There were several aspects of Elon Musk’s personality that I picked up on when reading Walter Isaacson’s eponymous book. My short notes from the book included: “Elon seemed destined to do what he’s done.” And, “[Elon Musk] was an excellent book written about a man whose life was far from over.” But even in my notes, I improperly communicated what I understand about him. The average person hears “destined to do…” and believes that the skids were greased for him. I meant precisely the opposite. The first-generation American was as far from a scion as one could be despite how often the general media portrayed his parenting-to-career pipeline. He did have it hard growing up, he has an extraordinarily high risk tolerance, he’d been punched in the face (a fact that the average person cannot relate to), he’d been betrayed a number of times, he probably suffers a litany of mental health issues, and his mind works at a different pace and process than the vast majority of ours.

I think that it’s important to preface my analysis with the above because, though not a true journalist, I was more prepared for a one on one interview than Don Lemon was. Why? I read that book. The biography contextualized much of what I know of his companies, his work style, and him. It’s precisely because of that work style that I am confident in my belief that he would never consider what I propose. But it would be an “entertaining outcome” to consider.

The last time that I wrote about Tesla was in 2018 and in the shallow context of luxury, consumer psychographics, and DTC mechanics. I explained:

American manufacturers who are competing in the luxury space may not realize it yet. Despite Tesla’s many flaws in logistics and leadership, Tesla’s eCommerce operations have laid the groundwork to become a top of mind luxury product.

I believe Tesla’s core problem is less about Elon Musk’s scattered attention and perceived persona. I do believe that the car brand is no longer aspirational, the technologies once considered luxurious are more commonplace, and the novelty of well-engineered electric vehicles has gone down-market, cross-market, and up-market – each at Tesla’s expense.

It’s my belief that the company can correct this if it altogether reconsiders its pursuit of selling autonomous robo taxis. It would be an “investment thesis pivot,” a phrase coined by Barclays analyst, Dan Levy. This presents an alternative strategy, the “Tesla Bros” strategy.

The “Tesla Bros” Strategy: Rivian and Lucid

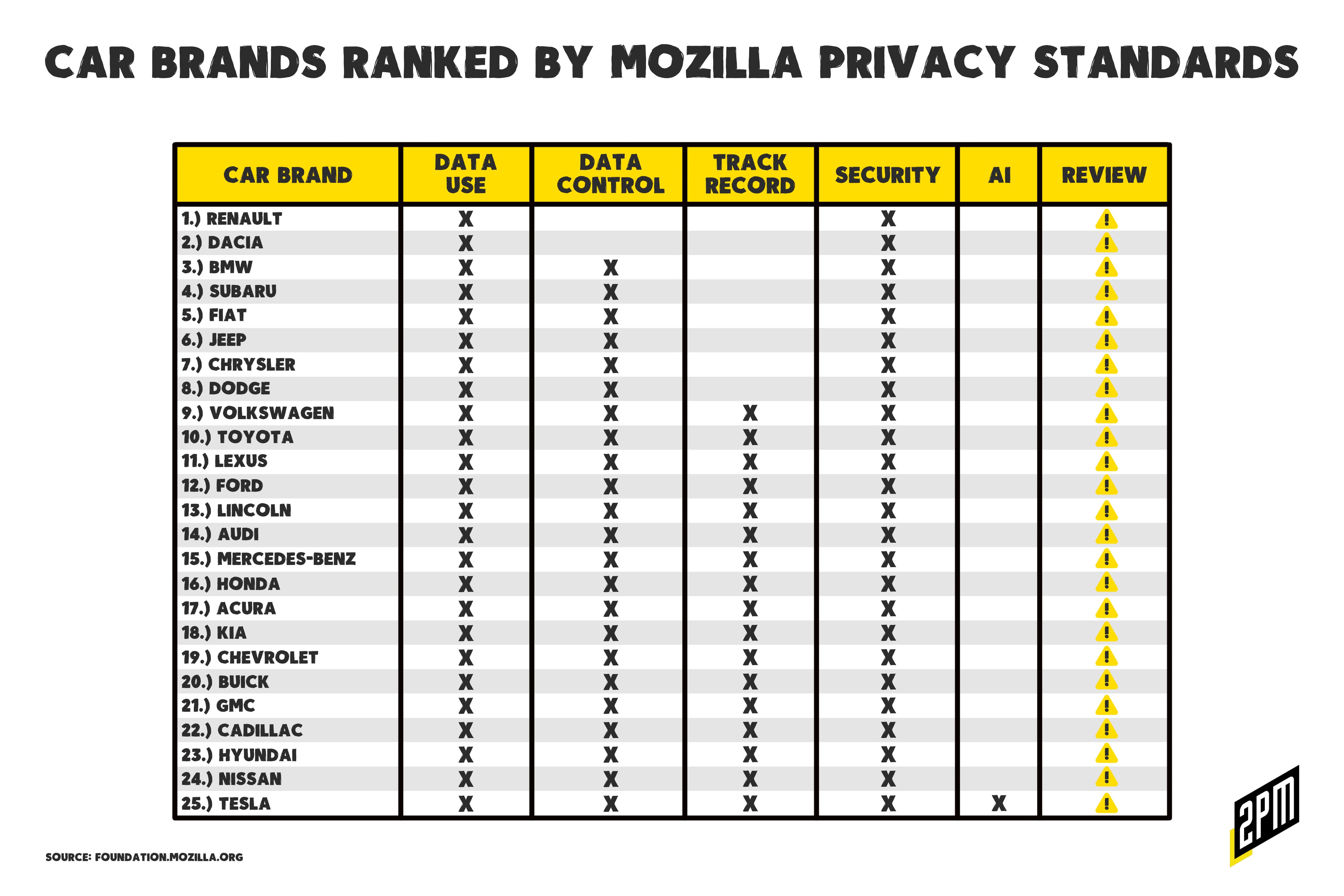

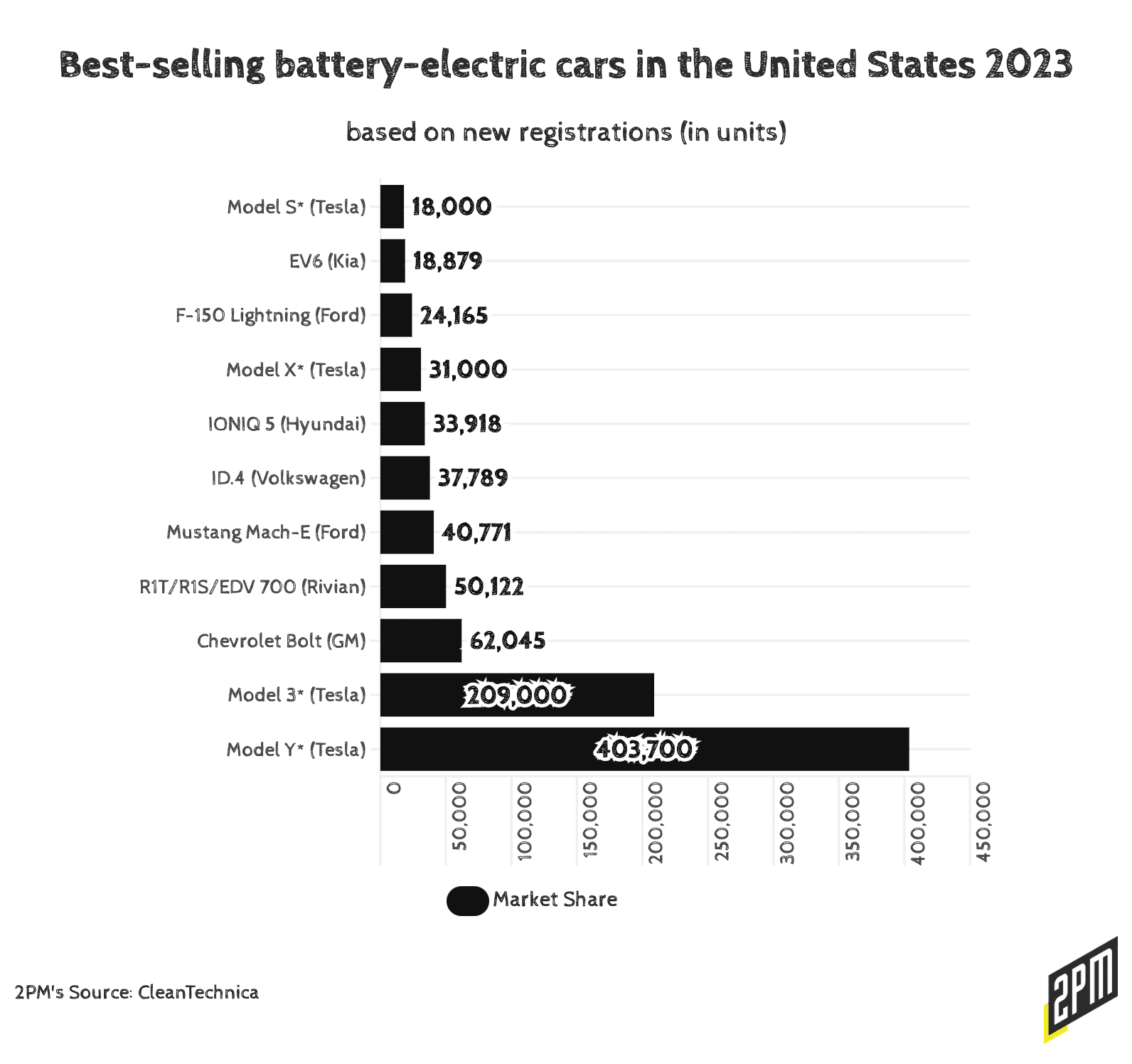

Tesla is at a crossroads. Despite its Model Y market share and its persisting brand prestige, it faces mounting challenges from both established automotive giants like Hyundai, Volkswagen, BMW, and Ford and emerging competitors – foreign and domestic. Look no further than BYD and Lucid. Here is a great snapshot of the best-selling EVs.

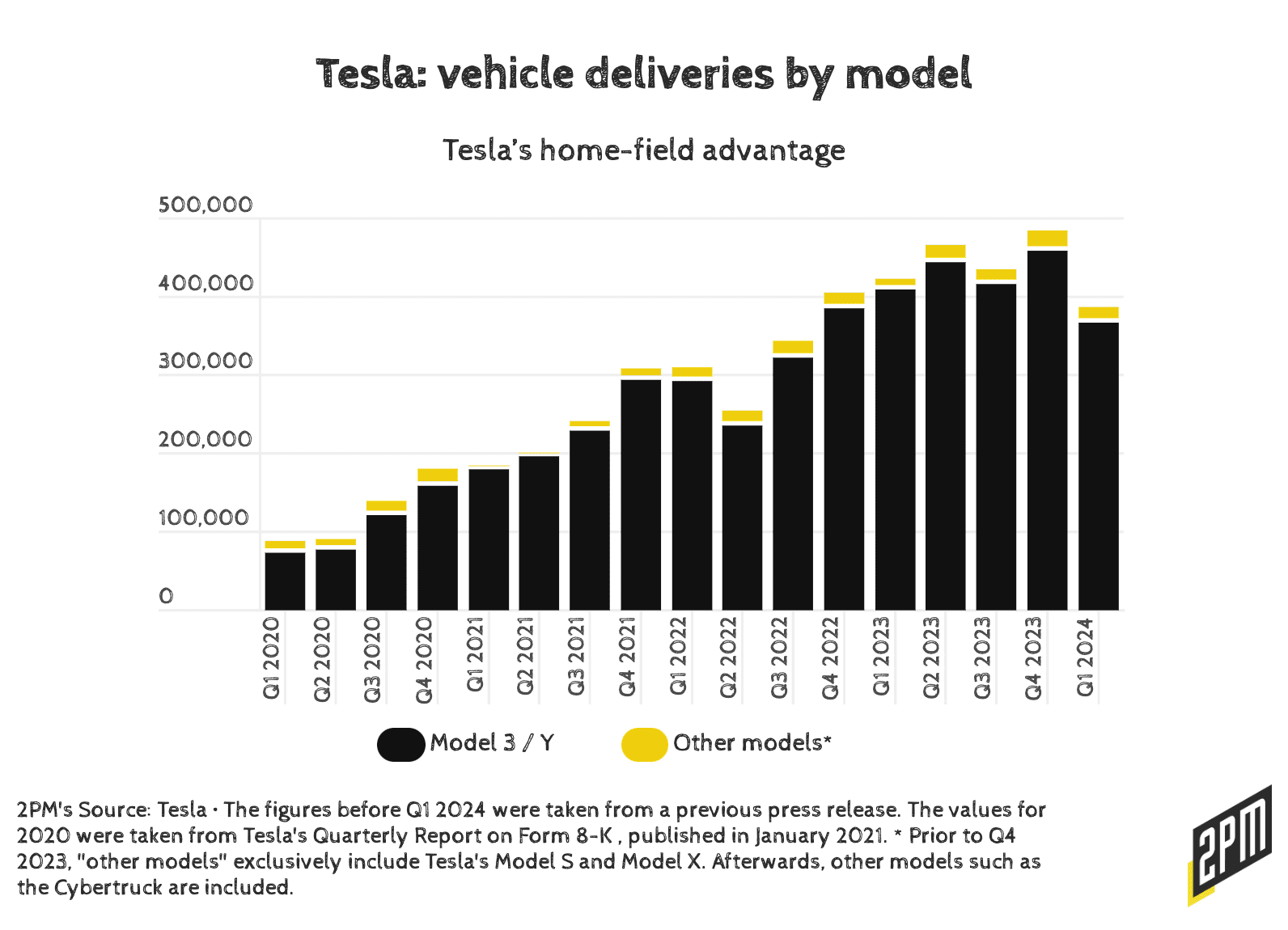

Tesla’s path to sustained dominance may lie in strategic acquisitions. Of the top of mind, acquiring Rivian and Lucid could be a masterstroke to bolster Tesla’s position as a luxury manufacturer against traditional American manufacturers, European luxury brands, and China’s rapidly ascending BYD brand. Review graph No. 3 of 5 for context.

Acquiring Rivian and Lucid could strategically reposition Tesla as “aspirational” in the upscale EV market while rejuvenating its model lineup and breaking the monotony of its current offerings. This could also improve pricing integrity and down market sales. Rivian’s adventure-oriented electric trucks and SUVs, alongside Lucid’s luxury sedans known for cutting-edge interior design, agility, battery technology, would provide Tesla with fresh, innovative models that cater to diverse consumer segments. The Model 3 and Model Y models continue to buoy Tesla’s volume.

Rivian, known for its focus on electric trucks and SUVs, aligns perfectly with Tesla’s gaps in these segments. Tesla’s Cybertruck has faced delays and skepticism, making Rivian’s more traditionally designed R1T and R1S appealing alternatives that could be integrated into Tesla’s product lineup. Furthermore, Rivian’s robust approach to off-road capable EVs complements Tesla’s urban and performance-oriented vehicles, providing a broader appeal to a more diverse customer base.

Lucid Motors, on the other hand, brings a different set of strengths. Known for its luxury sedan, the Lucid Air, which boasts industry-leading battery efficiency and range, Lucid could elevate Tesla’s status in the premium sport performance segment. And from Auto Evolution’s drag race between the venerated Model S Plaid and the $249,000 1,249 horse power Lucid Sapphire:

There’s a new kid on the block, and it goes after the Model S Plaid with Lucid vengeance intentions. That’s right; the Lucid Sapphire is the new name to beat after it demolished the venerable Tesla champion as if the old apostle of electric motoring was running on solar power at midnight.

As of yet, Tesla has no answer for this pricing segment or straight-line performance.

However, it’s crucial to note that neither Rivian nor Lucid has demonstrated long-term profitability independently, a concern that haunts many new EV brands, reminiscent of Fisker’s impending financial collapse. By integrating Rivian and Lucid, Tesla could leverage their unique technologies and design philosophies to inspire exciting new models and innovations, potentially preventing a similar fate and ensuring a dynamic and profitable future in the rapidly evolving automotive landscape

The Rising Threat of BYD and the Global Competition

If you are unaware, Chinese automaker BYD has emerged as a formidable global adversary, briefly surpassing Tesla as the world’s top EV seller. Unlike Tesla, BYD has capitalized on massive domestic demand in China and aggressive pricing strategies without even tapping into the American market.

However, BYD is also not without its troubles. The company faces challenges overseas, with issues like quality control and internal discord stymieing its global aspirations. This presents a window of opportunity for Tesla, but only if it can innovate rapidly and expand domestically. Meanwhile, European automakers like BMW are not sitting idle. BMW’s EV sales have surged, bucking the trend of faltering demand that has plagued others, including Tesla. Consider this from Bloomberg:

BMW’s success is all the more impressive since it coincides with a broader slowdown in demand for EVs, particularly in Europe, where governments are reducing subsidies.

This surge is attributed to BMW’s extensive experience with battery technology and its early move to electrify its lineup. This not only underscores the intensifying competition in Europe but also highlights the necessity for Tesla to diversify and strengthen its own EV lineup.

Synergies and Scale

Tesla’s domestic market share has been stalling due to an aging model lineup and increased competition from new entrants and established automakers expanding into the EV space. A brand refresh, facilitated by launching new models or through potential acquisitions or mergers, could invigorate Tesla’s appeal and market position. Introducing diverse and innovative vehicles would attract a broader customer base, revitalize the brand and addressing concerns over innovation fatigue. This strategic expansion could resolve persistent concerns by signaling Tesla’s commitment to continuous evolution and leadership in the EV market.

The acquisitions of Rivian and Lucid would not only expand Tesla’s product portfolio but also bring significant operational synergies. Tesla could leverage Rivian’s manufacturing facilities and Lucid’s advanced battery technology to enhance its production capacities and battery efficiency. This would be crucial in maintaining Tesla’s edge in a market where technological superiority and production scale are increasingly important.

Furthermore, Tesla’s vast experience in software and autonomous driving technology could greatly enhance Rivian and Lucid vehicles, potentially increasing their value proposition and market penetration. Integrating these technologies could lead to the development of new, innovative features that would set their vehicles apart from competitors like BYD and the European brands.

Financial and Market Considerations

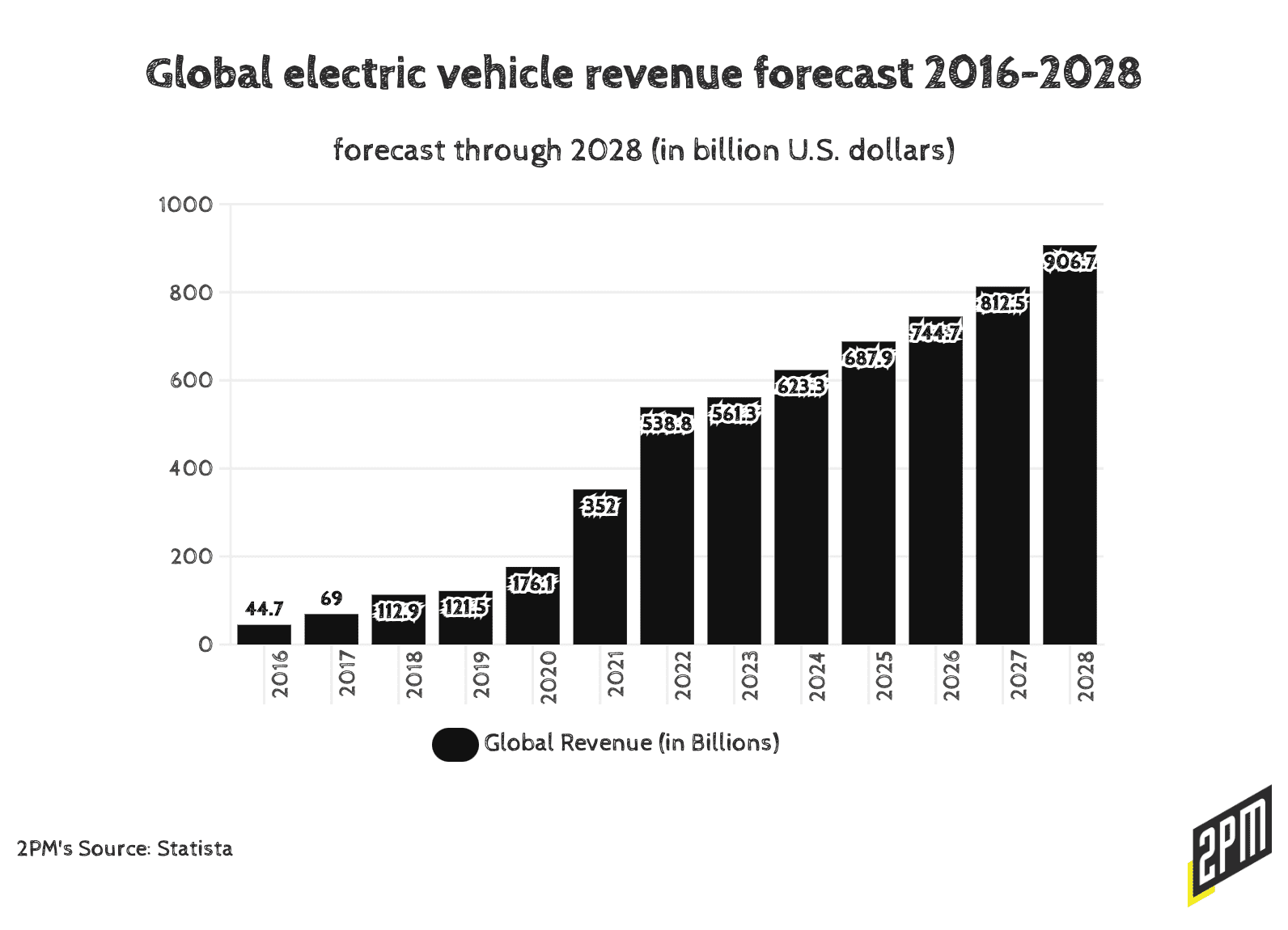

Global revenue for EVs is projected to reach a staggering $906 billion by 2028, illustrating a continued trajectory for the industry. For Tesla, maintaining its current leadership position will require not only sustaining its innovative edge but also succeeding in key markets such as North America and China. Achieving this is no small feat for any manufacturing company, particularly in a landscape crowded with aggressive competitors and rapidly evolving technologies.

To thrive, Tesla must transcend its current brand perception, which is tied to older models and past controversies. Here is Yahoo! Finance on the Q1 2024 Earnings:

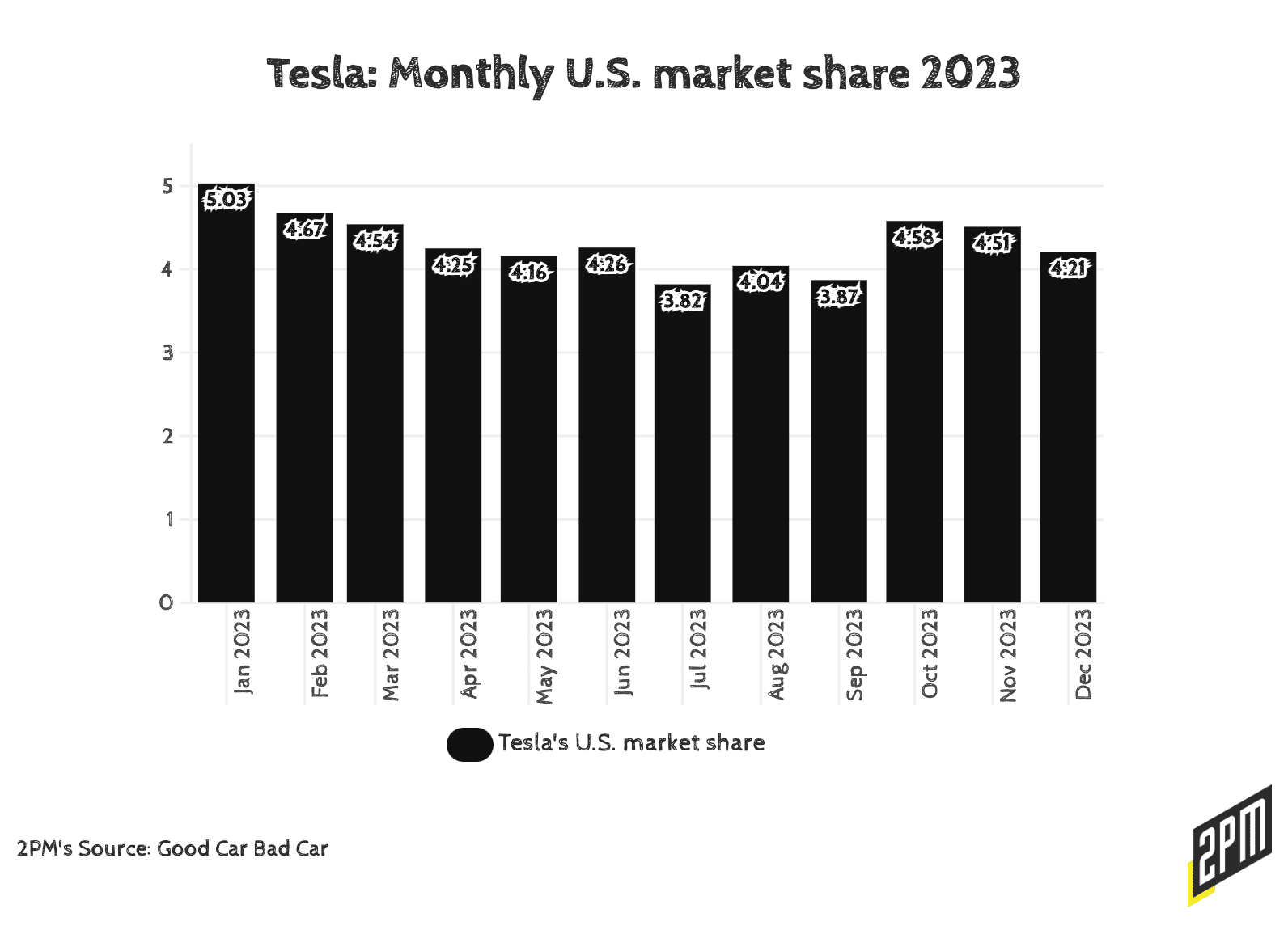

In Q1, Tesla reported 386,810 global deliveries, well below estimates of 449,080, and produced 433,371 vehicles, also below estimates of 452,976.

The difference of around 46,500 vehicles produced versus sold led to concerns of demand waning globally for Tesla vehicles, which in turn has led to round after round of price cuts. On Monday, Tesla cut prices for vehicles in the US and China, leading to weakness in the stock during the day.

By refreshing its brand and product lineup, incorporating new models, and leveraging cutting-edge luxury technologies, Tesla can enhance its market appeal and meet the rising consumer demand more effectively. To capitalize on the growing market potential, it is imperative for Tesla to evolve into a more dynamic, innovative, and globally dominant brand. It is no longer these things.

With Tesla’s stock experiencing volatility and its leadership facing legal challenges, Elon Musk and the management team need to reassure investors that the $25,000 Model 2 will take ultimate priority and that brand marketing and advertising spend will be devoted to the product’s appeal. This is in best interest of the company’s long-term growth.

Marketing and Advertising

As the EV market becomes more crowded and competitive, Tesla must look beyond the organic growth that it has long relied upon. While unlikely to give the idea much credence, Musk’s embattled $56 billion compensation package could and should be repurposed to acquire new design assets, technologies, and out right growth. This could potentially repay Musk several times over, over the long term. Acquiring Rivian and Lucid offers a pathway to enhanced product lines, advanced technology, and increased production capabilities, positioning Tesla to lead in the global EV arena against the likes of BYD and European manufacturers like BMW and Mercedes. These strategic moves could be crucial in securing Tesla’s market dominance for the next decade, aligning with its mission to accelerate the world’s transition to sustainable energy.

To sustain its market leadership and address pricing integrity challenges, Tesla will need to significantly reinvest in its brand marketing, advertising, media outreach, and influencer strategies. The recent layoffs, including the dissolution of Tesla’s newly formed “growth content” team, signal a retreat from a brief foray into traditional advertising initiatives approved by CEO Elon Musk. From Fortune on the matter:

The cuts signal a pullback from Tesla’s nascent advertising initiative. The automaker had long eschewed television, radio, print or online ads — and had built a formidable brand largely through word-of-mouth — before Musk said last year that Tesla would “try a little advertising and see how it goes.” [The recently laid off Alex] Ingram started building the growth team about four months ago.

As global EV sales growth decelerates and competition intensifies, Tesla cannot afford to rely solely on its past word-of-mouth or product-led marketing strategy. The company must adapt to the changing landscape by implementing a robust marketing strategy that leverages both digital and traditional media to reach broader audiences. This includes more effectively engaging with influencers (the Katie Perry effort was poor timing at best) and utilizing platforms like Meta, Instagram, and Snapchat more effectively, particularly in light of Musk’s hyper-dependence on X (which he owns).

****

Reinforcing Tesla’s brand through these channels may help mitigate downward market pressures and reinforce its pricing structure amidst growing competition. This strategy coupled with the speculation that he’d at least consider repurposing his compensation package as leverage to save Lucid and Rivian from similar turmoil (in their futures) would be entertaining at the very least. I am partial to this quote by Elon Musk in response to a SpaceX documentary filmmaker:

The most entertaining outcome is the most likely.

The “Tesla Bros” strategy would be entertaining, earned media generating, and potentially effective. If executed, it – along with the Model 2 strategy and proper marketing spend – could help return the car manufacturer and EV pioneer to the dominant future it once envisioned. If there is anyone out there who could succeed on all of these fronts – at once – it’s Elon Musk. History has proven that much.

By Web Smith