Golf is trying to have its own Formula 1 moment, thanks to Netflix and the natural drama that seems to be unfolding on and off the course. But unlike the carefully manicured Formula 1, professional golf is being pulled in two directions.

Consumers want to feel closer to the game, and they want the walls between the most exclusive country clubs and the most frequented public courses to teeter. But there are caveats here. Like many racing fans want access to the vaunted paddock club of F1 lore, they don’t want it to become any less exclusive. This is the trappings of aspiration.

A new generation and demographic of consumers are bringing a new energy to a stodgier sport. Brands and sponsors that were once the most buzzed about are losing their hold. New brands and technologies are emerging that introduce consumers to a new age of golf defined by joggers instead of slacks, Jordan brand golf shoes, and more African-Americans teeing off than ever before. It’s an interesting time to say the least.

The sport itself is democratizing with characters like Patrick “Tiger Hood” Barr, Jacques Slade, Roger Steele and companies like Eastside Golf and Fairgame leading in fashion and technology. Both Eastside and Fairgame boast African-American ownership and an easing of the tension between the traditions of old and the prospect of the new. So why doesn’t this cultural shift translate to more positive attention for LIV Golf, the professional league rivaling the PGA?

Here is my summary:

- We grew up with Michael Jordan and Kobe Bryant. Culture prefers stiff competition and cutthroat gamesmen. This is the brand of the PGA but not currently the LIV tour.

- Democratization does not mean “lacking class” or simplified, it means better access. The new fans of golf want to be included in the conversations of old, revising it where they see fit. They don’t want to have that conversation tossed out for something altogether new.

- History is as important as innovation. This is a generation that innovates on the past while paying it the reverence it deserves, from retro Jordan golf shoes to apparel styles that resemble fashion trends forgotten with the 90s and 00s.

If these things are true, it can begin to explain how LIV and its investors went wrong. To better understand the divide, it requires an understanding of the differences between the two leagues. For the golf junkie, most of this is self-evident but to the general public, there’s a lot to learn. The dueling broadcasts in February 2023 was the first time that the average consumer had the opportunity to compare the product for themselves.

The PGA Tour’s Honda Classic (February 23-26) was broadcast on the Golf Channel and NBC for the final two rounds. For the first time, LIV competed head on (February 24-26) and was broadcast on The CW, a network best known for Superman & Lois. According to LIV’s corporate site, the weekend was a successful one.

The league’s inaugural weekend of live coverage averaged a linear viewership of more than 537,000, surpassing the current season viewership average of the 105-year-old National Hockey League on ESPN and TNT (373,000), average viewership of the 2023 Australian Open Men’s Final on ESPN (439,000), and the average ABC and ESPN viewership of 2022 Major League Soccer (343,000), launched in 1996. All ratings are from US domestic audiences only.

However, the press release omitted the obvious. According to ESPN.com, The CW’s live broadcast drew an average of 289,000 viewers with a “0.18 household rating on Saturday and Sunday.” Golf.com made the comparison plain:

In comparison, the PGA Tour’s weekend broadcasts on NBC brought in just over 2 million viewers and averaged a 1.24 household rating — nearly seven-times as many viewers as LIV.

Critiques of the comparison suggest that it will take time for the LIV and CW partnership to take shape. It’s also the case that the Honda Classic was sandwiched between four top PGA events so the marketability of the Honda Classic was not what it could have been. Time will tell if the upstart LIV can find the television audience that The CW Network hopes it will deliver. The two products share very little in common.

The PGA Tour has a much longer history and more established reputation. The tour was founded in 1929, and it has been the premier professional golf circuit in the world for nearly a century. The tour has produced some of the greatest golfers of all time, including Jack Nicklaus, Tiger Woods, and Arnold Palmer. The PGA Tour is known for its tradition and prestige, and it is viewed by many as the pinnacle of professional golf.

LIV Golf, on the other hand, while having made some high-profile signings, lacks the prestige of the PGA Tour. LIV has taken its marketing cues from men who love drinking a six pack on the course with their friends. There are four-man teams, silly team names, uniforms, and music blaring on the course. The allure of golf’s second most important attribute (behind talent) is all but missing: prestige and affinity. Columbus Dispatch columnist Rob Oller:

Not many of LIV’s players are particularly likable. (Sergio) Garcia, (Patrick) Reed and (Bryson) DeChambeau belong on an injury lawyer billboard. The majority of LIV fields consist of has-beens and never-were’s. But my distaste for LIV goes beyond that … Results matter. LIV is exhibition golf, plain and simple. So is the virtual golf league being put together by Tiger Woods and Rory McIlroy… Anything that smells like TopGolf meets Putt-Putt can’t hold my interest.

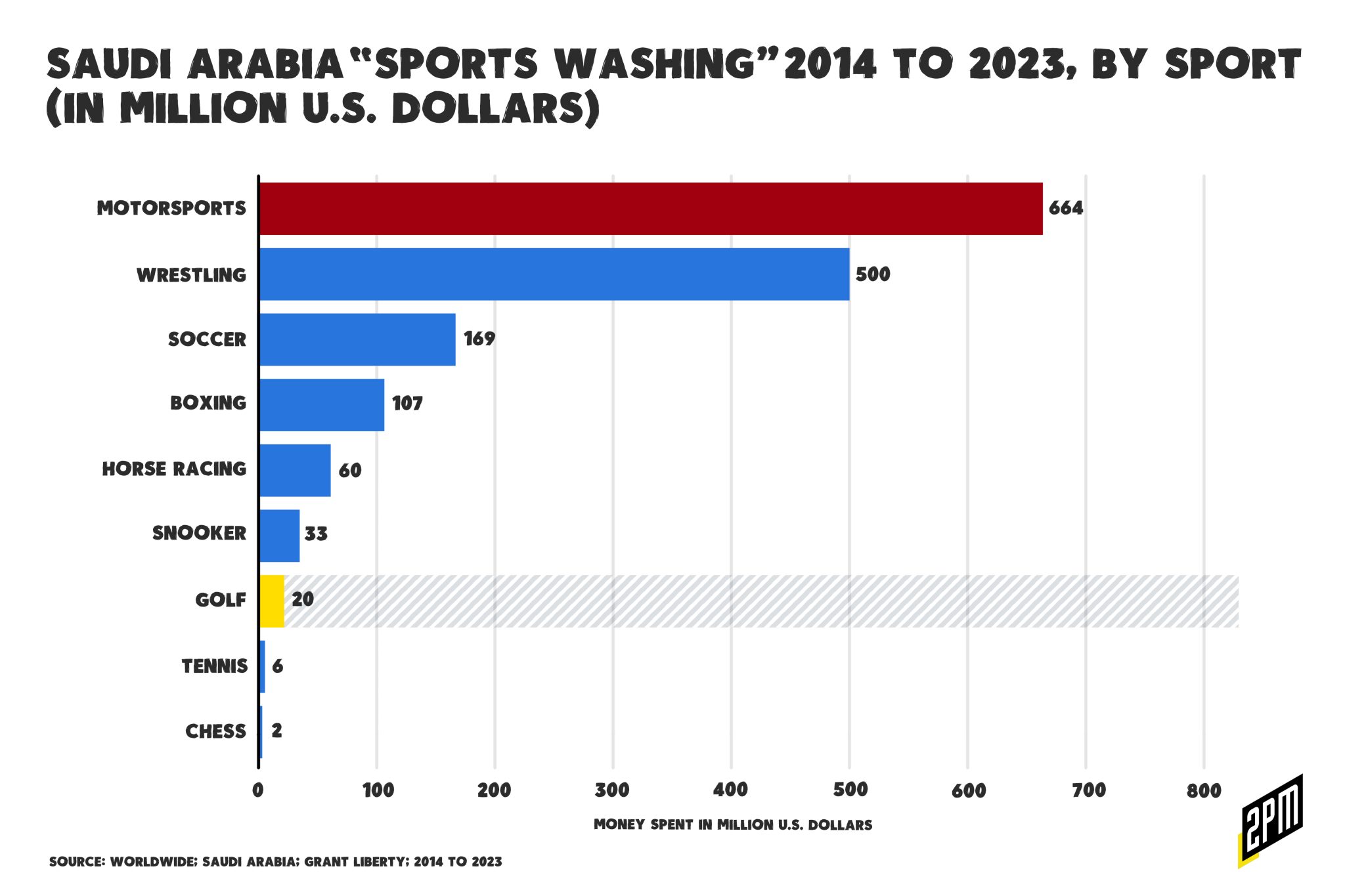

It remains to be seen if LIV Golf will be able to establish itself as a legitimate competitor to the PGA Tour, by either measure, in the long-term. The third obstacle that LIV faces is unique to the character of the sport. Golf, long a pursuit of wealthy white men, is democratizing. But this dispersion in interest isn’t far-reaching enough for LIV’s detractors to dog whistle about the source of its funding: The Saudi Public Investment Fund (PIF).

The irony of my comparison between F1 and professional golf is that Saudi Arabia has spent far more money on the FIA’s premiere racing circuit than on LIV golf. In fact, several sports saw more investment than LIV. It’s also important to note that LIV Golf features many golfers who are past their primes: Phil Mickelson, Sergio Garcia, Bubba Watson, Ian Poulter, and even the oft-injured Brooks Koepka are on their way out. There are a few exceptions, of course: Dustin Johnson and Cam Smith were at the tops of their games before leaving for guaranteed money and lighter workload. The PGA has deepened its position that it’s performance-based and financially upright, in contrast to its new competitor.

The “Saudi Money” connotation only works in golf precisely because the pecking order has remained monolithic for so long (until a multi-ethnic Stanford golfer roared onto the scene). This same guilt-by-association approach fails to garner much attention elsewhere – especially the investments into American markets.

Saudi Arabia’s sovereign wealth fund invested more than $7 billion to build new positions in US stocks including Amazon.com Inc., Alphabet Inc., BlackRock Inc. and JPMorgan Chase & Co. as markets were battered by recession fears.

The difference between these far greater investments into beloved American corporations and the advent of LIV is that golf will always rely upon the country club culture of excluding outsiders. The LIV golfers who have signed on are likely too aloof to understand their own relationship to the average consumer. Watch the Netflix show and you will see aging, losing professionals flying private, visiting their multiple homes, and showing up on America’s finest golf courses. Meanwhile, we are tasked with taking Bubba Watson comments like these seriously:

My 10-year-old son was sitting in the bed with me, and we were watching golf on the TV, and he knew the Aces – everybody knows the Aces, they keep winning. He knew the Aces, he knew the Stingers.

The PGA’s great allure, the same that many consumers share for F1, is that a middle-class golfer from Pensacola can work his way through junior college, on to the University of Georgia, to win the Masters twice. That comeuppance is what fuels professional golf’s democratization. Children from similar backgrounds want the same story as Bubba’s. LIV doesn’t quite deliver on that prestige. It attempts to make some of the most well-connected men on earth appear like the every-man. The PGA tour reminds you that it requires performance to enter the conversation the way that Watson did in 2012 at Augusta National.

What makes this comeuppance possible is the PGA Tour’s wide range of events, including major championships like the Masters, the U.S. Open, and the PGA Championship, as well as numerous other high-profile tournaments throughout the year. These events still attract many of the best golfers, sponsors, and media attention in the world. These platforms, the tour stops, provide fans with an opportunity to see the game’s biggest stars compete against each other. As of now, it is more difficult for LIV players to compete in those high-profile majors.

The PGA Tour also benefits from a more stable and established infrastructure. The tour has a well-established system for player development and progression, with multiple tiers of tours and qualifying events. This allows up-and-coming golfers to work their way up the ranks and earn their way onto the PGA Tour.

LIV Golf, on the other hand, has yet to establish a clear pathway for players to earn their way onto its tour. It is unclear how the organization will handle player development, promotion, or merchandising of its talent. This lack of clarity could deter some up-and-coming golfers from pursuing a career in the LIV Golf organization.

The tour has a large and passionate following of fans who are invested in the success of their favorite golfers and their stories. The PGA accomplishes this with its storytelling. It also has a robust media presence, with coverage on major sports networks and an extensive online and social media strategy. While LIV Golf has stated that it plans to leverage technology and social media to engage with fans, it remains to be seen if it will be able to replicate the PGA Tour’s success in this regard.

As golf trudges through its Formula 1 moment, the PGA Tour sits in an advantaged position. The class and prestige of the PGA tour resembles that of F1. Behind the scenes, you know that the men behind the circuits 20 cars are normal people. But as soon as the camera shines on them, there is a pomp and circumstance about them. As if they understand that the appeal is not speed alone. It’s also that a poor, mixed-race Brit could one day become a knight. If America had knights, professional golf would be one of its paths to the extraordinary.

In fact, we do have knightly figures in sport. In America, we know them when we see them. We strive to become them and it fuels our passion for the sports that they play: the PGA Tour is one of those paths. It might be its foremost; and it’s the marketing advantage over LIV that money cannot buy

This is what’s fueling golf’s democratization and a new era of fandom that will nod to the old without outright dismissing it. Despite defections, The PGA Tour – and the many new media projects, tech startups, and Instagram personalities that support it – maintain pole position over the Saudi-backed rival. Golf will be different, just not as different as LIV Golf hoped.

By Web Smith | Edited by Hilary Milnes with art by Alex Remy and Christina Williams

But while deficit is a visible marker of retail imbalance, there are other key measures that can indicate dependency on Chinese products. Two short months after the report was written on Amazon’s acquisition of Roomba, this report on

But while deficit is a visible marker of retail imbalance, there are other key measures that can indicate dependency on Chinese products. Two short months after the report was written on Amazon’s acquisition of Roomba, this report on