Этот краткий обзор предназначен исключительно для Исполнительные членыЧтобы упростить членство, вы можете нажать на кнопку ниже и получить доступ к сотням отчетов, нашему списку DTC Power List и другим инструментам, которые помогут вам принимать решения на высоком уровне.

Deep Dive: Value and Volatility (CPG Lending)

In the dynamic landscape of fintech lending, one leading lender initiated a strategic collaboration with 2PM. This partnership aimed to leverage 2PM’s deep insights into consumer behavior and brand performance, utilizing key data points to refine lenders’ approaches to credit offerings.

By analyzing detailed market data, the lender was better positioned to assess the financial health and potential of individual brands, enabling more informed decision-making processes. This collaboration not only underscores this particular lenders’ commitment to “outside-of-the-box” data-driven strategies but also enhances their capability to support sustainable brand growth in an increasingly competitive market. All is not well in the market.

Confirmed by subsequently published reports, the pressure on fintech lenders like Ampla is mounting. This is evidenced not only by their reported financial struggles but also by the outreach from competitors seeking to capitalize on Ampla’s vulnerabilities. A recent LinkedIn post by a Paperstack employee highlighted the concerns within the CPG industry and their competitor’s potential failure. It specifically acknowledged the deep financial challenges Ampla might be facing and extending a helping hand to those affected. This situation underscores a larger trend in the fintech sector, where companies are both competitors and crucial lifelines, offering necessary capital to businesses navigating the capital-intensive journey of eCommerce.

By analyzing detailed market data, the lender was better positioned to assess the financial health and potential of individual brands, enabling more informed decision-making processes. This collaboration not only underscores this particular lenders’ commitment to “outside-of-the-box” data-driven strategies but also enhances their capability to support sustainable brand growth in an increasingly competitive market.

****

Ampla’s notable clients include:

- MrBeast Feastables: A brand launched by the YouTube personality MrBeast, focusing on snacks.

- Cuts: A clothing brand known for its high-quality men’s shirts.

- Serenity Kids: A company that produces baby food.

- Hatch: A brand offering sleep-related products.

- Recess: A beverage company specializing in sparkling water infused with hemp and adaptogens.

- Glamnetic: A beauty brand known for magnetic eyelashes.

- Maev: A pet food company that provides raw dog food.

- MM.LaFleur: A women’s clothing brand focusing on professional attire.

- Toybox: A company that offers 3D printers designed for kids.

- Wandering Bear: A coffee brand offering cold brew coffee.

- Stately: A men’s fashion subscription service.

- &Collar: A sustainable clothing brand.

****

According to recent reports, the pressure on fintech lenders like Ampla is mounting. This is evidenced not only by their reported financial struggles but also by the outreach from competitors seeking to capitalize on Ampla’s vulnerabilities. A recent LinkedIn post by a Paperstack employee highlighted the concerns within the CPG industry and their competitor’s potential failure. It specifically acknowledged the deep financial challenges Ampla might be facing and extending a helping hand to those affected. This situation underscores a larger trend in the fintech sector, where companies are both competitors and crucial lifelines, offering necessary capital to businesses navigating the capital-intensive journey of eCommerce.

In addition to this particular blog from Paperstack, I’ve personally received similar messages a few of Ampla’s other competitors, each presenting their services as stable, long-term financial solutions. Other publications and smaller consultancies have reported similar activity. These interactions tell a tale. For one, they mark a significant shift in how digital capital is being approached in today’s market. The competitive market was difficult for these lenders, as early as February 2023 (according to this Betakit report on the growing lender – Paperstack). It can only be more difficult now.

Amid these conditions, Toronto’s Clearco and Dublin-based Wayflyer—two of the biggest FinTech firms providing revenue-based financing to e-commerce brands—have undergone significant layoffs. In Clearco’s case, the company has also changed CEOs and exited overseas markets, handing this portion of its business to London-based competitor Outfund.

The much smaller Paperstack faces the same conditions that forced bigger players to regroup, from mounting inflation and interest rates, which have made it difficult for many startups to raise capital, to slowing e-commerce growth.

Fintech lenders are operating in an even higher-pressure environment marked by several intersecting challenges:

Macroeconomic Shifts: The end of historically low interest rates has significantly impacted fintech lenders, increasing their cost of capital and forcing them to reassess their lending models. As borrowing becomes more expensive and economic growth cools, both lenders and borrowers face heightened financial stress.

Increased Competition: As traditional banks tighten their lending standards, more businesses have turned to revenue-hungry fintech startups for solutions, intensifying the competition among these lenders. Each platform strives to offer more attractive, flexible, and innovative financing solutions to stand out, as evidenced by the proactive outreach efforts from companies like Paperstack, Ampla, Kickfurther, Clearco, Shopify, Stripe, and others.

Sector-Specific Challenges: For fintechs focusing on CPG brands, like Ampla, the shift in consumer behavior towards more cost-effective purchasing and the rise of white-label products presented additional hurdles. These changes affect the financial stability and growth prospects of their clientele, directly impacting the risk assessments and business models of the lenders.

Regulatory Environment: Increasing scrutiny from regulators on lending practices adds another layer of complexity, pushing fintechs to innovate within the confines of new financial regulations. This requires continuous adaptation and compliance efforts, further straining their resources.

Technological Advancements: To stay competitive, fintech lenders must continuously invest in technology to improve their financial products and services. This includes enhancing risk assessment models with AI and machine learning, and developing more user-friendly platforms that can integrate seamlessly with the businesses they serve.

These challenges collectively contribute to the high-pressure environment that defines the new era of digital capital. Fintech lenders are not only required to be financially robust but also agile and innovative, capable of quickly adapting to changing market conditions and customer needs.

The public and private outreach from companies like Paperstack is indicative of the broader strategic shifts occurring within the fintech sector. As companies vie for leadership in this tumultuous market, their ability to provide reliable, flexible, and efficient financial solutions will likely determine their success. For consumer businesses reliant on these financial services, the landscape offers both potential risks and rewards, emphasizing the importance of choosing partners that align with their long-term financial goals and operational needs.

The Core Target of the Fintech SAAS Lender

The core target industry is undergoing significant transformation due to evolving consumer behaviors and economic pressures, which in turn are impacting the CPG lending industry. In a recent deep dive on CPG, I reported:

The landscape for CPG brands is undergoing a seismic shift, marked by increased challenges in distribution avenues, market consolidation by retail giants, diminishing venture capital interest, and heightened cost pressures. This confluence of factors is rapidly closing the window of opportunity for CPG brands to achieve widespread distribution and visibility.

As the financial landscape shifts, fintech companies that specialize in lending to CPG brands are facing unique challenges but, also, new opportunities that necessitate strategic adaptation to stay competitive and relevant. Here are the key points influencing the changing role that debt financing is playing in the role of CPG brands and beyond.

By nature, this makes debt a much higher risk to the brand and the lender.

As eCommerce continues to expand, small retailers are finding the space increasingly challenging to navigate, contrary to the expectations set by eCommerce’s growing adoption. This complexity is rooted in various structural changes in consumer behaviors, market dynamics, and intensified competition, particularly from dominant industry players.

The CPG Struggle

The story of Foxtrot Market’s failure illustrates a critical issue many small eCommerce retailers face: misalignment with consumer expectations. Foxtrot aimed to differentiate itself with a unique, upscale product mix and aesthetic appeal but neglected to integrate essential items that meet daily consumer needs, which are crucial for driving repeat business in the convenience sector. This example highlights a broader narrative where small retailers struggle to balance unique offerings with the essential expectations of convenience and necessity. Their focus on specialty items rather than staples, combined with high operational costs from city center locations, rendered Foxtrot’s business model unsustainable in a highly competitive market.

Moreover, the digital advertising landscape, once a boon for small eCommerce ventures, has become prohibitively expensive. As costs escalate—with 96% of CPG companies managing spends across multiple networks—the already tight budgets of smaller players are further squeezed. Additionally, the consolidation of market power by retail giants such as Walmart, Costco, and Kroger further narrows the window for smaller brands to gain visibility and shelf space. Data show a significant concentration of CPG spending among these major players, which captures a substantial portion of U.S. CPG expenditures, creating formidable barriers for smaller companies.

Evolving consumer preferences complicate the entry of new or smaller brands into the market, particularly the preference for purchasing groceries from established retailer websites over new online marketplaces or direct brand channels. As eCommerce grows, especially in sectors like food and beverage, small retailers must navigate the challenging waters of gaining consumer trust and visibility amidst dominant competitors.

The landscape for entering eCommerce has also become tougher, with diminishing venture capital interest in new, unproven markets. The shift in economic conditions, increased interest rates, and a demanding profitability path have led to a more cautious approach from investors. This financial backdrop makes it increasingly difficult for small eCommerce retailers to secure the necessary capital for growth and sustainability. By nature, this makes debt a much higher risk to the brand and the lender.

Another dimension of the challenge for small retailers is the blurring of lines between high-end and mass-market offerings on major e-commerce platforms. The presence of luxury brands on platforms like Walmart underscores the difficulty of maintaining brand integrity and visibility in an overcrowded online space. This juxtaposition creates a confusing marketplace where small retailers struggle to position themselves effectively.

In an eCommerce environment described as “junkified,” (a direct quote to Vogue Business by Neil Saunders) where the proliferation of products overwhelms consumers, small retailers must find ways to stand out. The necessity for strategic innovation, effective curation, and clear brand positioning has never been more critical. Marketplaces need to balance the breadth of offerings with curation, ensuring consumers are not overwhelmed but rather guided to quality and relevant products.

These challenges collectively depict an eCommerce landscape that is becoming more complex and less accessible for small retailers, demanding a strategic recalibration and innovative approaches to consumer engagement, product offerings, and market positioning.

Consumer Shifts to Cost-Conscious Buying

Economic constraints have led consumers to become more cost-conscious, increasingly opting for white-label or generic products over branded goods. This shift is driven by a squeeze on household budgets, where affordability has begun to trump brand loyalty. A Forbes article from May 2024 highlighted that over half of consumers are concerned about their personal finances, influencing their purchasing decisions towards cheaper alternatives. This consumer behavior shift impacts the revenue streams and stability of CPG brands, which are critical factors that lenders consider when evaluating creditworthiness.

Impact on CPG Brands and Their Financing Needs

As CPG brands adjust to these market changes, their need for flexible and responsive financing solutions increases. Traditional lending models, which rely heavily on stable and predictable revenue streams, may no longer be adequate. Fintech lenders, therefore, need to adapt their products to accommodate fluctuations in CPG companies’ cash flows and provide more tailored financing options that can adjust to a more volatile market environment.

The Role of Fintech in Adapting Lending Practices

Fintech companies like Ampla have been at the forefront of providing innovative financial solutions tailored to the needs of CPG brands; this is both a gift and a curse. These companies leverage technology and data analytics to offer dynamic credit products that can adapt to rapid changes in the market. For example, fintech lenders might use advanced underwriting algorithms that take into account real-time sales data or seasonal fluctuations, allowing for more flexible repayment terms that align with a brand’s cash flow patterns.

Increased Competition and Market Pressure

The tightening of lending standards by big banks, as reported by Bloomberg in May 2024, is creating an additional layer of complexity. As banks become more conservative in their lending practices, particularly in response to economic instability and previous bank failures, CPG brands may find it more difficult to secure traditional financing.

Lenders have generally been tightening credit standards since the second quarter of 2022, following a string of high-profile regional bank failures. The Fed lifted its benchmark rate last year to a two-decade high in a bid to curb inflation, and high borrowing costs have weighed on businesses and households.

This situation presents both a challenge and an opportunity for fintech lenders. While it opens the door for these lenders to fill the gap left by banks, it also puts pressure on them to manage risk more effectively amid an increasingly competitive landscape.

****

To effectively serve CPG brands under these new conditions, fintech lenders are increasingly looking towards strategic collaborations. For instance, partnerships between fintechs and retail data aggregators can provide deeper insights into consumer trends, brand performance, and market dynamics, enhancing the lenders’ ability to assess risk and customize financial products. Moreover, as CPG brands seek to differentiate themselves in a crowded market, fintech solutions that can support innovative retail strategies—such as DTC models and online marketplaces—become particularly valuable.

The evolving CPG industry, marked by a shift towards more price-sensitive consumer behaviors and the resultant impact on brand stability and growth prospects, is significantly influencing the CPG lending industry. Fintech lenders are responding with more adaptive, innovative, and risk-aware lending solutions that align more closely with the current needs of CPG brands, ultimately reshaping the landscape of financial services in this sector.

Веб Смит

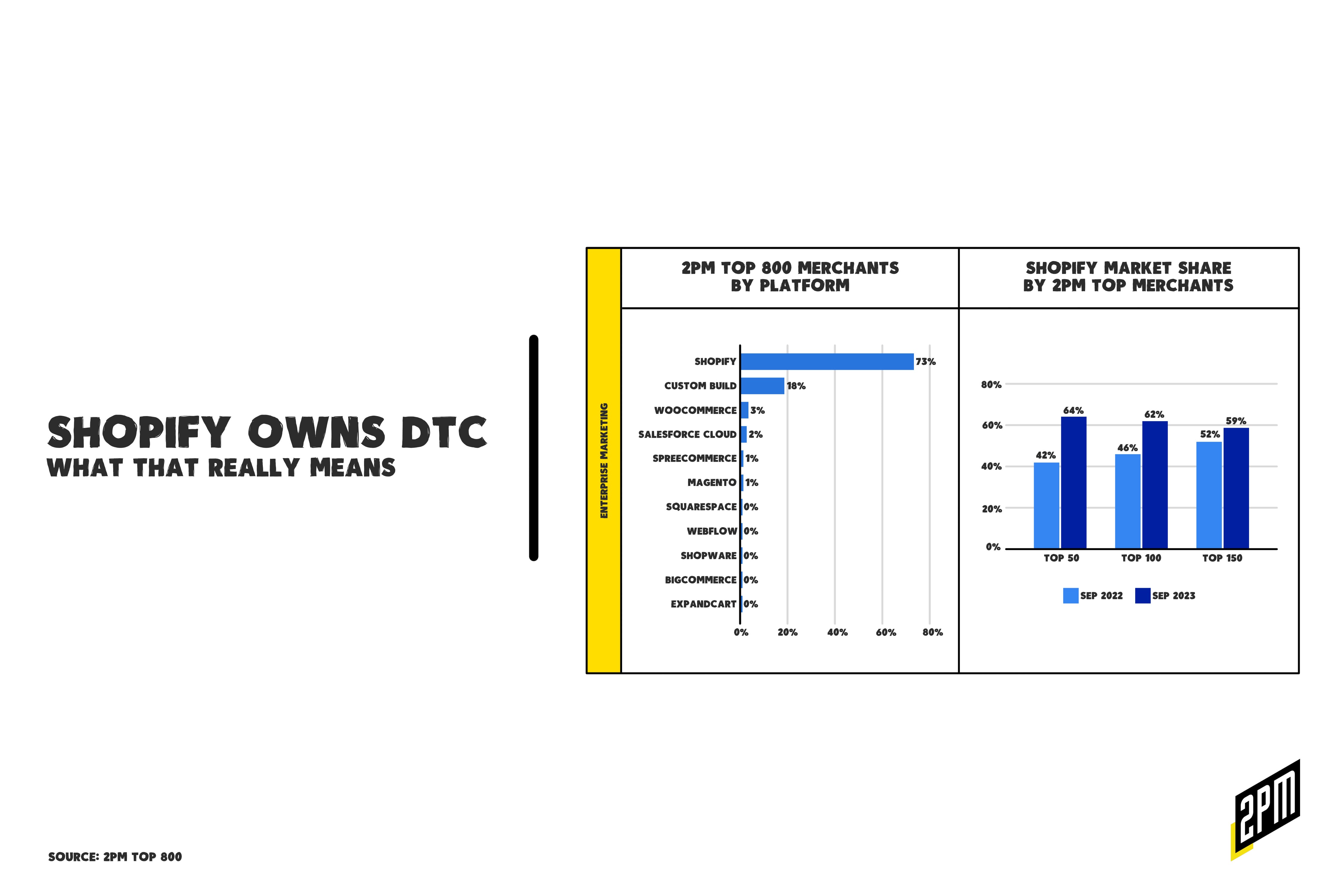

Меморандум: Shopify владеет DTC

Но что это значит на самом деле? Все чаще это нечто иное, чем вы думаете. Давайте посмотрим правде в глаза: октябрьский запуск Nike Strength был не слишком удачным. Частично это объясняется тем, что сайт был создан на базе Shopify. Это не диссонанс Shopify, это отражение состояния розничной торговли по принципу "от потребителя к покупателю".

Впечатляет не только то, что Shopify из года в год возглавляет список DTC Power List, но и то, что это свидетельствует о грядущих переменах. Мы находимся на пороге эпохи трансформации технологий электронной коммерции, которая отчасти формируется благодаря растущей доле рынка Shopify. Восхождение Shopify - это свидетельство надежной платформы, предлагающей предприятиям инструменты для беспрепятственного создания и управления интернет-магазинами. Хотя этот подъем подчеркивает демократизацию электронной коммерции, предоставляя как корпоративным брендам, так и мелким торговцам упрощенный путь к цифровым продажам, он также побуждает к критическому анализу инвестиционных стратегий в секторе онлайн-ритейла.

Удобство Shopify, заключающееся в более низком барьере для входа, возможно, невольно привело к сокращению инвестиций в специализированные инфраструктуры онлайн-ритейла, что ставит стратегическую дилемму, поскольку многоканальная розница и цифровые рынки продолжают доминировать во взаимодействии с потребителями. Рассматривая запуск Nike Strength на Shopify или экспансию True Classic в физические магазины, мы обнаруживаем сложный ландшафт возможностей и проблем.

В 2022 году True Classic в партнерстве со сторонней платформой Leap открыла пять поп-апов в Лос-Анджелесе, Сан-Хосе, Чикаго и Вашингтоне. Хотя поп-апы останутся открытыми, компания заявила, что берет физические розничные операции под свой контроль, что позволит ей оснастить свои магазины "возвышенным, доступным брендингом, который резонирует с их потребителем".

Для компании размера и скорости развития True Classics Shopify - отличное решение, относительно недорогое и бесконечно масштабируемое. Оно не мешает другим планам. Сегодня, как никогда ранее, бренды рассматривают DTC как часть стратегии, а в некоторых случаях это наименее значимая часть многостороннего подхода. Как это выглядит? Один из недавних примеров - партнерство Mars с Uber в рекламе Skittles.

Mars демонстрирует интерактивные объявления Uber Journey Ads и Post-Check Out Ads потребителям, которые едут в автомобиле Uber или ожидают свой заказ в Uber Eats. Эти объявления позволят потребителям легко взаимодействовать с сайтом Skittles и добавлять продукты Skittles в свои корзины Uber Eats.(CSA)

По мере того как маркетинговые каналы продолжают сливаться с каналами продаж, мы можем увидеть меньше внимания к традиционным маркетинговым воронкам (Meta или Google > Shopify.com > checkout) и больше ориентированных на контент онлайн-направлений, как на вышеупомянутом сайте Skittles. Но без такого уровня амбиций маркетинга и продаж подобная архитектура больше не характерна для DTC-операций.

Преимущества роста доли рынка Shopify

Снижение барьеров для входа. Shopify произвел революцию в индустрии электронной коммерции, сделав создание интернет-магазина доступным и экономически эффективным. Это преимущество ощутимо при наблюдении за решением Nike использовать Shopify для NikeStrength.com. Этот шаг свидетельствует о стратегическом повороте, когда для новых предприятий на первый план выходят оперативность и время выхода на рынок. Снизив технический и финансовый порог, Shopify позволил множеству организаций принять участие в цифровой экономике с максимальной гибкостью и минимальными инвестициями.

Omnichannel Synergy. Расширение розничной сети True Classic иллюстрирует потенциал Shopify для повышения эффективности омниканального взаимодействия. Их магазины, оснащенные технологиями, ориентированными на цифровые технологии, способны преодолеть разрыв между удобством онлайн и тактильным знакомством с брендом. Эта синергия подчеркивается в недавней статье Inc., где отмечается, что такие бренды, как Bark и Bala, отказываются от чистой модели DTC в пользу гибридного подхода, объединяющего физическую розницу и онлайн-каналы.

"Мы не считаем себя DTC-брендом", - говорит Кислевиц, чья компания производит Bala Bangles - приспособленные для упражнений гири, которые пристегиваются к телу. "Я обнаружил, что омниканальный подход создает по-настоящему эффективную экосистему", - продолжает он.(Inc.)

Виртуозный цикл взаимодействия магазина и онлайн создает всеобъемлющую экосистему бренда, которая может увеличить охват и лояльность клиентов.

Потенциальные недостатки доминирования Shopify

Недостаточное инвестирование в онлайн-ритейл. Несмотря на преимущества, существует риск, что простота использования Shopify может способствовать минимализму в инвестициях в инфраструктуру онлайн-ритейла. Бренды могут пренебречь разработкой оригинальных и инновационных онлайн-проектов, подобных тому, что предлагает Skittles, что приведет к насыщению рынка магазинами, сделанными по шаблону и не отличающимися друг от друга. Лидеры должны осознать, что, хотя такие решения, как Shopify, играют важную роль в запуске онлайн-платформ, они не являются панацеей для конкурентного цифрового рынка, который требует уникальности и индивидуальности бренда. И хотя многие реализуют омниканальные стратегии, когда стратегии DTC-first снова станут популярными, бренды могут захотеть больше изысканности или индивидуальности.

Omnichannel и конкуренция на цифровом рынке. Эволюция модели omnichannel требует переоценки подхода direct-to-consumer. Как отмечается в статье Inc., нельзя игнорировать экономическую логику, лежащую в основе оптовых поставок по сравнению с индивидуальным исполнением. Осознание этого факта побуждает игроков DTC диверсифицировать свою модель продаж. Простота Shopify поначалу может привлекать бренды, но вскоре становится очевидным спрос на более диверсифицированную, омниканальную стратегию, что заставляет бренды выходить за рамки только цифровых моделей.

Тематические исследования: Стратегические шаги Nike и True Classic

Выбор компании Nike в пользу Shopify. Переход Nike на Shopify для специализированной линейки продуктов отражает скорее гибкую стратегию, ориентированную на конкретные проекты, чем оптовую смену платформы. Это иллюстрация того, что даже известные бренды видят ценность в использовании простоты Shopify для определенных сегментов, не перекладывая на нее все свое присутствие в Интернете. Это стратегическое решение, нацеленное на быстрое развертывание и гибкость, а не на большие инвестиции и индивидуальную настройку основного сайта.

Кирпично-минометная стратегия True Classic. В отличие от этого, предприятие True Classic по созданию физической розничной сети, о котором подробно рассказывается в статье Chain Store Age, означает стратегический поворот к "собственным и управляемым" магазинам. Этот шаг позволяет бренду погрузить покупателей в контролируемую, ориентированную на бренд среду, дополнив их онлайн-присутствие осязаемым опытом. Приверженность бренда иммерсивной цифровой вовлеченности в магазине свидетельствует о глубоком понимании динамики современной розничной торговли, где физическое движется за счет цифрового, чтобы продвигать бизнес вперед.

Компания True Classic, основанная в 2019 году, направляет свои усилия на быстрое расширение розничной торговли, что является естественным следующим шагом для личного общения с покупателями, а также для привлечения новой аудитории, говорится в сообщении компании.

Контраст здесь разительный и показательный. True Classic опирается на ценность близости к покупателю, которую могут создать физические магазины, делая ставку на привлекательность личного опыта для укрепления лояльности к бренду. Nike, напротив, использует гибкость Shopify, чтобы расширить сферу влияния своего бренда без необходимости вносить значительные изменения в инфраструктуру. Оба подхода подчеркивают важнейшее стратегическое понимание: будущее розничной торговли - это не универсальный подход, а индивидуальный подход к бренду и ожиданиям покупателей.

Это два бизнеса на двух разных этапах; оба используют Shopify по разным причинам. Расширение доли рынка Shopify предвещает доступную точку входа в сферу электронной коммерции, но одновременно побуждает лидеров отрасли задуматься о долгосрочных последствиях такой модели. Конвергенция простоты и вездесущности не должна удерживать нас от инвестиций в особый, захватывающий опыт бренда в онлайне и офлайне. Мы должны разработать стратегии, которые бы использовали сильные стороны таких платформ, как Shopify, и в то же время стремились к целостному омниканальному видению. Такой двойной подход обеспечит нам не только процветание на нынешнем рынке, но и подготовку к его будущему, в котором бренды будут гордиться тем, что относятся к категории DTC, и вести свой бизнес именно так.

Веб Смит | Редактор: Хилари Милнс с иллюстрациями Алекса Реми и Кристины Уильямс