DoorDash has an opportunity to power an evolved, local commerce economy where urbanization has taken a back seat to remote work, the homestead is more relevant than ever before, and the “arming of the rebels” has yet to capture the imagination of Main Street businesses. This is bigger than late night takeout: Food delivery is to DoorDash what book sales were to Amazon.

DoorDash has an opportunity to power an evolved, local commerce economy where urbanization has taken a back seat to remote work, the homestead is more relevant than ever before, and the “arming of the rebels” has yet to capture the imagination of Main Street businesses. This is bigger than late night takeout: Food delivery is to DoorDash what book sales were to Amazon.

A singular failure has shaped my understanding of commerce and how digital would influence physical retail. In 2014, eCommerce accounted for just 7.7% of US retail sales, the investment into urbanization had a positive trajectory, and apps like Postmates and DoorDash had begun to eat market share of incumbents like Grubhub. With that backdrop, a close friend and I pieced together a mobile application with a simple marketplace function. It featured an open chat room to guide users through recommendations, sales, and checkout.

The experiment had one goal: To understand if eCommerce could improve the viability of local, analog retail businesses. To do so, we targeted hard goods (not food products). We built atop Uber’s then-available pricing API and enabled independent retailers to market their products within our app and ship products as far as 20 miles outside of the city. Uber’s drivers delivered the goods to their homes.

To accomplish this, we indexed the goods of independent retailers and tracked inventory with a relatively light integration that relied on imported Quickbooks data. And then each product’s corresponding image was pulled into the app through .JSON web calls. Given that the vast majority of featured stores were within a mile of us, contractors were tasked with acquiring the goods and bringing them to a central location to stage for delivery by Uber. The last shipment left by the close of business and inventory was painstakingly updated upon the completion of each business day. In just under a year, the app sold $627,000 in top line sales at an average margin of around 17%.

That’s where the positives ended. The price of doing business with Uber was costly and the fleet of drivers was subpar, causing a number of customer service issues. The demand for hard goods was outpaced by the demand for perishable goods (food). And the area’s physical retail scene was a draw, so most consumers opted to walk, drive, or bike over instead. The app eventually amounted to an expensive experiment in between jobs.

The Difference: Now and Then

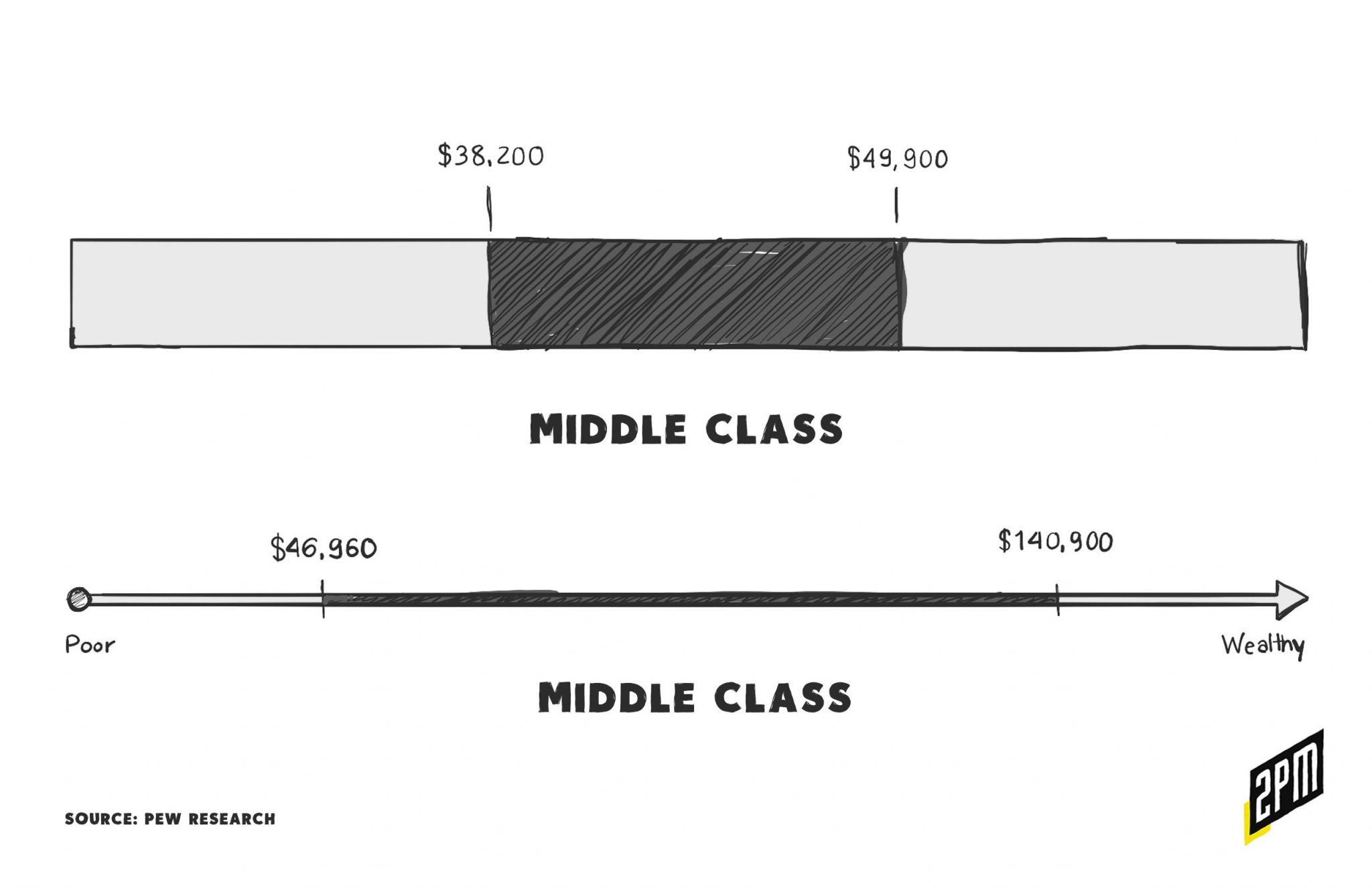

The experiment wasn’t a complete failure, however. By the time that we shut the application down, we’d developed a better understanding of the intersections between real estate, retail, technology, and the limitations of small businesses. I also learned an important lesson about eCommerce adoption: 2014 was far too early. Today, the former 7.7% share of retail (in 2014) sales has tripled. Nearly one of every four dollars is spent online in 2020.

Given that our focus was on non-coastal markets and second-tier cities, the marketplace helped us understand the needs of retailers outside of the country’s main retail hubs: Los Angeles, New York, San Francisco, and so on. The app experience was nowhere near perfect, but the experiment was valuable. I went on to build DTC brands, founding 2PM Inc just a year later. That friend of mine became the founder of Loop Returns.

Fast forward and many of the retailers who once considered eCommerce a distraction have now invested heavily into building online retail as a primary channel. Consider Josh Quinn of Ohio’s Tiger Tree, a multi-million dollar independent retailer and former partner of our app experiment. Quinn recently shuttered Tiger Tree’s doors to pursue an eCommerce-first strategy. He said:

It’s an interesting example of just how fast retail has accelerated in six years. To say I don’t think my customers would have seen the utility in an on-demand delivery solution seems laughable now. But we could have been better positioned. We did so well as brick-and-mortar stores that it kept us from investing the way we should have. It hurts to think of where we’d be if we would have put the time into eCommerce back then.

Quinn is representative of a large swath of retailers who relied upon a brick-and-mortar business before the pandemic. But he won’t make the mistake again. He added: “We are in the middle of local online retail being a thing. Almost half of our eCommerce orders go to the Columbus, Ohio area.”

This is the new economy that DoorDash is primed to capture. The permanence of remote work culture and the restrictions placed on urban dining and nightlife has spawned three separate trends. There is a shift from major cities to smaller ones, urban flight to suburban “cities”, and housing to the all-encompassing homestead.

Sanitized urbanization removes the perceived risks of living in urban areas while adding the value of – what’s often – upgraded infrastructure, improved schools, and lower tax bases. [2PM, 1]

As remote work and distance learning continues to become more commonplace, entertainment, commerce, and utility will shift from physical to digital as well. There has been an extraordinary shift from thinking along the lines of office perks to thinking about optimizing the home. Consider Wayfair’s sudden shift of fortune. In 2017, the furniture reseller traded at a $5 billion market cap. Today it trades at nearly $26 billion, a growth emblematic of a boom in redesigning the home for modern needs: remote work, leisure, and comfort.

If this is any indication of how small business owners will react to these macroeconomic changes, we can expect second and third-order effects in the housing market to continue to materialize.

Inside The Home

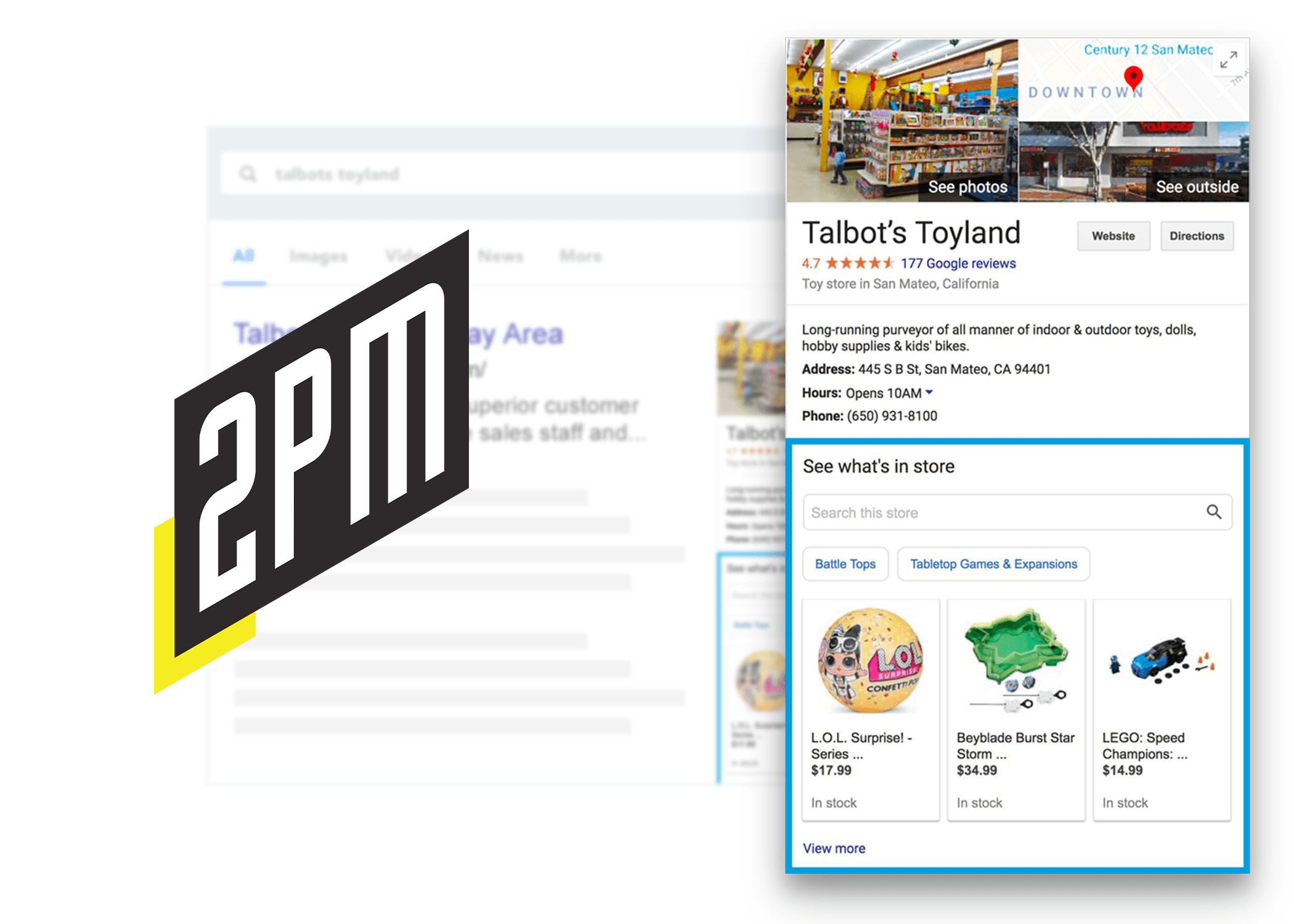

Like Postmates, which has long tested hard goods marketplace capabilities, DoorDash’s opportunity lies with supporting the businesses of independent retailers by providing new opportunity for them. Not just by delivering the goods but by fostering a marketplace that expands their reach to wider, local audiences. By streamlining retailers as sources of goods and developing new initiatives to reach customers, their marketplace partners will be more inclined to view DoorDash as an effective customer acquisition engine.

Success or failure will depend on growth beyond food delivery as the core model. This means that the development of efficient customer acquisition, fair and incentivized pay for its last-mile workforce, and paths to hyper growth in gross merchandising volume are key to the company’s long term viability. Consider this excerpt from a recent analysis on DoorDash:

That inability to change the business model is also likely to keep DoorDash from making any meaningful profit. Grubhub, the only US food delivery service on the stock market, recently complained that food delivery is not enough to build a sustainable and profitable business. [2]

By instituting a local marketplace model, DoorDash would encourage retailers like Quinn who find value in reaching more customers in their cities without relying upon the postal service for delivery. Quinn cited his frustration with existing local shipping models:

Independent retailers like us are facing something of a crisis with USPS shipments being delayed. Not that I am blaming them – I understand the strains on their system.

Amazon Prime has popularized next day and same day delivery. Services like HBO Max have begun to shift resources away from physical theaters and towards home-streaming models. And founded a year before our local commerce experiment, DoorDash is now trading at $55.6 billion. Like Jeff Bezos former marketplace of books, Tony Xu’s marketplace of local retailers is in its infancy. While intended for restaurants, the technology could easily be applied to retailers. And while DoorDash touts partnerships with large and sophisticated companies (Macy’s, etc), the delivery app’s real opportunity lies with locally-owned retailers who’d rely on DoorDash for the technical expertise and the audience to grow their businesses – a model that not even Shopify could compete with right now.

In its short existence, DoorDash has evolved well beyond just delivery logistics, adding services like Storefront, which enables merchants to set up digital ordering directly from their native channels. [3]

We look at apps like DoorDash and see food delivery. Rather, view them as the last-mile enabler for businesses who are leaning into localized eCommerce. Food delivery, alone, will not justify the $50+ billion market cap but a city-by-city network of local retailers may. This is the eCommerce era now. Like every other retailer, DoorDash must learn to create new demand and service it with creative solutions. I suspect that the company’s reach will soon extend beyond your kitchen or your mobile phones. In the near future, the app may function more like a retail operating system.

By Web Smith | Editor: Hilary Milnes | Art: Alex Remy | About 2PM