The transformative potential of Name, Image, and Likeness (NIL) legislation has catalyzed a significant shift, particularly for sports outside of men’s basketball and football. This evolution presents an unparalleled opportunity for brands to forge partnerships that are not only financially lucrative but also rich in cultural and social capital.

This, along with a host of other positive indicators, suggests a renaissance for the marketability of sports and the athletes playing them – especially the athletes who are often relegated to third or fourth place in the fandom sweepstakes.

The emergence of athletes as pitchwomen and pitchmen has heralded a new era in sports marketing, one that promises an exciting time to be a fan or the athlete.

****

Outside of the highest tiers of football or men’s basketball, the most valuable partnerships will be found across the aisle. 2023 emerged as a landmark year for women in sports, a tipping point underscored by record-shattering events such as the NCAA women’s basketball tournament and the Women’s World Cup. 2024 is shaping up to be a continuation, according to Axios among many others:

San Diego Wave FC lost 2-1 Saturday night but drew 32,066 fans to Snapdragon Stadium, breaking its own NWSL home opener attendance record set last season.

And Front Office Sports recently dished on the marketability of Caitlin Clark versus two highly marketable male athletes in Bronny James and Caleb Williams, the future NFL No. 1 draft pick:

[Caitlin] Clark’s situation is unique: She’s entering the professional ranks after years of being marketed as a professional. Ryan Hoge, PSA’s president, says Clark has outpaced USC’s Bronny James, Heisman winner Caleb Williams, and other college stars in terms of PSA submissions.

Deloitte’s forecast for 2024, projecting revenues for women’s elite sports to surpass $1 billion — a staggering 300% increase from 2021 — underscores the burgeoning commercial viability of women’s sports, according to CNBC.

This meteoric rise in the financial stature of women’s sports can be attributed to a constellation of factors, including the magnetic appeal of young phenoms, alongside strategic investments in professional leagues and enhanced sponsorship opportunities. These elements collectively fueled the commercial dynamism and audience engagement characteristic of the contemporary NCAA sports landscape.

****

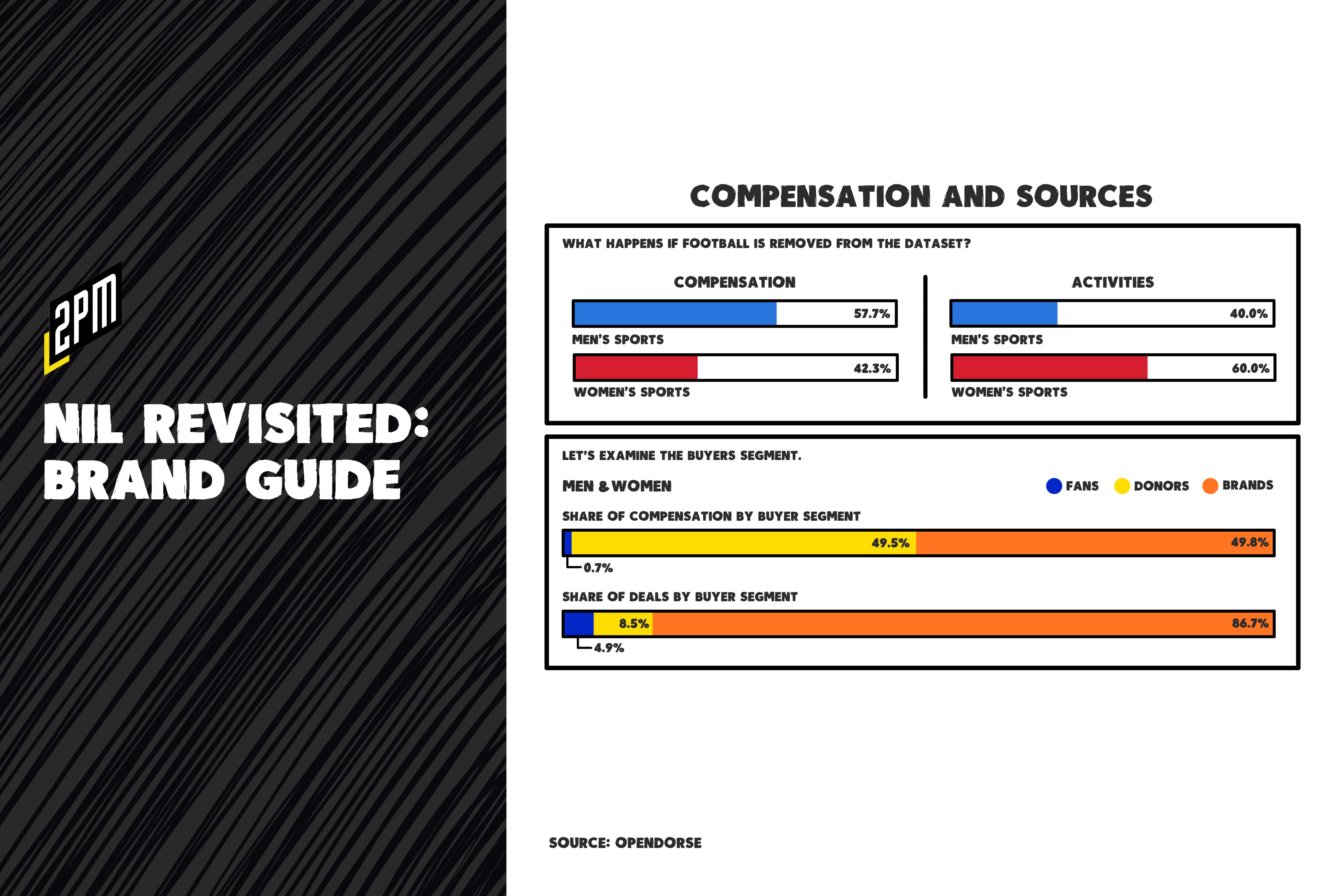

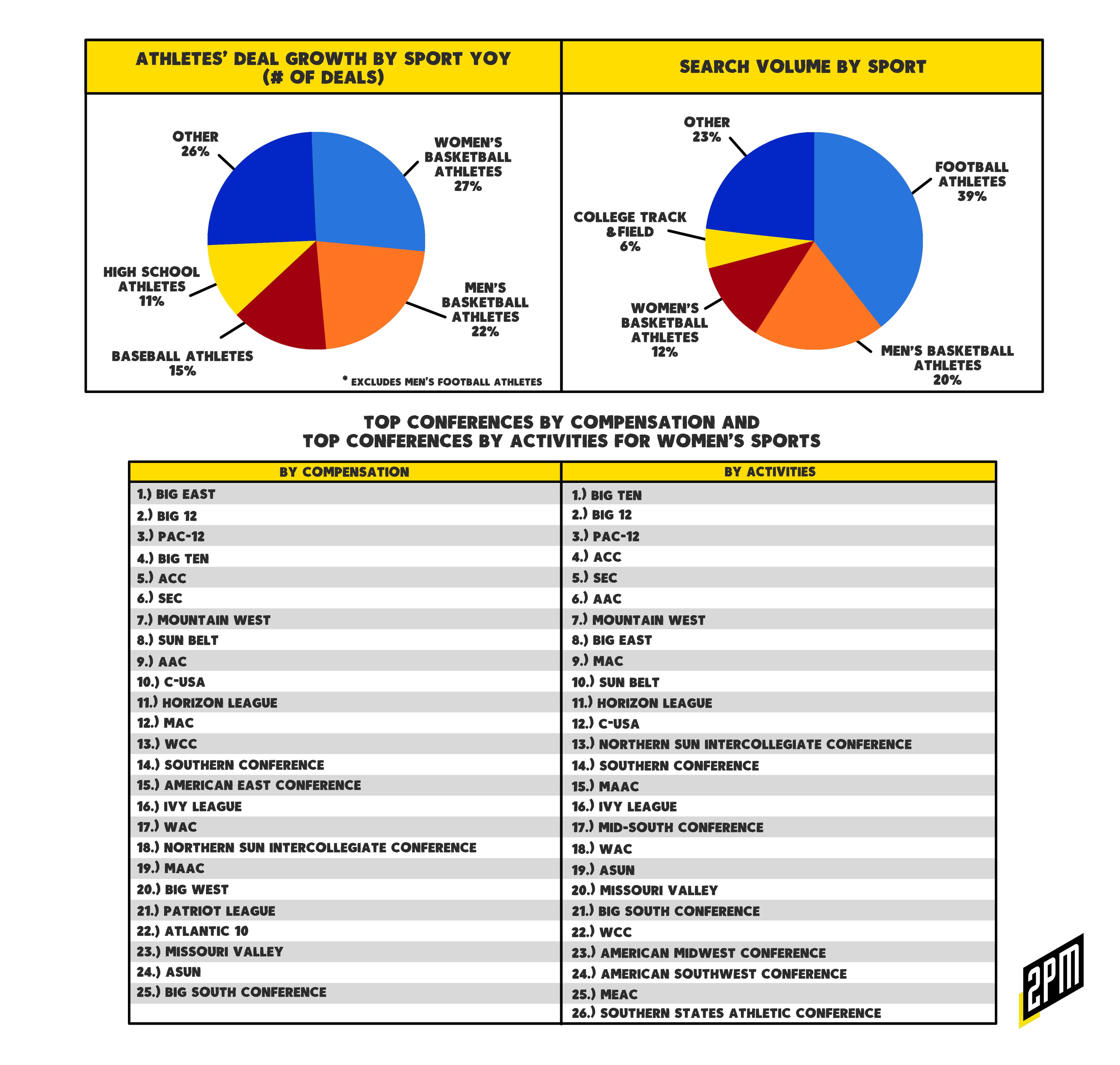

The implementation of NIL legislation in 2021 marked a watershed moment, enabling college athletes to monetize their personal brand through endorsements, thereby becoming pivotal influencers for brands targeting the lucrative Gen Z demographic. It also opened the door to athletes accepting payments from collectives of alumni and other interested parties. Outside of football, women’s basketball athletes have outpaced men’s basketball athletes in deal growth. Men’s basketball and football still maintain the highest interest by search volume.

This now three-year-old pivot has engendered a fertile ground for brand partnerships, significantly impacting the marketing strategies of companies across various sectors, particularly those in the athletic and athleisure domains.

Athletic fashion brand Vuori exemplifies this shift through its partnership with LSU All-American gymnast Livvy Dunne, who has become the brand’s first NIL athlete collaborator. Vuori’s Chief Marketing Officer, Karen Riley-Grant, emphasizes the alignment between Dunne’s “athletic expertise, determination, and positivity” and the brand’s core values, highlighting the success and authentic resonance of this partnership according to Forbes.

As Vuori’s partnership with Livvy Dunne has grown since 2021, so has her ability to collaborate with the brand.

The proliferation of NIL deals, as evidenced by Vuori’s partnership with over 400 NIL athletes, underscores the burgeoning opportunity for brands to engage with college athletes’ highly engaged fan followings. These partnerships not only offer brands a lower-cost avenue to penetrate the sports marketing realm but also enable them to leverage the personal and regional appeal of athletes, thus enhancing their marketing efficacy and reach.

Expanding Marketing Opportunities

The NIL landscape has democratized access to the collegiate sports marketing domain, allowing both established and non-traditional brands to engage with a previously inaccessible audience segment. As noted by Dan Lobring of Stretch PR, NIL provides an opportunity for individual athletes to break through the clutter, offering brands a novel pathway to capture the attention of the vast and engaged audience of March Madness and beyond. He recently spoke with Modern Retail:

It’s this unique moment where there’s obviously a ton of interest, which is great, but it also can be harder for brands to break through.

In April 2023’s Ted Lasso and Major League Soccer, I explained: “Women’s basketball figured that out and, in one season, leapfrogged the MLS and others in viewership thanks to the heroics and charisma of Caitlin Clark and Angel Reese.” Indeed, the Caitlin Clark effect and the record-breaking attendance at women’s sporting events signify not just the rising star of women’s sports but also the deepening well of marketing opportunities for brands. These events reflect an engaged and expanding audience base, ripe for brands to tap into through strategic partnerships. The remarkable viewership of the 2023 NCAA Division 1 championship game, attracting nearly 10 million viewers and NCAA women’s volleyball’s championship peaked at 2.1 million viewers according to the NCAA. To put this into perspective, the 2023 NBA finals was watched by just 1.64 million more than the NCAA’s women’s basketball title game. The NBA’s finals viewership is down 45% from its 20 year ratings highs.

****

The burgeoning domain of women’s sports, catalyzed by the advent of NIL legislation, represents a frontier of untapped potential for brands. The remarkable growth and increasing commercial viability of women’s sports have opened the doors to a plethora of marketing opportunities, enabling brands to introduce themselves to highly engaged and diverse audiences through authentic, values-aligned partnerships.

As we stand on the precipice of this new dawn in sports marketing, it is clear that the trajectory of women’s sports is not just ascending. The abilities, determination, and excellence that these athletes represent resonate profoundly with a broad spectrum of consumers, underscoring the invaluable role of NIL deals in shaping the future of sports marketing. Frankly, while college sports will always be about the money, women’s sports presents a better balance between the two realities: NCAA sports had a particular appeal built atop of the notion of the student-athlete and the fact that many of the best of those athletes are now compensated handsomely.

In the words of Karen Riley-Grant, “It’s about finding the right influencer partners…who embody the core values of [the] brand.” This ethos, captured by Forbes, encapsulates the essence of the opportunity at hand: to forge partnerships that are not merely transactions but are deeply embedded in shared values and mutual aspirations. You’re more likely to find that on the women’s side than on the men’s, where it has become nearly mercenarial for short-term gain. As brands and athletes learn this and navigate this new landscape, the potential for impactful, lasting relationships that transcend the college game is high.