It’s not farfetched to argue that brands are capable of attracting consumer attention and commerce in ways that resemble traditional media and entertainment companies. A Vuori yoga studio would be in high demand for daily classes. An LMNT trail run series would attract enthusiasts in a number of cities known for outdoor activity. Both of these venture-backed companies share more than fitness in common; they share tremendous secondary market interest.

If given the option (even in today’s depressed secondaries market), the brand’s most avid supporters advocates, would buy shares of Vuori or LMNT or Gymshark or Liquid Death. The purchase of secondaries is an expression of brand equity, and it may be the best indicator for a brand’s market viability moving forward.

Brands and their equities are not determined solely by their retail sales. A pop entertainer’s value is not determined solely by primary market sales. If you’ve ever tried to buy Taylor Swift tickets from Seatgeek, you’ll know what I mean. Swifties, perhaps the purest expression of brand advocacy in modern entertainment, are willing to pay a premium just to be there for the show.

In the contemporary marketplace, brands have evolved to become much more than mere purveyors of products or services; they are, in many ways, entertainers. This reality is particularly evident in how consumer engagement and brand experience play central roles in shaping customer perceptions and loyalty. Just as a blockbuster show or a high-profile concert captivates an audience, successful brands like Vuori, Shein, Skims, Faherty, Whoop, and LMNT enrapture many of their customers. These brands leave customers wanting more from them, leaving open the idea of creating immersive and emotionally resonant experiences for then.

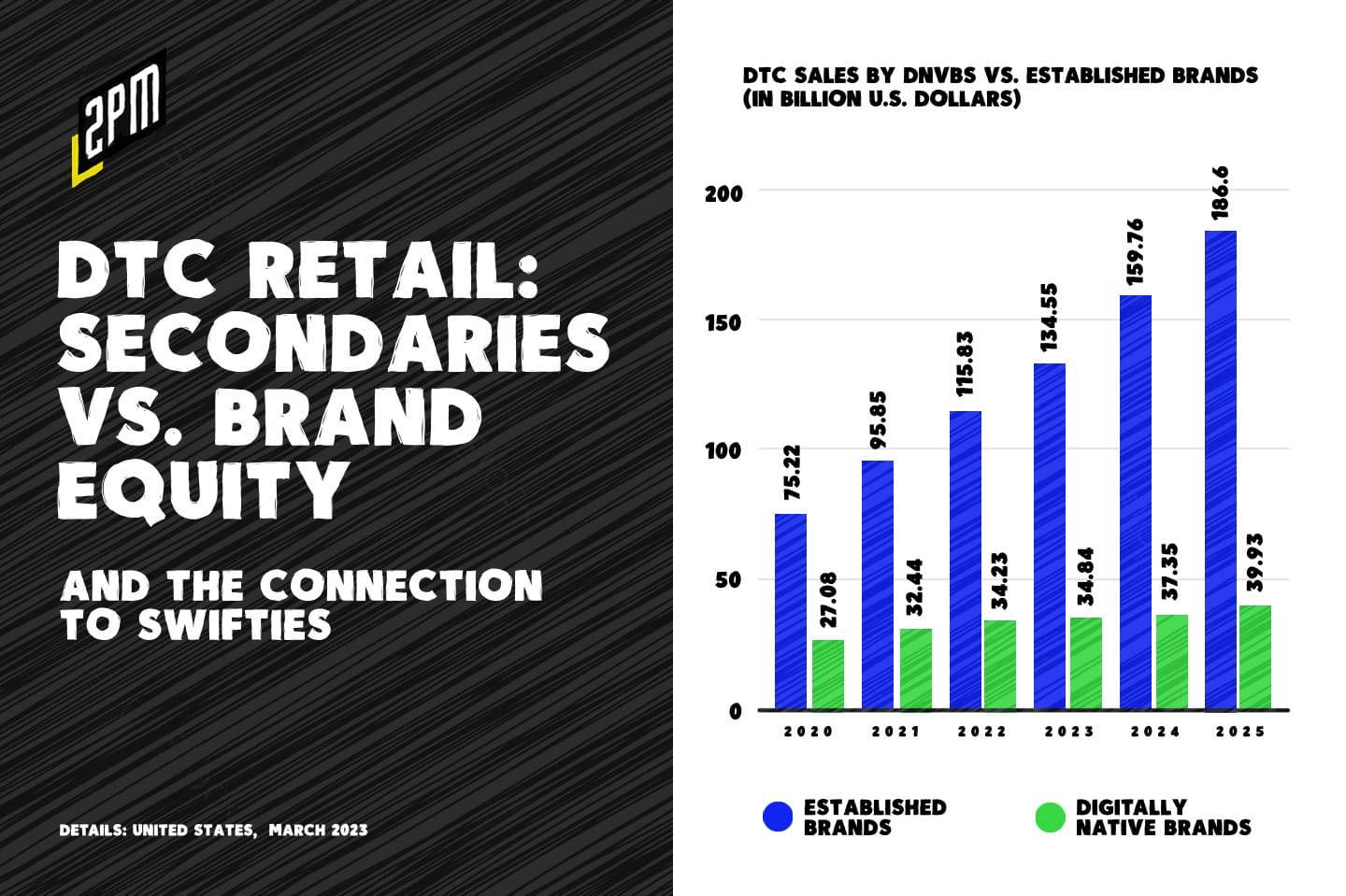

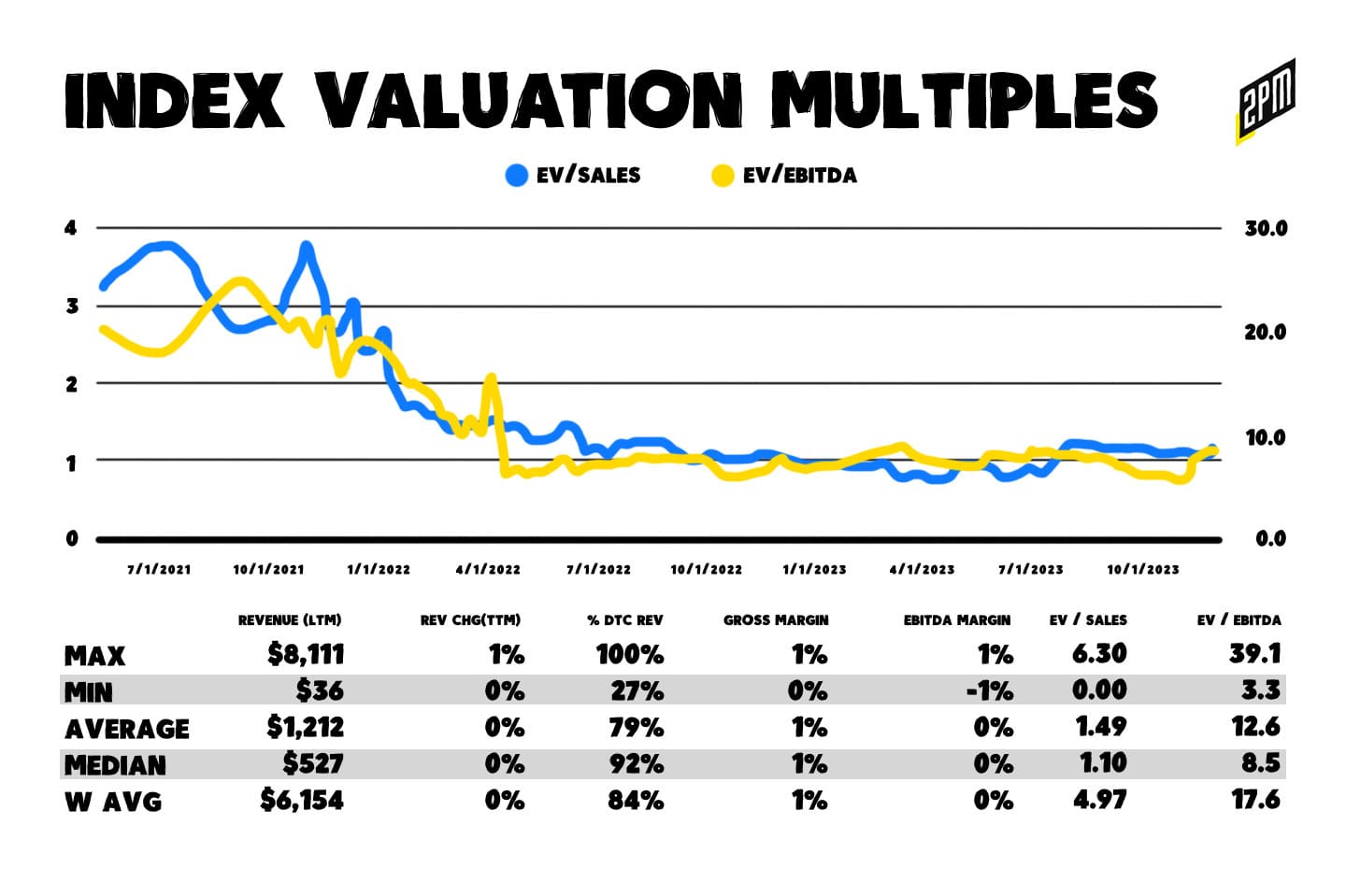

This extends into the realm of financial valuations. For the aforementioned brands, a cross section of extraordinary DTCs, their secondary interest can be likened to after-market ticket prices for major entertainment events. Across the market, valuation multiples in DTC are depressed according to the Drivepoint index that includes: Lululemon., Yeti, Canada Goose, Purple, Hims, Solo Brands, FIGS, Brilliant Earth, Lulu’s, Allbirds, and Laird Superfood Inc. But according to a recent report by Carta, secondary interest in internet-based companies till remains high.

A plurality of startups conducting liquidity programs so far this year on Carta have been in the SaaS sector, which is in line with historical norms. Two other sectors have seen substantial increases in their share of secondary activity: About 23% of deals so far this year involved internet & media companies, up from 18% for the full year 2022. (H1 Report – Carta)

But while this is an indicator of industry health, it is somehwat Carta added: “When the percentage of employees who are sellers declines, the percentage of sellers who are founders and investors increases.” In the context of the ratio of employee offering to founder offering, “Back in H1 2021, nearly seven out of every eight sellers was an employee.” That rate fell to three out of four in H1 2022, and it indicates a reflection of market appeal and the level of excitement a brand generates among investors, akin to a must-see show that draws crowds willing to pay premium second-market prices for the experience.

A barometer for brand equity: what’s the brand’s secondary market like? If the answer is non-existent, it could be a cause for concern. A brand advocate should always want behind-the-scenes access to the top brands.

Just as a sold-out concert or a hit Broadway show signifies high demand and popularity, robust and rising secondary interest in the private market signal a brand’s strong position and the high regard in which it is held by investors. These prices are not just numbers; they represent the collective anticipation and enthusiasm of the brand’s future in the market, mirroring how audience demand drives up ticket prices for a hit entertainment event. While not representative of a secondary market, we commonly see this stock vs. product purchase discussion in the context of Tesla. A Reddit thread on the psychology of this situation is fascinating:

Based on my current behavior, I would rather invest in the company…really want one of the cars though, just not enough to sell the stock.

Or this one:

I have 643 shares of Tesla and don’t own a Tesla. I have a Toyota Tacoma (paid off) and will keep that until the new quad CyberTruck comes out. I will definitely be purchasing that.

When this pattern of thinking is considered, the dynamics of private stock trading become a barometer of a brand’s ‘star power’ in the market. Brands that successfully engage and entertain their audience – with innovative products, compelling marketing, and strong customer relationships – see their ‘ticket prices’ rise, reflecting their desirability and success. Conversely, brands that fail to captivate an audience, much like a lackluster show, might find their secondary interest languishing, indicative of waning investor interest and market appeal. Consider this quote from the Academy of Business Research Journal. There, in 2017, Wei Feng examined the relationship between a firm’s brand equity and its investment value:

Stocks with deteriorating brand equity generally feature lower return potential.

Why do we only consider this with respect to public stock value? Combining the concepts from the business journal review on brand equity with the discussion about secondary stock sale interest for private companies reveals an intricate correlation between increased brand equity and secondary market interest.

High brand equity often translates to a strong, favorable, and unique presence in the consumer’s mind, which can significantly influence their purchasing decisions. Here are three correlations:

Brand Awareness and Equity: The journal article indicates that brand awareness, encompassing recognition and recall of a brand, plays a pivotal role in building brand equity. A private company with high brand awareness is likely to be more recognizable in the market, attracting investor attention. This awareness, especially in the upper echelons of DTC brands, signifies a strong market presence and suggests a robust potential for growth and profitability – key factors that make the company’s shares attractive in secondary markets.

Brand Image and Equity: A positive and strong brand image – comprising attributes, benefits, values, culture, personality, and user type – directly contributes to enhanced brand equity. For private companies, a compelling brand image can be a decisive factor for investors in secondary markets. A favorable brand image often reflects a company’s stability, market strength, and potential for long-term success, making its stocks a desirable commodity in secondary transactions.

Sales Promotions and Equity: Effective sales promotion strategies, both monetary and non-monetary, can bolster a brand’s market presence, directly influencing its equity. For private companies, innovative and successful promotional strategies can signal market agility and consumer appeal, traits that investors seek in secondary market transactions.

When it comes to secondary stock sale interest, this is where the concept of brand equity becomes even more crucial for private companies. High brand equity suggests to potential investors that the company has a strong market position, loyal customer base, and significant growth potential, making its shares a valuable investment.

On platforms like Hiive Markets, Forge Global, and Equity Zen, where secondary transactions for private companies occur, the level of activity and interest in a company’s shares can and should be measured as a data point. Active trading is itself a product offering and can signal strong brand awareness and a positive brand image, suggesting overall robust brand equity.

Summary: For private companies, the interest in secondary stock sales is closely correlated with the brand equity, which is a composite of brand awareness, brand image, and the impact of sales promotions. Strong brand equity not only enhances a company’s standing in the eyes of consumers but also elevates its attractiveness to investors in secondary markets, thereby influencing the liquidity and perceived value of its shares. It can be a virtuous cycle.

In the modern era of branding, where customer engagement is paramount, brands must think and act like entertainers, constantly seeking to captivate and delight their audience. They should also expand their definitions of what a customer is to a brand. A retailer’s ability to do so is not just a matter of market strategy but is directly mirrored in the valuation of their secondary interest. And like a Swiftie’s desire for a ticket at almost any cost, the higher the perceived brand-as-entertainer value, the more customers will be willing to invest. The effort to assess and publish secondary interest in top brands should become a priority, it should become as common as any other subjective measure of equity.

By Web Smith | Editor: Hilary Milnes with art by Alex Remy

Editor’s Note: to join this memo, we’ve added a study to the DTC Power List. For the new feature on polled secondaries interest, we combined a poll (n=97) with internal data on this update’s top 250 brands to assess whether those polled and others would pursue an interest in secondary stock sales from employees, founders, and / or existing shareholders of the retailers mentioned. We weighted the poll as 90% of the the assessment and we plan on growing the list to the full 800+ in the coming weeks. As mentioned above, interest in purchasing secondaries is a positive indicator for the current brand equity, potential brand equity, and current financial health of the retailers mentioned.