This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.

NATSEC Roundtable No. 10: The Forges Went Dark

Years ago, when Mizzen+Main was still a young brand trying to prove that performance fabric had a place in the dress shirt category, I made an argument that nobody wanted to hear: keep the manufacturing in America. Not because of patriotism in the greeting-card sense, but because of what domestic production would have enabled over time. Mizzen+Main had something unusual for a direct-to-consumer brand at that stage of its life. The product had coastal cues, the kind of clean technical construction that reads well on a dock and equally well in a briefing room. It had military adjacency in its aesthetic DNA without ever having claimed it explicitly. The fabrics performed under stress. The fit was disciplined. There was a customer profile hiding inside that brand that went well beyond the weekend golfer and the startup founder who wanted to look put-together on a Zoom call.

The argument I was making, even if I wasn’t articulating it in these terms at the time, was that Mizzen+Main had the early profile of a dual-use textile company. Not a contractor; not a uniform supplier. Something more interesting than either of those things: a civilian brand with the product credibility to serve both markets without compromising the identity that made it matter to consumers in the first place. The manufacturing stayed offshore. The brand grew, was acquired, and became a solid mid-market performance apparel business. The other version of the story, the one where domestic production and defense-adjacent positioning compound over a decade into something that looks more like a platform than a brand, never happened. I don’t think anyone regrets the decision they made. I do think the window they missed is worth understanding.

What the Chart Actually Shows

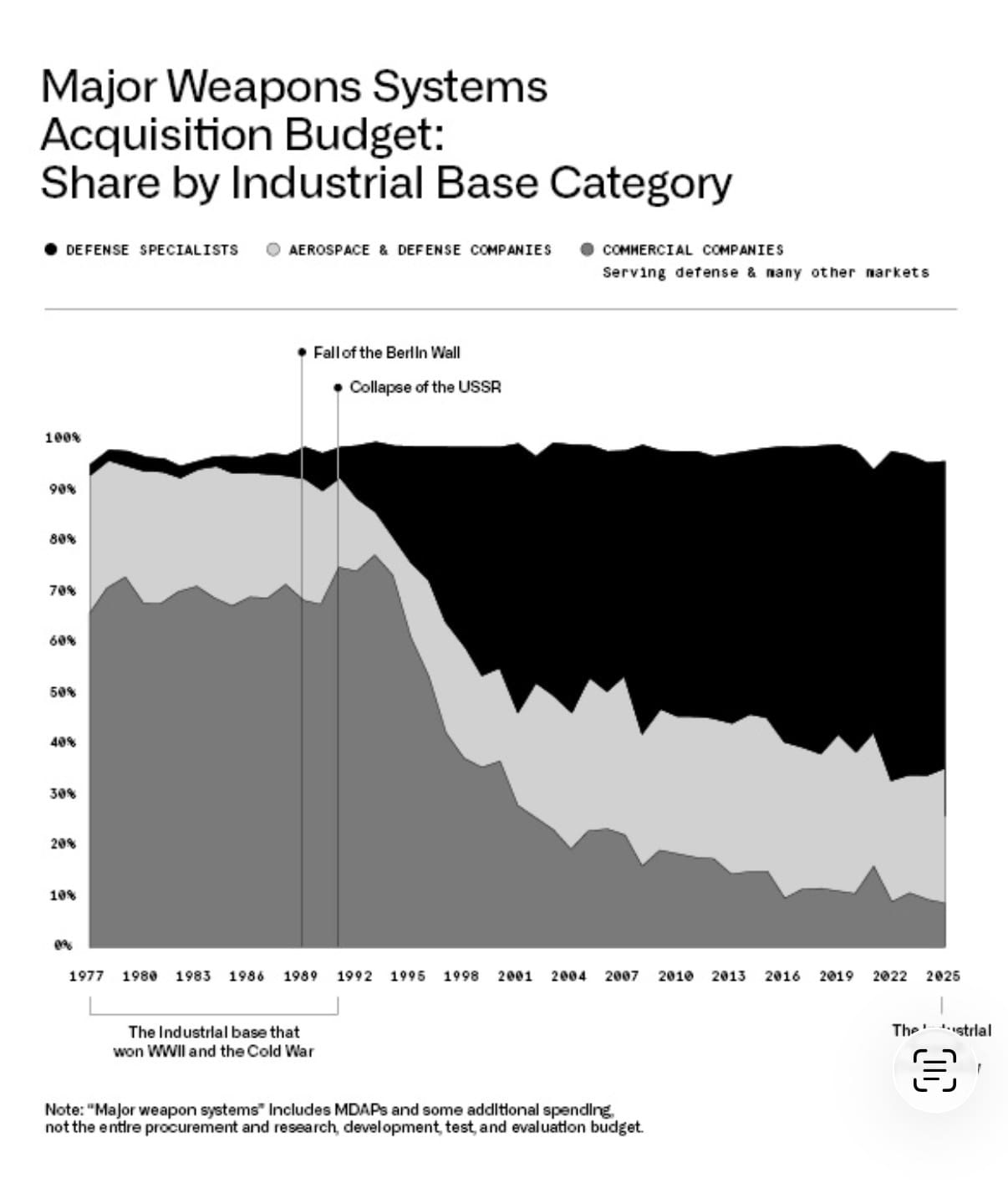

Shyam Sankar and Madeline Hart published Mobilize this month, and the Palantir CTO’s argument is not subtle. The book is a call to resurrect the American industrial base before the structural consequences of its decay become irreversible. The chart that anchors the book’s diagnosis shows the Major Weapons Systems Acquisition Budget broken down by industrial base category from 1977 to 2025, and what it reveals is one of the most consequential and least discussed shifts in American economic history.

In 1977, commercial companies, companies serving defense and many other markets simultaneously, represented the largest single category of weapons systems acquisition spending. These were companies like Chrysler, which built tanks. General Mills, which built naval fire control systems. Ford, which built aircraft engines. The industrial base that won World War II and the Cold War was not a specialized defense economy. It was the American commercial economy, partially redirected. The capacity that defeated the Axis powers was the same capacity that built automobiles and refrigerators and breakfast cereal. The defense budget flowed through companies that also competed in consumer markets, which meant their manufacturing processes, their supply chains, and their engineering talent were being continuously sharpened by commercial competition.

Then the Berlin Wall fell and the USSR collapsed, and the procurement world made a decision that seemed rational in the moment and has proven disastrous in hindsight. Defense spending consolidated into a smaller number of specialized contractors; I lived that too. As the Cold War came to a halt with the fall of the USSR, my father left Texas Instruments’ missile defense practice for greener pastures at Time Warner Communications. TI sold its practice to Raytheon, four years later, for $2.9 billion in cash. For an ex-military officer turned defense contractor, he segued pretty well for the time. Commercial companies exited the defense market because the margins didn’t justify the compliance costs and the procurement timelines didn’t suit commercial operating rhythms. By the 2000s, the commercial company share of the acquisition budget had fallen to a fraction of what it had been, replaced almost entirely by defense specialists and aerospace and defense companies whose entire business model was organized around government contracting. The industrial base that had once been synonymous with American economic vitality became a separate and increasingly fragile ecosystem.

Sankar and Hart’s argument is that this separation is the source of nearly every current American defense capability problem. The Pentagon now buys from companies that have no commercial discipline, no competitive pressure, and no incentive to innovate faster than the contract requires. The companies that might bring speed and manufacturing competence to defense problems have largely opted out because the procurement system was designed to exclude them. The result is the chart: a graph whose shape tells the story of American industrial decline more clearly than any policy paper or congressional hearing.

The Dual-Use Premise

The concept that Sankar and Hart are trying to recover is not new. It is, in fact, the original operating model of American industrial power. What made the United States capable of outproducing every adversary in the twentieth century was not a defense industry in the modern sense of that term. It was a manufacturing economy that could be mobilized because its capabilities were genuinely general-purpose. A factory that makes automobiles can, with the right conversion effort, make tanks. A company that supplies textile mills can, with the right contracts and specifications, supply the military. A logistics network built to move consumer goods can, under pressure, move war materiel. The dual-use company is not a strategic novelty. It is what American industry looked like when America was winning.

What has changed is that the procurement system spent thirty years actively discouraging commercial companies from participating in defense markets, through compliance requirements, contracting structures, and classification barriers that made the cost of entry prohibitive for any company that had a viable alternative. The companies that might have stayed in the market left. The companies that entered the market after that period were purpose-built for government contracting, which meant they were optimized for compliance rather than performance and for contract retention rather than innovation. The defense industrial base became a walled garden, and the plants went quiet, and China spent those thirty years building the manufacturing capacity that the United States was methodically dismantling.

Anatar and What Domestic Manufacturing Looks Like Now

Anatar is an American apparel manufacturing company building automated domestic production capacity through its Loom OS platform, an AI-orchestrated system that manages production planning, dynamic line routing, and downstream demand sensing from a single integrated software layer. The company’s Georgia manufacturing facility will be among the first domestic apparel plants built around autonomous production at commercial scale.

What makes Anatar worth discussing in the context of Mobilize is not the eCommerce angle. It is the defense relationship that has been there from the beginning without being the headline. Anatar is an approved member of the Advanced Robotics for Manufacturing Institute, a Manufacturing Innovation Institute funded directly by the Office of the Secretary of Defense. It is also a member of the Revolutionary Fibers and Textiles Consortium, another Department of Defense Manufacturing Innovation Institute. These are not marketing relationships. They are structural integrations into the defense manufacturing innovation ecosystem, which means Anatar’s technology is being developed in the same environment, against the same standards, and in conversation with the same institutional stakeholders as the military textile supply chain.

This is what a dual-use company looks like in 2026. It is not a defense contractor that makes civilian products on the side. It is a commercial manufacturing company that has built its technical infrastructure inside the defense innovation ecosystem from the beginning, which means that when the procurement system eventually opens up to the kind of agile domestic manufacturers that Sankar and Hart are arguing for, Anatar will already be there. The capability is commercial. The relationships are governmental. The manufacturing platform serves both markets without being compromised by either.

The version of Mizzen+Main I was imagining in those early conversations was something along these lines, even if the path from performance dress shirts to a defense textile supplier requires a longer argument than most brand founders are willing to make. The aesthetic profile was right. The product performance was right. The only missing element was the domestic manufacturing decision that would have created the infrastructure for the rest of it to follow.

Ten Already Building the Dual-Use Industrial Base

The list I want to make is not about brand aesthetics or defense-adjacent positioning. It is about companies sitting inside the Ohio-Indiana-Michigan-Pennsylvania manufacturing corridor that are already producing the kind of output, or already developing the kind of platform, that a reformed procurement system should be routing contracts through. These are not aspirational candidates. Most of them are already there in some form. What they need is not encouragement. They need the procurement barrier removed.

Rogue Fitness consumed 26 million pounds of steel in a single year at its 800,000-square-foot factory on East Fifth Avenue in Columbus, along with 14 million feet of welding wire. The company already sells equipment to military units, collegiate programs, and the professional sports teams whose athletes feed into the services. The manufacturing process that produces a barbell to tolerance is the same process that produces precision steel components for any program that needs them. Rogue is not a defense company. It is an Ohio steel fabricator with a consumer brand attached, and that distinction is the entire point.

Path Robotics is a Columbus startup that has trained its Obsidian AI model on tens of millions of welded inches and deployed autonomous welding cells into fabrication shops across the country. In February 2026, Path signed an MOU with HII, the nation’s largest military shipbuilder, to bring autonomous welding to naval shipyards, and separately announced a deployment with Saronic, the autonomous vessel builder, in Louisiana. The intelligence behind those systems, the vision models, the machine learning architecture, the software stack, is an Ohio product built in Columbus. Path is not aspiring to defense relevance. It is already there, and the procurement system has barely noticed.

Vertiv, headquartered in Westerville and manufacturing in Delaware and Ironton, Ohio, announced in late March 2026 a $50 million expansion of its Ohio facilities adding up to 730 new jobs through 2029. The company builds the power management, thermal management, and critical digital infrastructure that keeps data centers running without interruption. That is also what keeps a command and control facility operational under pressure, what keeps a forward operating base’s communications infrastructure alive, what keeps any mission-critical computing environment running when the grid is contested. Vertiv became a Fortune 500 company in 2026 and its technology is already embedded in defense-adjacent infrastructure worldwide. The formal relationship to the procurement system is the only thing missing.

French Oil Mill Machinery has been building hydraulic presses in Piqua, Ohio, since 1900. The company already lists aerospace, military, and defense as a primary market on its website. Its custom hydraulic presses are used in composite manufacturing, rubber molding, and lamination processes that appear throughout the defense supply chain, from aircraft components to armor systems. French Oil is the company on this list that most clearly illustrates what the chart is measuring: a commercial manufacturer with over a century of domestic production that has always served both markets, quietly, without the procurement system building the kind of formal relationship that would make that capability visible and scalable.

Lincoln Electric, headquartered in Cleveland, is the world’s largest manufacturer of welding products and a company whose equipment is already in every serious fabrication shop in the country, including the ones building defense hardware. The dual-use argument for Lincoln Electric is straightforward: the company that makes the machines that weld the components is upstream of every manufacturing program in the defense supply chain. Lincoln Electric’s commercial relationships with fabricators and its technology development roadmap, including automation and AI-assisted welding, position it as a platform company for the industrial mobilization that Sankar and Hart are describing.

Cummins, based in Columbus, Indiana, manufactures diesel and alternative fuel engines that power commercial vehicles, construction equipment, and generators worldwide. They also power military vehicles, generators in forward operating bases, and the logistics infrastructure that keeps any sustained operation functional. Cummins already has defense relationships through its commercial engine business. The question the procurement reform agenda should be asking is not whether Cummins can serve defense programs. It is why those relationships are not more formal, more durable, and more strategically structured.

Parker Hannifin, headquartered in Cleveland, makes the motion and control technologies that appear in aircraft, satellites, defense systems, and the industrial equipment that builds all of the above. Parker’s commercial business is already deeply integrated with aerospace and defense through its product portfolio, and the company has formal defense programs. It belongs on this list not as an aspirational candidate but as a demonstration of what a mature dual-use industrial company looks like, and as a standard against which the others here should be measured.

Kennametal, based outside Pittsburgh, makes cutting tools, tooling systems, and engineered components from tungsten carbide and other advanced materials. Its products are used in machining operations that produce defense hardware, aerospace components, and precision manufactured parts across the industrial base. Kennametal is the kind of company that the chart is mourning the loss of: a materials science company with deep manufacturing expertise whose commercial and defense customers require the same underlying capability.

Dana Incorporated, headquartered in Maumee, Ohio, makes drivetrain and sealing products for commercial vehicles, off-highway equipment, and industrial applications. The same components that Dana engineers for heavy commercial trucks also appear in military vehicle programs, because the underlying engineering problem is identical: transmitting power reliably under load, in harsh conditions, without failure. Dana already has defense programs. The barrier to deeper integration is not capability. It is the procurement structure that treats commercial and defense supply chains as separate systems when the twentieth century proved they function best as one.

Whirlpool, based in Benton Harbor, Michigan, is the largest appliance manufacturer in the country, with domestic production and a supply chain built for volume. The dual-use case for Whirlpool is not about appliances. It is about the fact that a company capable of producing millions of precision-engineered units per year from domestic factories has the manufacturing management systems, the quality control infrastructure, and the workforce scale that a mobilization scenario requires. General Mills did not win World War II by making cereal for the Army. It won by demonstrating that its production capacity and manufacturing discipline could be redirected. Whirlpool is the closest contemporary equivalent in the consumer goods space.

A Direct Address

I have been covering the intersection of consumer commerce and defense technology at 2PM long enough to watch the conversation move from the margins to the center. I see which centers consume the data and insights, from the Pentagon to the main lands of our adversaries. I often write with this in mind. Both the good guys and the bad guys have access to the same analyses and opinions in the modern day, and the ideas in this essay will travel accordingly.

For those in positions to act on the reform agenda that Mobilize describes, the commercial brand world is a more capable and more willing partner than the current procurement structure has allowed it to be. The brands on the list above are not waiting for a government relationship to validate their product quality. They have already proven it in commercial markets that are harder to fool than government procurement, because commercial customers can leave and defense customers historically have not been able to. What these brands need is not subsidy or preference. They need procurement barriers removed, compliance costs reduced to something proportionate to a commercial company’s operating model, and contracting timelines that do not require a company to wait three years to find out whether the relationship was worth pursuing.

Sankar and Hart end Mobilize with a call for people and ideas before hardware, which is the correct sequencing. The people building dual-use companies today, the Kaia Rhodes building Anatar inside DoD manufacturing institutes, the founders choosing domestic production when offshore would be cheaper, the brand operators applying military-grade performance standards to civilian products, are the industrial base that the reform agenda needs. The question is whether the procurement system can move fast enough to meet them before they conclude that the commercial market alone is a sufficient reason to exist.

The forges went dark because the system made it rational to let them. The system is being reformed. What happens next depends on whether the reform is fast enough to matter and ambitious enough to actually reintegrate the commercial and defense economies that the twentieth century proved were stronger together. The brands are ready. The manufacturing talent is available. The technical infrastructure is being built, in Georgia, in Oregon, in Maine and Massachusetts, by people who did not wait for a procurement officer to tell them it was worth doing.

Research and Writing by Web Smith

Web Smith is an outside consultant, the founder of 2PM, and the Chief Revenue Officer at MTN Haus, a Shopify Premier Partner agency specializing in complex commerce systems. The 2PM NATSEC briefing series covers the intersection of defense technology and commercial brand strategy.

Deep Dive: No Brand’s Demo

Over the past several months, a few in the running community have reached out to invite me onto podcasts to discuss a goal that I have begun to make public. The goal is to reach day 1,108 of running a 10K or longer. The streak began to celebrate a reconstructed knee that recovered faster than expected. The hosts are serious athletes with serious audiences, and I appreciate every invitation but it’s not going to happen. I am not their demo. I don’t talk about running the way runners talk about running. I don’t track PRs or carry a racing calendar or optimize for a result that I’m building toward. What I am doing, if I’m honest about it, is running a data collection operation that happens to require putting on shoes every morning.

What 786 days of 7-12 miles and 58+ mile weeks will produce is not a running identity but it does produce a dataset. Every morning, regardless of conditions or how the body feels or what the week looks like, I cover the distance. That constraint has stripped away almost every variable that recreational and competitive runners use to make product decisions. I don’t choose gear based on what I’m training for because I’m always training for the same thing, which is tomorrow. I choose it based on what survives, what doesn’t fail me at mile four of a mandatory six point one, and what I’m still reaching for after two-plus years of daily use rather than replacing. That has made me a strange and occasionally useful observer of a category that most product reviews address from exactly the wrong angle.

The running apparel market writes for people who are excited about running, which is understandable because that’s the majority of the market. I am someone who does it without exception and without excitement being a prerequisite, which means the gear that performs under my conditions is not the same gear that performs best in a review written by someone running four days a week with full recovery between sessions. Those are genuinely different use cases, and the category has not caught up to that distinction.

I Support These Brands. They Don’t Dress Me.

Before we get to the data, there are some things worth saying plainly. I believe in what Bandit is building. Their Unsponsored Project, which I covered in the July 2024 memo on Nike versus the boutique field, remains one of the most coherent community-building strategies in the running market, and the fact that they are genuinely open to product feedback in a way that larger brands are structurally incapable of being makes them interesting to watch. But the brand is built for a specific runner: the young, skinny, urban competitor or the track culture participant or the person for whom running is also a social statement. I admire the brand and I cannot wear it without feeling like I’m performing a version of running I don’t actually practice, which is a more interesting diagnosis than simply saying it doesn’t fit right.

Satisfy is the most aesthetically rigorous running apparel brand in the world right now, and the product is extraordinary in ways that are difficult to overstate if you’ve spent real time in it. The brand DNA is running culture filtered through Paris, which gives it something that no American brand has successfully manufactured: the feeling that performance and beauty are making the same argument. I first identified Satisfy in the February 2023 brief on Euro DTC brands invading the American market, and everything that piece predicted about their trajectory has proven correct since. The half tights I tested are the best half tights I have worn. And still, Satisfy doesn’t make apparel for a 6’1″ 215 lb person whose primary question is whether the pocket architecture survives 50-plus days of daily use before showing fatigue. Their customer is a specific kind of serious runner, and I am a different kind.

Lululemon is indestructible, and I want to be precise about what I mean by that because it is not a compliment and it is not exactly a criticism either. It is a product specification. There is no identity inside the product for a running purist, no sense that the brand understands what running actually is versus what running looks like when observed from outside the sport. The gear survives conditions that compromise most of the competition. The brand cannot tell you why any of it matters.

Tracksmith is the most interesting broken thing in the market at the moment. In the 2024 Nike memo, I described their strength as the celebration of the amateur spirit of running and the cultural and historical aspects of the sport, and that framing was accurate at the time. In 2026, what I see is a brand navigating a corporatized no-man’s land: they have scaled far enough beyond the boutique credibility that made them matter without achieving the distribution strength that would make them a genuine challenger to the primes. Being between identities is the most dangerous place for a brand to stand, and Tracksmith is standing there right now.

Wolaco and Represent make products, and there is nothing wrong with the products. But there is a structural difference between a product company and a brand company, and that difference is the entire ballgame when the market begins to consolidate. A product company gets acquired for its manufacturing relationships or its customer file. A brand company gets acquired for its identity, which commands meaningfully different multiples. Both of those brands are in the product category, and that limits what the ceiling looks like.

The Half Tights Test

I have ran the same 10K-plus routes in half tights from brands across sixty days of use each. I was not looking for what felt best on the first wear because first wears are irrelevant to my use case. I was looking for what held up under daily pressure, what I reached for first on the worst weather days, and where I could see the brand communicating something beyond the category minimum of a compression garment that doesn’t fall down. The four independent brands I added alongside the better-known names were Janji, Soar Running, Rabbit, and Wolaco, each of which had shown up in my research in some form and warranted a real evaluation.

| Brand | Fit & Compression | Durability | Pocket Architecture | Fabric at 60+ Days | Brand Identity | Feedback Openness | High-Mileage Suitability |

|---|---|---|---|---|---|---|---|

| Satisfy | Excellent | Good | Strong (rear zip secure) | Minimal fade | Strong / coherent | Limited (by design) | High |

| Lululemon | Good | Exceptional | Adequate | No degradation | Weak for running purists | Low | High (durability driven) |

| Bandit | Very Good | Good | Adequate | Moderate fade at seams | Strong / community-coded | Excellent | Moderate |

| Tracksmith | Very Good | Good | Adequate | Minor pilling | Drifting / uncertain | Low | Moderate |

| Wolaco | Good | Very Good | Strong (phone pocket) | Minimal degradation | Thin / product-first | Low | High (functional) |

| 24/7 | Good | Good | Adequate | Some stretch loss | Very thin | Low | Moderate |

| Janji | Good | Good | Adequate | Moderate fade | Mission-forward, light | High | Moderate |

| Soar Running | Excellent | Good | Strong | Minimal fade | Strong / European | Limited (accessibility) | High |

| Rabbit | Good | Very Good | Adequate | Minimal fade | Soft / undefined | Moderate | Moderate |

Satisfy won the test, and not because of any single variable but because no single variable failed across the full testing window. The rear zip pocket holds a key and a card without moving during the run. The fabric compression stays consistent from mile one to mile six rather than starting firm and relaxing into looseness somewhere in the middle. The aesthetic reads as craft rather than marketing, which sounds like an intangible thing to score but reveals itself clearly over sixty days of daily use when you’re making the same choice every morning without thinking about it. The brand is communicating something with the product.

The Lululemon result needs more context because there is a real engineering achievement inside that garment. The fabric does not degrade under conditions that compromise most of what else is on this list, and if what you need is half tights that will outlast your interest in the category, Lululemon is the honest answer. The brand just cannot tell you why the running matters.

Soar Running was the genuine surprise of the test. The product competes directly with Satisfy on fabric quality and compression consistency, with slightly stronger upper-leg coverage for longer efforts than the Satisfy entry point. The limitation is distribution: a brand built in Hackney, London, with limited American retail access, is structurally constrained in its ability to reach the American market at the scale that an acquisition conversation requires. That constraint is temporary and addressable, and it is not a brand problem.

Of the ten brands in the test, Bandit’s half tights fit the best and look the best, and on certain colorways I felt more put-together walking out the door than I did in anything else I tested. There is a cut and a confidence in how they sit on the body that the other brands in this price range are not achieving. The membership structure made replacement frictionless when the seams began to show wear: a few clicks, a new pair, no friction. That is a real thing to get right and most brands don’t. But none of that changes the core diagnosis. The fault is not in their product. I am simply not the person they are making it for, and the brand is honest enough in its identity that it never pretended otherwise.

The Acquisition Thesis

The February 2023 piece on Euro DTC running brands made the argument that the European independents were the rightful heirs of the running revolution and that Nike and the established primes were on notice. Two years later, with On Running posting 40 percent year-over-year growth and Satisfy entering footwear with a stated long-term commitment, the question has shifted from whether these brands are a threat to which one gets acquired, by whom, and for what price.

The acquisition logic operates along two vectors. The first is performance legitimacy: a prime brand whose running credibility is under pressure needs a boutique brand that has earned what the prime is trying to buy back through marketing spend alone. The second is demographic access: boutique running brands carry the most loyal and highest-converting customer files in the category, and those files represent exactly the enthusiast tier that precedes mass-market adoption. Both vectors are real and they favor different targets.

Satisfy is the most acquisition-ready brand in the field on brand identity coherence, and the case is not complicated. The aesthetic is fully formed. The customer is loyal and high-spending. The international footprint, headquartered in Paris with growing global distribution, is a geographic diversification argument for any American acquirer evaluating the conversation. The footwear entry in 2025 demonstrates ambition beyond apparel, which makes the business case larger than the apparel alone. The most logical acquirer is ASICS, which needs a premium culture brand to sit alongside its strong technical product story and has historically underinvested in brand identity relative to the product quality it actually delivers. An ASICS-Satisfy combination gives ASICS the running apparel credibility it has never been able to build internally while giving Satisfy the manufacturing and distribution infrastructure it needs to scale without compromising the retail strategy that makes the brand what it is.

Bandit is the most compelling acquisition target for Nike specifically, and the reason goes back to what made Bandit interesting in the first place. The Unsponsored Project was the most articulate critique of Nike’s athlete relationship strategy to come from a brand that could have been a Nike vehicle and chose not to be. Nike’s current turnaround under Elliott Hill is explicitly structured around returning to performance credibility and rebuilding trust with serious runners, and acquiring Bandit would give Nike a legitimate community platform inside the urban competitive running culture that the brand has spent years trying to re-enter through campaign spending rather than through actual belonging. The risk is that the acquisition destroys the thing that makes Bandit worth acquiring, since independence is the product. Nike would need to operate it as a genuine house-of-brands subsidiary rather than absorbing it into the Nike identity, and whether the current management has the discipline to do that is a legitimately open question.

Soar Running is the sleeper in this conversation. The brand has the strongest per-garment product story in the European independent field, a premium positioning that has never been diluted by mass-market distribution decisions, and a cultural adjacency to the serious British and European running community that gives it credibility the American primes cannot easily manufacture. Brooks is growing strongly in Asia and needs a credible premium apparel story to match the footwear positioning it has spent years building. A Brooks-Soar combination would be the most defensible on brand coherence grounds: both brands are genuinely serious about running, both are uncommercial in their positioning, and both are underselling their product quality relative to the performance they actually deliver.

Tracksmith is the most complicated case in the field. The identity that made them matter, amateur running culture as a worthy and beautiful pursuit, is the correct identity for the current market moment. The execution drift of the past two years has opened a gap between what the brand stands for and how the business has been running, and that gap is a problem for an independent operator while being an opportunity for an acquirer patient enough to let the brand recover its coherence. Adidas, returning to running credibility in North America from essentially zero base, could use Tracksmith as a premium American running culture anchor in the same way Adidas has historically used acquisitions to establish category credibility before scaling into it. The timing is wrong for that conversation right now. In twelve to eighteen months, if Tracksmith has not closed the identity gap on its own, the price becomes attractive enough that the strategic math changes for someone.

What the Streak Taught Me About the Category

Running for 786 consecutive days, with a goal of 1,108, has not made me a runner in the way the running community defines runners. I have run a few marathons, and yes, I have an ultra and a half Ironman coming up. I will not enjoy them. I hate running. I run because the discipline of an unbroken streak is more interesting to me as a data-generating constraint than running is as a sport, and that posture makes me a poor ambassador for any running brand while making me an unusually objective consumer of all of them.

What that objectivity looks like in practice is this: I have run through injury and through the kind of motivational malaise that doesn’t come with a dramatic story, just the quiet weight of not wanting to go and going anyway. I have gained discipline I didn’t ask for and data I didn’t know I needed. I have run in cities that understand running and in a state where the running stores feel like approximations of running stores, doing their best with what the market gives them. I have been inside Nashville’s Exchange and Austin’s Loop and a dozen others that do the thing correctly, that make you feel like the sport has a culture worth dressing for. None of those stores are near where I live. None of those brands are making things for me anyway.

I am never going to be skinny. I am never going to be Parisian. Brooklyn is not my context and New England is behind me. The brands that occupy the top of this category were built with a specific person in mind, and I am not that person, and that is fine, except that I am also not the only one. There are a lot of people covering serious mileage in places where the aesthetic reference points of boutique running culture feel like dispatches from somewhere else entirely, people who keep showing up every morning not because running gives them an identity but because the streak is the point and the discipline is the product. The data I have accumulated across 786 days, many brands, and thousands of miles tells me one thing clearly: that person does not have a brand yet. The void is real. One will fill it; the miles will still be there when they do.

Research, Running, and Writing by Web Smith