The moment that changed the music business happened insurgently, as they do. In 1998, when Shawn Fanning began working on Napster, the once-infamous file sharing platform, it was built on a borrowed laptop with little money and even less support. And then, in an act of serendipity, a pre-Facebook Sean Parker met Fanning in a hacker chat room. The two would go on to raise a quick $50,000, move to California, and settle in on the second floor of a bank.

Though networks of distributed files existed across the web, Napster’s focus on MP3 files (coupled with a relatively simple interface) pushed the service to 80 million registered users. The growth was seemingly instantaneous. The platform’s sweet spot: unreleased and hard-to-find music (such as studio recordings, concert bootlegs, and older songs). In a number of ways, Napster paved the way for today’s streaming economy.

There was no ramp up. There was no transition. It was like that famous shot from 2001: A Space Odyssey, when the prehistoric monkey throws a bone in the air and it turns into a spaceship. Napster was a ridiculous leap forward.

Alex Winter, Director of Downloaded

The disruption felt like the violent recoil of heavy artillery after a feather’s landing on the trigger. There was collateral damage on both sides of the barrel. The music industry was unprepared for a disruption that would cannibalize the physical retail of music. And Napster was unprepared for the litigation that would come. Chaos was created, whether intentional or not.

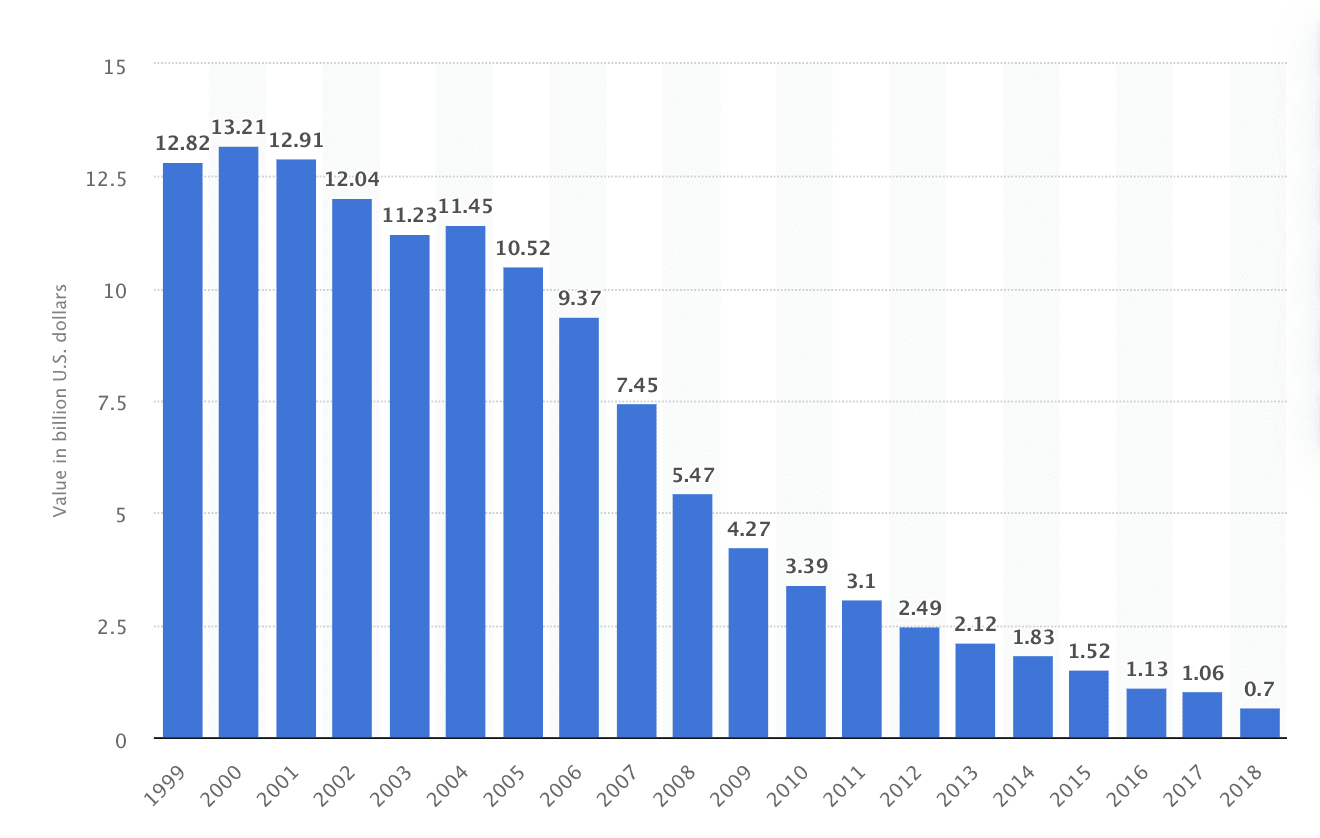

In a year’s time, billions in value was lost to Napster, a platform that was designed to market music into a public good. The whole of today’s streaming economy was born of this disruption. And while Napster was at the precipice of this shift from physical to digital, its key technologies are no longer relevant. The modern version of Napster lives on as a carbon copy of the economy that it would later influence: subscription-based streaming. It would be a retail innovation by Amazon that, when applied to digital media marketplace, would re-define a two hundred year old industry for a new millenium.

Fanning and Parker’s platform emerged at the end of an explosive decade for the music industry. There were healthy profits reaped by many labels and publishers, thanks to the maturing of the compact disc (CD) as a preferred medium. At $15 – $21 per unit, the music industry’s primary channel was an expensive one. In this way, Napster was a catalyst for market correction. Until that point, a consumer would have to purchase an entire CD to listen to the two or three songs that they preferred. Napster allowed for the ownership of individual tracks and, in turn, it devalued the sale of entire albums.

Joe Rogan recently hosted The Wu-Tang Clan’s Robert Fitzgerald “RZA” Diggs on Episode No. 1382 of his podcast. The host couldn’t have predicted that the most newsworthy snippet of the conversation would hinge on the technology of the 1990’s.

Napster comes right in and and takes all these songs where all these people who are waiting for their publishing checks are waiting for the economics to be created from music. Now, there’s no publishing check. All of the numbers have decreased because there’s no physical sell of the music to accumulate value.

Diggs would go on to explain that between 2000 – 2015, the loss in physical sales ultimately transformed the industry into one that we see today. There were few winners in music during that span. Of them: the iPod, the iPhone, Spotify, Beats By Dre, Live Nation, and Universal Music Group. Music was no longer the product for sale.

On Chaos Theory and Patent US5960411A

As eCommerce is a multi-dimensional consideration, a single theory may not be sufficient for the overall perspective views. […] However, the Chaos Theory is suitable for describing the customer decision making, especially the buying behaviours seems to be random in which the classical model of classical decision model cannot be described. [1]

The market would begin to mold around Napster’s influence. Platforms with similar architecture went live. That list included: Gnutella, Freenet, BearShare, Kazaa, LimeWire, AudioGalaxy, and Madster. It’s important to note that each of these platforms was disrupted by copyright litigation.

Flapping a butterfly’s wings over the Amazon could influence the storm in China. This is the basis of the Butterfly Effect, also known as deterministic chaos, a phenomenon where equations with little to no uncertainty yield uncertain outcomes. Chaos Theory is the mathematics that explains the butterfly wings’ theoretical influence over China’s weather patterns. In this analogy, there is a bit of irony.

Chaos Theory is a delicious contradiction – a science of predicting the behavior of “inherently unpredictable” systems. It is a mathematical toolkit that allows us to extract beautifully ordered structures from a sea of chaos. [2]

It was Apple’s CEO Steve Jobs who challenged conventional wisdom by questioning the value proposition of file sharing. For Jobs, piracy wasn’t the catalyst for Napster’s monumental growth and influence. Rather, the combination of ease and convenience was the deterministic chaos. Steve Jobs would recruit the help of Jeff Bezos and a now-famous Amazon patent to address the mathematics of buying behaviors. When the deal was announced between the two companies, Jobs levied a glowing endorsement of Bezos’ early technological advantage.

The Apple Store has been incredibly successful and now we’re taking it to the next level. Licensing Amazon.com’s 1-Click patent and trademark will allow us to offer our customers an even easier and faster online buying experience.

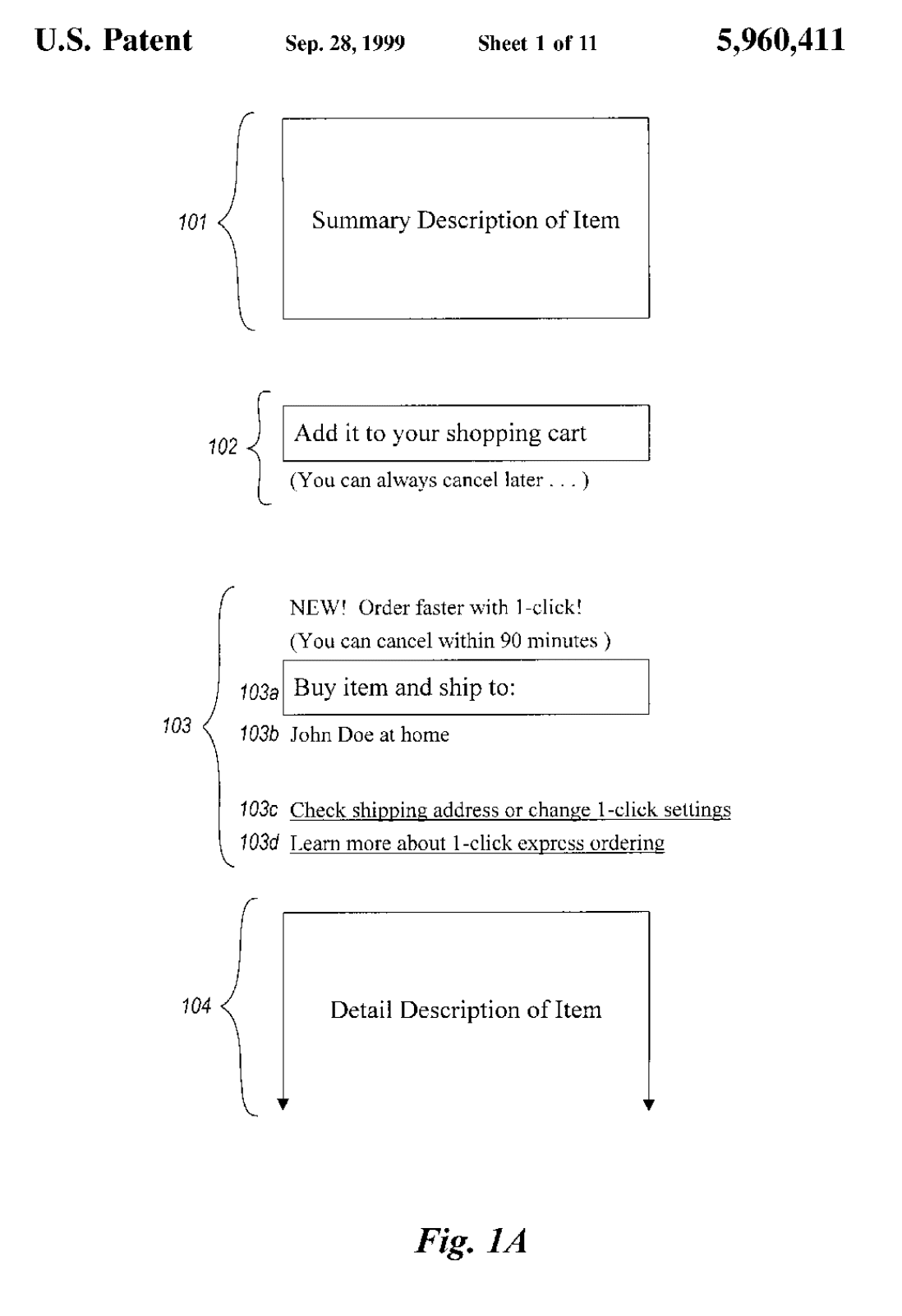

In September of 2000, Apple became the first company to license Amazon’s 1-Click patent (US5960411A) and trademark for use across Apple’s eCommerce properties. This innovation enabled Apple to store billing and shipping information, allowing customers to click their mouses once without any data input. To Jobs, this was the key to the industry’s music problem. By making conversion easy and ownership effortless, consumers would flock to legitimate sources of commerce. And he was right.

By 2003, the iTunes Music Store was outselling its next best competition by a margin of five to one. That competition was a legitimate version of Napster. Apple’s combination of iTunes and the iPod provided a seamless experience for conversion, management, and consumption. Apple understood that Amazon’s advantage wasn’t what it was selling, it was how it was selling. This influence would affect music and entertainment. iTunes was a precursor to 2005’s Pandora and 2008’s Spotify. Apple’s 1-Click system of retail influenced a new style of movie consumption, one that would spawn companies like Netflix in 2010 – though streaming technologies hadn’t yet caught up to market demands.

Apple would become the only company to license Amazon’s technology. US Patent 5960411A would help Amazon to nearly two decades of unfettered growth. That patent would expire in 2017. By that year, nearly half of all online retail volume in America was completed through Amazon.com and its affiliates. Consumers are willing to set aside cost for ease of purchase. Amazon was the first to prove this; Apple may have been the second.

Chaos Theory Revisited

Others, including Amazon competitors, have already noticed the 1-Click patent’s expiration. Last year, a group of companies in the alliance known as the World Wide Web Consortium, including Apple, Facebook and American Express, started working on standards to implement one-click purchasing. Google is also reportedly working on a one-click payment solution. [3]

Amazon’s innovations influenced an unforeseen number of industry advancements. With 1-Click commerce in the public domain, new upstarts like Fast join technology’s giants in building independent solutions to bolster the adoption of frictionless commerce. Apple Pay has seen wide adoption. Shopify Pay was a star of the most recent holiday season, garnering praise from the vendors who benefited from frictionless payments. This dizzying pace of innovation is the result of a technology that’s been locked away about for nearly 20 years.

Until recently, Amazon’s patents prevented wide use. Amazon’s 1998 lawsuit against Barnes & Noble is a persisting example of why few companies test Bezos knack for IP litigation.

Amazon started using one-click technology in September 1997, but did not receive a patent for it until Sept. 28 this year. Barnesandnoble has offered “Express Lane,” its one-click checkout, since the spring of 1998. “The one-click feature is one of Amazon.com’s signature strategies for differentiating itself from the competition and building loyalty among its customers,” Amazon wrote in its complaint. [4]

In 2000, then-students Erik Brynjolfsson and Michael D. Smith identified this in a case study written for MIT’s Sloan School of Management. Pricing rationality matters less when ease-driven loyalty is at the forefront of the consumer’s mind.

A direct prediction of these models then is the retailer with the lowest prices should have the highest proportion of sales since it will get sales from all the informed consumers in addition to its “share” of the uninformed consumers. However, this prediction is not supported by our data. Amazon.com is the undisputed leader in online book sales, and yet is far from the leader in having lower prices. [5]

To this end, a solution for the reduction of bottom-funnel friction recently launched. And it may be the most fluid of them all. “Ten years ago today, I was packing boxes.” Gary Vaynerchuk will go on record as saying that he isn’t very smart. Don’t let him fool you. In 1998, at the onset of his early days of growing his family’s online business, his team built one of the first iterations of an automated cart abandonment recovery. Unfortunately, he didn’t file a patent for that process – a tool that is now common throughout cloud-based carts like Shopify, BigCommerce, Adobe, and SalesForce Commerce Cloud.

Polymathic Audio No. 3: Gary Vaynerchuk

In 1998, Wine Library was grossing nearly $3 million annually. By 2011, that figure inched toward $67 million in annual sales. Vaynerchuk didn’t accept any outside investment to get to that point, a remarkable note when you consider the constraints of cash flow-driven growth. That same year, he stepped down from the family business to build VaynerMedia. When Vaynerchuk and I spoke with 2PM for Polymathic, he relayed a recent story of his father reaching out to him and asking for him to come back to the Vaynerchuk family’s original business and course-correct a company that had halved in size since Gary’s departure. Deterministic chaos: the solution that Gary executed may end up becoming another proverbial butterfly over the Amazon.

To solve the problem for Wine Library, Vaynerchuk recruited some help from his VaynerMedia team. The result was WineText, an SMS-based marketing and commerce channel. The user begins by signing up on the homepage, providing a few key details: name, address, phone number, and payment data. Like Amazon’s 1-Click system, WineText saves users’ credit cards with the help of Stripe. Powered by Twilio, Vaynerchuk and team can send a daily deal to the list at a cost of anywhere between $240 and $360 per text. According to Vaynerchuk, the SMS list of nearly 9,000 customers consistently outperforms Wine Library’s email list of 400,000 by a magnitude of 9x. And here’s why.

WineText opt-in grants Vaynerchuk access to your phone number. On occasion, a customer will receive an SMS prompt with a “high value wine offer.” Users have up to ten minutes to respond to the text with the number of bottles requested. That number of bottles is at your door within 48 hours of shipping. The top-of-funnel friction removes all bottom-funnel checkout thinking. It makes a commerce decision reflexive.

To accomplish this, WineText built a native checkout solution to account for Shopify’s native restrictions with respect to stored credit cards. For those who are interested, there is a way around it according to Postscript Co-Founder and President Alex Beller:

One way around this for more mainstream merchants who want to allow customers to buy in-message is using Postscript + Recharge + Shopify. Recharge allows for that sort of open access to credit cards of saved customers.

Beller added:

All brands should not jump on this bandwagon. However, any brand with subscriptions, natural reorder cycles, or drop strategies should lean in here. Engagement rates are too high to ignore.

As more retail operators become aware of the technology stack implemented by Vaynerchuk and team, WineText-like services will become more common. There are no patents to protect it. Amazon’s innovation indirectly impacted the streaming industry that exists today. Just as eCommerce patents changed music forever, you have to consider unrelated industries that will thrive with frictionless commerce.

Chaos Elsewhere

The Action Network, created by the Chernin Group in 2017, has an app where gamblers can track their bets across sportsbooks. It’s also using in-depth stats and analysis to draw in bettors, and has been striking content and other deals with companies like Yahoo Sports, Nascar, PointsBet, William Hill, and DraftKings, to expand its footprint. [6]

In a conversation with Action Network’s Darren Rovell, I mentioned how 1-Click technology could impact publisher-driven betting. Rovell remains skeptical that a media platform could vertically integrate in such a way. When asked if Action Network would ever facilitate live bets, the industry veteran responded:

Facilitate? Yes. Click on our platform and it clicks to a [sports] book. Or bet with a book and you can track the progress with us. But, as of now, it’s not in our best interest to be an operator.

But in the analogy of the butterfly’s flight over the Amazon, all signs point to the intersection of media, commerce, and legalized gambling as the next major disruption in consumer media. Platforms like Barstool Bets, theScore, FanDuel, Draft Kings, B/R Sports Odds, and others are positioning to move beyond informing wagers by partnering with sports books to facilitate end to end commerce. They’ll eventually want users to place bets, natively.

In the past, people would read articles or watch videos on these publishers’ properties that would inform the bets they make elsewhere. But with sports betting becoming more widely legal, publishers can close that gap — and turn this into a revenue stream for themselves. “Our whole philosophy is if we do it right and give people an opportunity to bet within theScore, they’re not going to go elsewhere,” said John Levy, CEO of theScore. [7]

Frictionless commerce will define the next ten years of mid-market, online retail in North America. As it does, savvy commerce architecture will find its way to other industries once again. Legalized gambling appears ripe for this sort of disruption. Publishers want to shorten the distance between “finding your line” and you acting on it. What was once an industry built on publishing data and insights will become one where users can act with one click of a button. If there is one thing that we’ve learned from Napster, Amazon, Apple, and the streaming economy: ease of use is the safest bet.

Investigación e informe de Web Smith | Sobre las 2PM

Alimentos52 pertenece a una nueva generación de plataformas digitales que combinan operaciones comerciales y de medios de comunicación. Esto ayuda a diversificar los canales de ingresos al tiempo que minimiza los costes crecientes de la captación tradicional de clientes. No es fácil, pero puede ser gratificante. Hay varios editores en esta categoría: Barstool Sports, Uncrate, Highsnobiety, Hypebeast, y Hodinkee. Y recuerde, Glossier comenzó como un blog llamado Con brillo.

Alimentos52 pertenece a una nueva generación de plataformas digitales que combinan operaciones comerciales y de medios de comunicación. Esto ayuda a diversificar los canales de ingresos al tiempo que minimiza los costes crecientes de la captación tradicional de clientes. No es fácil, pero puede ser gratificante. Hay varios editores en esta categoría: Barstool Sports, Uncrate, Highsnobiety, Hypebeast, y Hodinkee. Y recuerde, Glossier comenzó como un blog llamado Con brillo.