over the last 40 years, starting from 1973 you see that major changes have taken place. By 1983, one-third of these companies have fallen off the list. By 2013, only 30% of the original companies are still on the list. This pace of change will continue to increase as only a third of today’s major companies are expected to survive the next 25 years.

Twitter and Square seem to operate differently than many of its aforementioned contemporaries. Created in 2006, Twitter.com ($27.32b) has revolutionized two-way communication with public persons, news, and business. For power-users, it has become what LinkedIn was designed for and what Facebook can never be. It is the platform that is closest to a globally-available forum for ideas, creativity, research, and culture.

Likewise, Square has revolutionized credit and cash transactions. Founded in 2009, Square ($34.77b) has accomplished a great deal in the commerce and peer-to-peer payments space. It’s Cash App product is a billion dollar property, according to analysts. The two companies haven’t taken on the form of today’s polymathic (conglomerate) corporation. Perhaps, because it has one at its helm.

The argument to consider is whether or not the platforms are better as focused vs. positioned along a path to conglomeration.

…Except When It’s Not

The more deeply you specialize, the more money you’re likely to make. And that’s fine. Except when it’s not. Before the announcement of Elliott Management’s acquisition of $1 billion worth of Twitter stock, Dorsey’s most prominent critic was entrenched in academia. When New York University’s esteemed Professor Scott Galloway wrote to Twitter’s Executive Chairman in December 2019, it would become a call to action for a number of restless public market investors and institutional holdings. Galloway began his letter with clear intent:

To be clear, my primary objective is the replacement of CEO Jack Dorsey. However, your firm’s weapons of mass entrenchment include a staggered board that may force shareholders to seek to replace other directors, including yourself, first. [….]

It is difficult to ask people to work evenings and weekends when the CEO works mornings (is part-time). The exodus has resulted in anemic product development that has stunted growth and monetization. [5]

Admittedly, Dorsey has few executive comparisons. Though, when critics and advocates do attempt to provide an analog to his personality: Steve Jobs is occasionally cited. Critics will compare Dorsey’s worst characteristics to Jobs’ antics: lack of focus, imbalance, knack for stoicism, and pursuit of spirituality. Advocates will compare Dorsey’s best characteristics to Jobs’. Most often, this comparison ends at both executives’ ability to run two large companies at once.

In the fourth quarter of last year, Twitter generated more than $1 billion in revenue, a first for the company. Advertising sales of $885 million during the quarter were up 12 percent from the same time in 2018. And the number of users who see ads on its platform on a daily basis grew 26 million in 2019, up 21 percent from the prior year. [9]

This is fair, there will only ever be one Steve Jobs, a leader with the talent to run Pixar and Apple in tandem. Jobs founded Pixar when he was fired from Apple. He returned to Apple once it acquired NeXT, yet another company that Jobs founded and led. He remained in a leadership role at Pixar until it was acquired by Disney in 2006. The iPhone debuted within a year of Pixar’s acquisition, an inspired device that found new ways to combine media, technology, and commerce. But to be fair to Dorsey, he’s successfully running two companies with a combined market cap of nearly $70 billion and he’s doing so with an eye on the future of two evolving industries: media and commerce.

The Call For Dynamism

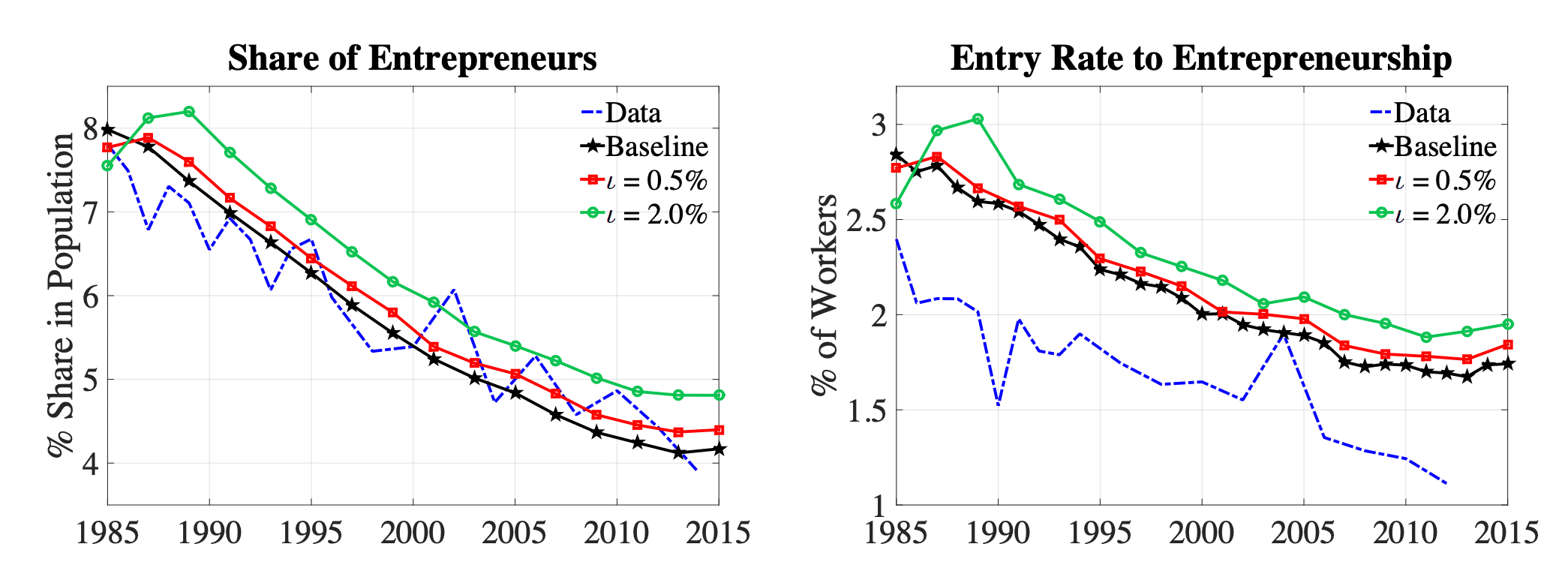

A critical factor in accounting for the decline in business dynamics is a lower rate of business startups and the related decreasing role of dynamic young businesses in the economy. For example, the share of US employment accounted for by young firms has declined by almost 30 percent over the last 30 years. [7]

Multidisciplinary thinking is a shared trait of early-stage business leaders. To solve new, difficult problems, it takes more than abundant funding. It requires the type of outside-of-the-box thinking that Dorsey has prescribed and conglomeration has discouraged.

The markets may not reward Twitter for its market discipline until conglomerates like Facebook and Google begin to adjust as the headwinds of government scrutiny and new data privacy legislation continue to mount. Data-privacy bills are being authored across the United States at an incredible pace. Today, New Jersey’s legislature joined this conversation:

The bill would require companies to obtain permission from New Jersey consumers before they can collect and sell personal data to third parties. The legislation, which would apply to internet companies like Alphabet Inc.’s Google and Facebook Inc., would have implications for any company that collects consumer data. [8]

As data privacy becomes more of a concern, a pivot towards commerce is the intuitive path. We’re beginning to see this with Facebook’s emphasis on Instagram’s cart capabilities or Google’s acquisition of Pointy and its emphasis on marketplace development. Imagine if Twitter had a CEO with practical knowledge of both of these disciplines. Would its board dismiss that chief executive?

Conclusion

Twitter has avoided a number of the headwinds facing today’s top corporate conglomerates: (1) media’s pivot from advertising data to transactional data (2) antitrust scrutiny of conglomerates (3) a growing chorus of data policy concerns. It’s precisely Dorsey’s outside-of-the-box thinking that may serve his companies well as the shift towards linear commerce continues.

Square and Twitter represent two fixtures of industry (media and commerce) that have grown without infringing on other verticals. But more importantly, both companies represent a sort of democratization of entrepreneurship that is required for dynamism to mark its return. In short, they are two of the last remaining tools of early-stage entrepreneurs.

On a technical front, it’s possible that Square may be of service to Twitter’s appeal to brand partnership as platforms reimagine advertising in the privacy-driven data economy. Together, Twitter’s best chance at pioneering a path forward is with Dorsey. But Dorsey’s appeal to dynamism’s reemergence isn’t solely based on the two companies that he helms. He’s the rare founder-CEO that isn’t protected by classes of voting shares, another emblem of today’s risk-less nature of conglomeration. Rather, his style of leadership translates well to aspiring entrepreneurs looking to establish careers outside of career specialization. This, I believe, is a precursor to dynamism’s reemergence.

Dorsey’s leadership style a needed in today’s public markets. And it may take the public market’s tolerance of his style of multi-disciplinary thinking and leadership. Surely, the incredible team at Elliott Management may come to a similar conclusion once wider data points are considered. But admittedly, Dorsey may finally need his own Jobsian moment to silence critics and pacify supporters, alike.

Report by Web Smith | About 2PM