This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.

Memo: Middle Class Opportunity

In what can only be characterized as a leading indicator for shifting economic tides in retail, the middle-class brand is beating the S&P and leaving a trail of upper-scale competitors in its wake. It’s emblematic of the slowing bifurcation of consumers and the retailers that support them. This is from our report on the Gilded Age 2.0, a period that seemed to last for about four to five years (2017-2022).

While history doesn’t repeat itself, it does rhyme. The economically-disadvantaged deliver food, novelties, alcohol, and commodities to urban sprawls and gated suburbs – within the hour. Across the country, the net worths of the top 1% have become noticeable as conspicuous consumption of products and services have risen; the rise of platforms like StockX, Hodinkee, and Uncrate demonstrate this. For the top .01%, there are more 40,000+ square foot homes than there were in the Roaring 20’s. Retail is responding to economic realities of today. Wealth is galvanizing; retail strategies should adjust to meet the shifts head on.

As well-funded resale sites like The RealReal, thredUp, and Poshmark battle it out online, spending big money on marketing while rapidly losing valuation, a decidedly offline company is quietly winning. Its success is emblematic of the power the long middle wields in retail today. That power is only growing as bifurcation trends putters out.

Winmark owns franchises of secondhand shops across the United States to include: Plato’s Closet, Play It Again Sports, and Once Upon a Child. You’ve probably never heard of its parent company but you have at least driven by one of the shops in a suburban strip mall. Forbes profiled the company, which is a profitable, public, billion-dollar business that goes so far under the radar that it doesn’t do earnings calls. Twenty investors own 80% of the company:

Call it the tortoise of the resale wars. The company, which went public in 1993, before hardly anyone was shopping on the internet, has taken a slow-and-steady approach. New stores are opened at a modest pace, allowing the company to be selective about the franchisee applicants it accepts. It hasn’t overspent on splashy marketing.

The resale industry (formerly known as second-hand shops) is growing fast. The segment could double to $82 billion by 2026, according to an industry-funded report—fueled by a generation of young shoppers interested in buying unique pieces in an affordable, environmentally friendly way. It’s getting an added boost at a time of soaring inflation and supply chain issues, with many shoppers flocking to thrift stores after encountering high prices and out-of-stock items at big-box retailers.

Winmark’s business model is the right one for the moment. It offers affordable, practical goods for middle class Americans who, as Once Upon A Time franchisee Diane Hubel says, need to be efficient with their dollar as inflation has spiked and wages remain stagnant for most. It even offers them a way to make money in return by selling off stuff they no longer need. And because the products are secondhand, the supply chain problems plaguing other retailers don’t exist within Winmark’s portfolio of retailers. The stock isn’t guaranteed, which can be a disadvantage, but it’s reliable in that it can typically provide some option, even if it’s not the first preferred.

Then there’s the profitability. Winmark will not build an unprofitable operation.

Winmark has dabbled in e-commerce, but only when the prices are high enough to make it profitable. For instance, at Music Go Round, which sells things like used saxophones and electric guitars, the average order value is over $250, so it launched a website to sell goods online. It has no such plans for clothing stores like Plato’s Closet or Once Upon A Child, where the average item costs under $10.

As laid out by Forbes, Winmark’s online competitors are not profitable and their valuations have been sliced their IPOs. It’s likely that if they were still private, they would avoid IPO altogether:

These DTC competitors were revolutionaries of an antiquated secondhand market but the business mechanics are hard to make work. They’re learning that now, and the boom times are over. Winmark is leaner — it doesn’t have to invest in the extensive process of listing secondhand items for mass consumption.

All of this makes for a story of a retailer who is winning in difficult times. It’s not flashy. It hasn’t raised venture capital. But it’s there for a middle class that is finding themselves against market forces working against them. It’s a bleak outlook right now for many — meaning simpler, down to basics businesses are finding themselves in better position than the recent years defined by consumer bifurcation and the companies appealing to a luxury consumer.

By Web Smith | Art by Christina Williams and Alex Remy | Edited by Hilary Milnes

Also read: Sak Pase, a reflection on our last several weeks and the recent missionary trip that I was fortunate enough to embark on.

Member Brief: Klarna’s Challenges Ahead

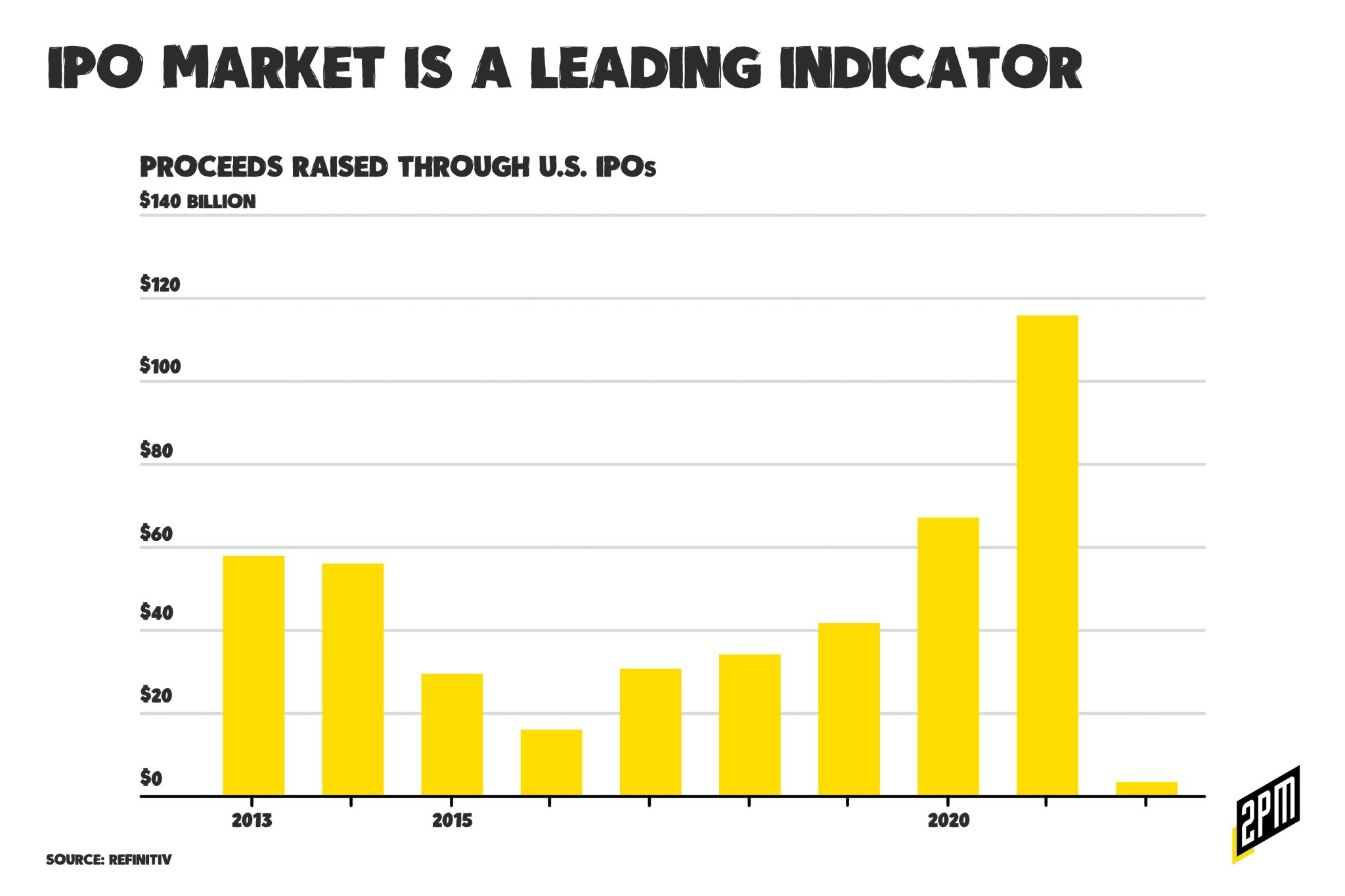

Venture-backed consumer technologies thrived throughout the decade-plus long bull market. Profitability was secondary to growth. Market capture was the key performance indicator. The buy now, pay later (BNPL) industry is one of those industries facing the strongest headwinds.

From $5.5 billion market capitalization and up to a $46 billion before falling to $15 billion and dropping: Klarna’s rollercoaster valuation over the past two years is symbolic of the larger buy now, pay later cohort of fintech companies that promised to change the way we consume online. For online retailers, BNPL represented a promise of higher conversion rates for costly products. According to recent reports, the investment capital has dried up. Of all of the recent reports on the matter, WIRED’s was the most thorough:

Klarna’s dream—to replace credit cards, which Siemiatkowski describes as “the worst form of credit”—is facing a series of existential threats. The company’s workforce is still reeling from layoffs that affected 10 percent of its staff and new regulation which will impose stricter rules on BNPL providers in the UK, one of its key markets. At the same time, BNPL executives told WIRED that investors are losing faith in the sector in the face of a potential recession.

What is the main culprit causing Klarna’s valuation to tank after such soaring heights? Is it being in the sights of Apple’s next ground capture? Or PayPal developing its own competitive products? Is it the regulations emerging in the UK against Klarna and its peers over predatory practices appealing to young customers? Or is it the sobering up of venture capitalists as we loom on the brink of a recession? It’s likely a combination of the above.

What it all means is that Klarna and companies like it, including Affirm and Afterpay, will need to place greater ambitions for taking over online shopping on the backburner in order to focus on core product and profitability. It’s back to reality.

The most apparent form of that reality is the impending regulation that 2PM forecasted back in 2020. As BNPL normalizes, more attention will be paid to how these companies operate. From the recent report in WIRED:

The problem of the summer surge in competition is compounded by the UK government’s plan, announced on June 21, to require lenders to carry out affordability checks on people using BNPL, to make sure they can afford the loans they take out. (1)

This was predictable based upon our study of the consumer debt cycle in China, a country that adopted the democratization of this form of debt long before the United States.

Like millions of people around the world, Zhang Chunzi borrowed money she thought she’d be able to repay before the coronavirus changed everything.

Now laid off from her job at an apparel exporter in Hangzhou — one of China’s most prosperous cities — the 23-year-old is missing payments on 12,000 yuan ($1,700) of debt from her credit card and an online lending platform operated by Jack Ma’s Ant Financial. “I’m late on all the bills and there’s no way I can pay my debt in full,” Zhang said. (2)

China has since regulated their accessible consumer credit industry. In America, regulations could lead to a ripple effect, putting a leash on Klarna and other BNPL’s bounds by enacting borrowing protections typical of regular credit. According to the UK government’s statement, BNPLs are “rapidly increasing in popularity, resulting in potential risk of harm to users.” As more risks behind BNPL schemes – which can sometimes seem too good to be true – are made apparent, users could second guess whether or not to use them at all.

Klarna and its peers are not the only class of disruptors who are facing growing pains. The glory days are over for other companies like Uber and Airbnb, and the industries they operate in. Ride share companies in New York City often make less sense than hailing a taxi, while rates have ballooned in all markets to make up for driver shortages. Uber is in ongoing legal battles over whether or not its drivers count as employees, as regulations hit the rideshare industry. Airbnb is wading through customer backlash as people report poor experiences and stacked-high fees that make hotels the better option in comparison. How Airbnb began, versus where it is now, is drastically different: it’s playing into the housing crisis and struggling to maintain quality across its rental options as its inventory has become more and more expensive.

When disruptor companies grow out of their scrappy startup stages, they face realities of incumbents: regulation, widespread competition and fewer outside funds. For BNPL companies, the biggest threat is being replicated by institutions that have the customer base and protections to withstand regulations. Why outsource your payments to Klarna when you could use Apple Pay? And who says Apple and PayPal are the last to step into this territory. This scenario is reminiscent of a concern that we published in 2020 on The Credit Report. In it, we explain what happened to the debt bubble in China:

According to Atlantis Financial Research, defaults in China have risen from 1% to 4%. And with overdue credit up 50%, delinquency has increased from 13% to 20%. Once a conservative country with respect to debt-to-income ratios, China’s consumer habits mirror America’s. The aggregate debt load of China has doubled since 2015. Globally, it’s even more frightening. Some projections by the International Labour Organization cite 25 million global jobs lost with a potential debt load of $3.4 trillion. But here in the United States, economic matters are shaping up to be an historic outlier of devastation.

This makes debt alternatives more risky than the traditional credit institutions, a realization that only seems to arrive as bull markets become bear markets. Here is that TL;DR from that now two year old report on the matter:

In the short-term, there is a train headed towards the consumer economy that can only be slowed. If China’s response to a weakening economy is any indication, the corporate and consumer debt bubbles are in danger.

For now, BNPL firms are going to try to distance themselves from the BNPL tagline. According to WIRED, Klarna, Affirm and others will focus on profits as well as other financial services like debit and wallets. Klarna’s modest valuation could set the space on a more responsible track. It’s the market leader of the new era of fintech creditors like Afterpay, Zip, Sezzle, and Affirm. In pursuing profitability and product diversification, its next steps will serve as a bellwether for the rest of the industry.

By the 2PM Team