Para entender melhor o setor de supermercados, cada vez mais competitivo, li "The Secret Life of Groceries" (A vida secreta dos supermercados), de Benjamin Lorr, cujos elementos serão resumidos aqui. Isso abriu meus olhos para dizer o mínimo; nunca mais consumirei outro pacote de carne bovina, frutos do mar, frutas vermelhas, saladas embaladas ou até mesmo minha bebida enlatada favorita sem pensar no sacrifício necessário para que esses produtos cheguem às nossas portas.

O segredo para fazer compras de supermercado com sucesso está em entender a psicologia por trás da colocação de produtos e do marketing. [...] No moderno setor de supermercados, a concorrência é feroz, com os varejistas disputando constantemente nossa atenção e fidelidade.

A mercearia moderna é uma maravilha do comércio contemporâneo, revolucionando a maneira como fazemos compras, comemos e vivemos. Também é tão cruel quanto os setores que historicamente associamos a esse descritor: petróleo e gás, têxtil e qualquer outro que sabemos ter elementos de violência, trabalho forçado ou coisa pior.

Vamos começar com um pouco de história.

****

A evolução da mercearia começou com a introdução da Piggly Wiggly em Memphis, Tennessee, em 1916, por Clarence Saunders. Essa foi a primeira mercearia de autoatendimento, revolucionando o cenário do varejo ao permitir que os clientes procurassem e selecionassem seus próprios produtos, um desvio do modelo tradicional assistido por balconistas.

Em 1937, Sylvan Goldman, um empresário de Oklahoma, transformou ainda mais a experiência de compras com a invenção do carrinho de compras. Observando que os clientes paravam de comprar quando suas cestas ficavam muito pesadas, Goldman criou um carrinho com rodas e cestas, aumentando a conveniência e incentivando mais compras.

O setor de supermercados continuou a inovar com o estabelecimento de cadeias maiores. A Kroger, fundada em 1883, tornou-se uma grande empresa ao implementar muitas das práticas modernas de varejo desenvolvidas pela Piggly Wiggly e pelo Sr. Goldman, expandindo sua gama de produtos e serviços. A Whole Foods, lançada em 1980, visava consumidores preocupados com a saúde, com foco em alimentos orgânicos e naturais e, em 2017, foi adquirida pela Amazon por US$ 13,7 bilhões.

A Trader Joe's, fundada em 1967, se destacou com produtos exclusivos de marca própria (lançando efetivamente o setor de marcas próprias) e uma abordagem peculiar e centrada no cliente. A Aldi, que entrou no mercado dos EUA em 1976, ofereceu uma experiência de compra econômica e sem frescuras que atraiu compradores preocupados com o orçamento.

Esses pioneiros lançaram as bases para o cenário diversificado e competitivo dos supermercados de hoje, caracterizado por inovação, conveniência e uma evolução constante para atender às mudanças nas demandas dos consumidores.

****

De acordo com o Bureau of Labor Statistics: em 1901, os americanos gastavam em média 42,5% do orçamento doméstico em mantimentos. Na década de 1930, esse número estava em torno de 33% e hoje: Os consumidores americanos gastam apenas 11% de sua renda familiar em mantimentos. Pelo menos até recentemente (impulsionados por um IPC mais alto e pela inflação persistente), os alimentos pareciam disponíveis e comoditizados. O livro de Lorr me fez perceber o quanto essa percepção é falsa.

Longe de serem simples varejistas de alimentos, as mercearias evoluíram para entidades complexas que refletem tendências sociais, econômicas e tecnológicas mais amplas. Desde os humildes primórdios das lojas de autoatendimento no início do século XX até os grandes supermercados e mercearias especializadas de hoje, o setor de mercearias se tornou um segmento dinâmico e extremamente competitivo do varejo. Este relatório explorará a ascensão do merceeiro, as complexidades das cadeias de suprimentos, a natureza cruel do setor e os desafios cada vez maiores enfrentados pelas marcas de CPG em um cenário de varejo em evolução.

Ontem e hoje: Uma lição para o varejo moderno

A Trader Joe's, uma cadeia de supermercados adorada, conhecida por seus produtos exclusivos e abordagem centrada no cliente, deve seu sucesso à liderança visionária de seu fundador, Joe Coulombe. Depois de se formar em Stanford em 1958, Coulombe trabalhou inicialmente para a Rexall, a maior cadeia de farmácias de varejo da época, onde desenvolveu com sucesso uma nova linha de lojas de conveniência chamada Pronto Markets. Quando a Rexall decidiu fechar essas lojas, Coulombe pediu dinheiro emprestado, comprou-as ele mesmo e passou de funcionário de uma empresa para um empresário determinado.

Reconhecendo a concorrência iminente da 7-Eleven, Coulombe mudou seu modelo de negócios. Ele reformulou a marca de suas lojas com um motivo dos mares do sul, diversificou a linha de produtos e batizou o novo empreendimento de Trader Joe's. Sua capacidade de prever e capitalizar as tendências emergentes foi um fator fundamental para seu sucesso. Com a introdução do 747 pela Boeing, Coulombe previu que o aumento das viagens internacionais despertaria o interesse dos consumidores americanos por alimentos exóticos. Isso o levou a estocar a Trader Joe's com alimentos importados exclusivos, que se destacavam das ofertas típicas dos supermercados americanos.

Coulombe também tinha um conhecimento profundo de seu mercado-alvo. Ele identificou indivíduos "supereducados e mal pagos" - roteiristas, músicos, curadores de museus e jornalistas - como seus principais clientes. Esse foco em um grupo demográfico específico permitiu que ele adaptasse as ofertas de produtos a seus gostos e preferências. A Trader Joe's ficou conhecida por sua mistura eclética de produtos, incluindo itens de marca própria que aumentaram os lucros, como a agora icônica manteiga de amêndoa.

Outra estratégia inovadora foi a localização das lojas. Diferentemente de outras redes com layouts de loja idênticos, as lojas da Trader Joe's apresentavam decorações e murais exclusivos criados por artistas internos para refletir a comunidade local. Essa abordagem promoveu um senso de conexão entre a loja e sua vizinhança, aumentando a fidelidade do cliente.

Ouvir os clientes também foi um dos pilares do sucesso da Trader Joe's. Coulombe respondeu consistentemente ao feedback dos clientes acrescentando mais itens orgânicos e saudáveis, eliminando produtos provenientes da China devido a preocupações com a segurança e eliminando gradualmente as embalagens plásticas. Essa capacidade de resposta ajudou a manter a confiança e a fidelidade dos clientes ao longo dos anos.

Um diferencial importante para a Trader Joe's foi sua seção de vinhos. Coulombe, um entusiasta do vinho, reconheceu que os consumidores instruídos tendiam a beber mais vinho. Ao dedicar uma parte substancial do espaço da loja a vinhos de valor, especialmente da Califórnia, a Trader Joe's atraiu os amantes de vinho que, em seguida, descobriram as ofertas exclusivas de alimentos da loja. A introdução do "Two Buck Chuck", um vinho de marca própria vendido por US$ 1,99, tornou-se um fenômeno cultural e atraiu inúmeros novos clientes para a Trader Joe's.

Hoje, apesar de pertencer a uma empresa alemã, a Trader Joe's continua a operar de acordo com os princípios estabelecidos por Joe Coulombe. Sim, a Trader Joe's é de propriedade da mesma família que é proprietária da Aldi's.

O fundador da Trader Joe's, Joe Coulombe, vendeu sua empresa para Theo Albrecht em 1979, tornando oficialmente a família Albrecht a orgulhosa proprietária dos dois prósperos mercados - especificamente, a filial Aldi Nord, já que a empresa é dividida em duas.

Sua visão inicial foi notavelmente presciente, antecipando muitas tendências que definem o setor de mercearia moderno: foco nas importações, atendimento a consumidores instruídos, criação de novos produtos a partir de commodities existentes e alavancagem de rótulos privados para aumentar a lucratividade. A história de sucesso da Trader Joe's é um testemunho da visão empresarial, do foco no cliente e do pensamento inovador.

Antes do surgimento dos supermercados, as compras de supermercado envolviam a visita a várias lojas especializadas - padarias, açougues e mercearias - o que consumia muito tempo e muitas vezes era inconveniente. O supermercado consolidou essas várias categorias de alimentos em um único local, oferecendo uma conveniência extraordinária e uma variedade sem precedentes. Essa evolução continuou após a Segunda Guerra Mundial, impulsionada pela suburbanização e pelo crescimento da classe média, resultando nos gigantes arquitetônicos que reconhecemos hoje. Esses gigantes vêm com uma bagagem de plástico.

Complexidades da cadeia de suprimentos

A operação ininterrupta de uma mercearia moderna depende de uma rede intrincada e muitas vezes invisível de cadeias de suprimentos que se estendem por todo o mundo. Essas cadeias de suprimentos envolvem vários participantes, incluindo agricultores, fabricantes, distribuidores e varejistas, todos trabalhando em conjunto para atender à demanda dos consumidores. Entretanto, nos bastidores, há um mundo repleto de desafios, alguns dos quais revelam questões éticas preocupantes.

Um dos aspectos mais angustiantes da cadeia global de suprimentos de alimentos é a exploração da mão de obra, exemplificada pelo setor de camarão tailandês. O livro de Lorr revelou histórias angustiantes que vão desde os trabalhadores dos bastidores do seu Whole Foods favorito, passando pelos perigos econômicos e físicos do transporte rodoviário, até a escravidão literal da indústria tailandesa de camarão mencionada anteriormente. Não estou usando esse termo como uma figura de linguagem.

Suas investigações revelaram abusos graves, incluindo trabalho forçado e tráfico de pessoas, em que os trabalhadores são submetidos a condições brutais e tratados como escravos modernos, na pior das hipóteses, ou como servos contratados, na melhor. Essas práticas são impulsionadas pela demanda incessante por frutos do mar baratos nos mercados ocidentais, destacando um lado sombrio da globalização e o custo humano oculto embutido em nossas compras.

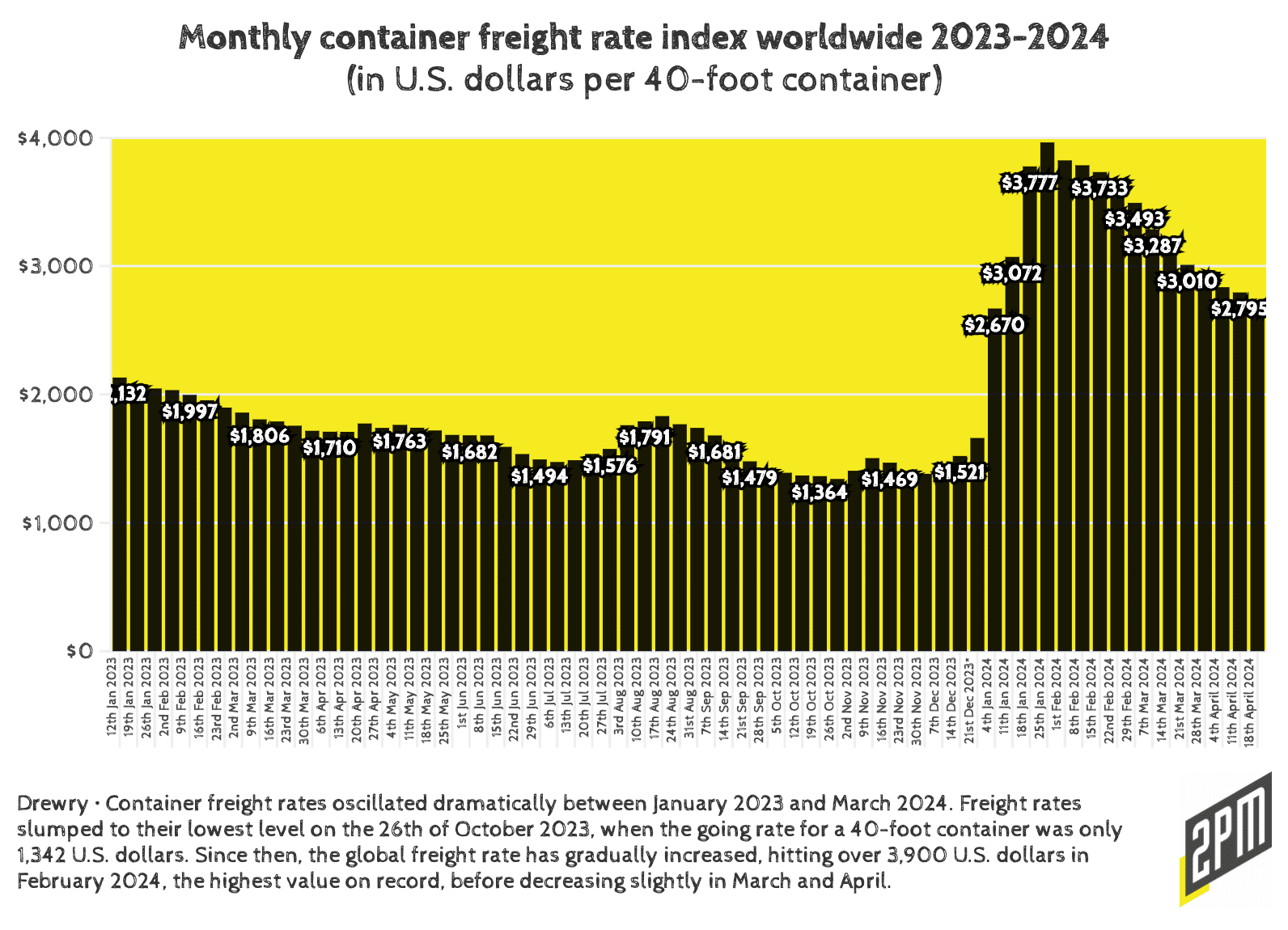

A complexidade da cadeia de suprimentos também envolve desafios logísticos. A manutenção do frescor e da qualidade de produtos perecíveis exige sistemas de refrigeração sofisticados e rotas de transporte eficientes. Os sistemas de estoque just-in-time, projetados para reduzir os custos de armazenamento e os tempos de retenção de estoque, exigem uma sincronização perfeita. Além disso, a dimensão global da cadeia de suprimentos introduz obstáculos regulatórios, políticos e ambientais que devem ser enfrentados com cuidado.

A geopolítica e o futuro do varejo de alimentos

O futuro do setor de supermercados dependerá cada vez mais de executivos que estejam cientes dessas preocupações crescentes. A natureza global das cadeias de suprimento de alimentos significa que a instabilidade política, as disputas comerciais e as mudanças regulatórias podem ter impactos profundos sobre a disponibilidade e o custo dos produtos. Os executivos precisam aprender a lidar com esses desafios e, ao mesmo tempo, equilibrar as demandas por fornecimento ético, sustentabilidade e lucratividade.

O Subscribe & Save da Amazon mudou o comportamento do consumidor, reduzindo as compras na loja de itens não perecíveis. Os avanços tecnológicos desempenharão um papel crucial na definição do futuro do varejo de alimentos. A ascensão do comércio eletrônico e das compras de supermercado on-line transformou os hábitos dos consumidores. Em Subscription Box Fatigue, escrevi sobre o que agora é chamado de "compras de reposição":

Essa direção é mais do que uma expansão dos negócios; é um alinhamento estratégico com as mudanças de comportamento dos consumidores que desejam simplicidade e conveniência em sua experiência de compra. Ao garantir um lugar no inventário das lojas afiliadas à Amazon Prime ou à Instacart, as marcas DTC podem assegurar que seus produtos sejam tão acessíveis quanto um clique ou uma rápida corrida ao supermercado. Elas também podem criar um modelo seguro para a crescente fadiga das assinaturas, que parece ser desencadeada pelo aumento das preocupações econômicas.

As compras de reposição, ou a aquisição frequente de mercadorias com um clique para substituir estoques reduzidos, para produtos não perecíveis alteraram significativamente a experiência de compras de supermercado para varejistas, consumidores e marcas de lojas. Em vez de compras por assinatura rígidas, os clientes têm uma automação livre por meio de plataformas como Amazon, Instacart, DoorDash ou UberEats. Varejistas como o Walmart estão perdendo participação no mercado de produtos de corredor central - como toalhas de papel, papel higiênico, produtos de consumo embalados e enlatados - para serviços de assinatura de comércio eletrônico como o Subscribe & Save da Amazon. Essa mudança significa que os consumidores estão passando menos tempo em lojas físicas, sendo que 42% dos assinantes de varejo compram na loja com menos frequência devido às suas assinaturas.

Vice-presidente sênior e diretor de análise da PYMNTS Scott Murray observou: Toalhas de papel, papel higiênico e até latas de sopa e coisas do gênero, mas quando se trata de perecíveis, acho que as pessoas geralmente ainda vão [às lojas].

Para os varejistas tradicionais de supermercados (com exceção do Trader Joe's e do Aldi's, aparentemente), isso representa uma ameaça, exigindo uma mudança para canais orientados para a conveniência, como a entrega no mesmo dia, para manter a fidelidade do cliente. Os consumidores se beneficiam da conveniência e da economia de custos dos serviços de assinatura, enquanto as marcas das lojas precisam inovar para competir com esses novos padrões de compra. De modo geral, o aumento das compras de reposição está remodelando o cenário dos supermercados, enfatizando a necessidade de os varejistas se adaptarem à evolução dos comportamentos e preferências dos consumidores.

Mudança na dinâmica entre varejistas e CPG

Essa ruptura e inovação alteraram significativamente o relacionamento entre os varejistas e as empresas de CPG. Ambas investiram pesadamente em novas tecnologias, canais, desenvolvimento de produtos e pontos de contato com o consumidor para se manterem relevantes. No entanto, suas funções e estratégias em evolução criaram tensão, pois cada uma assume partes das funções tradicionais da outra e inova de maneiras diferentes.

Os varejistas, especialmente no setor de supermercados, tornaram-se mais capacitados. A pandemia acelerou os planos de tecnologia, levando à implementação de pagamentos sem contato, caixas de autoatendimento, serviços de clicar e coletar e opções de entrega ampliadas. Os varejistas também ampliaram suas gamas de produtos de marca própria e melhoraram a experiência do cliente, aumentando a conveniência, a eficiência e o valor; as marcas de CPG perdem quando essa estratégia é bem-sucedida. Em alguns casos, as mercearias se posicionaram como defensoras do consumidor, resistindo aos aumentos excessivos de preços das empresas de CPG e se recusando a estocar determinados produtos de marca.

Por outro lado, as empresas de CPG têm procurado reduzir sua distância dos consumidores desenvolvendo modelos de negócios de reabastecimento, incluindo sites, modelos de assinatura avulsos e parcerias de publicidade em plataformas como a Instacart, que podem lembrar ao cliente que a disponibilidade do produto é sua. As empresas com melhor desempenho se concentraram em tornar as cadeias de suprimentos mais flexíveis e responsivas, revisando ingredientes e receitas para reduzir custos e ser mais sustentáveis, e explorando vários canais físicos além dos principais supermercados.

Desafios adicionais para as marcas de CPG

As mudanças na dinâmica tornaram o setor de supermercados particularmente desafiador. O espaço nas prateleiras é escasso, com os varejistas exercendo maior controle sobre suas ofertas de produtos. O EY Future Consumer Index indica que os consumidores estão se afastando das marcas que antes eram favoritas, e muitos optam por produtos de marca própria. Os produtos de marca agora vêm em embalagens menores, e os consumidores estão mais dispostos a mudar para novos produtos se eles oferecerem melhor qualidade ou valor.

À medida que mais consumidores recorrem às compras on-line para a maior parte de suas compras de reposição, os supermercados tradicionais enfrentam desafios para manter suas margens e se adaptar a um ambiente de compras fragmentado.

As empresas de CPG estão achando cada vez mais difícil controlar a narrativa de seus produtos em um cenário em que as informações estão prontamente disponíveis e os consumidores estão mais informados do que nunca. A transparência, a autenticidade e o propósito se tornaram cruciais para manter a confiança e a fidelidade do consumidor. Entretanto, com oportunidades limitadas de comunicar esses atributos no ponto de venda, as marcas de CPG precisam investir em vários canais para manter a visibilidade e o controle da mensagem da marca. Isso, é claro, pode ser incrivelmente caro em um momento em que os consumidores se sentem economicamente desfavorecidos como um todo.

Os consumidores estão cada vez mais procurando maneiras de controlar seus gastos em meio a desafios financeiros. Dados recentes da PYMNTS Intelligence mostram que uma porcentagem significativa de consumidores alterou seus hábitos de compras de supermercado devido ao aumento dos preços, reduzindo os gastos não essenciais e mudando para comerciantes mais baratos. Essa mudança ressalta a necessidade de os varejistas e as empresas de CPG se adaptarem às mudanças no cenário econômico e no comportamento do consumidor.

****

A ascensão das mercearias, desde os primeiros dias das lojas de autoatendimento até os sofisticados supermercados de hoje, reflete tendências mais amplas no comportamento do consumidor, na tecnologia e na globalização. As complexidades das cadeias de suprimentos, incluindo questões éticas preocupantes como o trabalho forçado, destacam os custos ocultos por trás de nossas compras. O setor de mercearia continua sendo um dos segmentos mais disputados do varejo, exigindo inovação e adaptação constantes.

À medida que o setor avança, ele dependerá cada vez mais de executivos que estejam sintonizados com as preocupações geopolíticas e sejam capazes de navegar em um cenário global complexo. O futuro das compras de supermercado será moldado pelos avanços tecnológicos e por um foco contínuo em práticas éticas e sustentáveis.

Em um ecossistema tão interdependente como este, o sucesso agora consiste em promover formas abertas, colaborativas e ágeis de pensar e trabalhar. Os varejistas e as empresas de CPG devem aproveitar os pontos fortes e as inovações uns dos outros para abordar o futuro a partir de uma posição de força. Em última análise, é fundamental continuar entendendo o consumidor.

As mudanças na forma como o CPG e o varejo trabalham juntos podem apresentar uma oportunidade para uma reformulação mais radical, não apenas de como eles vão ao mercado, mas também de como medem o sucesso em um mundo em constante mudança. À medida que o setor de alimentos enfrentar esses desafios, ele continuará sendo uma parte vital e dinâmica de nossas vidas diárias. Essa última citação de Benjamin Lorr é algo que dificilmente esquecerei.

Para restringir seus esforços,a [Humanity United] concentrou-se em setores que provavelmente atingiriam a mídia: O produto era importado para os Estados Unidos em quantidades significativas? A gravidade do abuso chocaria os consumidores? Dez commodities diferentes atenderam a esses novos critérios: chocolate, café, camarão, gado, minerais de conflito, como tungstênio, algodão, madeira, açúcar, óleo de palma e ouro.

A história provou que quando você faz a coisa certa para o consumidor, todo o ecossistema do consumidor ganha. Mas, se aprendi alguma coisa ao longo desta pesquisa, é que as vitórias do consumidor muitas vezes significam que a mão de obra - em algum ponto da cadeia de suprimentos - está sofrendo uma perda cruel. Seis das commodities que a Humanity United identificou são aquelas que fazem nosso setor de supermercados funcionar.

Acredito que essa é a coisa mais importante a ser lembrada ao comprar o que parece ser algo natural para todos nós: mantimentos. É um sistema que nos permite "odiar nosso camarão, mas comê-lo também", como disse Lorr de forma tão eloquente. À medida que a economia de reabastecimento continuar a crescer, estaremos cada vez mais distantes das cadeias de suprimentos que fazem o trabalho para tornar possível a entrega de mantimentos no mesmo dia.

Pesquisa, redação e dados por Web Smith