Некогда малоизвестный бренд, расположенный недалеко от Далласа (штат Техас), превратился в модель поколения, демонстрирующую, как ведется бизнес, создаются бренды и достигается ликвидность для заинтересованных сторон. Основанная в 2010 году и торгующаяся сегодня на бирже $DTC с рыночной стоимостью около 500 миллионов долларов, компания Solo Brands имеет исключительную историю.

The maturing of Solo Brands is as a masterclass in strategic expansion and fiscal diligence. While many navigate the turbulent waters of the DTC marketplace, Solo Brands has set a gold standard, embodying a synergy of vision, cooperation, fiscal responsibility, and an understanding of its target customer. And they’ve just made their latest acquisition.

The company started as Solo Stove, a portable fire pit retailer, and evolved into a powerhouse of diverse outdoor brands. Their acquisition strategy stands testament to their understanding of who buys their products. By integrating brands such as IcyBreeze Cooling, they’ve not only augmented their product line but also enhanced the holistic experience for their consumers. The company’s genius in curating complementary and diverse offerings, and capturing the essence of outdoor adventures, is not novel. However, it is novel at the relatively early stage at which Solo Brands is operating. Thirteen years after its founding by brothers Spencer and Jeff Jan and bootstrapped since inception, the company has risen to a level that other brands can only dream of.

In 2016 it was still just my brother and me — no employees. We didn’t have an office; we worked out of our homes. We used third-party fulfillment providers and other vendors for various tasks. We wanted a lifestyle business, one that offered a balance for careers and time to ourselves. By 2016 the company was growing beyond what we had envisioned. […] So in 2016 we started exploring a sale. But the response came back that the business wasn’t salable since we had no employees, staff, or systems. A buyer couldn’t step in and keep it growing. We spent the next three years building a company to sell. That was our focus. (Practical eCommerce)

What truly sets Solo Brands apart is its unwavering commitment to the consumer. More than just selling products, they invest in sincere market needs; it’s in the company’s DNA. By focusing on forging genuine consumer connections, they’ve successfully transformed one-time purchasers into loyal brand evangelists. The burgeoning popularity of products like IcyBreeze, revered by renowned events and global influencers, is a glowing endorsement of Solo’s dedication to quality and consumer satisfaction.

Financial acumen is the other separator for Solo Brands. Their alliance with Generational Equity is a testament to their vision and commitment to fiscal prudence. Operating with discretion and strategic foresight, Solo Brands ensures that every financial move, every acquisition, is a carefully choreographed step towards sustainable growth.

In today’s digital era, a brand’s reach determines its success. Solo Brands, in its pursuit of ubiquity, has crafted a multifaceted distribution model. This tapestry of eCommerce platforms, strategic wholesale partnerships, and physical storefronts ensures they’re omnipresent and catering to consumers across diverse touchpoints.

The power of synergy shines brightly in Solo’s approach to brand integration. Brands like Chubbies, Oru Kayak, and ISLE, while distinct in their offerings, coalesce seamlessly under the overarching vision of Solo Brands. This harmony ensures that while each brand retains its individuality, they collectively cater to the myriad facets of the adventurous lifestyle. That list of offerings recently grew by one, further cementing Solo as a destination for well-built, profitable, niche-drawn DTC brands:

IcyBreeze, based in Sweetwater, Texas, has carved a niche in manufacturing and direct-to-consumer distribution of personal air-conditioning and heat relief solutions. The pioneering firm said its products combine a portable AC’s efficiency with an insulated cooler’s convenience. (Dallas Innovates)

Leadership, they say, determines the fate of a venture. Solo Brands’ monumental success can be attributed to its leaders, both pre- and post-private equity majority ownership. At every stage, the company’s leader steered the ship with precision and passion while maintaining the venture’s original inspiration. Their astuteness in facilitating strategic collaborations, as evidenced in the partnership with IcyBreeze, showcases their expertise in harnessing collective strengths for shared success.

Innovation is a core tenet of Solo Brands. Their commitment to breaking new ground is evident in their association with pioneering products, be it Oru Kayak’s groundbreaking designs or IcyBreeze’s unique cooling solutions. This constant push for innovation ensures Solo remains not just relevant but a trendsetter in an ever-evolving marketplace.

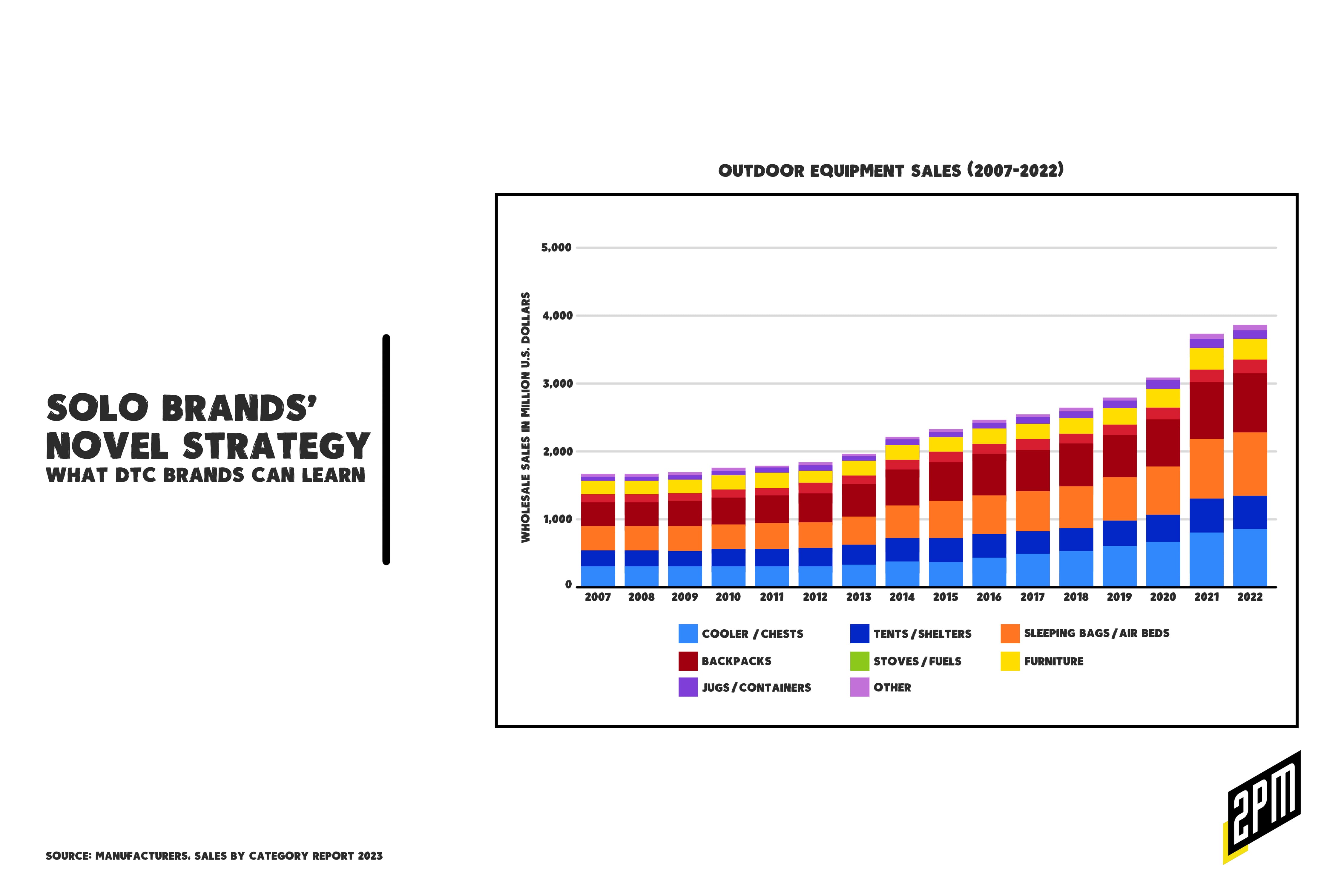

Yet, even as Solo Brands continues its rise, another potential avenue beckons: shared financial services. Despite Solo’s public push for more and better retail spaces (see below), the company still purports to earn upwards of 70% of its volume through DTC channels.

Since consumers are seeking more in-person experiences, Dick’s Sporting Goods aims to utilize its physical presence and introduce a contextual commerce experience in its brick-and-mortar stores. The company intends to expand by introducing 20 new Dick’s House of Sport concept stores, which offer rock-climbing walls, batting cages, and putting greens to enhance the customer experience. (PYMNTS)

Such a unifying product as a shared financial service could revolutionize the consumer experience for most brands, but especially a savvy aggregator like Solo Brands. Imagine a Solo co-branded credit card or a consolidated loyalty program, offering incentives across all of Solo’s brands. This would not only elevate sales but further deepen brand loyalty. Such integration could provide unparalleled insights into consumer behavior, enabling Solo to tailor experiences, offers, and products with pinpoint accuracy. Furthermore, these shared services could enhance brand cohesion, reminding consumers of the interconnected ecosystem that Solo Brands offers, catering to every nuance of their outdoor lifestyle.

In the grand tapestry of DTC brands, Solo Brands stands tall, a luminous beacon of strategic prowess and fiscal wisdom. Their journey, replete with lessons on growth, diversification, and consumer engagement, is a playbook for brands across the globe. As the narrative of Solo Brands continues to unfold, their legacy serves as a testament to clear leadership, innovative strategy, and unwavering commitment to an underserved target consumer.

Веб Смит | Редактор: Хилари Милнс с иллюстрациями Алекса Реми и Кристины Уильямс