Этот краткий обзор предназначен исключительно для Исполнительные членыЧтобы упростить членство, вы можете нажать на кнопку ниже и получить доступ к сотням отчетов, нашему списку DTC Power List и другим инструментам, которые помогут вам принимать решения на высоком уровне.

No. 338: UpWest and Hygge

A publicly-traded retailer launched a DTC brand. This is a deep dive into their reasoning, the build, and their internal expectations.

Middle-class retail is at an impasse. Since the beginning of 2019, there have been 19 bankruptcies to include Forever 21, Gymboree, Charlotte Russe, Payless ShoeSource, Diesel, and Destination Maternity. And there are another eight retailers at risk to include: J.C. Penney, Neiman Marcus, J. Crew, and Hudson’s Bay. In Gilded Age 2.0, I explain that our current retail era signals a casualty of the middle class consumer; a class that once emerged in response to the industrial and financial booms of the late 19th century and the governmental reforms of the mid-20th century.

With a flailing gig economy, stagnant wages, and rising personal debts, 2019 presents a break from the mid-century momentum that defined the 20th century. We are beginning to hear faint echoes of an earlier time of boom or bust and feast or famine. Rather than appealing to pure luxury consumers or fast fashion-loving millennials, the “long middle: erroneously remains the bullseye of the target. Retailers have been slow to optimize for a new market of coveted consumers.

In a recent report by Business of Fashion proclaimed that America still doesn’t have an answer to LVMH. They explain:

Spoilt for choice, consumers are less interested in mid-priced products available at scale: they want dangerously affordable fast fashion or pure luxury. (And preferably at a discount.) It’s harder for consumers to see the value in something that is not cheap but not that expensive, either. Especially if it’s not utterly unique. That’s a problem for Tapestry in particular, which deals exclusively in accessible luxury. [1]

Against the backdrop of abundant choice and a bifurcating market, Ohio retailer Express launched a new brand. Express is currently trading at a $265 million market cap with north of $2b in sales. The cost of that revenue is extraordinarily high compared to healthier retailers. Trailing twelve months, Ralph Lauren Corporation earned north of $6.5 billion with a $2.45 billion cost of revenue.

In contrast, Express earned (TTM) north of $2.1 billion with a $1.5 billion cost of revenue. A 25% gross profit margin heading into a crucial holiday season, the Columbus-based retailer hopes to use the DTC initiative to improve their long-term outlook. The effort has been met with a mix of pessimism and optimism.

Pierre Kim of Away:

For years, retailers have been criticized for not evolving quickly enough to meet the demands of their customers, so what do they have to lose with this new strategy? Their core labels may be faltering, but they still have brand equity. Why not use it to experiment and launch new businesses? [2]

Paul Munford of Lean Luxe:

There’s baggage associated with being under a legacy retailer’s umbrella—it decreases the value of the brand to the savvy consumer,” he said. “However, execution will always ultimately be the key here. Spinoffs need to feel like their own entity, as opposed to a sub-brand of the legacy retailer. [2]

There are merits to both arguments. And a little bit of digging provided more clarity for this report. Under the umbrella of Les Wexner’s Limited Brands, Express launched as women’s clothier “Limited Express” in 1980 Chicago. Led by CEO Michael Weiss, the brand expanded to eight stores in 1981 and by 1986, Express began a test for menswear in 16 of its 250 stores. The men’s line spun out as Structure in 1989.

I remember the brand very clearly. As a twelve year old in 1995, the halls of my middle school were split between the haves and the have nots. For the ones with, shirts by Polo and Structure were the daily wears and all I could remember is the sensation of having neither.

The advancements that Express made during that 20 year run are astounding to think about. In 2001, Express became a dual gender brand – a pivot that Madewell is currently attempting to execute. Structure “sold” to Express, or at least that’s how I remembered it. Because immediately, I became a fan of Express. In actuality, the brand was owned by the same holding company. It funneled its mens business to a brand that provided more opportunity. L Brands then, quietly, sold the mark to Sears in 2003. The Structure brand was never heard from again.

Express is no longer owned by L Brands, one of the most prolific builders of retail brands in history. It was sold to Golden Gate Capital Partners, a private equity firm with $15b in assets under management. And then, in May of 2010, the retailer went public.

Demographic vs. Psychographic | Part Two

In 2016, Express made its first play for the direct-to-consumer era by acquiring a minority stake in HOMAGE, the Columbus Ohio retailer led by founder Ryan Vesler. It’s a genuine brand, one where the founder-product fit is as valuable as its product-market fit. The minority investment with vintage t-shirt company meant that Express bought a new audience of a key demographic: the college-aged millennial.

Homage President Jason Block said in an email that Express will consult with the company on an ongoing basis and the investment will allow Homage to expand both its digital and brick-and-mortar presence. [3]

Aside from investing in a growing company, Express gained the rights to include a limited selection of HOMAGE products in store. The investment was intended to bolster foot traffic while, potentially, benefitting from the long-term flip – if and when the HOMAGE brand grew with the help of Express. It’s unclear whether or not this initiative was successful for either of the brands. The company is currently trading below the price it maintained during the period that Express began its partnership with HOMAGE. The publicly-traded retailer’s missteps over the past two years were due, in part, to a number of macroeconomic shifts. The launch of UpWest represents a strategy shift of its own.

In Psychographics in Focus, I explain the difference between a demographic and psychographic. Consumer psychology involves the interest in lifestyle, behavior, and habit. It’s an encompassing measure that considers our idiosyncrasies, our temperament, and even our subtle personality traits. These are the variables that influence our behavior as consumers. Psychographic segmentation is the analysis of a consumer cohort’s lifestyle with the intent to create a detailed profile. [4]

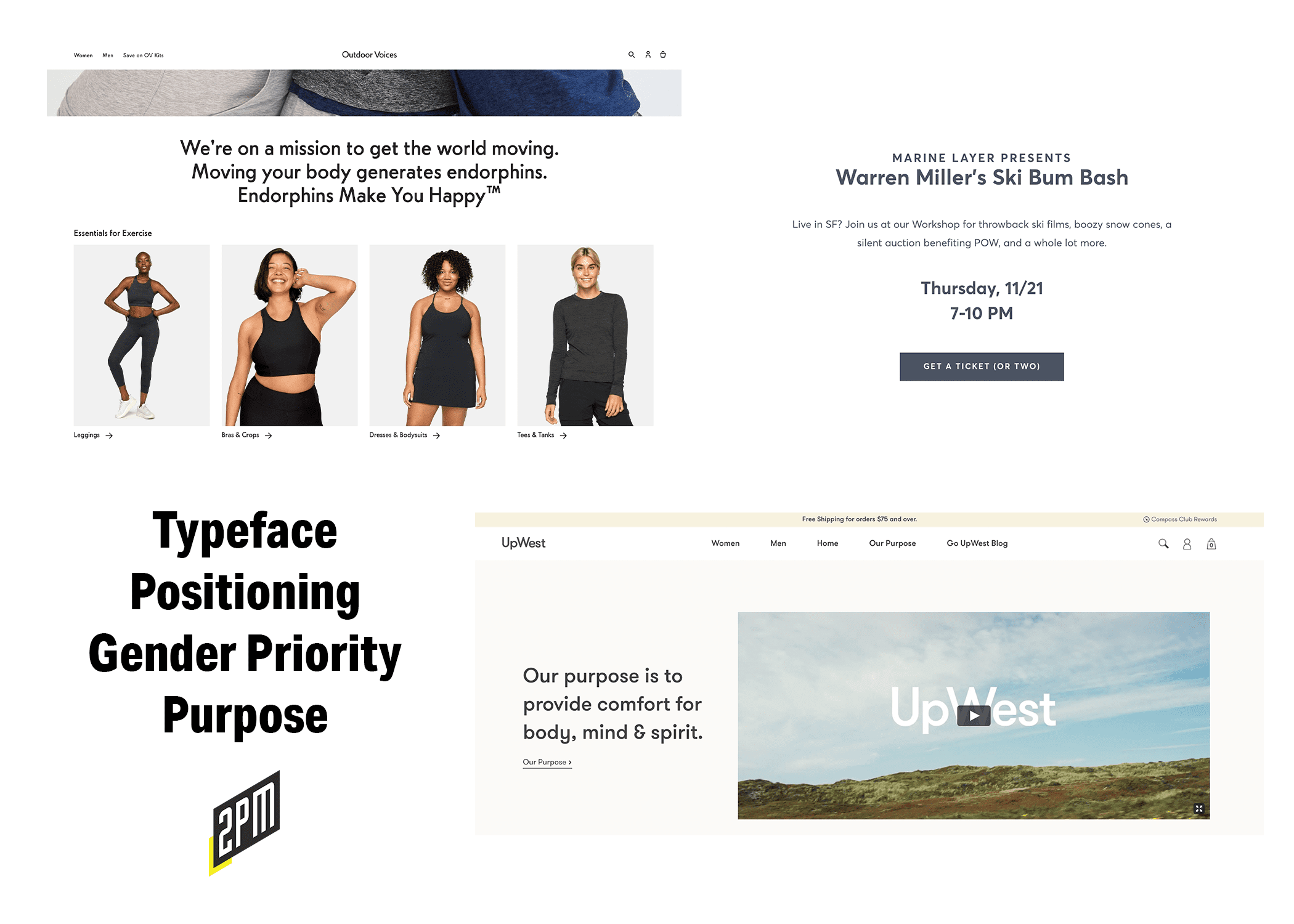

Taking a community-building approach, UpWest plans to connect with new customers through experiential events, including a regional tour across the US that features the UpWest Cabin, a mobile pop-up exhibit featuring relaxation-focused experiences like yoga and meditation classes. Slated stops include Columbus, Chicago, Nashville, Denver and Austin. [2]

From the typeface, to the story-telling, to the merchandising – the UpWest brand is designed to attract fans of the digitally-native industry. Rather than a specific demographic, Express pursued an interest (DTC) and is building a brand atop of that engaged audience.

DTC As A Psychographic

Веб Смит в Twitter

DTC, 2012: a tech stack strategy. DTC, 2016: a logistics strategy. DTC, 2020: a brand strategy.

In a span of three days, I received multiple emails and texts from contacts close to the launch of UpWest. Kaleigh Moore, Forbes writer and 2PM collaborator had a story in queue by then. In the Lean Luxe Slack, it was a topic of conversation. Rather than building in-house with Express’ existing engineering group, UpWest contracted Shopify agency BVAccel to handle the design and development work. This was a nod to several of the most successful digitally native brands in the space to include Untuckit, Cubcoats, Chubbies, and Rebecca Minkoff.

The site’s architecture communicates a desire to be mentioned in the DTC conversation, this includes UpWest’s partnership with Klaviyo and its new-age loyalty program. It would appear that UpWest chose to focus on the DTC psychographic for the sake of earned media and brand positioning. As far as the nuts and bolts are concerned, the site’s build communicates that the desired target demographic is millennial-aged women. On day zero, the brand has an explicit purpose: to provide comfort for body, mind, & spirit. The clothes, are priced similar in design and price to Marine Layer – its next closest competitor.

Identifying Waves: Importing Hygge to America

In the past year, this concept of Scandinavian coziness has made inroads with an international audience. [5]

Imagine a whiteboard in one of Express’ suburban Columbus boardrooms; the word “hygge” would have been at the center of it in big and bold lettering. You can picture the brand’s chief comfort officer (and Express’ SVP of Strategic Initiatives) standing in the corner of the room, jamming as Cody’s It’s Christmas plays on the room’s four Sonos speakers. The brand wants you to feel a feeling. Analysts agree. Emily Singer, founder of the DTC newsletter “Chips and Dip” had this to say:

There’s something very boring about it. Maybe that’s intentional. This line feels a little too on the nose: ‘Welcome to curated comfort. For those who are seeking peace and calm in a stressful world.’ Brands tap into emotional states, but it’s rarely laid out so explicitly.

It’s this perceived boredom that is viewed as an understated luxury in American culture. To the Danes, hygge is free of economic status. The culture’s entire focus is on practicality, movement, wellness, and mindfulness. It’s this underlying culture that Express hopes to import with the help of some obvious visual cues from well-known DTC retailers.

The UpWest typeface is nearly identical to the typeface of Outdoor Voices and Marine Layer’s. Ironically, both retailers have references to Scandinavian hygge throughout their brand messaging. But for UpWest, there’s no understatement. Every message is turned to maximum volume. Like the primary header of Express.com: UpWest’s primary menu is a throwback to “Limited Express”, a retailer for women-first and men-second. There are elements of luxury abound. Upwest’s blog features new-age terms like: nourish, mindfulness, tranquility, and sanctuary. The traveling pop-up is a “cabin.” These are all symbols of wealthier millennials with time and resources to spare. As is the concept of philanthropy and sustainability (though UpWest sells products that are made with synthetics).

It starts with our cozy apparel, home and wellness products. We want to surround you with calm and give you balance. But it’s not just the tangible things. It’s also about slowing down. Diving deeper. And giving back.

Not to be outdone, UpWest wants consumers to help them donate $1 million to the Mental Health Association. The Express-borne retailer plays the entire DTC hand of cards. This report began with a simple statement: middle-class retail is at an impasse. To the average consumer, this DTC play is akin to Structure being launched as Express Men. Like a sheep, the seventeen year old me bought from Express as soon as my adolescent wallet would allow. The mechanics are similar here. Express is attracting an existing audience (the DTC psychographic) and using it to invigorate a brand that is plateauing.

Заключение

The UpWest bet is that the retailer can earn the business of the upwardly mobile DTC audience by engineering a product-market fit. One with heavy branding, ideal-alignment, and market messaging. This is one of the first upmarket attempts that we’ve seen from a specialty retailer. It’s one that deserves praise. Their management team engineered a brand with contemporary pricing and luxury messaging – void of pricing promotions (for now). They’ve acknowledged that the data shows a middle-class at an impasse. They have the supply chain, the logistics, the distribution, and a snapshot of a brand. But do the executives at Express truly understand what makes the top DTC brands work? That remains the question that could move the market.

Time will tell if Express can duplicate the brand architecting of their L Brands era – a time defined by face-less brands, clever signage, billboards, and foot traffic. My guess is that Express will find an audience that is more sophisticated and critical than the young adults of the 80’s, 90’s, and 2000’s. Messaging, distribution, and customer acquisition methods will evolve with this realization. And if that’s the case, their hygge may be tested for quite some time.

Research and Report by Web Smith | About 2PM

Краткая информация для пользователей: НАСА, Луна и Джеффри Стар

Этот краткий обзор предназначен исключительно для Исполнительные членыЧтобы упростить членство, вы можете нажать на кнопку ниже и получить доступ к сотням отчетов, нашему списку DTC Power List и другим инструментам, которые помогут вам принимать решения на высоком уровне.