Let’s face it: the subscription model is hurting. This is a problem, especially for food-based brands. Now add inflation and other cost of living increases and you have a recipe for increased churn, poor sales efficacy, and a less-than-optimal marketing operation. Here are several of the common issues facing the subscription box model for foodstuffs:

Niche market limitation: This company targets a specific market segment interested in a premium product. This focus, while beneficial for brand identity and customer loyalty, may limit its market reach. Expanding its appeal without diluting its brand could be a challenge.

Perceived value versus cost: The cost of subscribing might be perceived as high by some potential customers, especially when compared to buying a similar product from local supermarkets. Communicating the value and justification for the price difference is crucial.

Subscription fatigue: As mentioned in the context of subscription model fatigue, consumers are increasingly wary of accumulating too many subscription services. Food delivery services is likely at the bottom of the priority list when compared to services like: internet, streaming networks, and lower-cost niche media.

Customer retention: Keeping customers engaged and subscribed over the long term can be challenging. Subscription box companies need to continuously find innovative ways to add value to its subscriptions, such as introducing new products, offering flexible subscription plans, or providing unique recipes.

Geographic limitations: Face it, food delivery services cannot go international. And even more critical, there are challenges in maintaining product quality during shipping to certain areas. This could hinder market expansion and customer satisfaction. Ensuring consistent quality and expanding logistical capabilities are key.

Failure to respond to consumer trends: The rapidly changing food industry requires constant adaptation to new consumer trends, such as plant-based diets or the latest dietary fads. Diversification of products or distributive partnerships can help the subscription box company to stay relevant and appeal to a broader audience.

From apps that promise to make our lives easier to the toothbrushes that magically arrive at our door, we’re drowning in monthly charges. This October 2023 Harvard Business Review sheds light on this phenomenon, revealing that we’re not just imagining things – subscription fatigue is real, and it’s cluttering up our digital and physical doorsteps with an overwhelming array of choices. At the core of the problem at hand is consumer bifurcation.

In response to this bifurcated economic reality, retailers must chart new courses with a new focus that shifts to creating offerings tailored to a spectrum of economic segments. (2PM, December 2023)

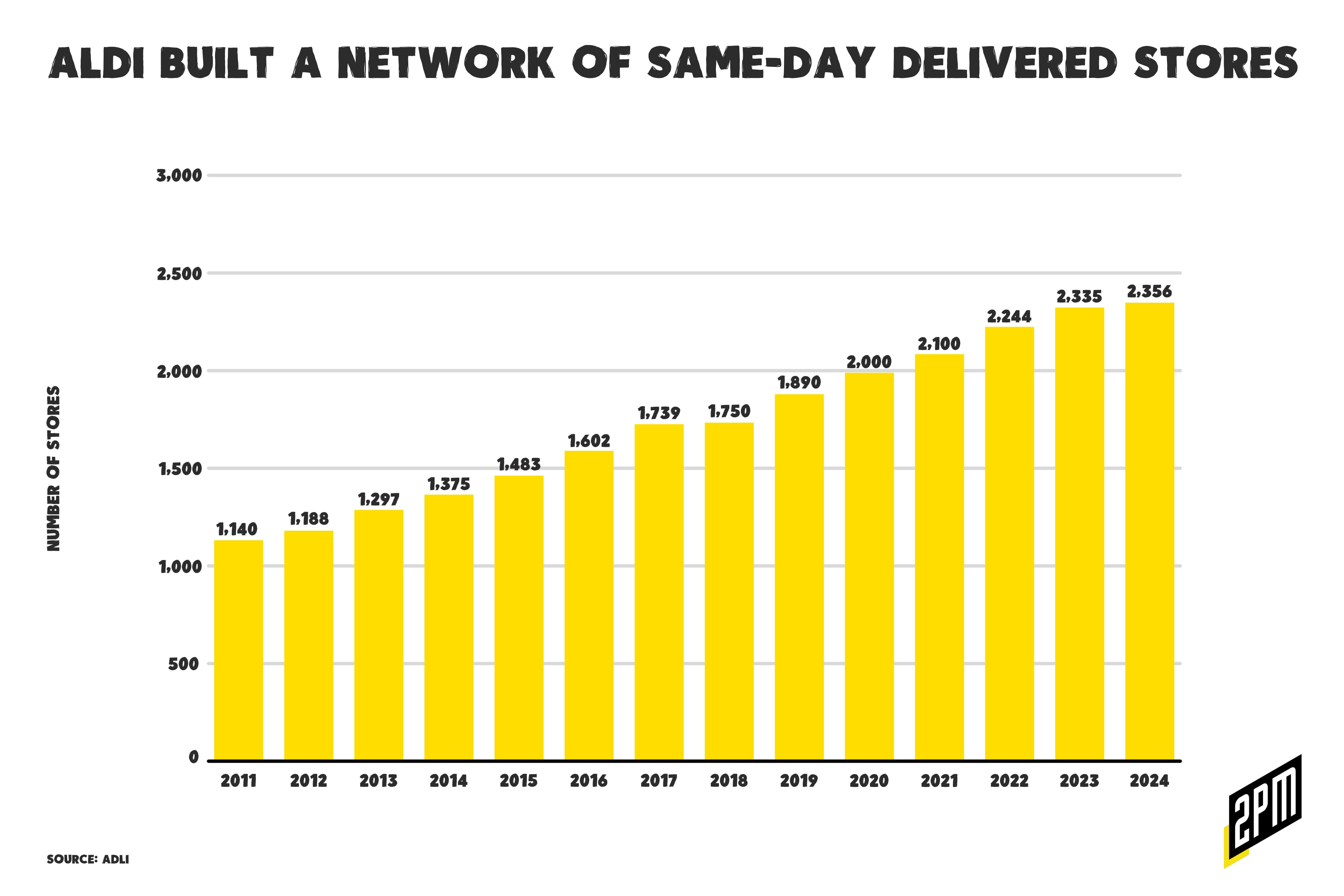

While Amazon tends to appeal to the upper wrung of customers, Aldi’s growth is indicative of the changing consumer landscape. With 2,356 stores, it would land at third on this list. The place is the antithesis of complication. Shopping at Aldi is like a breath of fresh, budget-friendly air. The store’s design is straightforward, and the selection, while limited, covers all the basics at prices that test the American belief of consumer pricing index. It’s the kind of simplicity that makes you wonder why shopping anywhere else feels like preparing for a space mission. Aldi’s model is a testament to the power of keeping it simple – a lesson many subscription services could learn from.

Then there’s Amazon – the Goliath of eCommerce. With its finger on the pulse of payments technologies, Amazon has the tools to make subscriptions feel less like a chore and more like a convenience. Imagine a world where subscriptions are so seamlessly integrated into our lives that we barely notice them, thanks to Amazon’s predictive algorithms and personalized recommendations. This wouldn’t just convenient; it would be revolutionary. Now Imagine if Aldi and Amazon, two giants from seemingly different worlds, both pursued the problem of subscription fatigue by allowing customers to be more fluid in how they request and receive their goods. Aldi’s mastery of simplicity and efficiency combined with Amazon’s technological prowess could pave the way for a subscription model that’s both effortless and exciting for food brands in search of growth. Subscriptions would no longer be a source of dread but a carefully curated part of our daily lives, offering exactly what we need, right when we need it.

A New Frontier: DTC Brands in the Grocery Aisle

But what about the DTC brands that are in need of efficient growth? There’s a new frontier for these brands, and I believe it’s piercing the veil of omnichannel distribution. The mission for those retailers, whether they are hawking beef, vegetables, or anything else with an expiration date is to land on the shelves of stores like Whole Foods, Kroger, CostCo, and Aldi. For DTC brands, this is not just about expanding distribution; it’s about integrating into the daily lives of consumers. It requires building an internal strategy that aligns with the values and operations of these retail giants. DTC brands need to understand the logistics, the pricing models, and the customer base of stores like Aldi and Whole Foods. They need to navigate the complexities of large-scale retail while maintaining the agility that made them stand out in the first place.

This direction is more than a business expansion; it’s a strategic alignment with the changing behaviors of consumers who crave simplicity and convenience in their shopping experience. By securing a spot in the inventory of stores affiliated with Amazon Prime or Instacart, DTC brands can ensure their products are as accessible as a click or a quick grocery run. They can also build an insurance model for the growing subscription fatigue that seems to be triggered by rising economic concerns.

In a world where subscription fatigue is the new norm, Aldi and Amazon emerge as potential beacons. For DTC brands looking to make their mark in the grocery world, the path is clear: align with the simplicity and technological savvy of these retail giants, and become an indispensable part of consumers’ lives.

The future of shopping is here, and it’s streamlined, personalized, and, most importantly, uncomplicated. The growth is in grocery delivery, not box shipments. This is the changing consumer behavior that the smartest retailers can opt-in to grow alongside.

By Web Smith