The commerce, payments, and debt products industries are converging. Shopify is one of the few companies that sits at the nexus of these three.

Over the last few months, I spent a substantial amount of time preparing for and passing my Securities Industry Essentials Exam (SIE) to gain at least a rudimentary understanding of consumer, fiduciary, and monetary principles and how they impact equity and debt markets. I learned a lot along the way. The motivation was and is to understand the mechanics of financial markets with some proficiency (and maybe pursue a Series 7, who knows). As I went through this studying process, it became clear that understanding today’s online retail landscape requires a firm grasp of the financial systems.

Payments, debt, and commerce are all converging. Shopify is at its nexus.

Shopify is one company at the intersection of commerce, payments, and debt. To properly analyze the growth of companies like it, you also have to understand the financial systems that it relies on for growth businesses.

At its core, Shopify is a platform that enables small and medium-sized businesses to build and operate online stores. The company’s value proposition and its ability to support merchant growth have positioned it as a pillar of the eCommerce ecosystem. But many on the outside may not realize that Shopify’s growth trajectory is tied not just to the number of new stores it enables, but also to the financial products it offers. Shopify’s venture into lending and merchant cash advances (MCAs) through Shopify Capital has positioned it as both a commerce enabler and a financial services player.

This dual role becomes even more interesting when you consider that new store growth is slowing, as indicated in its most recent earnings call. While Shopify remains a dominant force in eCommerce, the platform is maturing. The initial and later surges of new store creations, the latter driven by a combination of pandemic-driven digital adoption and Shopify’s user-friendly interface, has naturally slowed. Today, the company faces a new challenge: sustaining growth not through the sheer number of stores created, but through deepening its relationships with existing merchants, which is where its Capital division becomes crucial.

Shopify Capital: The Key Growth Business

In 2024, Shopify Capital became an understated yet vital piece of Shopify’s growth strategy. In Q2 of this year, Shopify originated $700 million in loans. Shopify CFO Jeff Hoffmeister referred to this arm of the company as a “growth business,” highlighting its increasing importance. Yet, despite these numbers, Shopify has downplayed the role of Capital in its overall strategy, a stark contrast to earlier years when it would broadcast the growth of its lending arm during earnings calls. Amazon followed a similar model, until recently. It now refers its clients to third-party lenders.

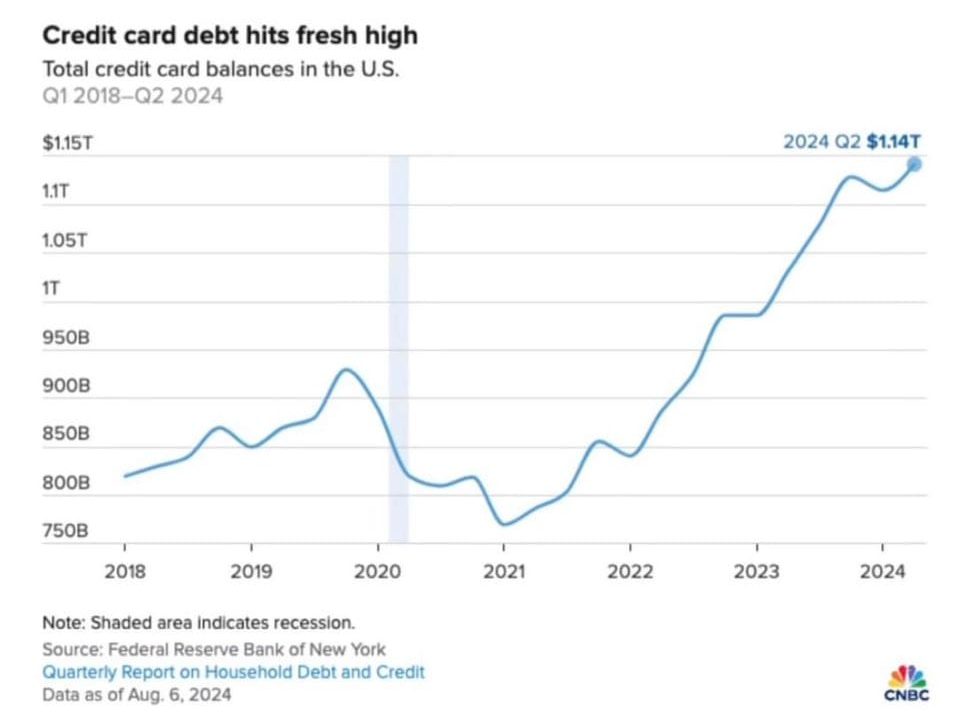

One of the reasons for Shopify’s newfound reticence could be tied to market conditions. With U.S. credit card debt reaching a record $1.14 trillion by Q2 2024 and delinquency rates rising, the financial environment is becoming increasingly precarious for both consumers and small businesses. Shopify’s merchants, most of whom are small businesses, are particularly vulnerable to these macroeconomic trends. Shopify’s hesitation to promote its lending growth could be a protective measure, shielding itself from scrutiny should the economic environment worsen, leading to higher default rates among its loan recipients.

Financial Strain and the Broader Economic Picture

To truly understand the risks Shopify faces, it’s essential to look at the broader financial landscape. The latest data from the Federal Deposit Insurance Corporation (FDIC) shows a sharp increase in past-due and nonaccrual rates for non-owner occupied, nonfarm, nonresidential loans, particularly for banks with assets exceeding $250 billion. This indicates stress in the commercial real estate market, a crucial segment for many small business owners, particularly those operating physical stores.

Shopify Capital’s loan recipients, who are predominantly online merchants, might seem insulated from this trend, but they are not immune to broader economic pressures. Rising consumer debt levels signal that end customers may reduce discretionary spending, which directly impacts Shopify merchants’ revenue streams. If consumers tighten their belts, small businesses – many of which operate on razor-thin margins – will struggle to maintain cash flow, driving demand for short-term capital (often MCAs) to bridge gaps in revenue.

This increased demand for Shopify’s primary growth market, MCAs, comes amidst heightened risk. The more merchants turn to Shopify for financial support, the greater Shopify’s exposure to potential defaults, especially as economic conditions worsen. In an environment where loan delinquencies are rising across the board, Shopify will need to strike a careful balance between sustaining growth through lending and managing the risk that accompanies it.

A Shift in Growth Strategy: Beyond New Store Creation

The slowing growth in new store creation means that Shopify can no longer rely on onboarding new merchants to fuel its financial growth. Instead, it is now identifying clients from existing legacy platforms. Additionally, the company is maximizing the value of its existing merchant base while helping each of these merchants find new ways to drive their own increase in revenues. This is where the intersection of commerce, payments, and debt becomes critical. Shopify is no longer just a commerce platform; it has evolved into a multi-faceted financial services provider, using its intimate knowledge of merchants’ sales data to offer targeted lending products.

By leveraging its financial data and payment processing capabilities, Shopify has created a flywheel effect. It enables merchants to grow their businesses, process payments through Shopify Payments, and then access capital through Shopify Capital when needed. This ecosystem not only ties merchants deeper into the Shopify platform but also creates multiple revenue streams for the company. However, this financial flywheel is not without its challenges during periods of systemic risk.

As consumer and commercial debt levels rise, Shopify faces increasing risk exposure. The company’s balance sheet shows $815 million in loans and MCAs as of Q1 2024, a slight decrease from the previous quarter ($816 million). While Shopify has yet to provide transparency on whether it is offloading some of these receivables to banks like Synchrony, the flat growth in receivables is notable, especially in a time when demand for small business funding should be increasing.

Shopify is navigating a delicate balance. On the one hand, it must continue to grow its lending division to maintain momentum as new store creation slows. On the other hand, it must manage the growing risks associated with rising default rates and the increasing financial stress on small businesses and consumers alike.

The Road Ahead for Shopify

As Shopify’s business models continue to evolve, its future growth will increasingly hinge on its ability to operate effectively at the convergence of commerce, payments, and debt.

While the company has been quiet about its lending business in recent quarters, its growing importance is hard to ignore. Shopify Capital long represented an opportunity for the company to deepen its relationships with existing merchants, generate recurring revenue, and diversify its income streams. However, the growing risks are outside of Shopify’s control and the company will need to be vigilant in managing its exposure to defaults as economic pressures mount.

In an environment where financial literacy is becoming a crucial part of understanding company growth, Shopify serves as a prime example of how deeply intertwined commerce and financial services have become. Understanding the company’s future means not only tracking new store growth but also keeping a close eye on its balance sheet, its lending practices, and the broader economic conditions that will shape the trajectory of the industry’s major players.

Research, Data, and Writing by Web Smith