One is known as an entertainment savant of sorts: he is a writer, rapper, actor, director, comedian, film and television producer. Donald Glover’s show “Atlanta” can be watched on Hulu, a streaming property owned by the Walt Disney Company.

One is known for his successful replacement of Michael Eisner and his ensuing acquisition of Pixar films, returning the Walt Disney Corporation to its animation roots. Bob Iger also led negotiations to acquire Marvel Entertainment, and then three years later acquired LucasFilm. And six years after that, Disney purchased assets from Fox. But most importantly, Iger self-identifies as a centrist and has been appointed to positions by two of America’s most powerful political families: The Clintons and The Trumps. According to his Wikipedia page, Iger considered a 2020 election run but later chose to discard his political ambitions. Netflix Founder and CEO Reed Hastings nodded to both key attributes of the latter:

Ugh. I had been hoping Iger would run for President. He is Amazing.

Two days after the firing of Bob Chapek, Iger assumed his role as CEO (again).

Glover’s most fascinating episode of his final season of “Atlanta” featured an odd story about the hiring and firing of a Disney CEO amidst the backdrop of cultural and political change.

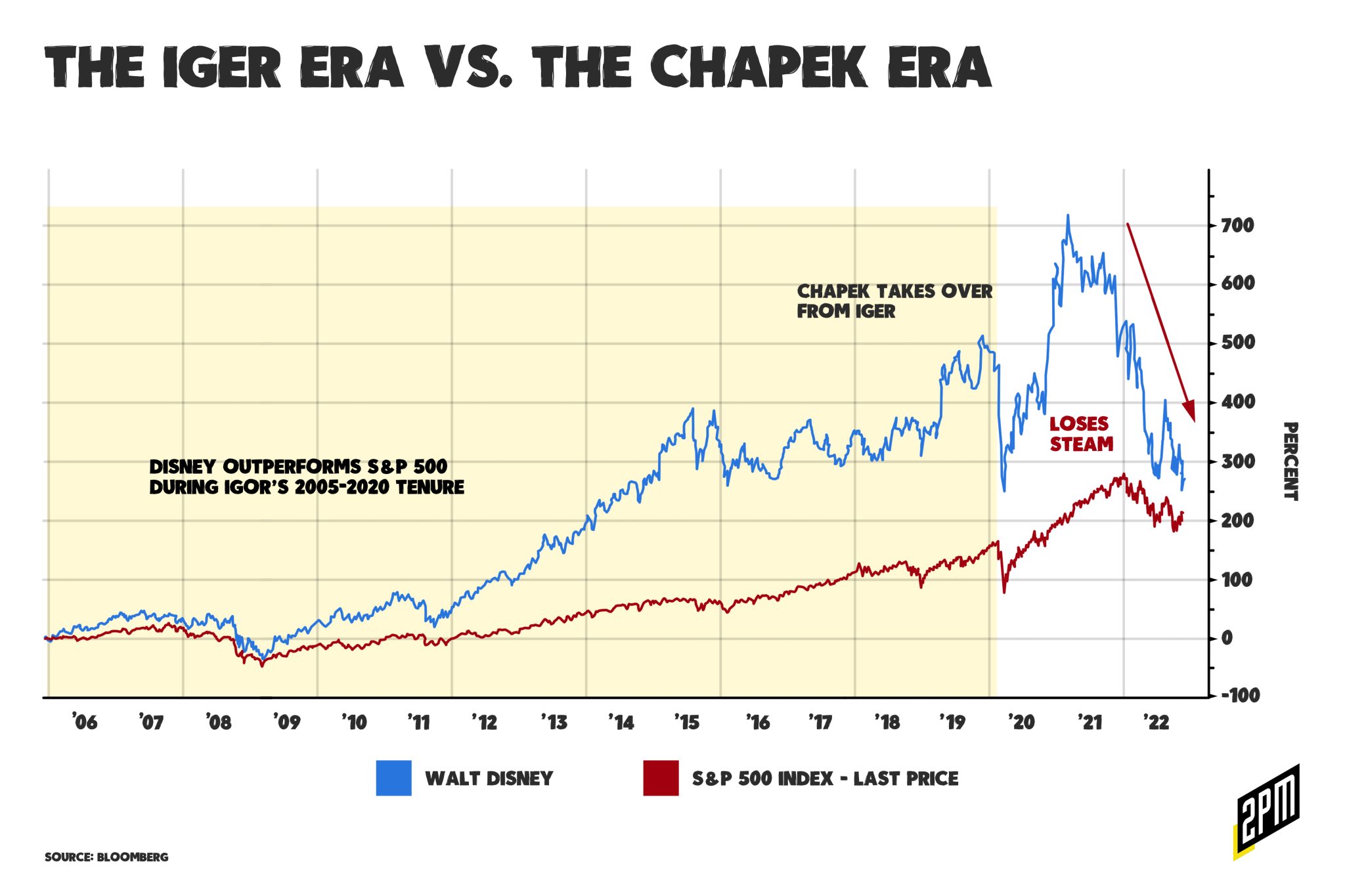

Chapek’s tenure as CEO was cut short, not for any other reason than Iger realized he was not going to be able to run for Governor of California or President of the United States. It is a dream deferred for Hastings, who now must match up against the industry’s most capable executive. While the narrative will likely hold that Chapek’s missteps cost him his seat, it’s more likely that Iger is just better at the job and is much better at managing the political pressures of the time we’re in.

It was Bob Chapek and Chairperson of Distribution Kareem Daniel who ultimately signed off on the Donald Glover-led “Atlanta” episode that featured a fictional documentary about an African-American man named Thomas “Tom” Washington. The show featured a faux-disclaimer at the show’s beginning, taking a subtle jab at Disney’s management. It was surreal. In the episode (S4E8) that I highly recommend that you watch, Washington was CEO of the Walt Disney Corporation leading up to the 1995 release of “The Goofy Movie,” a film that has long been viewed as Disney’s first film for black millennials. Vulture Magazine presented the best summary of the Atlanta episode’s premise:

As racial tensions rose in L.A. and across the country, Disney happened to lose its CEO due to ultimately fatal health complications. The executive board voted for Tom Washington — a man whose real name was Thompson Washington, not Thomas — thus installing a Black CEO due to a clerical error. Not wanting the optics of quickly hiring and firing a Black man, and being unable to sweep things under the rug because of Tom’s insistence that he is rightfully the CEO, Disney moved forward with the accidental decision.

In the faux-documentary, the first black CEO of Disney radically changed the organization’s creative process to promote stories of inclusivity. In this narrative, The Goofy Movie was a film about Black-American fatherhood, produced by a Black-American father. As CEO, Tom Washington turned the organization inside out to build a company that highlighted its black talent and black stories. Then, the Board of Directors unceremoniously saw him to the door and course-corrected by hiring someone more suited to lead the company in a centrist manner. The Goofy Movie hit theaters as a less-radical version of the vision Washington had for the film.

In a way, this feels so meta to write. The episode of Atlanta was a stroke of genius. And it may go down as somewhat prescient given the recent critiques of Disney mirrored the critiques foreshadowed by the episode of Atlanta. The three executives who likely signed off on the project were CEO Bob Chapek, Kareem Daniel, and Dana Walden, Disney’s current Chairman of Digital Content.

Walden was promoted into the role after Chapek’s unceremonious firing of Peter Rice. Like Atlanta’s episode on Disney’s executive management, the company seems to be adept in firing executives without warning. Variety wrote about Rice’s firing:

By all accounts, Rice didn’t see it coming — at all. He was blindsided as he learned of his fate in what was described by a source as a conversation with Disney CEO Bob Chapek that lasted less than 10 minutes. Chapek simply felt that Rice was not, in fact, Team Chapek, according to multiple sources close to the situation.

So, after one of the most surprising terminations in the entertainment industry, Chapek suffered the same fate just five months later. And Bob Iger is back at the helm at Disney after two years. Iger’s return is effective immediately, will last two years and comes “with a mandate from the Board to set the strategic direction for renewed growth and to work closely with the Board in developing a successor to lead the company at the completion of his term,” according to Disney’s press release. The board fired Chapek, who was handpicked by Iger to replace him, on Sunday. In a way, a Disney property (Atlanta can be seen on Hulu) foreshadowed its own corporate concerns and changes.

It’s been a turbulent two years for Disney under Chapek and some of it is Chapek’s own doing. The company’s shares have fallen 40% this year and it reported in the most recent quarter that Disney+ lost $1.5 billion despite growing its digital subscribers. But how do you follow the leadership that bought Pixar, Marvel and Stars Wars over 15 years? A series of Chapek’s early moves were not very well received by the industry or by customers. Quartz sums up a series of misfires:

It was a given that Iger would be a tough act to follow but Chapek made his own leadership blunders including a bungled reorganization, an ugly public spat over Black Widow star Scarlett Johansson’s streaming remuneration, and his botching his response to Florida’s controversial “Don’t Say Gay” bill, which restricted instruction on gender identity and sexual orientation in classrooms. (Iger did not explicitly call him out on the latter, but did say it’s a matter of “right or wrong” and “you have to take a stand.”)

Under Chapek’s leadership, Disney was often mischaracterized with that eye-roll of an adjective: “woke.” This characterization was used for every content decision and park strategy. Chapek managed to anger both major political ideologies by action or inaction. By comparison, Iger was more comfortable dealing in political proxy wars by being direct and decisive. Variety explained:

Chapek’s reluctance to wade into the controversy came in contrast with his predecessor, Bob Iger, who tweeted his opposition to the bill on Feb. 24. Chapek is said to be less willing than Iger to take political stands in general. But he is facing a climate in which employees have become more emboldened to demand action from their bosses.

Ultimately, it may be the firing of Rice that most contributed to Chapek’s own firing. It wasn’t just Disney’s struggles with its park division, poor viewership ratings, or the unit economics of its streaming product. According to ScreenRant:

In the end, though, Chapek’s fate was likely decided by a disappointing financial statement at the beginning of November 2022. The core problem lies with streaming; although Disney+ has exceeded expectations for subscriptions – ironically helped by the pandemic – it is still making a loss.

Chapek’s answer to his streaming concerns and Disney+’s failed unit economics was to fire the well-liked Peter Rice and to replace him with Dana Walden. Chapek didn’t give much reason, according to Variety’s recounting of the incident, but the opinion was that Chapek “didn’t think Rice was fully behind him.” I read this as “Peter Rice could be CEO after me, potentially shortening my tenure.”

Iger has two years to reset the company’s path and find another successor. Iger’s decisions and rationale for them will be definitive and unwavering – surely changing the perception of Disney and its politics.

The faux Disney documentary was larger than life and just believable enough to confuse some of Atlanta’s casual viewers. There were archival clips, nostalgic details, and real events that peppered the narrative. The story seemed both far-fetched and believable. But this week, a CEO who just received a three year extension was fired over a weekend with no notice. This was also far-fetched and believable.

One of the first changes made was Iger’s termination of Chapek’s top lieutenant Kareem Daniel, the Chairman of Disney’s Media and Entertainment Group. To Daniel’s credit, he helped streaming services grow to 235 million active users. The decision places more power with the content creators and less with the streaming service executives who distribute their work.

In a September interview with Daniel, he explained:

So you fast-forward to this new organization that is two years old next month … There’s incredibly talented content teams that are making things that are entertaining people all over the world. I feel like I have a bit of understanding of what that’s like having spent time in a creative organization without that ultimate authority, where I know that collaboration is absolutely critical. You can’t operate a business without having a true appreciation and connection with that creative group.

Disney’s DTC division (which includes Hulu and ESPN+) lost $1.5 billion in Q3 2022. In Q3 2021, that figure was $630 million. Daniel’s distribution strategy was an obvious flaw. Within 24 hours, Iger showed an appreciation and connection with the creative group. And in the process, he established that streaming may no longer be the holy grail for Disney. Atlanta’s four season run on Hulu ended at the right time and Reed Hastings may be happier after all. Disney+ may be less of a concern to Netflix.

By Web Smith | Edited by Hilary Milnes with art by Alex Remy and Christina Williams