On aluminum, the war economy, and the consumer brands that will not survive the next five years. This essay is a feature post for the NATSEC @ 2PM briefing series.

I was in the Carolinas, earlier, when the conversation in a small meeting turned to aluminum, and not in the way it turns at a beverage conference. This was not packaging weight, sustainability narrative, or the standard pieties of the can. The room was a small one, a glass table and the kind of muted hospitality that signals money is in the process of being moved, and someone at the end of the table, defense-adjacent in the way that certain operators are now, laid out what they were modeling on a five to seven year horizon. The following was attributed and cleared accordingly.

The model was designed against a thinned smelter base, munitions replenishment, allied stockpiles, the per-unit aluminum content of a Tomahawk against a Patriot interceptor against a loitering munition flown out of a shipping container by a defense-technology startup that did not exist in 2019.

The horizon, a word repeated more than once, was five to seven years.

I have heard a lot of forecasts in commerce, and most of them are a performance of optimism for an audience that has already paid to hear them. This one was not. It was the math of a strategic input being absorbed by a buyer that does not negotiate, on a timeline long enough to matter and short enough to act on, and I have not stopped thinking about a twelve ounce can since.

The story has a shape, and the shape is older than the industry it threatens.

The Read From the Chart

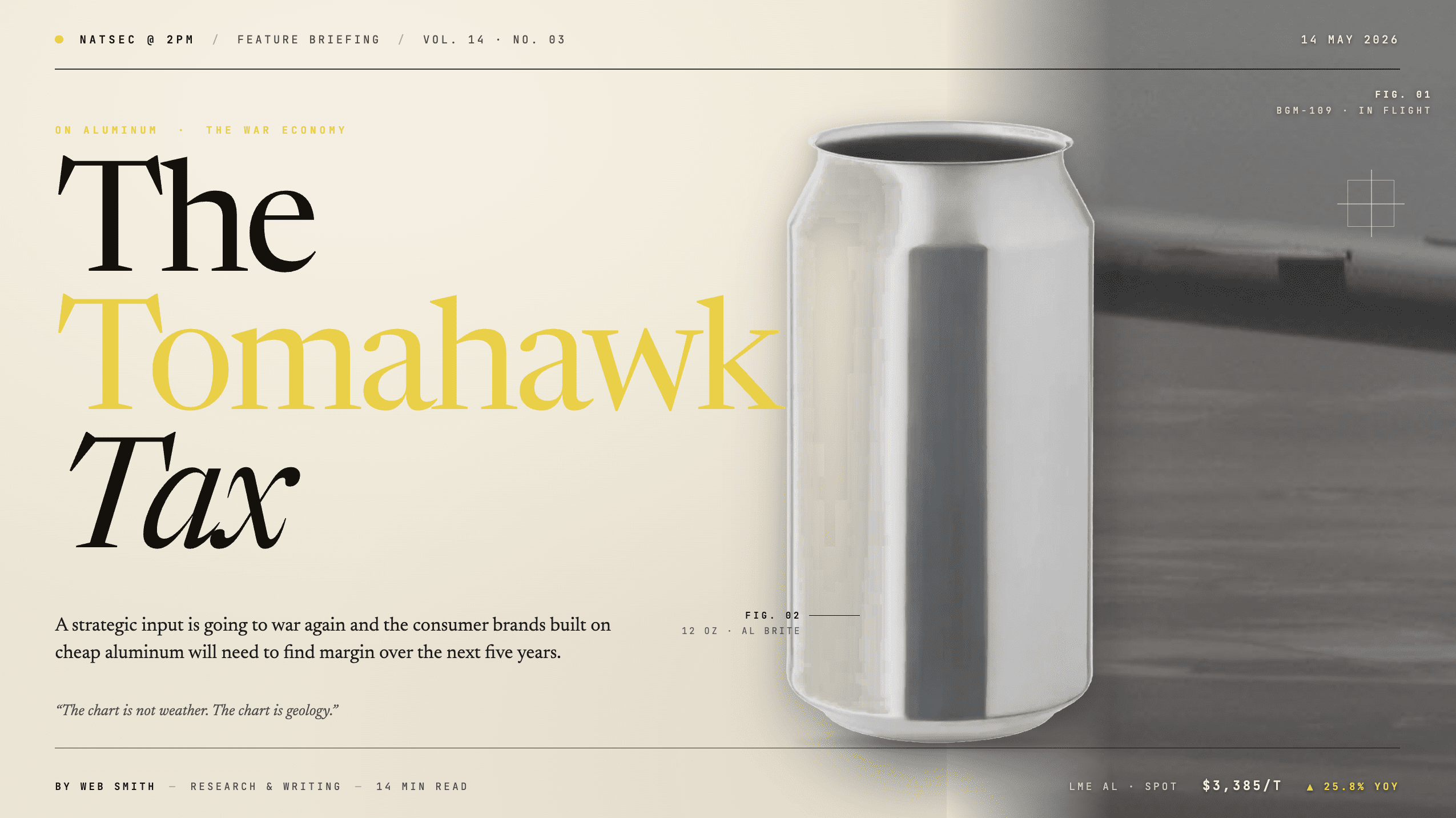

The number, as of the most recent close on the London Metal Exchange, is roughly $3,385 per tonne. The chart on Trading Economics is a four-year line of memory: an all-time high of $4,103 in March of 2022 when Russia entered Ukraine and a different commodity scare ran through the global supply, a long drift through the back half of 2023, and a steep ascent through 2025 and into the first quarter of 2026 that has carried the price up 25.84 percent against the same week last year and up 9.14 percent against the prior month. The same model puts the twelve month forward at approximately $3,616 per tonne, which is to say within reach of the 2022 high.

Three forces are pulling on the chart, and they are not the kind of forces that resolve themselves through a single quarter of resupply.

The first is acute and geopolitical. In March, Iran struck targets across all six Gulf Cooperation Council states in what the United States and Israel have referred to as Operation Epic Fury, and the operational consequence for global aluminum has moved faster than the consumer press has reported. Qatar halted its joint refinery operation with Norsk Hydro, Bahrain’s Alba declared force majeure on all deliveries, and roughly ten percent of global primary supply now sits in a region operating under siege conditions, with LME and COMEX inventories already near record lows before the strike package was authorized. The market response was not panic. The market response was reprice, and the reprice has held.

The second force is structural. China, which produces approximately sixty percent of the world’s primary aluminum, has imposed an annual production cap of 45 million tonnes, a self-imposed ceiling designed to manage overcapacity and the carbon profile of its heavy industrial sector. Indonesia, which has been the consensus answer to the question of marginal capacity, is constrained by energy costs and by a regulatory regime that has made greenfield smelting more difficult rather than less. There is, in other words, no swing producer of consequence, and the absence of one is the condition the market is now pricing.

The third force is political and domestic. The fifty percent tariff on imported aluminum, including imports from Canada, which has been the largest source of beverage-grade can stock in North America for decades, passes through to packaging in the kind of penny increments that look modest on a slide and feel structural on a profit and loss statement. Zevia, which is publicly traded and therefore obligated to disclose what private competitors can keep quiet, has booked an incremental $5 million in 2026 aluminum costs attributable to tariffs alone. That is one mid-cap brand making one disclosure on one quarter, and the disclosure scales across a category that has been built on the assumption of cheap, abundant, recyclable, infinitely available aluminum.

The chart is telling operators something the salesforce cannot, and the operators in the Carolinas were listening to it.

A Reminder From 1941

The first time aluminum became geopolitics, it nearly cost the United States the war, and the history is worth a careful read because the architecture of the problem is more familiar than the trade press tends to remember.

In 1939, Germany was the world’s leading producer of primary aluminum, and the Reich had built that capacity through a combination of domestic investment and cartel agreements to which Alcoa, the American monopolist of the period, had been at least a tolerant participant. R. S. Reynolds, the foil entrepreneur, traveled to Europe in the same year, saw what he saw, and came home alarmed enough that he mortgaged his existing foil plants to fund new smelters in Listerhill, Alabama and Longview, Washington, because he could not move Washington fast enough to do it for him.

By the time of Pearl Harbor, the United States had a problem the records describe in plain language. Glenn L. Martin required roughly 16,000 pounds of aluminum to build a single medium bomber. President Roosevelt’s plan called for 50,000 aircraft per year. That math required 400,000 tonnes of capacity, and Alcoa had committed to 187,500. The Secretary of the Interior at the time, Harold Ickes, told the press, plainly, that if America lost the war it could thank the Aluminum Corporation of America.

What followed is the part of the story that the contemporary business histories tend to skip, and it is the part that matters most for the present analysis. The federal government did not negotiate with the monopoly; it built around it. The Defense Plant Corporation broke ground on three new smelters in the Pacific Northwest, the Bonneville Power Administration appropriated $2 billion to multiply the generating capacity of the Columbia River hydroelectric system by a factor of six, and one well-cited estimate credits Grand Coulee power alone with producing the aluminum in one-third of the American aircraft built over the course of the war. Reynolds, using a Norwegian process that Alcoa had refused to license under cartel discipline, added 450,000 tonnes of capacity inside U.S. borders during the war years, and Aluminium Limited added another 300,000 in Canada. By 1941, U.S. primary production had crossed one million tonnes for the first time in history, and by 1945 the Supreme Court had ruled that Alcoa had monopolized the American market and ordered its remedy.

The lesson, preserved in the institutional memory of the Office of the Secretary of Defense industrial base shop and in a small handful of business school case studies, is that aluminum is not a commodity in the way that wheat is a commodity. It is a strategic input, and when the country requires it, the country acquires it. The price you pay for a can is the residual of what the country did not need in a given quarter, and that residual is the variable that the operators in the Carolinas were attempting to model.

We are about to relearn the lesson, and the relearning is already underway.

The Replenishment

The Pentagon’s Munitions Acceleration Council, which is a body that did not exist three years ago, issued a memo at the end of April naming fourteen “critical” munitions for fast-tracked, multiyear procurement, and the list reads like the inventory of a campaign that has been spent down to the studs. Twelve of the fourteen are legacy systems: Patriot PAC-3, Standard Missile-3 Block IB at $896 million for fifty-two missiles and components, Standard Missile-6, Tomahawk in two variants, AMRAAM, JASSM, LRASM at $473 million split across the Air Force and the Navy, and THAAD. The remaining two are emerging systems: a low-cost containerized cruise missile program in which Anduril, CoAspire, Leidos, and Zone 5 will collectively produce more than 10,000 units beginning in 2027, and Castelion’s hypersonic Blackbeard, contracted under terms that require a minimum of 500 missiles per year once testing validates.

The 2026 spending bill funds the list at $6.3 billion, which is $1.9 billion above the administration’s original request, with multiyear procurement authority running through fiscal year 2032. Another $500 million is appropriated for solid rocket motor industrial base expansion, workforce development, and supplier qualification. An additional $2 billion was added to the $25 billion reconciliation tranche allocated last summer. The total U.S. defense budget for 2026 is approaching $1 trillion, which is approximately 39 percent higher than 2021, and NATO defense expenditure is now estimated at $1.4 trillion. None of these numbers, on their own, are surprising to anyone who has been watching the geopolitical situation since 2022. The interaction of these numbers with a strategic input that the market has just repriced by roughly twenty-five percent year over year is a different conversation, and it is the conversation that the consumer category is not yet having.

A Tomahawk uses aluminum. A Patriot interceptor uses aluminum. A loitering munition is, in structural terms, a lightweight aluminum airframe wrapped around a warhead, an electronics package, and a battery. Every drone in the autonomous fleet that the defense-technology investor class has been funding requires aluminum, and the new low-cost containerized cruise missile program has been deliberately designed for affordable mass, which is the contracting term of art for thousands of units per year of an airframe whose cost basis is structurally a function of aluminum, electronics, and propellant.

Mark Cancian at CSIS has placed the production timeline at three to four years before output meets demand, and until then, allied procurement runs behind U.S. requirements rather than alongside them. The Gulf states want their air defenses replenished, Ukraine still wants Patriots, Japan wants Tomahawks, and Europe is mobilizing its own production base under the European Defence Fund. The aluminum coming out of a Bahrain smelter under siege conditions is not coming to a beverage can factory first, and it is not coming second either.

Where the New Money Has Gone

The second leg of the squeeze is capital, and the magnitude of the reallocation has not been adequately metabolized by the consumer commerce press.

Venture capital deployed approximately $49.1 billion into defense technology in 2025, which is nearly double the $27.2 billion deployed in 2024 and the largest annual figure that PitchBook has recorded. U.S. equity funding in the sector tripled to $14.2 billion, with American startups capturing the lion’s share of the global pool. Manufacturing-focused defense investment, which is the unsexy capex layer where smelting capacity and forging lines and CNC throughput live, rose to $4.7 billion across 39 deals, up from $2.6 billion across 24 deals the prior year. Defense-technology exits hit a record $54.4 billion, more than triple the $18.2 billion of 2024, and most of the exit volume cleared through acquisitions rather than public offerings.

The headline rounds are familiar to anyone who has been reading the NATSEC @ 2PM briefings over the past eighteen months. Anduril raised $2.5 billion in June at a $30.5 billion valuation. Saronic raised $600 million for uncrewed maritime systems. Helsing raised $694 million in Germany. Hadrian, the defense-manufacturing startup, took $260 million from Founders Fund and Lux Capital. Castelion, which most consumers have never heard of, has just signed a Pentagon agreement that obligates a minimum 500-missile annual production rate. The pattern is consistent, the capital is patient, and the policy environment is catching up to the capital rather than the other way around.

The argument that 2PM has been making across the Drop Economy essay and the dual-use thread that preceded it is the argument that matters here. The same Silicon Valley funds that wrote consumer brand checks in 2021 are writing defense manufacturing checks in 2025, and the operator talent that built growth-stage consumer brands is being recruited into defense operations and ground-truth manufacturing roles. Capital is finite, attention is finite, and operator bandwidth is finite. The reallocation is already complete in the rooms that matter, even if the trade press has not finished reporting it.

The downstream consequence for the consumer category is straightforward. When a tier-one venture fund leads a $260 million Series C in a defense manufacturer at a clearing multiple, the same fund’s limited partners reset their expectations across the rest of the portfolio. Premium consumer brands with thin margins, soft moats, narrative-led positioning, and no defensible distribution are no longer the asset class. They are the cautionary tale told at the limited partner meeting, and the well-funded brands have already absorbed this and adjusted their internal messaging accordingly. The brands that have not absorbed it are still printing pitch decks that assume a 2021 capital environment.

The Math of the Can

It is worth running the numbers cleanly, with every operator anonymized, because the math is unambiguous and the math is where the conversation should be moving.

A twelve-ounce aluminum can, sold in volume to a beverage brand under a long-form supply agreement, has historically priced somewhere between 10 and 13 cents for the empty can itself, with sleek and slim formats running slightly higher and standard formats slightly lower. Add fill, label, contents, freight, and slotting, and the fully loaded cost of goods on a single unit lands somewhere between 25 and 35 cents, depending on the brand’s scale and the terms of its co-packing relationships. Packaging, taken together across aluminum, glass, and plastic, accounts for roughly one-third of total raw material cost in beverage manufacturing, and aluminum is the largest single line within packaging for a sparkling water brand built on the slim can format.

A premium sparkling water brand sells to a major grocery account at somewhere between 55 and 75 cents per unit at wholesale, with co-packer and distributor margin layered in. Direct-to-consumer pricing on a 24-pack runs between $30 and $48, which is $1.25 to $2.00 per unit on the retail face, with freight and last-mile fulfillment absorbing most of the apparent premium. Gross margins at wholesale run between 35 and 50 percent on a good quarter, and at DTC between 50 and 65 percent on the contribution line before customer acquisition cost.

A 25 percent rise in aluminum, holding all other inputs equal, adds roughly 3 cents to the cost of a single can. On a 65-cent wholesale unit, that is four to five percentage points of gross margin compression. If aluminum tracks the Trading Economics twelve-month forward and adds another seven percent on top of where the chart already sits, the compression deepens to five to seven points by the middle of 2027, which on a brand operating at a 38 percent wholesale margin amounts to approximately fifteen percent of gross profit erased before a single dollar of customer acquisition spend has been deployed.

For omnichannel sparkling water, which is to say the brands selling 24-packs into apartment doorsteps in coastal metropolitan markets, the compression is structurally worse rather than better. Freight is itself aluminum-adjacent in the sense that trucking, fuel, and corrugated packaging all carry their own inflation profiles, and the DTC consumer base is the segment most willing to trade down at the moment that price moves on the digital shelf. Premium DTC sparkling water as a category has never had pricing power in the way that Poppi or a small handful of cult-coded competitors have had pricing power. It has had narrative power, and narrative power compresses faster than COGS does when the underlying input is no longer underwriting the deck.

Three Anonymized Archetypes

Brand A is well-capitalized, holds national distribution, has dominant shelf presence at scale, and has hedged aluminum forward through structured supply agreements with its can converter. The brand has the volume to negotiate sleeve pricing on cans, the operator depth to manage co-packer leverage actively, and the marketing efficiency to absorb a one to two point gross margin hit through promotional rationalization rather than retail price. Brand A will look fine on the next earnings call and the call after that, and Brand A will quietly acquire one or two distressed competitors in 2027 at multiples that look like opportunism in retrospect.

Brand B is mid-tier, venture-funded, operating somewhere between $40 million and $80 million in revenue, with premium DTC and natural channel presence. Brand B has four to six months of can inventory on the books and a co-packer contract that resets in the third quarter. The brand’s pitch deck has, for the last two raises, shown a path to 65 percent contribution margin at scale, and the deck does not survive contact with aluminum at $3,600 per tonne. The next raise will be a flat or down round if it happens at all, or a strategic sale to a category platform, or, in the most common case, a tightening exercise that ends in a retrenchment from DTC and a return to wholesale at lower velocity and tighter terms. Some of these brands will not raise at all, and some will burn down to a sale that the press release will describe in flattering terms even when the deal terms are not.

Brand C is indie, founder-led, operating between $3 million and $11 million in revenue, premium-positioned without institutional capital. The math at Brand C is the cleanest and the most brutal. Without scale leverage on can pricing, without hedging, and without a Series B war chest, Brand C either pivots to a higher-margin product extension, which is to say powders, concentrates, functional ingredients, or formats other than the slim aluminum can, or it does not exist in any commercially meaningful form by 2028. The brands at this tier that exercise fiscal discipline will pivot, and the brands that have been operating on aesthetic alone will not. The acquisitions at this tier will be few, and they will not be flattering. Strategic buyers do not pay premium multiples for compressed-margin businesses in categories they already understand, and the exits, where they happen, will be classified as talent-and-IP acquisitions rather than as category roll-ups.

Who Survives the Next Five Years

The survival profile of the category, looking out across the procurement window the Pentagon has now made explicit through 2032, is legible enough to plan against, and the planning is the point of this essay.

The brands that survive will share four characteristics, and the characteristics compound on each other in the way that brand defensibility compounds across the moats that 2PM has been mapping for the better part of a decade.

The first characteristic is structural cost advantage, which means scale, vertical integration, or proprietary formulation that allows the brand to move at least part of its volume out of pure aluminum dependency. The energy drink houses that already own their can supply contracts qualify, the functional beverage brands building in formats other than the standard twelve-ounce slim sleeve qualify, and the hybrid-format players who can shift between can, glass, bottle, and powder without rebuilding the line qualify.

The second characteristic is real pricing power, which is less common than the founder decks claim and which has very little to do with the price the brand currently charges. Real pricing power means that the consumer will not trade down if the brand raises retail by ten percent, and the test for pricing power is the cultural meaning, ritual context, or flavor specificity that a competitor cannot replicate. Most premium sparkling water does not pass the test. The category has taste, which is a substitute for pricing power until the substitute becomes too expensive to maintain.

The third characteristic is distribution moat, which is rare and getting rarer as retailers consolidate their own private-label sparkling water programs to capture exactly the contribution margin that a national brand can no longer hold. The brands that own the cold case, the route, the cooler placement, or a category captaincy at a grocery banner are the brands that will be permitted to absorb input inflation without losing shelf, and the brands that depend on shelf rental are not.

The fourth characteristic, which 2PM has been arguing across the Universal Commerce Protocol work in January and across the Drop Economy work in April, is the editorial and retrieval layer that the AI age now requires. The brand that controls the vocabulary that the answer engines use to describe a category will own that category through the procurement window, and the control is built through editorial discipline, narrative density, and community signal rather than through performance marketing spend. Palantir is a defense and data company that has built a Shopify storefront operating as an investor relations channel that happens to accept Apple Pay, and the brand has earned more cultural coverage in eighteen months than most CPG operators earn in a decade.

The infrastructure that made it possible is the same infrastructure that powers any merchant on the platform. The lesson is not that a sparkling water brand should sell defense merch, and the lesson is not that a sparkling water brand should pivot to drone parts. The lesson is that editorial control of the answer engine layer compounds across exactly the kind of category compression cycle the next five years will deliver, and the brands that build the layer now will be the brands that the AI describes to a future customer who has not yet typed the question.

The Verdict

Is the squeeze coming. Yes, on the procurement schedule the Pentagon has already published, with the capital flows the venture data has already confirmed, and against the chart that is sitting on Trading Economics for anyone who cares to look. About the timing, yes. About the magnitude, yes. About the structural nature of the move rather than a cyclical one, yes on every count that the data supports.

About the consumer category response, partially. The well-funded brands will be fine, in the way that well-funded brands tend to be fine in a compression cycle, and the brands operating with some semblance of fiscal responsibility will pivot to higher-margin formats and survive in a smaller, more profitable, less narratively exciting form than the decks of 2021 promised. There will be a number of survivors. There will be very few acquisitions, and the acquisitions that occur will not be flattering on the terms the press releases will describe. The remainder of the category, which is to say the brands that have been operating on aesthetic alone in the absence of pricing power, distribution moat, cost advantage, or editorial discipline, will return capital gracefully or they will not.

The conversation in the Carolinas did not end with a resolution, in the way that the most useful conversations tend not to. Someone refilled a glass, someone made a joke about the price of a Patriot interceptor, and the room broke up into the smaller conversations that follow the formal agenda. I drove back to the hotel thinking about aluminum, about the country, about the five to seven year window the room had been modeling, and about how few of the brands at the table when I started this work will be at the table when the procurement cycle clears.

A strategic input is going to war again, in the way that strategic inputs have done before, and the brands that prepare for it now will exist in 2030 in a recognizable form. The brands that wait for the chart to confirm the trend will discover, as every operator who has ever sold a hard good through a hot input eventually discovers, that the chart is not weather, the chart is geology, and the time to plan against geology is before the geology reaches the shelf.

Research and Writing by Web Smith

Reporting reflects aluminum spot pricing and forecasts as of the most recent close on the London Metal Exchange via Trading Economics; Pentagon Munitions Acceleration Council disclosures and FY2026 appropriations; PitchBook, CB Insights, and Crunchbase defense-technology venture data for 2025; SIPRI global defense expenditure data; CSIS analysis on munitions surge production; and historical accounts from the U.S. wartime aluminum buildup of 1939 through 1945, including the Defense Plant Corporation program and the antitrust resolution of the Alcoa monopoly.