В связи с планом компании Elliott Management сместить Джека Дорси с поста генерального директора Twitter в этом отчете рассматриваются следующие вопросы: динамизм, корпоративная конгломерация и модель нестандартного мышления, которой могут поучиться новые предприниматели. Twitter не отстает, а опережает свое время.

Защита лидерства Джека Дорси - это защита эрудитов в бизнесе. Публичные рынки вознаградили тот тип глубокой специализации, которого Дорси избегает. Однако эти же рынки начинают отражать падение динамизма американской экономики. В статье, опубликованной в 2012 году в Harvard Business Review, предприниматель Кайл Виенс пишет:

Мы живем в эпоху, когда глубокая специализация очень поощряется - в эпоху того, что технический аналитик Винни Мирчандани называет "мономатом". Врачи специализируются, юристы специализируются, ученые специализируются, механики специализируются... практически все профессионально специализируются. Чем глубже вы специализируетесь, тем больше денег вы, скорее всего, заработаете. И это прекрасно. За исключением тех случаев, когда это не так.[4]

Из ряда источников данных о занятости можно сделать вывод, что Соединенные Штаты приближаются к новому периоду пересмотра рынка труда, хотя глубокая специализация всегда будет характерна для таких профессий, как медицина и научные круги. Способность рассматривать проблему под разными углами, избегая узкого анализа, вновь становится высокой профессиональной ценностью. Полиматия - это черта характера, которая присуща Дорси. Но что еще более важно, его руководство Twitter и Square - один из немногих оставшихся столпов, которые решают проблему сокращения путей к предпринимательству для среднего класса.

Аудитория и коммерция. В ходе ненаучного опроса, проведенного 2PM (n=632, доход на дому: $42 000 - $98 000), из почти тридцати вариантов были выбраны следующие инструменты. Каждый из них был отмечен за свою ценность для предпринимателей среднего класса, находящихся на ранней стадии развития: Twitter (27,1%), Reddit (17,8%), Gumroad (11,1%), Patreon (22,9%), Substack (7,3%), Shopify (31,1%) и Square (29,4%).

Чем более сфокусирована компания, тем больше она ориентирована на предпринимательство на ранних стадиях. Однако за это приходится платить. Критики ставят под сомнение рекламный потенциал Twitter, рост которого достигается за счет конгломерации бизнеса. Академические круги и публичные рынки обычно приходят к выводу, что корпорации, которые по своей природе являются полиматематическими (компании, которые успешно работают в трех или более отраслях), ценятся дороже. На ум приходит целый ряд компаний: AT&T, Facebook, Amazon, Comcast и Google. На протяжении десятилетий этим корпорациям разрешалось работать в новых вертикалях при минимальном государственном надзоре. Корпорация-полиматик - относительно новое явление в американском воображении, но человек-полиматик уже давно не поощряется.

Эпоху конгломерации можно напрямую связать с уменьшением числа стартапов, создаваемых в США. После рейгановского антимонопольного взрыва 1982 года элементы закона начали смещаться от структурализма в сторону благосостояния потребителей. В том же году AT&T и IBM столкнулись с антимонопольными судебными разбирательствами, которые заставили каждую из компаний внести изменения к 1984 году.[1] Этот период в конечном итоге проявился в тех формах, которые только сейчас начинают тщательно изучаться; он привел к новой форме антиконкурентного поведения. Это означало, что появлялись новые компании, которые были уничтожены более быстрыми и капитализированными компаниями, такими как Facebook, Google или Amazon.

Рынок вознаграждает эти компании, и это справедливо: они практически неподвижны. Средства массовой информации хотят, чтобы читатели поверили, что предпринимательство находится на пике популярности. Однако это не так уж далеко от истины. Американская экономика окостеневает. В книге "Самодовольный класс" Тайлер Коуэн пишет:

В наши дни американцы реже меняют работу, реже перемещаются по стране, а в определенный день вообще реже выходят из дома [...] экономика более окостенела, более контролируема и растет более низкими темпами.

Защита Джека Дорси - это напоминание о том, что Twitter - одна из немногих крупных медиаплатформ с небольшим риском антимонопольных действий. Поворот к модели конгломерации, подобной Facebook или Google, - это награда с пресловутым сроком годности. Главный аргумент инвестора-активиста Elliott Management заключается в том, что, в отличие от Facebook или Google с их обширным каталогом аудитории и рекламных продуктов, Twitter не решается на инновации. Я считаю, что это было сделано намеренно.

Инвесторы жалуются на то, что Twitter не может предложить новые инновационные продукты. Хотя его основная социальная сеть остается заметной - она является одним из главных рупоров президента Трампа, - конкуренты-стартапы, включая совсем недавно появившийся TikTok, захватили воображение и глаза публики.[6]

Подумайте о предвыборной кампании, где кандидаты по обе стороны линии разграничения с удовольствием критикуют антиконкурентное поведение. Упоминание современников Twitter - обычное дело. Из платформы сенатора Уоррена[2]:

Крупные американские технологические компании поставляют ценные продукты, но при этом обладают огромной властью над нашей цифровой жизнью. Почти половина всей электронной коммерции проходит через Amazon. Более 70 % всего реферального трафика в Интернете проходит через сайты, принадлежащие или управляемые Google или Facebook.

Специализация против глубокого генерализма

Чтобы получить одну из самых желанных и надежных должностей в Америке, лучше всего скрыть свои многопрофильные интересы. Если бы Джек Дорси не основал компанию, вряд ли его разносторонние интересы заинтересовали бы типичного рекрутера. И это несмотря на превосходный послужной список инженера-программиста.

Эта волна специализации карьеры стала ответом на тенденцию конгломерации отраслей, которая десятилетиями влияла на публичные рынки. Рекрутеры высшего звена отмечали определенные преимущества составления подобных резюме: повышение ценности предложения, сокращение сроков обучения, "восприятие авторитета", более высокая конверсия и превосходный нетворкинг.

Возникновение корпоративного конгломерата совпало с акцентом на специализацию после окончания колледжа - на эту тенденцию повлияли практика найма и гарантии занятости в прибрежных технологических компаниях. Руфус Франк, основатель компании "Консультанты 500", объяснил[3]:

Если взглянуть на список Fortune 1000 за последние 40 лет, начиная с 1973 года, то можно увидеть, что в нем произошли серьезные изменения. К 1983 году треть этих компаний выпала из списка. К 2013 году в списке осталось только 30 % компаний, которые были в нем изначально. Темпы изменений будут нарастать, так как ожидается, что только треть современных крупных компаний переживет следующие 25 лет.

Twitter и Square, похоже, работают иначе, чем многие из вышеупомянутых современников. Созданный в 2006 году Twitter.com (27,32 млрд долларов) произвел революцию в двустороннем общении с публичными людьми, новостях и бизнесе. Для опытных пользователей он стал тем, для чего был создан LinkedIn и чем никогда не сможет стать Facebook. Это платформа, которая ближе всего к глобальному форуму для идей, творчества, исследований и культуры.

Компания Square также совершила революцию в сфере кредитных и наличных операций. Основанная в 2009 году, компания Square (34,77 млрд долларов) добилась многого в сфере коммерции и одноранговых платежей. По оценкам аналитиков, продукт Cash App приносит миллиарды долларов. Эти две компании не приобрели форму современной полимафиозной корпорации (конгломерата). Возможно, потому, что у ее руля стоит один человек.

Спор заключается в том, лучше ли платформам быть сфокусированными, чем расположенными на пути к конгломерации.

...кроме тех случаев, когда это не так

Чем глубже вы специализируетесь, тем больше денег вы, скорее всего, заработаете. И это прекрасно. За исключением тех случаев, когда это не так. До объявления о приобретении компанией Elliott Management акций Twitter на сумму 1 миллиард долларов самый известный критик Дорси был в академических кругах. Когда в декабре 2019 года уважаемый профессор Нью-Йоркского университета Скотт Гэллоуэй написал письмо исполнительному председателю совета директоров Twitter, оно стало призывом к действию для ряда беспокойных инвесторов на публичном рынке и институциональных холдингов. Гэллоуэй начал свое письмо с явным намерением:

Чтобы быть ясным, моя главная цель - замена генерального директора Джека Дорси. Однако оружие массового закрепощения вашей компании включает в себя ступенчатый состав совета директоров, который может заставить акционеров сначала добиваться замены других директоров, включая вас. [....]

Трудно просить людей работать по вечерам и выходным, когда генеральный директор трудится по утрам (работает на полставки). Отток людей привел к анемичной разработке продуктов, что замедлило рост и монетизацию.[5]

По общему признанию, у Дорси мало сравнений с руководителями. Хотя критики и защитники все же пытаются найти аналог его личности: Стив Джобс иногда упоминается. Критики сравнивают худшие черты Дорси с выходками Джобса: отсутствие фокуса, неуравновешенность, склонность к стоицизму и стремление к духовности. Сторонники сравнивают лучшие черты Дорси с чертами Джобса. Чаще всего это сравнение сводится к способности обоих руководителей управлять двумя крупными компаниями одновременно.

В четвертом квартале прошлого года выручка Twitter превысила 1 миллиард долларов, что стало первым показателем для компании. Продажи рекламы в размере 885 миллионов долларов за квартал выросли на 12 процентов по сравнению с тем же периодом 2018 года. А количество пользователей, ежедневно просматривающих рекламу на платформе, выросло на 26 миллионов в 2019 году, что на 21 процент больше, чем в предыдущем году.[9]

Это справедливо: на свете есть только один Стив Джобс, лидер, обладающий талантом управлять Pixar и Apple в тандеме. Джобс основал Pixar, когда его уволили из Apple. Он вернулся в Apple, когда та приобрела NeXT, еще одну компанию, которую Джобс основал и возглавил. Он оставался на руководящей должности в Pixar до тех пор, пока компания не была приобретена Disney в 2006 году. Через год после приобретения Pixar дебютировал iPhone - вдохновляющее устройство, которое нашло новые способы объединить медиа, технологии и торговлю. Но если быть справедливым к Дорси, он успешно управляет двумя компаниями с совокупным рыночным капиталом почти 70 миллиардов долларов и делает это с прицелом на будущее двух развивающихся отраслей: медиа и коммерции.

Призыв к динамизму

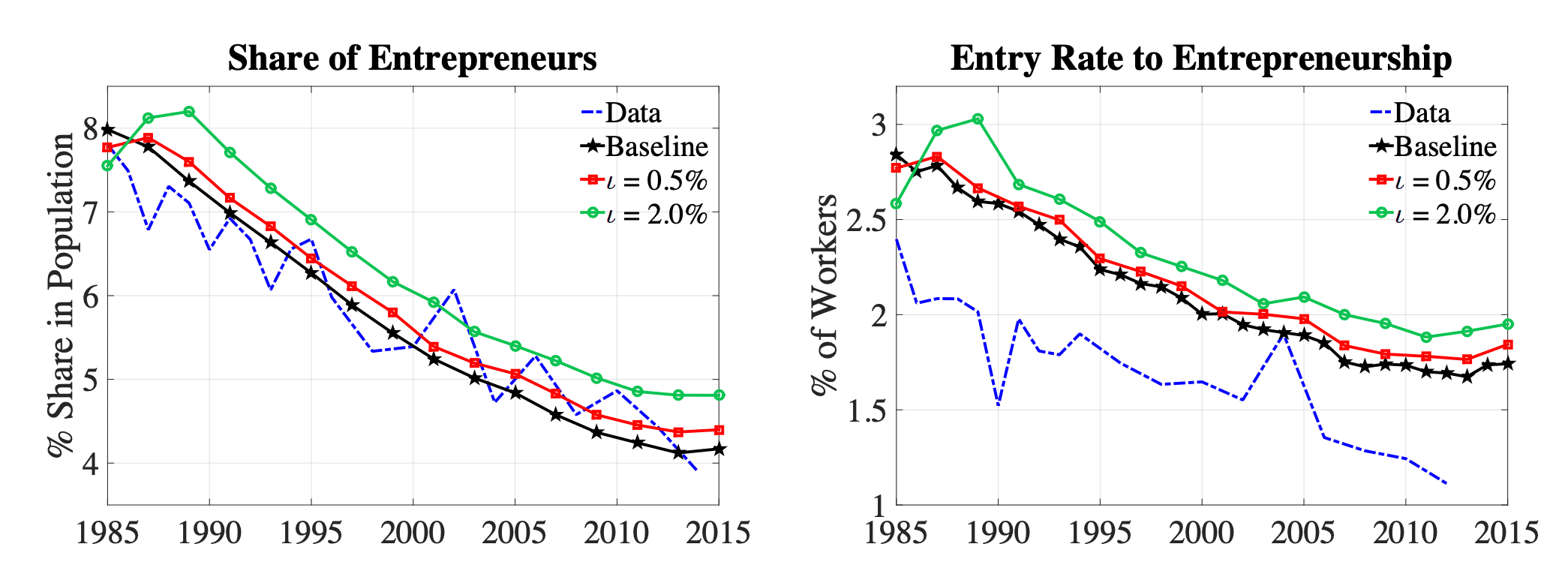

Важнейшим фактором, объясняющим снижение динамики развития бизнеса, является уменьшение числа начинающих предпринимателей и связанное с этим снижение роли динамичных молодых предприятий в экономике. Например, за последние 30 лет доля занятости в США, приходящаяся на молодые фирмы, сократилась почти на 30 %.[7]

Междисциплинарное мышление - общая черта лидеров бизнеса на ранних стадиях. Для решения новых, сложных проблем требуется не только обильное финансирование. Для этого необходимо нестандартное мышление, которое предписывает Дорси и не поощряет конгломерация.

Рынки могут не вознаградить Twitter за его рыночную дисциплину до тех пор, пока такие конгломераты, как Facebook и Google, не начнут приспосабливаться к новым условиям, поскольку правительственные проверки и новые законы о конфиденциальности данных продолжают усиливаться. Законопроекты о конфиденциальности данных разрабатываются по всей территории Соединенных Штатов с невероятной скоростью. Сегодня к этому разговору присоединилось законодательное собрание Нью-Джерси:

Законопроект потребует от компаний получать разрешение от потребителей Нью-Джерси, прежде чем они смогут собирать и продавать личные данные третьим лицам. Законопроект, который будет применяться к таким интернет-компаниям, как Google и Facebook, принадлежащим Alphabet Inc, будет иметь последствия для любой компании, собирающей данные о потребителях.[8]

Поскольку конфиденциальность данных становится все более актуальной, интуитивно понятным становится поворот к коммерции. Мы начинаем видеть это, когда Facebook делает упор на возможности корзины в Instagram или когда Google приобретает компанию Pointy и делает упор на развитие рынка. Представьте себе, если бы у Twitter был генеральный директор, обладающий практическими знаниями в обеих этих дисциплинах. Уволил бы его совет директоров?

Заключение

Twitter удалось избежать ряда препятствий, с которыми сегодня сталкиваются ведущие корпоративные конгломераты: (1) переход СМИ от рекламных данных к транзакционным данным (2) антимонопольный контроль за конгломератами (3) растущий хор проблем, связанных с политикой в области данных. Именно нестандартное мышление Дорси может сослужить хорошую службу его компаниям в условиях продолжающегося перехода к линейной коммерции.

Square и Twitter представляют две отрасли (медиа и коммерция), которые развиваются, не ущемляя другие вертикали. Но что еще более важно, обе компании представляют собой своего рода демократизацию предпринимательства, которая необходима для того, чтобы динамизм вновь заявил о себе. Короче говоря, это два последних оставшихся инструмента для предпринимателей ранних стадий.

С технической точки зрения Square может оказаться полезной для Twitter в деле налаживания партнерских отношений с брендами, поскольку платформы переосмысливают рекламу в условиях экономики данных, основанной на конфиденциальности. Вместе с Дорси у Twitter больше всего шансов стать первопроходцем. Но привлекательность Дорси для возрождения динамизма основана не только на двух компаниях, которые он возглавляет. Он - редкий основатель-генеральный директор, который не защищен классами голосующих акций, что является еще одной эмблемой сегодняшней конгломерации, не связанной с риском. Скорее, его стиль руководства хорошо подходит для начинающих предпринимателей, стремящихся сделать карьеру вне рамок профессиональной специализации. Я считаю, что это предвестник возрождения динамизма.

Стиль руководства Дорси необходим на современных публичных рынках. И для этого может потребоваться терпимость публичного рынка к его стилю междисциплинарного мышления и лидерства. Безусловно, потрясающая команда Elliott Management может прийти к аналогичному выводу после рассмотрения более широких данных. Но, по общему мнению, Дорси, возможно, наконец-то понадобится свой собственный джобсовский момент, чтобы заставить замолчать критиков и успокоить сторонников.

Доклад Веба Смита | Около 2 часов дня