Over nearly 20 years, the DTC brand landscape has seen an explosion and relative decline. These brands, known for their innovative marketing strategies and unique product offerings, captured the hearts of consumers, media groups, and investors alike. However, beneath the glossy surface of perfect branding, careful narratives, and paid marketing, the financial reality often trailed brand equity for the companies and their founders. Parade, a once-promising DTC intimates startup, is a poignant example of how even seemingly thriving brands can find themselves on the precipice of insolvency.

The superpower of the DTC industry has never been branding (that can be easily duplicated) or platform (Shopify and BigCommerce democratized eCommerce) or even the manufacturing of a novel product. The superpower has been the ability to identify arbitrage opportunity and capitalize on it. The superpower of DTC is getting there first. In this case, there is a geographical location.

****

In Steady Brand vs. Cool Brand, I wrote about two brands who both lost sight of the hidden advantages of being an agile DTC brand:

But the constraints faced by the brand, including the product’s increasingly commoditized nature and shifting preferences in raw material usage, may limit its exit optionality.

Then, I published on a brand who seemed to exercise its understanding of its super power at every stage of its growth. Solo Brands began as Solo Stove, a quiet but profitable manufacturer of portable firepits. Few paid attention to the brand outside of its loyal customer base. The founders were near-anonymous; this was a byproduct of the brand being founded outside of the New York / Los Angeles / Miami brand bubble. I explained in the Solo Brands Novel Strategy:

A once-obscure brand just outside of Dallas, Texas evolved into a generational model for how business is done, brands are built, and liquidity is achieved for stakeholders. Founded in 2010 and trading today at $DTC with a market cap that hovers around $500 million, Solo Brands has an exceptional story.

While the two stories paint different pictures (stuck in pre-exit vs. post-exit), this essay is about what brands can do to make it easier on themselves by pursuing high value, lower risk arbitrage opportunities.

Arbitrage in this context refers to the strategic exploitation of discrepancies or gaps in the market, whether they pertain to technology, product branding techniques, or new marketing channels.

****

Part One: The DTC Brand And The Unspoken Crisis

The purchase of Parade by lingerie manufacturer Ariela & Associates International in August was initially perceived as a standard acquisition, in line with the trend of larger companies snapping up promising digitally native brands. Yet, what unfolded was far from ordinary. Parade, once valued at around $200 million by investors, ended up in a last-ditch sale, resembling a bankruptcy liquidation process. What’s more, this sale obliterated the investments of all its shareholders, painting a grim picture of the brand’s financial health.

Behind the scenes, internal financial data revealed that Parade was teetering on the edge of insolvency. By the end of 2022, the company’s cash reserves had dwindled to $7.3 million, which was inadequate to sustain the brand’s operations, given its projected cash burn rate for 2023. The story of Parade serves as a stark reminder of the intense financial pressures that many DTC startups currently face, particularly those that pursue rapid growth through heavy investments in paid marketing:

Although the company cut its paid advertising costs to around 40% of net revenue in 2022, it still burned more than $33 million in cash last year. As of this spring, the company had forecast its cash balance would dip below zero by August of this year, according to the documents. (The Information)

The company’s success was further buoyed by high-profile collaborations with industry giants like Coca-Cola and Swarovski as well as a number of partnerships with celebrities and influencers. Parade’s net revenue exhibited impressive growth, more than doubling in 2021 and increasing by 50% to nearly $32 million in 2022. However, this growth came at a steep cost. Parade committed substantial resources to paid marketing, with advertising expenses devouring more than 60% of its net revenue in 2021. The brand expended significant sums to acquire new customers, with the cost of acquiring each new buyer roughly equivalent to the average order value (AOV).

The result was the drain on Parade’s cash reserves. Despite efforts to rein in advertising expenses in 2022, the company still hemorrhaged. The reported figures, in comparison to other DTC companies, were unsustainable and served as a warning of impending financial catastrophe.

While Parade scrambled to secure a buyer, it ultimately fell into the arms of Ariela & Associates International. It’s been noted that investors made nothing. This financial wipeout was largely attributed to Parade’s mounting debt, which stood at over $19 million in bank loans, convertible notes, and credit card debt as of May. Before the distress sale, Parade had raised a significant $56 million from investors, including Maveron, Lerer Hippeau, and Greycroft Partners.

The story of Parade highlights the vulnerability that many DTC brands currently face. While the DTC model offers unique advantages in terms of brand control and customer engagement, it also comes with significant financial risks. Parade’s rapid growth, fueled by aggressive marketing spending, ultimately led to its financial downfall. There are broader implications of Parade’s predicament and its connection to a larger movement toward insolvency in the DTC industry. Parade’s outcome is far from unique in this respect. In fact, the distress sale of DTC brands will seem more common than the conventional exit over the next 12-24 months.

Part Two: A Fix For The Unspoken Crisis

In the ever-evolving landscape, the ability to identify and capitalize on arbitrage opportunities has been a defining characteristic of success. Arbitrage in this context refers to the strategic exploitation of discrepancies or gaps in the market, whether they pertain to technology, product branding techniques, or new marketing channels. These opportunities enable young brands to gain a competitive edge and secure a foothold in the highly competitive world of retail. It’s a marketplace whose difficulties are often underestimated.

The notion of arbitrage can be observed in the fashion industry, particularly in the context of a number of American brands over the years that have understood Japan’s unique role as a trendsetting hub.

Japan, long renowned as a fashion-forward nation, has been a mecca for avant-garde fashion since the 1980s. Japan’s fascination with American fashion has roots that extend back over 70 years. In the mid-20th century, it served as an unofficial second home for mid-century American collegiate cool, a phenomenon exemplified by the popularity of “Take Ivy” by Teruyoshi Hayashida, a photo book capturing the life and style of Ivy League students in the 1960s. This book became a cultural sensation in Japan, reflecting the nation’s penchant for embracing and adapting global fashion trends.

In contemporary times, Japan continues to be the go-to destination for those seeking the best denim, the hottest streetwear, meticulously handcrafted eyewear, and the most forward-thinking fashion labels. But success is not limited to the most forward-thinking in fashion. Now-retired Pendleton President Mort Bishop was quoted in 2015:

We’ve been in Japan for thirty-five years, and it is currently our best foreign market. There is so much interest among the fashion community in Japan for Pendleton. And it’s interesting that in the last few years we’ve had customers in Europe and the US ask what we’re doing in Japan.

The country has nurtured a fashion ecosystem that values innovation, craftsmanship, and individuality, making it a source of inspiration for designers and fashion enthusiasts worldwide. Brands that identify and leverage the unique arbitrage opportunities presented by the Japanese market often find themselves at the forefront of global fashion trends.

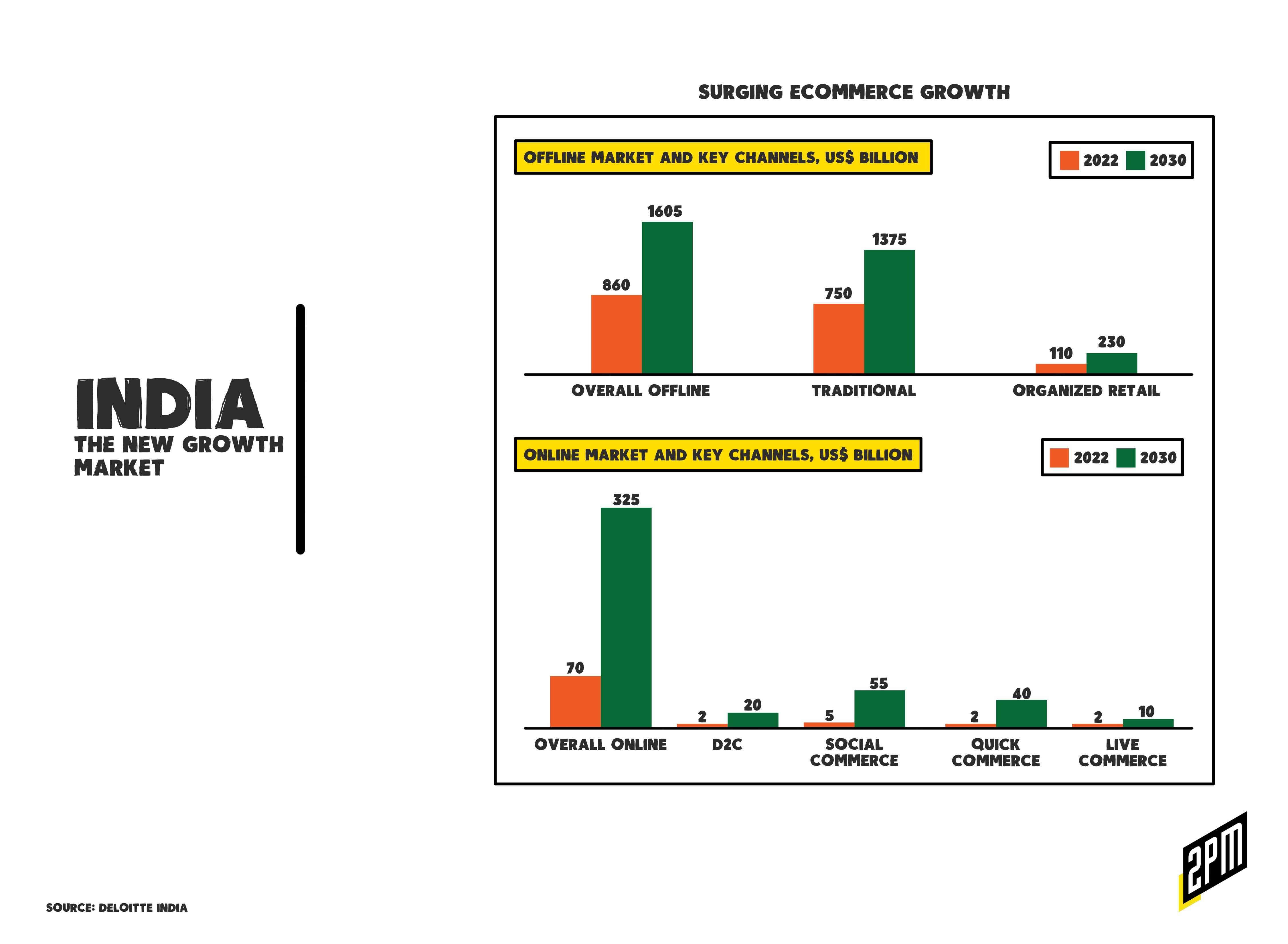

The New Growth Market. Now shift focus to India, a country of 1.425 billion and a middle class that ranges from 66 million to 432 million citizens depending on how you measure it. With a rich and diverse economic history, we witness a parallel narrative of arbitrage opportunities, this time in the realm of eCommerce. India’s recent economic history has been marked by rapid growth and transformation. Over the past few decades, the country has experienced a significant shift towards a more open and market-driven economy, unleashing a wave of entrepreneurial spirit and innovation.

The eCommerce sector in India, in particular, has seen explosive growth. Walmart’s $16 billion acquisition of majority ownership in Indian online retailer Flipkart in 2018 initially raised questions about the acquisition’s value. Critics wondered whether Walmart had overpaid for the platform. However, as time has passed, it has become evident that Walmart made a prescient move. The acquisition allowed Walmart to gain a strong foothold in India, positioning itself as a formidable competitor to Amazon in the Indian eCommerce landscape.

This strategic move has been vindicated by the rapid expansion of the Indian eCommerce market. According to projections cited by the Financial Times, eCommerce sales in India are expected to reach an impressive $135 billion by 2025, nearly tripling the amount recorded in 2020. This explosive growth presents a significant arbitrage opportunity for retailers and brands operating in the Indian market. Statista has India leading such countries as Brazil, Argentina, Turkey, and Mexico in projected CAGR (14.11%) between 2023-2027, versus the United States projected CAGR of 11.22% and a global average of 11.16%. There are additional positive markers of potential arbitrage. The DTC market is due to grow to $20 billion in 2030, up from $2 billion in 2022. In total, the eCommerce market will surpass $325 billion in annual volume, up from $70 billion in 2022.

While both Walmart and Amazon initially dominated the Indian eCommerce scene, they have faced fierce competition from homegrown conglomerates like Reliance Industries and the Tata Group. In 2021, Flipkart held a market share of 48%, surpassing Amazon’s 26%. Flipkart achieved $23 billion in gross sales in India during the same year, outpacing Amazon’s revenue, which ranged between $18 billion to $20 billion. This shift reflects the dynamic nature of India’s eCommerce landscape and the potential for domestic players to capture a substantial share of the market.

According to a recent study commissioned by Amazon India and conducted by Nielsen Media, consumers across India are enthusiastic about shopping online during this festive season. Amazon.in emerged as the most trusted and preferred online shopping destination, with 81 percent of consumers intending to shop online during this festive period. (Indian Retailer)

And Walmart’s success in India, as evidenced by its growing market share through Flipkart, underscores the enormous potential. It also aligns with the broader trend of eCommerce growth, with Walmart’s overall eCommerce sales increasing by 27%. The expansion of Walmart’s online marketplace in the US, accompanied by a diverse assortment of products and faster delivery options, has contributed to its success. Additionally, Flipkart’s expansion efforts are reaching Tier 2 and Tier 3 cities, tapping into previously underserved markets. In a section called “The Consumer Boom” of a recent Harvard Business Review on the topic of the booming Indian economy, it states:

Real wages are expected to grow at 4.6%, whereas disposable income will continue to grow in excess of 15%. Industries that are mature in the West are fast-growing in India: Private health insurance, for example, has almost tripled between 2015 and 2021, while consumer durables were expected to grow between 15% and 18% this year.

The concept of arbitrage has been a driving force behind success in both the fashion industry’s fascination with Japan’s stamp of approval, the early growth of the DTC industry (thanks to Meta’s paid marketing role and Google’s ease of use), and now India. The eCommerce boom in India underscores the importance of identifying and seizing unique opportunities in evolving markets.

Am I saying that a company like Parade could have saved millions by partnering with V-Mart’s sizable eCommerce presence and its 423 stores in 227 Indian cities? No. It takes the right brand, in the right category, with the right message to resonate in differing cultures. That being said, there will be examples of American brands that identify newer, more cost-effective growth opportunities in an emerging market. India is the most important of emerging markets.

Brands and retailers that are well positioned to navigate and leverage the Indian market’s growth potential are poised to benefit from this new arbitrage opportunity. As the world of retail continues to evolve, the ability to adapt and capitalize on emerging trends and markets will remain a key determinant of success for American DTC brands and corporate eCommerce giants alike.

By Web Smith | Edited by Hilary Milnes with art by Alex Remy and Christina Williams