Harry’s delivered a sizable outcome in their recent $1.37 billion exit. The men’s grooming company should be viewed as somewhat of a wake up call to DNVB leaders. Yes, Harry’s sold a simple product but it also disrupted the DTC playbook on its way to an exit. The company wrote and followed its own playbook, why don’t more digital-natives do the same? It has been reported that just 20% of Harry’s sales volume came by way of direct to consumer revenue. Everything about Harry’s ascension opposed the presumed operating instructions of the DTC era.

Yes, Target and J. Crew accounted for nearly 80% of Harry’s overall sales. But that isn’t only what sets Harry’s apart from the tendencies of other digital-natives. By all reports, Harry’s is a well-run business: the logistics operation is flawless, the company is reportedly profitable, and they’ve essentially retooled manufacturing for the demands of the DTC era. Simply put, Andy Katz-Mayfield and Jeff Raider have been extraordinary leaders.

Harry’s accomplished a great deal in six years. The razor manufacturer was an early omni-channel pioneer: partnerships with Target and J. Crew were pivotal in their ensuing mainstream success. Collaborations with digital publishers like Uncrate reminded consumers that Harry’s was an elevated brand, something more than their competitors. Harry’s was one of the first to launch pop-up activations. Each of these decisions countered conventional wisdom at the time.

From a 2014 interview with CNBC: Warby Parker takes on Gillette

Raider and Katz-Mayfield believe the key to Harry’s growth lies in this vertical integration, or what they like to call v-commerce. Simply put, the company now owns the entire process—from R&D to manufacturing to selling direct to the consumer. “It creates this virtuous cycle that makes for really happy customers, and then they become our best advocates,” says Katz-Mayfield.

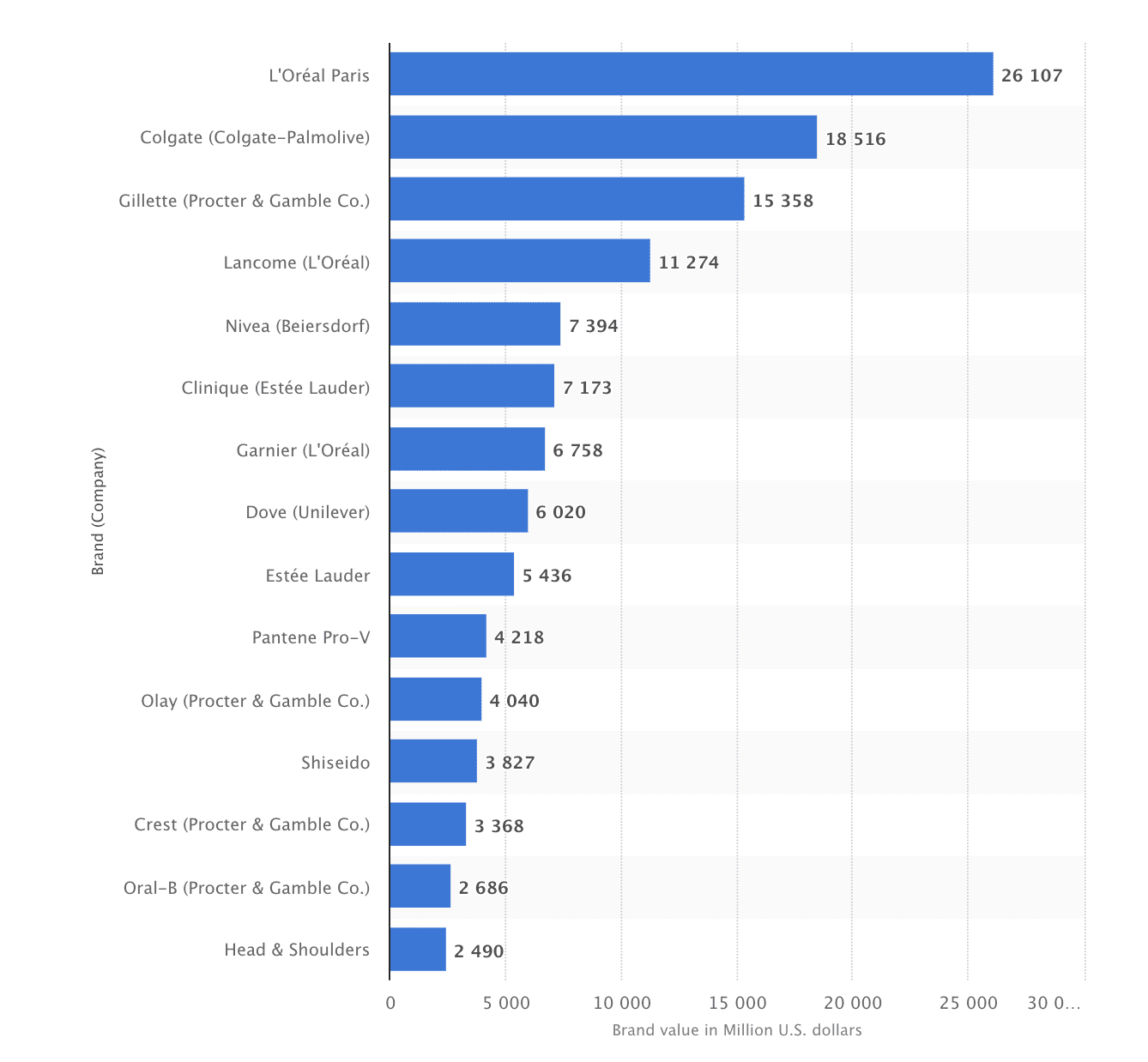

When Harry’s acquired their manufacturing partner, the company became one of the few truly vertical brands of the DTC era. This was also antithetical. But, it allowed them to iterate their core product quicker and streamline product iteration for their sourced products like skincare, soaps, and shaving additives. The result was a Target aisle that began to reflect that Harry’s was more than a product brand, they were a category leader. In this way, Harry’s began challenging Gillette in an asymmetrical fashion by becoming one of the first true DTC category brands. By designing appealing products in other product verticals, Harry’s gained an advantage. This leverage helped them to amass over 2.4% of the entire razor market. In short, Harry’s wasn’t just great at marketing and design – they disrupted their industry.

I’m bearish. It’s hard, only the disruptors will survive.

Anonymous Founder

Skepticism of the direct to consumer era of online retail isn’t new. General Partner of Great Oaks Ventures, Henry McNamara recently tweeted:

Henry McNamara on Twitter

DNVBs Valued @ $1B+ & Funding 👓Warby $1.75B- $290M raised (6x) 👟Allbirds $1.4B- $77M raised (18x) 🪒Harry’s $1.37B- $461M raised (3x)* 💄Glossier $1.2B- $187M raised (6.5x) 🛏️Casper $1.1B- $339M raised (3.5x) 🪒Dollar Shave $1B- $163M raised (6x)* 🧔Hims $1B- $197M raised (5x)

He later corrected his figure on Harry’s ($375 million in equity sold) but the point stands. Is investing in digital-natives worth it? Yes. But only if the brand is capable of disrupting prior growth tactics and brand positioning. Dollar Shave Club and Harry’s represent two of the most notable exits of the DTC era, both found ways to acquire customers and sell a growing catalogue of products to them. Both were valued between 4-6x the capital raised. These companies found innovative ways to market, distribute, and grow. In turn, they innovated their way to earned market share, at the expense of incumbents and other challengers.

THE DTC PLAYBOOK IS A TRAP

It goes without saying that I’m bearish on DNVBs as a whole. As a whole, the industry tends to rely upon left-brain operators with systems and definite plans. But, I’m bullish on the challenger brands who’ve figured out that winning is often a result of rewriting the playbook. For the brands looking to grow to (efficient) critical mass or even an exit, the DTC playbook is a trap. The journey from zero to one is not one backed by b-school theory. Brands won’t be able to project tomorrow’s viability by analyzing yesterday’s LTV:CAC ratio, alone. But DNVB growth isn’t an art, either. Digital-natives will have to be more than beautiful design and savvy copywriting. The proverbial DTC playbook must be rewritten each time. If the DTC playbook were to be written, it could be boiled down to this:

There is no playbook. DNVB growth must be a malleable and agile operation. Brands must find opportunities where there were none. They must seek to do what hasn’t yet been done.

So yes, I am bearish on many of today’s DNVBs. Brands are merely following the paths of the brands before them and I believe that it hinders more than helps. Their paths to their early-stage milestones are often unproven anecdotes written by investors who’ve likely never sold a physical product.

In a recent thread by Ryan Caldbeck on this same topic, the founder and CEO of Circle Up expressed his similar skepticisms with the following points:

-

- I’m not that convinced that DTC is going to kill a lot of incumbents. If we look at share loss for Pepsi, Unilever, etc- much of that is not DTC, it is products/brands that meet unique needs of today’s fragmenting consumers.

- I’m deeply skeptical that the DTC startups have nailed online marketing. Almost all of them are burning cash at levels unprecedented in CPG (most of $ for marketing). Does that mean they are good at marketing, or just that they have convinced venture capitalist to to give them money?

- A question might be: can they sustain the innovation? I haven’t seen a lot of startups come out with more than a small handful of products. Most of the DTC companies are not using DTC for what I think it’s great at – which is iterating on product development.

YOU SHOULD BE BEARISH

In a recent Member Brief, I wrote on the asymmetrical warfare that Caldbeck summarizes so eloquently, “A dynamic brand enables more than product success, it enables category success. As brands known for one thing enter the categories of other competitors, the companies with the most brand equity and marketing sophistication seem to be best positioned to make the leap from product company to category brand.”[1] But brand equity is just one component; Harry’s operational superiority and omnichannel sophistication has been on display over its six years as an independent company. It should be a message to younger companies that achieving an exit will take more than a beautifully-crafted facade that hides operational chaos (as is often the case).

Mientras las marcas DTC intenten seguir lo que se ha hecho antes que ellas, usted también debería mostrarse escéptico ante el sector. Muchos inversores parecen buscar un libro de jugadas DTC para entregar a las empresas de su cartera. Como si dijeran: "Así es como se hace. Ahora ejecute el plan de juego". Pero es probable que nunca sea así. A medida que los nativos digitales empiezan a competir en el territorio del comercio minorista tradicional, las marcas tradicionales deberían servir de recordatorio. Tuvieron caminos únicos hacia la masa crítica, muy pocas se encontraron con la previsibilidad que busca la era DTC.

Rather than determining speculative best practices with few data points, DNVBs should review the small number of successes from the DTC era. There have been but a few unicorns minted and even fewer exits earned. Those that do exit are often quiet, EBITDA-driven brands that represent “scalable profit.” Great examples of this are Schmidt’s Naturals or Native Deodorant. These retailers earned a place atop the market by responding to forces, maintaining agility, promoting executive autonomy, and thinking a few steps ahead of the curve. That should be the only guidance that earlier-stage founders need.

Read the No. 317 curation here.

Por Web Smith | About 2PM

Editor’s Note: Edgewell backed out of the Harry’s acquisition in February 2020, some eight months after breaking the news.