To better understand the increasingly cutthroat grocery industry, I read “The Secret Life of Groceries” by Benjamin Lorr, elements of which will be summarized here. It opened my eyes to say the least; I will never consume another package of beef, seafood, berries, packaged salad snacks, or even my favorite canned drink without thinking about the sacrifice required to get those products to our doors.

The secret to successful grocery shopping lies in understanding the psychology behind product placement and marketing. […] In the modern grocery industry, competition is fierce, with retailers constantly vying for our attention and loyalty.

The modern grocery store is a marvel of contemporary commerce, revolutionizing the way we shop, eat, and live. It’s also as cutthroat as the industries that we have historically associated with that descriptor: oil and gas, textiles, and any others that we know to have elements of violence, forced labor, or worse.

Let’s first begin with some history.

****

The evolution of the grocery store began with the introduction of Piggly Wiggly in Memphis, Tennessee, in 1916 by Clarence Saunders. This was the first self-service grocery store, revolutionizing the retail landscape by allowing customers to browse and select their own products, a departure from the traditional clerk-assisted model.

In 1937, Sylvan Goldman, an Oklahoma businessman, further transformed the shopping experience with the invention of the shopping cart. Observing that shoppers stopped purchasing when their baskets became too heavy, Goldman created a wheeled cart with baskets, increasing convenience and encouraging more purchases.

The grocery industry continued to innovate with the establishment of larger chains. Kroger, founded in 1883, grew into a major player by implementing many of the modern retail practices developed by Piggly Wiggly and Mr. Goldman, expanding its range of products and services. Whole Foods, launched in 1980, targeted health-conscious consumers with its focus on organic and natural foods, and in 2017, it was acquired by Amazon for $13.7 billion.

Trader Joe’s, founded in 1967, distinguished itself with unique private label products (effectively launching the private label industry) and a quirky, customer-centric approach. Aldi, which entered the U.S. market in 1976, offered a no-frills, cost-effective shopping experience that appealed to budget-conscious shoppers.

These pioneers laid the foundation for today’s diverse and competitive grocery landscape, characterized by innovation, convenience, and a constant evolution to meet changing consumer demands.

****

According to the Bureau of Labor Statistics: in 1901, Americans had an average spend of 42.5% of the household budgets on groceries. By the 1930s, that number was around 33% and today: American consumers spend just 11% of their household income on groceries. Until recently at least (buoyed by a higher CPI and persisting inflation), food felt available and commoditized. Lorr’s book made me realize just how much of a false perception that is.

Far from being simple retailers of food, grocery stores have evolved into complex entities that reflect broader social, economic, and technological trends. From the humble beginnings of self-service stores in the early 20th century to the sprawling supermarkets and specialized grocers of today, the grocery industry has become a fiercely competitive and dynamic segment of retail. This report will explore the rise of the grocer, the intricacies of supply chains, the cutthroat nature of the industry, and the intensifying challenges faced by CPG brands in an evolving retail landscape.

Yesterday And Today: A Lesson To Modern Retail

Trader Joe’s, a beloved grocery chain known for its unique products and customer-centric approach, owes its success to the visionary leadership of its founder, Joe Coulombe. After graduating from Stanford in 1958, Coulombe initially worked for Rexall, the largest retail pharmacy chain at the time, where he successfully developed a new line of convenience stores called Pronto Markets. When Rexall decided to shut these stores down, Coulombe borrowed money, bought them himself, and transitioned from a corporate employee to a determined entrepreneur.

Recognizing the impending competition from 7-Eleven, Coulombe pivoted his business model. He rebranded his stores with a South Seas motif, diversified the product range, and named the new venture Trader Joe’s. His ability to foresee and capitalize on emerging trends was a key factor in his success. With Boeing’s introduction of the 747, Coulombe anticipated that increased international travel would spark American consumers’ interest in exotic foods. This led him to stock Trader Joe’s with unique, imported foods that stood out from the typical American grocery offerings.

Coulombe also had a keen understanding of his target market. He identified “overeducated and underpaid” individuals—screenwriters, musicians, museum curators, and journalists—as his core customers. This focus on a specific demographic allowed him to tailor the product offerings to their tastes and preferences. Trader Joe’s became known for its eclectic mix of products, including private label items that bolstered profits, such as the now-iconic almond butter.

Another innovative strategy was the localization of stores. Unlike other chains with identical store layouts, Trader Joe’s stores featured unique decorations and murals created by in-house artists to reflect the local community. This approach fostered a sense of connection between the store and its neighborhood, enhancing customer loyalty.

Listening to customers was also a cornerstone of Trader Joe’s success. Coulombe consistently responded to customer feedback by adding more organic and healthy items, eliminating products sourced from China due to safety concerns, and phasing out plastic packaging. This responsiveness helped maintain customer trust and loyalty over the years.

A significant differentiator for Trader Joe’s was its wine section. Coulombe, a wine enthusiast, recognized that educated consumers tended to drink more wine. By dedicating a substantial portion of store space to value wines, particularly from California, Trader Joe’s attracted wine lovers who then discovered the store’s unique food offerings. The introduction of “Two Buck Chuck,” a private label wine sold for $1.99, became a cultural phenomenon and drew countless new customers to Trader Joe’s.

Today, despite being owned by a German company, Trader Joe’s continues to operate on the principles established by Joe Coulombe. Yes, Trader Joes’s is owned by the same family that owns Aldi’s.

Trader Joe’s founder Joe Coulombe sold his business to Theo Albrecht in 1979, officially making the Albrecht family the proud owners of both prosperous markets — specifically, the Aldi Nord branch, since the company is split into two.

His early vision was remarkably prescient, anticipating many trends that define the modern grocery industry: a focus on imports, catering to educated consumers, creating new products from existing commodities, and leveraging private labeling to enhance profitability. Trader Joe’s success story is a testament to entrepreneurial foresight, customer focus, and innovative thinking.

Before the rise of supermarkets, grocery shopping involved visiting multiple specialized shops—bakeries, butcheries, and green grocers—which was time-consuming and often inconvenient. The supermarket consolidated these various food categories under one roof, offering remarkable convenience and unprecedented variety. This evolution continued post-World War II, driven by suburbanization and the growth of the middle class, resulting in the architectural behemoths we recognize today. These behemoths come with plastic baggage.

Complexities of the Supply Chain

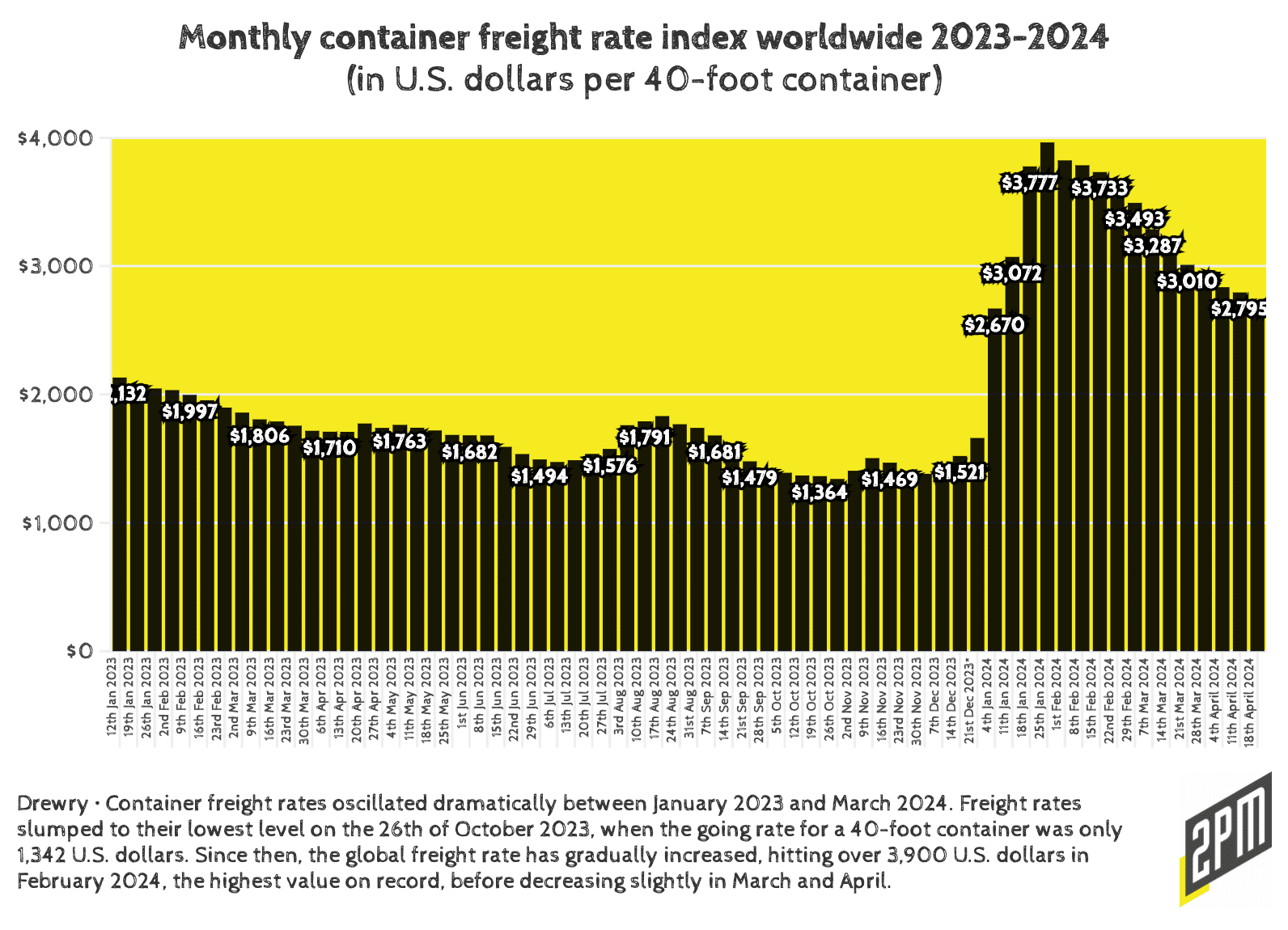

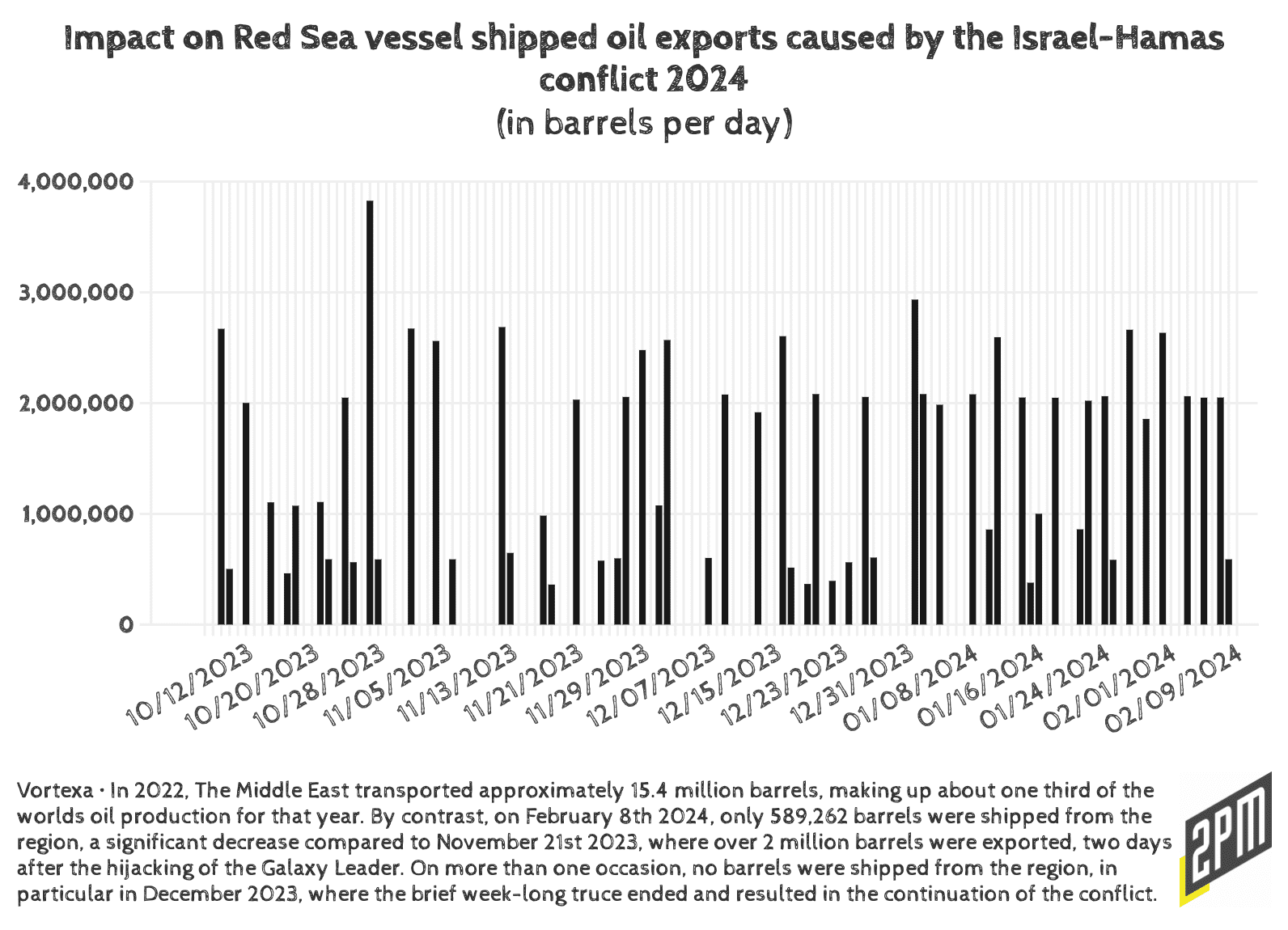

The seamless operation of a modern grocery store depends on an intricate and often unseen network of supply chains that span the globe. These supply chains involve numerous players, including farmers, manufacturers, distributors, and retailers, all working in concert to meet consumer demand. However, behind the scenes lies a world fraught with challenges, some of which reveal troubling ethical issues.

One of the most harrowing aspects of the global food supply chain is the exploitation of labor, exemplified by the Thai shrimp industry. Lorr’s book revealed harrowing stories that span from backroom workers in your favorite Whole Foods to the economic and physical dangers of trucking, to the aforementioned Thai shrimp industry’s literal slavery. I don’t use that term as a figure of speech.

His investigations uncovered severe abuses, including forced labor and human trafficking, where workers are subjected to brutal conditions and treated as modern-day slaves at worst or indentured servants at best. These practices are driven by the relentless demand for cheap seafood in Western markets, highlighting a dark side of globalization and the hidden human cost embedded in our groceries.

The complexity of the supply chain also involves logistical challenges. Maintaining the freshness and quality of perishable goods requires sophisticated refrigeration systems and efficient transportation routes. Just-in-time inventory systems, designed to reduce storage costs and inventory holding times, demand flawless synchronization. And the global dimension of the supply chain introduces regulatory, political, and environmental hurdles that must be navigated carefully.

Geopolitics and the Future of Grocery Retail

The future of the grocery industry will increasingly rely on executives who are aware of these intensifying concerns. The global nature of food supply chains means that political instability, trade disputes, and regulatory changes can have profound impacts on the availability and cost of products. Executives must learn to navigate these challenges while balancing the demands for ethical sourcing, sustainability, and profitability.

Amazon’s Subscribe & Save, has shifted consumer behavior, reducing in-store shopping for non-perishable items. Technological advancements will play a crucial role in shaping the future of grocery retail. The rise of eCommerce and online grocery shopping has transformed consumer habits. In Subscription Box Fatigue, I wrote about what is now called “replenishment shopping”:

This direction is more than a business expansion; it’s a strategic alignment with the changing behaviors of consumers who crave simplicity and convenience in their shopping experience. By securing a spot in the inventory of stores affiliated with Amazon Prime or Instacart, DTC brands can ensure their products are as accessible as a click or a quick grocery run. They can also build an insurance model for the growing subscription fatigue that seems to be triggered by rising economic concerns.

Replenishment shopping, or the frequent one-click acquisition of goods to replace diminished inventory, for non-perishables has significantly altered the grocery shopping experience for retailers, consumers, and store brands. Rather than strict subscription purchases, customers have a loose automation by way of platforms like Amazon, Instacart, DoorDash, or UberEats. Retailers like Walmart are losing market share of center-aisle products—such as paper towels, toilet paper, consumer packaged goods and canned goods—to eCommerce subscription services like Amazon’s Subscribe & Save. This shift means that consumers are spending less time in physical stores, with 42% of retail subscribers shopping in-store less often due to their subscriptions.

PYMNTS Senior Vice President and Head of Analytics Scott Murray noted: Paper towels, toilet paper and even cans of soup and things like that, but when it comes to perishables, I think people generally still go [to stores].

For traditional grocery retailers (with exception of Trader Joe’s and Aldi’s apparently), this poses a threat, necessitating a shift towards convenience-oriented channels such as same-day delivery to retain customer loyalty. Consumers benefit from the convenience and cost savings of subscription services, while store brands must innovate to compete with these new purchasing patterns. Overall, the rise of replenishment shopping is reshaping the grocery landscape, emphasizing the need for retailers to adapt to evolving consumer behaviors and preferences.

Changing Dynamics Between Retailers and CPG

This disruption and innovation have significantly altered the relationship between retailers and CPG companies. Both have invested heavily in new technology, channels, product development, and consumer touchpoints to stay relevant. However, their evolving roles and strategies have created tension as each takes on parts of the other’s traditional functions and innovates in different ways.

Retailers, especially in the grocery sector, have become more empowered. The pandemic accelerated technology plans, leading to the implementation of contactless payments, self-service checkouts, click-and-collect services, and expanded delivery options. Retailers have also extended their private label product ranges and improved the customer experience, driving convenience, efficiency, and value; CPG brands lose when this strategy succeeds. In some cases, grocers have positioned themselves as defenders of the consumer, pushing back against excessive price increases from CPG companies and refusing to stock certain branded goods.

Conversely, CPG companies have sought to reduce their distance from consumers by developing replenishment business models, including websites, loose subscription models, and advertising partnerships on platforms like Instacart that can remind the customer that product availability is theirs for the taking. The best performing ones have focused on making supply chains more flexible and responsive, reviewing ingredients and recipes to reduce costs and be more sustainable, and exploring various physical channels beyond major grocery stores.

Additional Challenges for CPG Brands

The shifting dynamics have made the grocery industry particularly challenging. Shelf space is at a premium, with retailers exercising greater control over their product offerings. The EY Future Consumer Index indicates that consumers are turning away from once-favored brands, with many opting for private label products. Branded products now come in smaller pack sizes, and consumers are more willing to switch to new products if they offer better quality or value.

As more consumers turn to online shopping for the bulk of their replenishment shopping, traditional grocery stores face challenges in maintaining their margins and adapting to a fragmented shopping environment.

CPG companies are finding it increasingly difficult to control their product narrative in a landscape where information is readily available, and consumers are more informed than ever. Transparency, authenticity, and purpose have become crucial in maintaining consumer trust and loyalty. However, with limited opportunities to communicate these attributes at the point of sale, CPG brands must invest in multiple channels to maintain visibility and control their brand message. This, of course, can be incredibly costly at a time when consumers feel economically disadvantaged as a whole.

Consumers are increasingly looking for ways to control their spending amid financial challenges. Recent PYMNTS Intelligence data shows that a significant percentage of consumers have altered their grocery shopping habits due to rising prices, cutting down on nonessential spending and switching to cheaper merchants. This shift underscores the need for both retailers and CPG companies to adapt to the changing economic landscape and consumer behavior.

****

The rise of the grocer, from the early days of self-service stores to the sophisticated supermarkets of today, reflects broader trends in consumer behavior, technology, and globalization. The complexities of supply chains, including troubling ethical issues like forced labor, highlight the hidden costs behind our groceries. The grocery industry remains one of the most cutthroat segments in retail, requiring constant innovation and adaptation.

As the industry moves forward, it will increasingly depend on executives who are attuned to geopolitical concerns and capable of navigating a complex global landscape. The future of grocery shopping will be shaped by technological advancements and a continued focus on ethical and sustainable practices.

In an ecosystem as interdependent as this one, success now is about fostering open, collaborative, and agile ways of thinking and working. Retailers and CPG companies must leverage each other’s strengths and innovations to approach the future from a position of strength. Ultimately, it’s critical to continue understanding the consumer.

The changes in the way CPG and retail work together could present an opportunity for a more radical rethink, not just of how they go to market, but how they measure success in a continually changing world. As the grocery industry navigates these challenges, it will remain a vital and dynamic part of our daily lives. This final quote by Benjamin Lorr is one that I am unlikely to forget.

To narrow down their efforts, [Humanity United] focused on industries that were likely to achieve a media hit: Was the product imported into the United States in significant quantities? Would the severity of abuse shock consumers? Ten different commodities met these new criteria: chocolate, coffee, shrimp, cattle, conflict minerals such as tungsten, cotton, timber, sugar, palm oil, and gold.

History has proven that when you do the right thing for the consumer, the entire consumer ecosystem wins. But if I have learned anything throughout this research, it’s that consumer wins often mean labor – at some point in the supply chain – is suffering a cutthroat loss. Six of the commodities that Humanity United pinpointed are ones that make our grocery industry go.

I believe that this is the most important thing to remember when shopping for what we all seem to take for granted: groceries. It’s a system that allows us to “hate our shrimp but eat it too,” as Lorr so eloquently put it. As the replenishment economy continues to grow, we will only be farther removed from the supply chains that do the work to make same day grocery delivery possible.

Research, Writing, and Data by Web Smith