This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.

Polymathic: BigCommerce’s Big IPO

This member brief is designed exclusively for Executive Members, to make membership easy, you can click below and gain access to hundreds of reports, our DTC Power List, and other tools to help you make high level decisions.

Memo: Evolving Brand of DTC

A conversation with my six- and 12-year-old daughters shaped my thinking on this subject. As two members of Generation Z, they both possess an acuity for digital communication, gaming, and commerce. And if you believe that a six-year-old doesn’t care about eCommerce, ask her what Robux are. The question to my oldest was simple: isn’t spending money on a virtual world a waste of money? It is not real.

Dad, this is where my friends hang out and talk and play. Not internet friends, my real friends. This is just what we do and how we see things. Go to the mall or something, millennial.

Her views on her preferred technologies differ little than my own. It was very similar to how millennials view our own class of brands, media, and commerce. Certain classifications make sense to us; one of them is the all-encompassing “DTC” term.

The phrases are interchangeable. There’s “DTC”, “DNVB”, “direct brands”, “challenger brands”, and “digitally-natives.” Some brands begin on the internet and move to wholesale. Some pursue wholesale formats, only to pivot to online retail in an effort to shore up margins. There is very little organizational consistency among the now thousands of DTC brands selling across platforms like Amazon, Adobe Cloud, Shopify, Magento, Alibaba, WooCommerce, and BigCommerce. From platform to sales strategy, they share little in common. The attribute that they do share is that they are all modern brands. They pursue customers where they are. They are well-designed, purposeful, and familiar.

A direct-to-consumer or “DTC” brand is one that launched in or after 2007. This category of brand typically launches with agile software architecture and a management style that valued the evolution of retail methods and technologies. Whereas the shelves of Target or Walmart made its predecessors, these brands are made on our iPhones. These brands are advertised, sold, and discussed on digital platforms. The term “DTC” does not signify a particular sales channel, a refrain that you commonly hear from traditional retail executives and investors. Rather, it’s a generational term that communicates age, awareness, and intent.

It’s also a category known for its relative failures. Of the now thousands of brand launches in the previous 13 years, there have been fewer than 50 notable exits. In a conversation with a publicly-traded cosmetics executive, she suggested that the direct-to-consumer (DTC) brand industry was overdue for a renaissance. Our internal data agrees.

A New Strategy, A New Time

In the aforementioned discussion, we both agreed that the pandemic has accelerated retail’s transition from traditional to digital-first. This has upended timelines, projections, and the fundamental understanding of how retail will operate in the coming years. But as a second order effect, the pandemic may impact exit viability of the DTC industry.

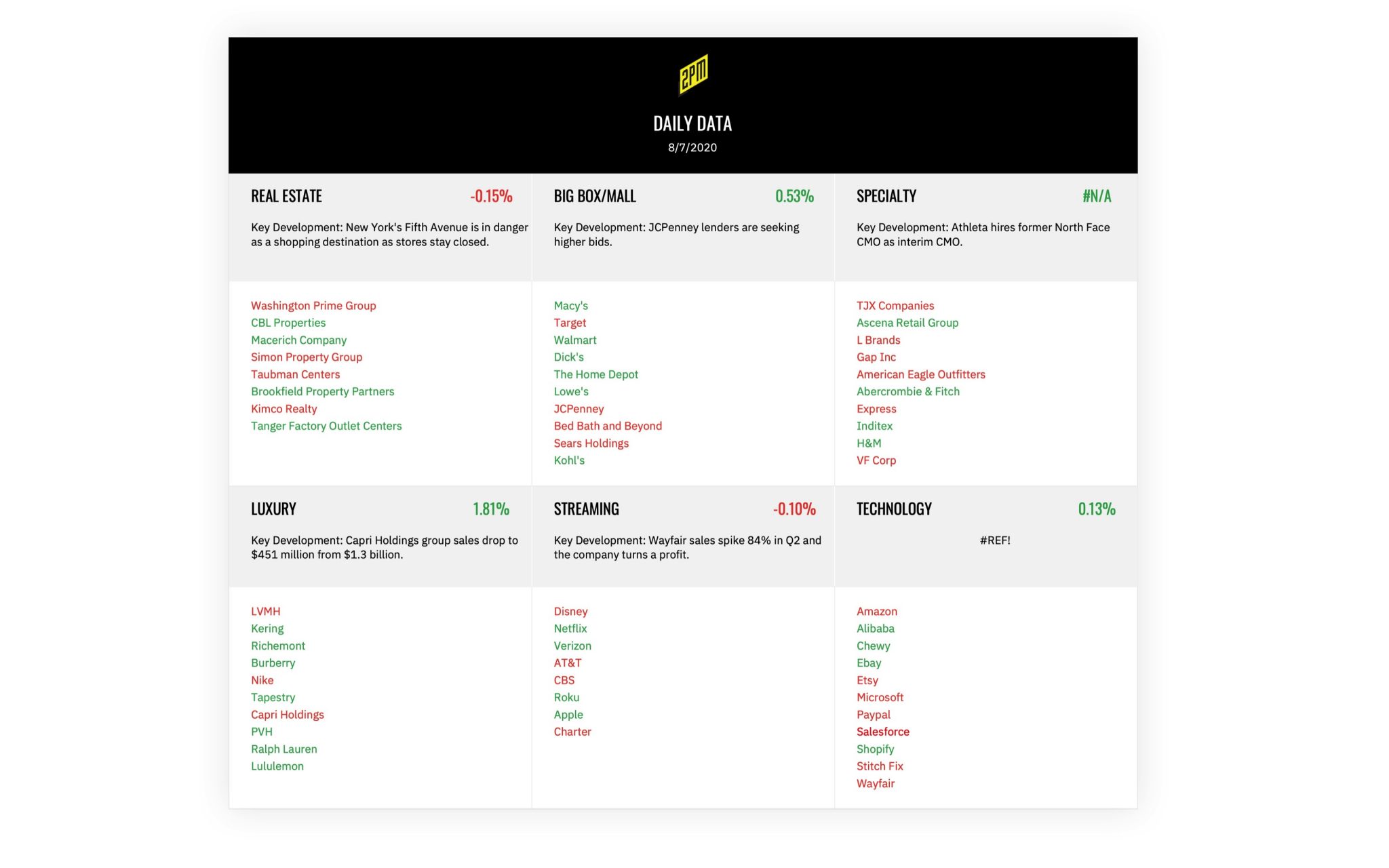

Consider the current state of retail. With malls shuttering, retailers defaulting on rents, foot traffic wavering, and closures at the mercy of state or federal officials, eCommerce has become one of the most reliable retail formats. Malls have become private equity investors in an attempt to preserve the status quo.

It’s possible [Authentic Brands Group] could do more deals with megamall owners such as Simon Property Group and Brookfield, given their track record. The three came together to acquire Forever 21 out of bankruptcy. And they all have ownership of the teen apparel company Aeropostale. Brookfield in early May said it was launching a retail revitalization program to focus on taking non-controlling stakes in retailers to assist them with their capital needs. It said it was targeting spending $5 billion on the plan. [1]

The retail real estate industry has done itself no favors with its latest attempts to calm its market. The trend of retail developers and management companies pursuing ownership in traditional brands has stabilized the market – in the short term – while piling on collateralized risk for the long term. As a result of the shift away from malls and strip centers, major brands have begun discussing their own strategies to counter an evolving retail market. Major brands have begun scouting for direct brands with the following attributes:

- a path to profitability

- a demonstrated omnichannel expertise

- an organic marketing flywheel

- a team or partnership that can continue to execute a savvy paid strategy

- founder-led with longer-term management potential

A common rebuke to the idea that DTC brands could serve as the savior to traditional retailers is also simple: their valuations are much too high. This is where the brand of DTC needs to further evolve. Frontrunning DTC brand Outdoor Voices made news this week:

On Sunday, the company announced that Ashley Merrill, founder and CEO of the women’s sleepwear brand Lunya, will become chairperson of Outdoor Voices’ board of directors. NaHCO3—the venture capital arm where Merrill serves as principal alongside her husband, Marc Merrill, the co-founder and former co-CEO of Riot Games—is making an investment in the company; Merrill declined to disclose the size of the deal. Haney, who resigned as CEO in February, remains on the company’s board. [2]

With $64.1 million raised and around $40 million earned in 2019, this announcement added to the complexity of the brand’s story, exit optionality, and its capitalization table. This is also the brand of “DTC.” But this isn’t the entire industry – just the most visible of it. Surely, with Ashley Merrill at the helm, Tyler Haney back in an active role, and a new CEO search in process: a positive outcome is more likely than it was with Mickey Drexler involved. But there are countless brands that have done or will accomplish more with a lot less press, intrigue, or funding. That variation of DTC brands may just be what major brands are looking to acquire.

Unless you frequent trade publications, it’s unlikely that you’ve ever heard of Moiz Ali, Jaime Schmidt, Chris Cantino, Tiffany Masterson, David Schottenstein, or Chase Fisher. Together, these founders’ recent acquisitions were valued at over $1.3 billion. It’s even less likely that you’ve seen aspirational business press on Bill and Caity Henniger, Evan Hafer, Mike Seguero, or Ben Francis. In each case, these founders’ brands have achieved growth that would make a venture-heavy DTC founder envy.

The Henniger’s have steered Rogue through a pandemic that depressed consumer confidence, increased unemployment, and saw a decrease in consumer spending by a reported 16%. Even so, their DTC fitness brand now employs over 900 in the Columbus, Ohio region.

The brand of DTC has evolved in a number of ways. I’d argue that the most notable has been the types of companies and founders that have been positioned as aspirational. The sentiment has begun to shift away from lionizing the founders who’ve raised $100 million to the veneration of the founders who’ve sold for $100 million. Despite the retail segment’s venture and tech origins, the DTC movement was never about building billion-dollar companies in five to seven years. The physics of that feat haven’t proven possible.

But with enough stories on Jaime Schmidt or Caity Henniger, potential founders will begin to understand that major acquisition or sustainable growth are far more admirable feats than magnificent bouts of fundraising.

I expected our daughters’ Roblox phase to end after a few months. It hasn’t. In fact, the games that they play have evolved to fit their needs. The in-game environments, games, and interactions have changed along with their levels of experience and commitment to the game. What the Roblox parallel taught this millennial dad is that any successful industry is built on five pillars: audience, transaction, engagement, evolution, and staying power. For the DTC industry, evolution and staying power are closely linked.

A retail industry with few positive outcomes has the opportunity to enjoy a period that could rewrite the media’s interpretation of its value. But to do so, the industry will have to evolve away from the venture mechanics that it’s known for. And in the process, we may begin to highlight the founders who’ve built ways to succeed without the spotlight. If we start, build, and scale more brands like the ones above, the narrative may change. And so may the brand of “DTC.”

The DTC industry is an economic bright spot upon which commercial real estate, traditional brands, and markets like Target and Walmart will depend on in the coming years. We just need more of them to finish their journeys. Then, we need to champion them – loudly – for doing so.

Memo by Web Smith | Editor: Hilary Milnes | About 2PM

Read today’s important edition: Letter No. 365