深入探讨:价值与波动(中央政府贷款)

在金融科技贷款的动态环境中,一家领先的贷款机构与 2PM 展开了战略合作。这一合作旨在利用 2PM 对消费者行为和品牌表现的深刻洞察,利用关键数据点来完善贷款机构的信贷服务。

通过分析详细的市场数据,贷款机构能够更好地评估各个品牌的财务健康状况和潜力,从而做出更加明智的决策。这次合作不仅彰显了这家特殊贷款机构对 "打破常规 "的数据驱动战略的承诺,还增强了他们在竞争日益激烈的市场中支持品牌可持续发展的能力。市场并非一切顺利。

随后公布的报告证实,Ampla 等金融科技贷款机构面临的压力越来越大。这不仅体现在他们所报告的财务困境上,也体现在竞争对手试图利用 Ampla 的漏洞进行扩张上。Paperstack 的一名员工最近在LinkedIn 上发表的一篇文章强调了 CPG 行业的担忧及其竞争对手的潜在失败。帖子特别提到了 Ampla 公司可能面临的巨大财务挑战,并向受影响者伸出了援助之手。这种情况凸显了金融科技领域的一个大趋势,即公司既是竞争对手,又是重要的生命线,为企业提供必要的资金,帮助它们在资本密集型的电子商务之旅中顺利前行。

通过分析详细的市场数据,贷款机构能够更好地评估各个品牌的财务健康状况和潜力,从而做出更加明智的决策。这次合作不仅彰显了这家特殊贷款机构对 "打破常规 "的数据驱动战略的承诺,还增强了他们在竞争日益激烈的市场中支持品牌可持续增长的能力。

****

Ampla 的知名客户包括

- MrBeast Feastables:YouTube达人MrBeast推出的品牌,主打零食。

- 剪裁:以生产高品质男士衬衫而闻名的服装品牌。

- 宁静儿童一家生产婴儿食品的公司。

- 哈奇提供睡眠相关产品的品牌。

- Recess:一家专门生产注入大麻和适应原的气泡水的饮料公司。

- Glamnetic:一个以磁性睫毛闻名的美容品牌。

- Maev:一家提供生狗粮的宠物食品公司。

- MM.LaFleur:专注于职业装的女装品牌。

- Toybox:一家提供专为儿童设计的 3D 打印机的公司。

- Wandering Bear:提供冷萃咖啡的咖啡品牌。

- Stately:男士时尚订阅服务。

- &Collar:可持续服装品牌。

****

根据最近的报道,Ampla 等金融科技贷款机构面临的压力越来越大。这不仅表现在他们所报道的财务困境上,还表现在竞争对手试图利用 Ampla 的弱点。Paperstack 的一名员工最近在LinkedIn 上发表的一篇文章强调了 CPG 行业的担忧及其竞争对手的潜在失败。帖子特别提到了 Ampla 公司可能面临的巨大财务挑战,并向受影响者伸出了援助之手。这种情况凸显了金融科技领域的一个大趋势,即公司既是竞争对手,又是重要的生命线,为企业提供必要的资金,帮助它们在资本密集型的电子商务之旅中顺利前行。

除了 Paperstack 的这篇博客外,我个人还收到了 Ampla 其他几个竞争对手的类似信息,他们都把自己的服务说成是稳定、长期的金融解决方案。其他出版物和小型咨询公司也报告了类似的活动。这些互动说明了一个问题。首先,它们标志着当今市场上的数字资本方式发生了重大转变。早在 2023 年 2 月(根据Betakit 这份关于成长中的贷款机构--Paperstack 的报告),这些贷款机构的市场竞争就很激烈。现在只会更加困难。

在这种情况下,多伦多的 Clearco 公司和都柏林的 Wayflyer 公司--两家为电子商务品牌提供基于收入的融资的最大金融科技公司--进行了大幅裁员。就 Clearco 而言,该公司还更换了首席执行官,并退出了海外市场,将这部分业务交给了总部位于伦敦的竞争对手 Outfund。

规模小得多的 Paperstack 也面临着迫使大型企业重组的同样情况,从通胀和利率的不断攀升(这使得许多初创企业很难筹集到资金)到电子商务增长的放缓。

金融科技贷款机构在压力更大的环境中运营,面临着几个相互交织的挑战:

宏观经济变化:历史低利率的结束对金融科技贷款机构产生了重大影响,增加了他们的资本成本,迫使他们重新评估自己的贷款模式。随着借贷成本的增加和经济增长的降温,贷款人和借款人都面临着更大的财务压力。

竞争加剧:随着传统银行收紧贷款标准,越来越多的企业转向渴望创收的金融科技初创企业寻求解决方案,这加剧了这些贷款机构之间的竞争。为了脱颖而出,每个平台都在努力提供更具吸引力、更灵活、更创新的融资解决方案,Paperstack、Ampla、Kickfurther、Clearco、Shopify、Stripe 等公司的积极拓展就是明证。

特定行业的挑战:对于 Ampla 等专注于消费类商品品牌的金融科技公司而言,消费者行为向更具成本效益的购买方式转变以及白标产品的兴起带来了更多障碍。这些变化影响到客户的财务稳定性和增长前景,直接影响到贷款机构的风险评估和业务模式。

监管环境:监管机构对借贷行为日益严格的审查又增加了一层复杂性,迫使金融科技公司在新的金融监管范围内进行创新。这就需要不断调整和合规,进一步加大了它们的资源压力。

技术进步:为了保持竞争力,金融科技贷款机构必须不断投资于技术,以改进其金融产品和服务。这包括利用人工智能和机器学习增强风险评估模型,以及开发能与所服务的企业无缝集成的更方便用户的平台。

这些挑战共同促成了数字资本新时代的高压环境。金融科技贷款机构不仅要财务稳健,还要灵活创新,能够快速适应不断变化的市场环境和客户需求。

来自 Paperstack 等公司的公共和私人拓展活动表明,金融科技领域正在发生更广泛的战略转变。随着各家公司在这个动荡的市场中争夺领导地位,它们提供可靠、灵活、高效的金融解决方案的能力很可能将决定它们的成败。对于依赖于这些金融服务的消费企业来说,这种格局既带来了潜在的风险,也带来了回报,强调了选择符合其长期财务目标和运营需求的合作伙伴的重要性。

金融科技 SAAS 贷款机构的核心目标

由于不断变化的消费行为和经济压力,核心目标行业正在经历重大转型,这反过来又影响了中央政府贷款行业。笔者在最近一篇关于 CPG 的深度报道中指出

中央产品品牌的格局正在发生巨变,其特点是分销渠道面临更多挑战、零售巨头进行市场整合、风险投资兴趣减弱以及成本压力增大。在这些因素的共同作用下,消费类商品品牌实现广泛分销和知名度的机会之窗正在迅速关闭。

随着金融格局的变化,专门为中央政府采购品牌提供贷款的金融科技公司正面临着独特的挑战,但同时也面临着新的机遇,有必要进行战略调整,以保持竞争力和相关性。以下是影响债务融资在中央政府品牌及其他方面所扮演角色变化的要点。

从本质上讲,这使得债务对品牌和贷款人的风险更高。

随着电子商务的不断扩大,小型零售商发现这一领域越来越难以驾驭,这与电子商务日益普及所带来的期望背道而驰。这种复杂性源于消费者行为的各种结构性变化、市场动态以及日益激烈的竞争,尤其是来自行业主导者的竞争。

中央政府的斗争

Foxtrot Market 的失败说明了许多小型电子商务零售商面临的一个关键问题:与消费者的期望不符。Foxtrot 的目标是通过独特、高档的产品组合和美学吸引力实现差异化,但却忽略了整合满足消费者日常需求的必需品,而这对于推动便利行业的回头客至关重要。这个例子突出说明了一个更广泛的问题,即小型零售商努力在独特产品与便利性和必需品的基本期望之间取得平衡。他们专注于特色商品而非主食,再加上市中心地段的高运营成本,使得 Foxtrot 的商业模式在激烈的市场竞争中难以为继。

此外,数字广告曾是小型电子商务企业的福音,如今却变得昂贵得令人望而却步。随着成本的攀升,96% 的 CPG 公司都在管理多个网络的支出,小公司本已紧张的预算进一步受到挤压。此外,沃尔玛(Walmart)、好市多(Costco)和克罗格(Kroger)等零售巨头对市场力量的整合进一步缩小了小品牌获得知名度和货架空间的机会。数据显示,这些大公司的消费类电子产品支出非常集中,占据了美国消费类电子产品支出的很大一部分,给小公司造成了巨大的障碍。

不断变化的消费者偏好使新品牌或小品牌进入市场变得更加复杂,尤其是消费者更愿意从成熟的零售商网站购买食品杂货,而不是从新的在线市场或直接品牌渠道购买。随着电子商务的发展,特别是在食品和饮料等行业,小型零售商必须在竞争者占主导地位的情况下,在赢得消费者信任和知名度方面应对挑战。

进入电子商务领域的形势也变得更加严峻,风险资本对未经验证的新市场的兴趣越来越小。经济形势的转变、利率的提高以及对盈利能力的苛刻要求,导致投资者的态度更加谨慎。在这种金融背景下,小型电子商务零售商越来越难以获得增长和可持续发展所需的资金。从本质上讲,这使得债务对品牌和贷款人的风险更高。

小型零售商面临的另一个挑战是,主要电子商务平台上高端产品和大众产品之间的界限越来越模糊。奢侈品牌出现在沃尔玛等平台上,凸显了在过度拥挤的网络空间中保持品牌完整性和知名度的难度。这种并置造成了一个混乱的市场,小型零售商很难有效地定位自己。

在一个被形容为 "垃圾化"(直接引用尼尔-桑德斯对《Vogue Business》的评论)的电子商务环境中,产品的泛滥让消费者应接不暇,小型零售商必须想方设法脱颖而出。战略创新、有效策划和清晰的品牌定位比以往任何时候都更为重要。市场需要在产品的广度和策划之间取得平衡,确保消费者不会被淹没,而是被引导到优质和相关的产品上。

这些挑战共同描绘了一个对小型零售商来说越来越复杂、越来越难以接近的电子商务环境,要求对消费者参与、产品供应和市场定位进行战略调整和创新。

消费者转向注重成本的购买方式

经济拮据导致消费者更加注重成本,越来越多地选择白标产品或非专利产品,而不是品牌产品。这种转变的原因是家庭预算受到挤压,经济承受能力开始压倒品牌忠诚度。福布斯》2024 年 5 月的一篇文章强调,超过一半的消费者担心个人财务状况,这影响了他们的购买决策,使他们倾向于选择更便宜的替代品。这种消费行为的转变影响了中央政府品牌的收入来源和稳定性,而这正是贷款人在评估信用度时考虑的关键因素。

对 CPG 品牌及其融资需求的影响

随着 CPG 品牌适应这些市场变化,它们对灵活、反应迅速的融资解决方案的需求也随之增加。传统的贷款模式在很大程度上依赖于稳定和可预测的收入流,但这种模式可能不再适用。因此,金融科技贷款机构需要调整其产品,以适应 CPG 公司现金流的波动,并提供更加量身定制的融资方案,以适应更加动荡的市场环境。

金融科技在调整贷款做法中的作用

像 Ampla 这样的金融科技公司一直走在前列,为中央政府品牌的需求量身定制创新的金融解决方案;这既是一种恩赐,也是一种诅咒。这些公司利用技术和数据分析提供动态信贷产品,以适应市场的快速变化。例如,金融科技贷款机构可能会使用先进的承保算法,将实时销售数据或季节性波动考虑在内,从而使还款期限更加灵活,与品牌的现金流模式保持一致。

竞争加剧和市场压力

据彭博社 2024 年 5 月报道,大银行收紧了贷款标准,这又增加了一层复杂性。随着银行贷款行为变得更加保守,特别是为了应对经济不稳定和以往的银行倒闭事件,CPG 品牌可能会发现获得传统融资变得更加困难。

自 2022 年第二季度以来,在一连串备受瞩目的地区性银行倒闭事件之后,贷款机构普遍收紧了信贷标准。美联储去年将基准利率上调至二十年来的新高,以抑制通胀,高借贷成本对企业和家庭造成了压力。

这种情况对金融科技贷款机构来说既是挑战也是机遇。它为这些贷款机构填补银行留下的空白打开了大门,同时也给它们带来了压力,要求它们在竞争日益激烈的环境中更有效地管理风险。

****

为了在这种新形势下有效地为中央政府品牌提供服务,金融科技贷款机构正越来越多地寻求战略合作。例如,金融科技公司与零售数据聚合商之间的合作可以深入洞察消费者趋势、品牌表现和市场动态,从而提高贷款机构评估风险和定制金融产品的能力。此外,随着中央政府品牌寻求在拥挤的市场中脱颖而出,能够支持创新零售战略(如 DTC 模式和在线市场)的金融科技解决方案变得尤为重要。

不断发展的消费类电子产品行业,其特点是消费者行为向对价格更加敏感的方向转变,从而对品牌的稳定性和发展前景产生影响,这对消费类电子产品贷款行业产生了重大影响。金融科技贷款机构正在以适应性更强、更具创新性和风险意识的贷款解决方案作为回应,这些解决方案更加贴近消费类电子产品品牌的当前需求,最终重塑了该行业的金融服务格局。

作者:Web Smith

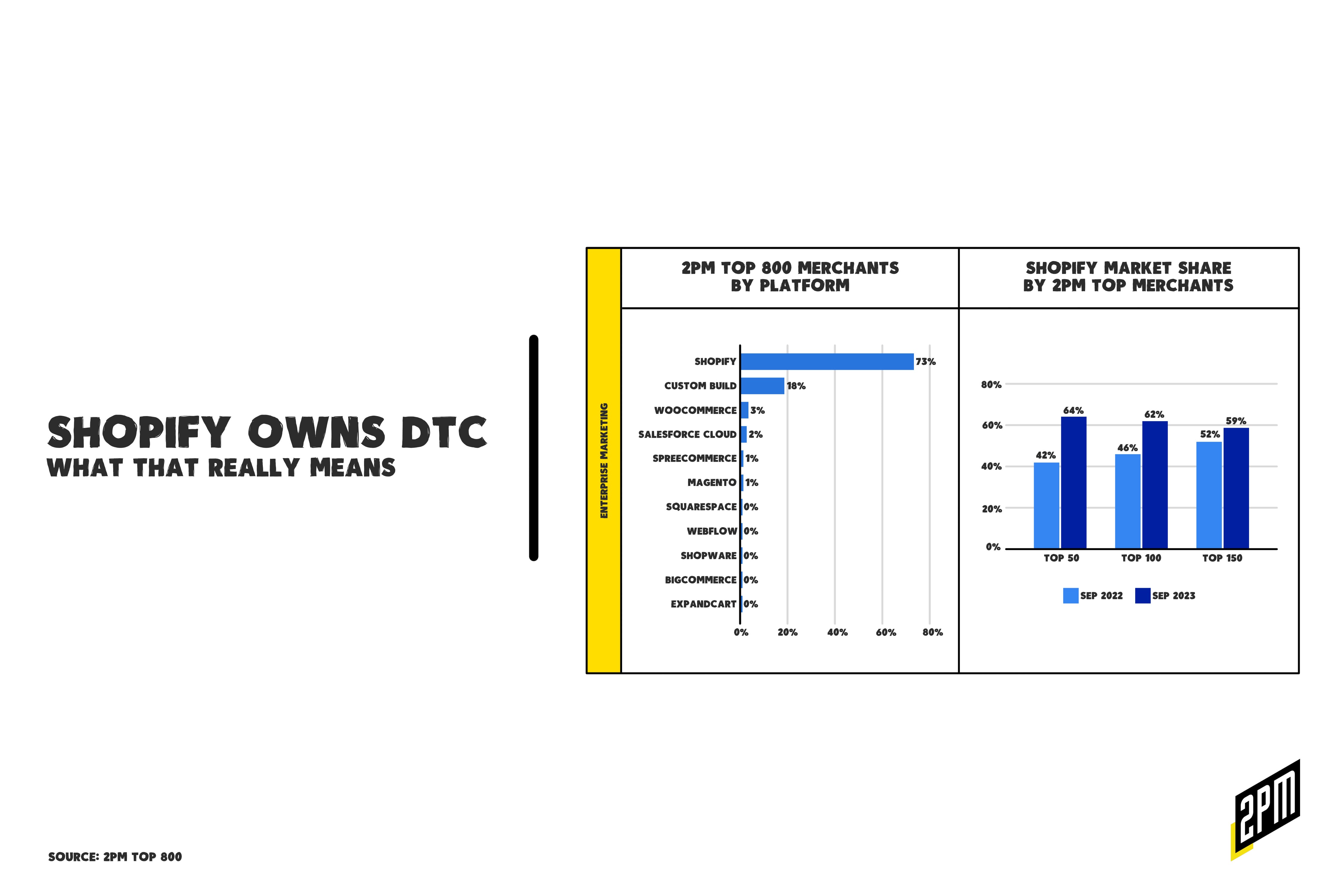

备忘录Shopify 拥有 DTC

But what does that really mean? Increasingly, it’s something different than you may think. Let’s face it: October’s Nike Strength launch was underwhelming. Part of the reason was the site’s basic build on Shopify. That’s no Shopify diss; it’s representative of the state of direct-to-consumer retail.

Not only is Shopify’s year-over-year command of the DTC Power List impressive, it’s also indicative of the changes ahead. We are at the cusp of a transformative era in eCommerce technology, shaped in part by Shopify’s growing market share. Shopify’s ascent is a testimony to its robust platform, offering businesses the tools for seamless online store creation and management. While this surge underscores a democratization of eCommerce, providing both enterprise brands and small merchants with a streamlined path to digital sales, it also prompts a critical analysis of investment strategies in the online retail sector.

The convenience of Shopify’s lower barrier to entry may have inadvertently led to reduced investment in bespoke online retail infrastructures, posing a strategic dilemma as omnichannel retail and digital marketplaces continue to dominate consumer interactions. Examining Nike’s launch of Nike Strength on Shopify or True Classic’s expansion into physical stores, we uncover a complex landscape of opportunities and challenges.

In 2022, True Classic partnered with third-party platform Leap to open five pop-ups in Los Angeles, San Jose, Chicago and Washington, D.C. While the pop-ups will remain open, the company said it is taking its physical retail operations in house, enabling it to outfit its stores with an “elevated, approachable branding that resonates with their consumer.”

For a company of True Classics’ size and velocity, Shopify is a great solution that is relatively low cost and infinitely scalable. It doesn’t get in the way of other plans. Today, more than ever, brands see DTC as part of the strategy and in some cases, it’s the least significant of a multi-pronged approach. What does that look like? One recent example is Mars’s partnership with Uber on a Skittles ad.

Mars is displaying interactive Uber Journey Ads and Post-Check Out Ads to consumers taking a ride in an Uber vehicle or waiting for their Uber Eats order. The ads will enable consumers to seamlessly interact with the Skittles website and add Skittles products to their Uber Eats shopping carts. (CSA)

As marketing channels continue to merge with sales channels, we may see less of an emphasis on traditional marketing funnels (Meta or Google > Shopify.com > checkout) and more content-driven online destinations like the aforementioned Skittles site. But without this level of marketing and sales ambition, this architecture is no longer typical of DTC operations.

The Advantages of Shopify’s Market Share Growth

Lower Barriers to Entry. Shopify has revolutionized the eCommerce industry by making online store setup accessible and cost-effective. This advantage is palpable when observing Nike’s decision to employ Shopify for NikeStrength.com. The move suggests a strategic pivot, wherein agility and time-to-market are prioritized for new ventures. By lowering the technical and financial thresholds, Shopify has enabled countless organizations to partake in the digital economy with maximum agility and minimal investment.

Omnichannel Synergy. True Classic’s retail expansion illustrates Shopify’s potential to enhance the omnichannel experience. Their stores, armed with digital-first technology, are positioned to bridge the gap between online convenience and tactile brand encounters. This synergy is highlighted in a recent Inc. article, noting that brands like Bark and Bala are abandoning a pure DTC model in favor of a hybrid approach that amalgamates physical retail and online channels.

“We don’t consider ourselves a DTC brand,” said Kislevitz, whose company produces Bala Bangles – fitted exercise weights that strap to the body. “I’ve found that there’s a really virtuous ecosystem in an omnichannel approach,” he continued. (Inc.)

The virtuous cycle of in-store and online interaction creates a comprehensive brand ecosystem that can amplify customer reach and loyalty.

Potential Downsides of Shopify’s Dominance

Underinvestment in Online Retail. Despite advantages, there’s an inherent risk that Shopify’s ease of use could foster a minimalist investment approach in online retail infrastructures. Brands might neglect the development of distinctive and innovative online experiences like the one found at Skittles, leading to a market saturated with cookie-cutter stores that lack differentiation. Leaders must recognize that while solutions like Shopify are instrumental in launching online platforms, they are not a panacea for the competitive digital marketplace that demands uniqueness and brand identity. And while many are pursuing omnichannel strategies, when DTC-first strategies become popular again, brands may want more sophistication or individuality.

Omnichannel and Digital Marketplace Competition. The omnichannel model’s evolution calls for a reassessment of the direct-to-consumer approach. As noted in the Inc. article, the economic logic behind bulk shipments versus individual fulfillment cannot be ignored. This realization is prompting DTC players to diversify their sales model. Shopify’s ease might initially attract brands, but the demand for a more diversified, omnichannel strategy soon becomes evident, compelling brands to expand beyond digital-only models.

Case Studies: Nike and True Classic’s Strategic Moves

Nike’s Choice of Shopify. Nike’s foray into Shopify for a specialized product line reflects an agile, project-specific strategy rather than a wholesale platform shift. It illustrates that even established brands see value in leveraging Shopify’s simplicity for certain segments, without committing their entire online presence to it. This decision is strategic, targeting rapid deployment and flexibility over the heavy investment and bespoke customization of their main site.

True Classic’s Brick-and-Mortar Strategy. Contrastingly, True Classic’s physical retail venture, detailed in the Chain Store Age article, signifies a strategic pivot to ‘owned and operated’ locations. This move enables the brand to envelop customers in a controlled, brand-centric environment, supplementing their online presence with a tangible experience. The brand’s commitment to immersive, in-store digital engagement reveals a sophisticated understanding of modern retail dynamics, where the physical is propelled by the digital to propel the business forward.

Founded in 2019, True Classic is now focusing its efforts on rapid expansion of brick and mortar retail, a natural next step to engage their customer in person as well as reach a new audience, the company said.

The contrast here is stark and telling. True Classic leans into the value of customer intimacy that physical stores can cultivate, betting on the allure of in-person experiences to strengthen brand loyalty. Nike, conversely, leverages Shopify’s agility to extend its brand reach without the commitment of extensive infrastructure changes. Both approaches underscore a critical strategic understanding: that the future of retail is not a one-size-fits-all, but a tailored fit to brand identity and customer expectation.

These are two businesses at two different stages; both are using Shopify for contrasting reasons. Shopify’s expanding market share heralds an accessible entry point into the eCommerce realm, yet it simultaneously prompts industry leaders to deliberate on the long-term implications of such a model. The convergence of ease and ubiquity must not deter us from investing in distinct, immersive online and offline brand experiences. It’s incumbent upon us to forge strategies that leverage the strengths of platforms like Shopify while pursuing a holistic omnichannel vision. This dual approach will ensure that we not only thrive in the current marketplace trend but also maintain preparation for its future, one that may segue back to one where brands are proud to be categorized as DTC and run their businesses as such.

作者:Web Smith | 编辑:Hilary Milnes,美术:Alex Remy 和 Christina Williams