This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.

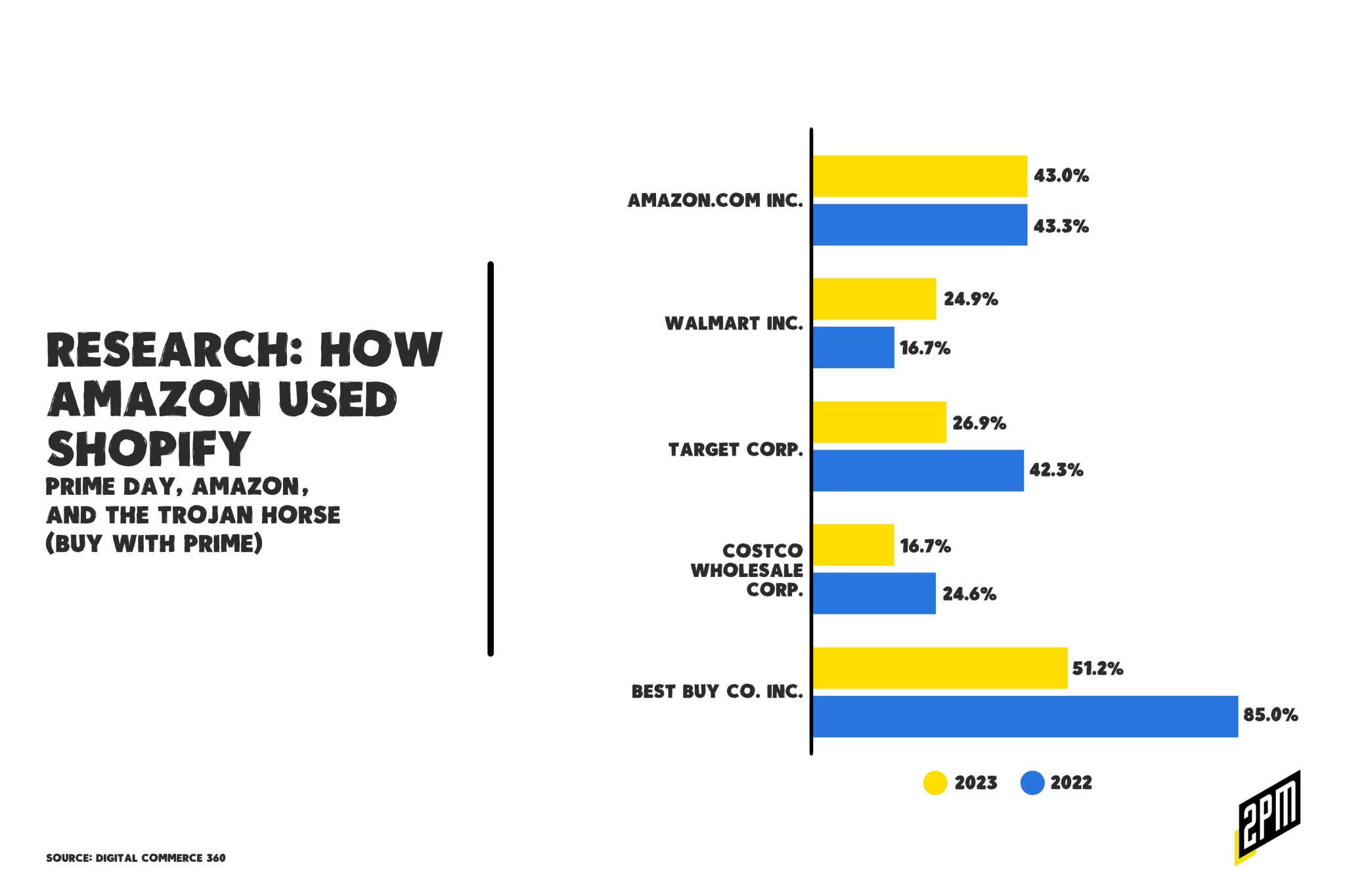

Member Research: How Amazon Used Shopify

This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.

Memo: Where Grocery Is Going (2053)

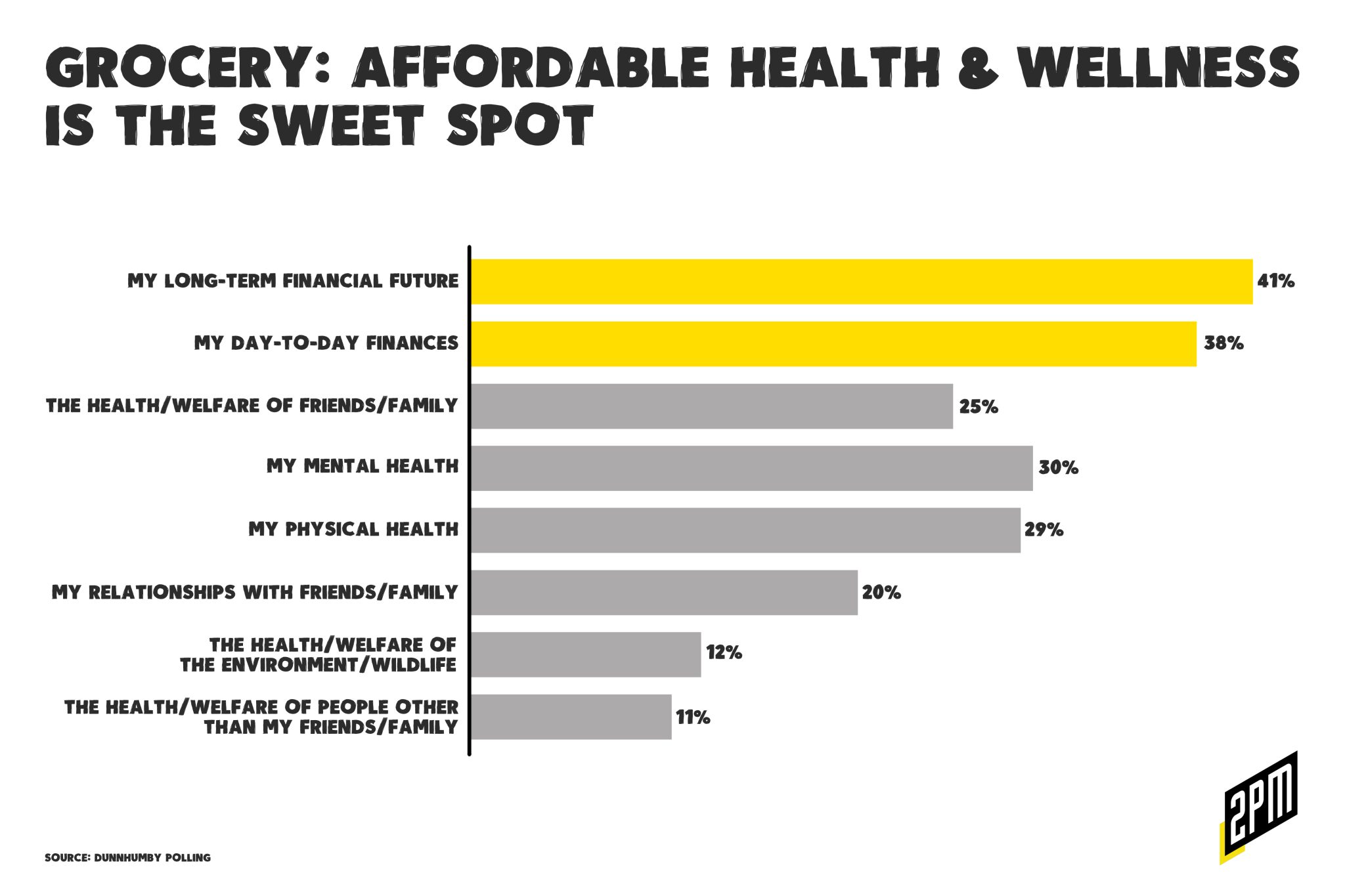

The future of the grocery industry is at a crossroads. Fiscal conservatism, technological advances, labor shortages, and shifting consumer preferences will dramatically shape the grocery landscape over the next 30 years. This essay examines these influences and proposes a strategic roadmap for the industry. According to recent data by global data science company Dunnhumby, there’s been a notable shift that will influence the rest of this report. For the last decade, speed of delivery and overall convenience were at the center of many buying decisions. Today, pricing and promotions may be eclipsing the perks of the eCommerce age. From the extensive Dunnhumby report:

2022 was all about finding the right products at the right prices and less about saving time. “Price, Promotions, and Rewards” has always been the most important need in our model, and it likely has been the most important customer need for much of the past 100+ years. The story of who has won and lost is also a story of the consumer’s insatiable appetite for a better deal.

The grocery industry, like any other, is not immune to the tides of change. I actually believe that it’s a leading indicator for what other industries may encounter. From economic concerns and the impact of generational behaviors to technological advancements, the industry is facing a multifaceted wave of transformation. Retail Dive’s recent publication of Dunnhumby’s report, “Grocery 2053: A Data-Driven Gaze into The Future,” provides insightful data, unraveling the complex layers that will impact grocery consumption over the next three decades. By analyzing these influences, we can forecast the shape of the grocery industry over the next 30 years. The Retail Dive summary provided great insights like these:

Harris Teeter, Wegmans, Publix and Sprouts Farmers Market are among the retailers whose market share is most vulnerable to fiscal conservatism over the next 30 years, according to Dunnhumby. Overall, Amazon, H-E-B, Costco, Sam’s Club and Walmart are best positioned to take advantage of the trend between now and 2053, when Dunnhumby expects the U.S. grocery retail industry to hit $1.9 trillion in sales, more than twice its size today.

At the heart of the industry’s evolution lies the pulse of fiscal conservatism, whose reemergence is driven by consumers’ worries about their economic future. Dunnhumby’s extensive survey of over 70,000 responses shows that price remains a decisive factor in grocery purchases, regardless of income. Generations Y and Z, more deeply impacted by the Great Recession and Covid-19 pandemic, express heightened concern over financial matters. While health and sustainability compete with cost as primary stressors for higher-income shoppers, cost is the primary obstacle for 60% of consumers seeking healthier food options.

This fiscal conservatism, expected to continue until 2053, signals a market shift toward value-oriented retailers. From Dunnhumby’s executive summary:

Between now and 2053, we see retailers doing much more: offering a grocery-helper budgeting AI, becoming their Customer’s trusted financial partner, and launching their very own private-brand-only, money-saving format of the future.

Amazon, H-E-B, Costco, Sam’s Club, and Walmart are poised to benefit from this trend, while the market share of Harris Teeter, Wegmans, Trader Joe’s, Publix, Sprouts Farmers Market, and other more premium stores might face challenges. This doesn’t spell doom for premium and specialty grocers, but it does necessitate strategic store locations, product differentiation, and customer experience enhancement to thrive.

Technological transformations will significantly impact how we manufacture and deliver products. I believe that it’s at times farfetched, but it’s important to recognize nonetheless. Dunnhumby’s Go-To-Consumer strategy suggests a potential revolution brought about by 3D food printing, synthetic biology, gene editing, and bioengineering. These technologies promise more sustainable and efficient value chains, valued at $72 billion. Drone deliveries, underpinned by a mobility tech market valued at $236 billion, could become the norm, eliminating the risk of disturbances like merchandise being stuck at ports.

The report also cited the promise of advanced connectivity, quantum computing, AI, machine learning, and no-code next-gen software development – collectively valued at $336 billion – powering the next phase of consumer insights. Retailers who plan to integrate these technologies into their vertical chains and customer experience strategies can tap into profound insights and emerge on top.

The digital revolution, driven by the rising importance of data privacy and the reduction of logistical waste, signifies a new frontier for customer engagement. Companies are expected to establish a presence in Web3, a space valued at $110 billion, reflecting the shift towards a more decentralized and user-empowered digital world. And generative AI, which we covered extensively here, opens opportunities for grocery retailers to actively participate in AI’s development, vetting, and regulation for AI-assisted grocery and commerce.

Virtual reality, and the advent of the metaverse, will redefine consumer engagement. With companies like Apple betting on mixed-reality headsets, it is wise for grocers to stay abreast of these technological innovations, even if they are in their early stages. I thought that this insight was pretty valuable:

Although the metaverse has diminished in importance in the new-tech hype cycle, its steady evolution over the last two decades suggests that it may reappear in a future horizon. The question is, just how soon will we get to that future? Apple’s recent announcement of a state-of-the-art mixed-reality headset is a strong indication that the technology world is still betting on the metaverse. Our position is that the metaverse is here, but still in the very early stages of adoption. It would be wise for grocers to keep track of all the innovation.

But back to physical reality. Labor shortages, another consequence of the pandemic, are a persisting challenge. Solutions lie in continued investments in AI and automation for unfilled jobs and in initiatives like the Kroger tuition program, Giant Food stores scholarships, Publix tuition reimbursement, and Walmart’s $5 billion upskilling initiative, which exemplify investments in education, skills training, credentialing, and employment frameworks. Amazon has its own upskilling program – 10 to be exact.

Career Choice—one of Amazon’s 10 upskilling programs—pays for educational opportunities, ranging from English as a second language classes to four-year college degrees for 750,000 eligible frontline workers. There’s no repayment clause should they leave the company. With 400 course options, 300 colleges, and 130,000 total participants to date, Career Choice is Amazon’s most expansive upskilling program. In September 2021, the retail giant pledged to invest $1.2 billion through 2025 in Career Choice and other upskilling efforts.

Amazon’s programs see success as illustrated through two measures: course completion and post-graduation job placement rates. The goal: retention and reinvestment. In each case, these upskilling strategies reflect the awareness that the industry is changing rapidly, wave by wave. The grocery industry, therefore, needs a comprehensive strategy to navigate these waves. In the short term, retailers can continue helping customers save money where it matters most, develop protocols with suppliers or accept price increases, and reassure customers through clear communication about mitigating impacts, such as inflation.

In the longer term, a more visionary approach is necessary. Retailers could consider developing AI-powered grocery budgeting tools, morphing into their customers’ trusted financial partners, and even launching private-brand-only formats of the future. Such strategies could allow grocery businesses to better meet customer needs while leveraging the forces shaping the industry.

The role of technology in this transformation is inescapable. Artificial intelligence and next-gen software development have the potential to revolutionize the way the grocery industry operates and interacts with its customers. The utilization of these technologies, coupled with a dedicated focus on data-driven insights, will enable retailers to provide fully integrated customer experiences and stay ahead in the fiercely competitive market. It’s imperative for grocery retailers to actively take part in the development and regulation of AI-assisted grocery commerce.

As the grocery sector steps into the metaverse, the way it engages with customers will evolve dramatically. Traditional brick-and-mortar grocery shopping could be supplemented, or in some cases replaced, by immersive virtual experiences. The successful navigation and adoption of these platforms could shape the future success of grocery retailers.

Summary

I believe that it comes down to people first. Investments in education, skills training, and employee development will not only help retailers address this issue but also serve as powerful marketing strategies. By portraying themselves as conscientious employers committed to their staff’s welfare and development, retailers can distinguish themselves in the crowded market.

The grocery industry is set to undergo a profound transformation in the coming decades. Amidst economic concerns and technological advancements, the industry must adapt to better serve its customers. Fiscal conservatism, technological breakthroughs, labor shortages, and the digital revolution are all ingredients in the recipe for the grocery industry’s future. Retailers who can effectively blend these components while continuously innovating to meet customer needs are those who will thrive until 2053 and beyond. The evolution of the grocery industry, therefore, hinges on its ability to transform challenges into opportunities, ensuring it remains a central part of our lives for generations to come.

The goal of grocery retailers will be to combine ease of purchase with an awareness of the pricing pressures that will come to define the next 30 years. Human resources, data science, and the employment of technologies available will determine which retailers do the defining.

By Web Smith | Edited by Hilary Milnes with art by Alex Remy and Christina Williams