This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.

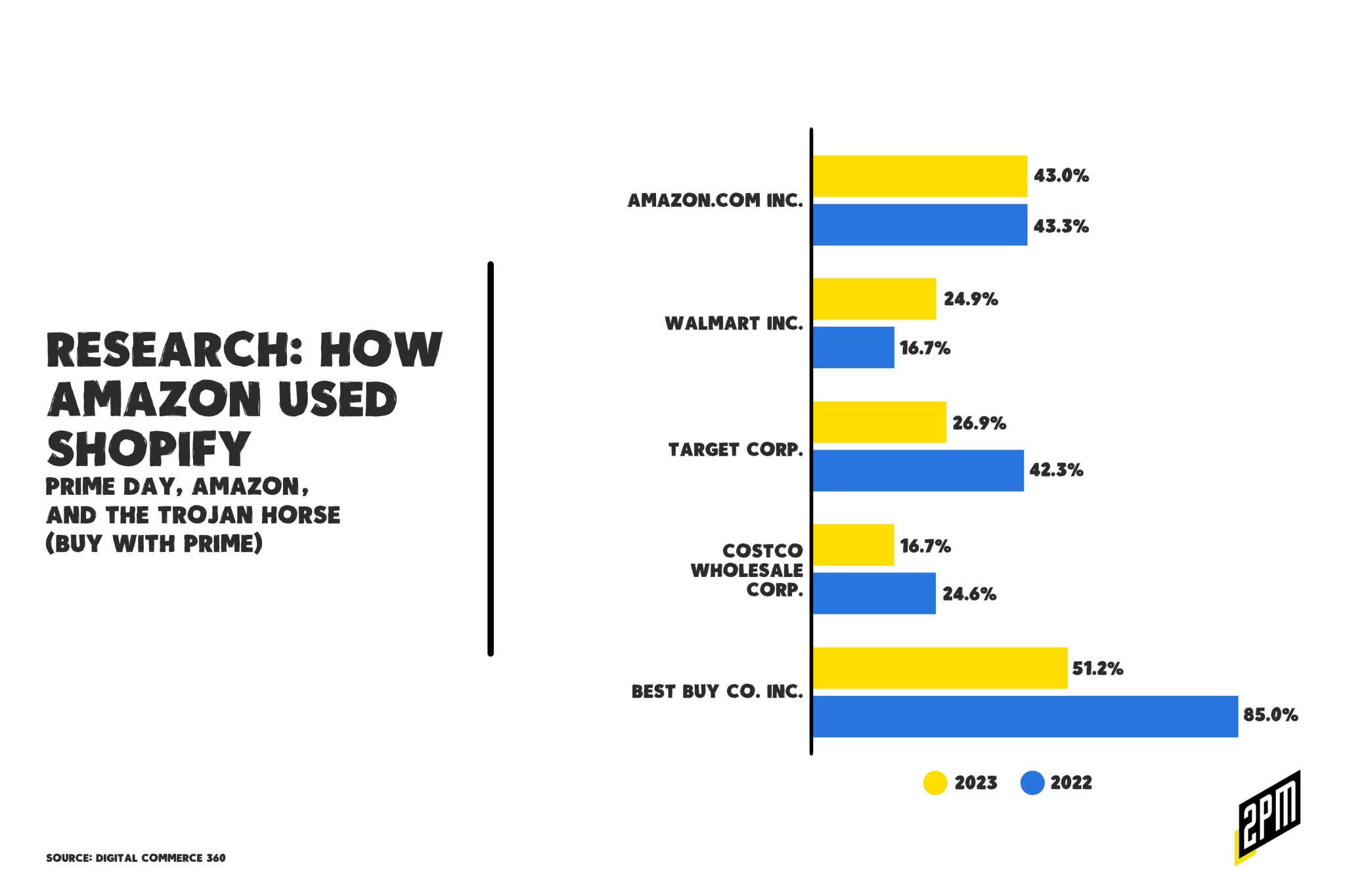

Member Research: How Amazon Used Shopify

This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.

Memo: Cyber Five

More than a quantitative measure of retail health, this year’s span of five days – beginning on Thanksgiving and ending on Cyber Monday – may serve as a judge of the entire economy. If text messages like these are any indication, our economy is coming out of its hole:

Positive news: we absolutely, unequivocally CRUSHED BFCM week.

Black Friday fought the good fight against inflation and cost of living hikes, this year. But there’s more to this weekend’s holiday shopping story than that day. Our Blackest Friday report began with a Jeff Bezos quote: “Don’t buy a fridge, hold on to your money.” So to spend or not to spend? This was the question. The answer was a resounding ‘yes’; consumers spent despite the economic forces at play. First, the top line numbers.

- According to Adobe, online sales for Black Friday reached a record $9.12 billion, a 2.3% year-over-year increase.

- Adobe anticipated that weekend online sales on the Saturday and Sunday on Thanksgiving weekend would hit $9 billion on their own, while Cyber Monday sales would hit $11.2-11.7 billion, versus $10.7 billion last year.

- This year, mobile shopping hit a new record, accounting for 48% of online sales, up from 44% last year. Buy now, pay later schemes also had a big year – a sign of the times.

- BNPL orders increased 78% during the holiday week (November 19-25) compared to the week prior, while BNPL revenue increased 81% in the same time frame.

- Exercise equipment, toys, smart home devices, audio equipment, games and gaming devices, Macbooks and Dyson products were all top sellers. Apparel, sporting goods and TVs all saw peak discounts over the weekend.

In all, Adobe data indicates 2022’s “Cyber Five” is on track to generate a total of $34.8 billion in online sales, a 2.8% increase over 2021’s data and a drop off from the projected 7% growth that analysts predicted. A few things are happening at once.

In the past several years, retailers successfully trained customers to shop earlier and earlier: Cyber 5 is more like October through December. This allowed for a steadier stream of high sales volume days – though none are expected to top Cyber Monday. The extension of the sales holiday also places less strain on logistics and supply chain efforts by spreading sales volume over 60-70 days rather than 6-7. As Adobe pointed out, savvy shoppers are waiting until December 1 to buy appliances, for instance, when discounts are expected to peak.

At the same time, inflation is the story of this season. A 2.8% increase is insignificant compared to the 7% projection. The 2.8% increase is less impressive when you consider the higher consumer pricing index (CPI). Discounts for the holiday weekend were also not as extreme, hinting that retailers are waiting to see how much is necessary in terms of markdowns before customers bite. As Axios calls it, it’s a “game of chicken” to see who gives in first: the customers making purchases vs. the retailers setting the prices. Last year, customers were scrambling to buy early to avoid everything selling out as supply chain backups gripped the season. USA Today reported on this year’s consumers bargain hunting before a different backdrop:

Due to elevated prices for food, rent, gasoline and other essentials, many people were being more selective, reluctant to spend unless there was a big sale. Some were dipping more into savings, turning to “buy now, pay later” services that allow payment in installments, or running up their credit cards at a time when the Federal Reserve is hiking rates to cool the U.S. economy.

The Two Winners: BNPL and Physical Stores

One industry segment that is benefitting from the current economic shortfall are the “buy now, pay later” family of companies. These platforms removed one more barrier out of the way of cash-sensitive consumers, allowing them to pay for products over the course of four or more payments – minimizing up front costs. Holiday seasons are often mortgaged during times of economic distress.

In a US survey, 60% of people were found to be more likely to use BNPL because of inflation, and 53% were using BNPL out of necessity. Forty-five percent said they were were most likely to use BNPL when their finances are tight. That means that Klarna’s 2022 troubles aren’t to be blamed on a decline in interest on BNPL. But rather, a more tenuous financial outlook makes people more reliant on services like BNPL. For many, it’s a way to make purchases now without taking on credit card debt. It’s a dangerously unregulated substitute for traditional debt. CNBC recently explained how Klarna’s rebound may be tied to increase usage:

In a US survey, 60% of people were found to be more likely to use BNPL because of inflation, and 53% were using BNPL out of necessity. Forty-five percent said they were were most likely to use BNPL when their finances are tight. That means that Klarna’s 2022 troubles aren’t to be blamed on a decline in interest on BNPL. But rather, a more tenuous financial outlook makes people more reliant on services like BNPL. For many, it’s a way to make purchases now without taking on credit card debt. It’s a dangerously unregulated substitute for traditional debt. CNBC recently explained how Klarna’s rebound may be tied to increase usage:

The Stockholm-based startup saw 85% erased from its market value in a so-called “down round” earlier this year, taking the company’s valuation down from $46 billion to $6.7 billion, as investor sentiment surrounding tech shifted over fears of a higher interest rate environment.

This Cyber Five’s winner? The physical store. This year: Walmart, Target and Kohl’s all overtook Amazon in terms of online Black Friday discount searches according to data from Captify. Walmart searches surged 386%, followed by Target, then Kohl’s, then Amazon. That’s telling for a few reasons. People seem to associate Amazon with the best deals less than they used to. And more people are likely to search for deals across stores and online, knowing they can strike both at any of the big-box retailers before Amazon. According to MasterCard SpendingPulse data, in store sales increased 12% year over year. RetailNext, tracking foot traffic to stores, found that traffic rose 7% this year on Black Friday compared to 2021. Here was the takeaway from Placer.ai:

Shopping malls saw far and above average visits. Indoor malls saw visits up 261% compared to the daily average for Q1-Q3 2022, outlet malls saw visits up almost 366%, and open-air lifestyle centers saw visits up around 151%. Compared to the first three weeks of November 2022, visits were up about 277% (indoor), 395% (outlet), and almost 160% (open-air lifestyle centers), respectively, at those mall types.

Going into Black Friday, we forecasted some of these key elements, to include muted growth and the return to physical stores:

(1) The recessionary effects are likely to cause muted growth in eCommerce performance in a YoY basis. Searching for bargains, more customers will be pursuing in-store purchases where deals may be greater. (2) Try to conserve your money this season to prepare for any additional market downturns. It’s likely that large purchases may be fewer and farther between in 2022 YoY basis. (3) eCommerce marketplaces will do better than traditional DTC brands’ online stores because utility purchases are likely to rise vs. luxury and other purchases that signal high-discretionary income.

But about that traditional DTC brand thought, it wasn’t altogether accurate. Shopify noted: “More than 52 million consumers globally purchased from brands powered by Shopify this year, an 18% increase from 2021.” Shopify reported promising Black Friday sales figures for its merchants; Shopify merchants brought in $1.52 million a minute on Thanksgiving and $3.5 million per minute at its Black Friday peak, setting a record with $3.36 billion and $7.5 billion between Friday and Monday. This was a 19% increase in sales and a 21% increase on a constant currency basis. But this is more a reflection of how Shopify has grown as an enterprise retail provider than as a snapshot of the greater whole.

Cyber Monday Data (via Adobe)

According to Adobe’s data, consumers rang in $11.3 billion on Cyber Monday, seeing the industry to a 5.8% YoY improvement and a whopping $12.8 million earned per minute. Vivek Pandya, lead analyst, Adobe Digital Insights:

With oversupply and a softening consumer spending environment, retailers made the right call this season to drive demand through heavy discounting. It spurred online spending to levels that were higher than expected, and reinforced e-commerce as a major channel to drive volume and capture consumer interest.

In all, the Cyber Five earned $35.27 billion, a 4% increase over 2021’s eCommerce-driven holiday season. This number is even bigger when you consider the entirety of the shopping season: November 1 – November 28 rang in $107.7 billion with $210 billion expected through December 31. How did this happen? Adobe Analytics noted that discounting hit records highs in 2022 to offset the rising costs of living. And BNPL services like Affirm saw volume rise 85% vs. the prior week, increasing revenue 88% over that time period. One surprising line from the analytics data provided by Adobe:

Strong consumer spending across Cyber Week was driven by net-new demand, and not just higher prices.

Consumers came out for the week and chose the glee over doom, there will be study after study written about this holiday season. It wasn’t all black and white. With the holiday shopping season at its peak, the statistics have been unpredictable at best but not altogether surprising. Retail is irrational and retailers are hoping that it stays that way over the closing four weeks of the holiday shopping season. Jeff Bezos went unheard, consumers chose the 30% off refrigerator over holding on to their money. Let’s just hope that the good news extends and the economy continues its slow recovery.

By Web Smith | Edited by Hilary Milnes with art by Alex Remy and Christina Williams