Este informe está destinado exclusivamente a Miembros ejecutivos, para facilitarle la afiliación, puede hacer clic a continuación y acceder a cientos de informes, a nuestra lista DTC Power List y a otras herramientas que le ayudarán a tomar decisiones de alto nivel.

Memo: The Case for QR

If you ever want to give up, consider the QR code’s journey from where it was just a few years ago. While immensely popular in Japan and other Asian countries, prior to the pandemic it was nearly forgotten in the United States.

The QR code dates back to 1994, when it was first used by a Toyota subsidiary to track auto parts during assembly. More information-rich than a barcode, QR codes were designed to unlock information like product files or manufacturing records. It wasn’t until 2002 that the “quick response” code took on a new life as a way to drive viewers to properties like websites and events. And by 2007, QR’s promise was what we know it today: for brands and advertisers to tack on additional storytelling, details and access when trying to get customers’ attention. Still, it never ever quite caught on in a meaningful way, at least not in the US.

In fact, the technology was the butt of many jokes. When Tim Armstrong reintroduced efforts to market brands through QR codes in 2018, the idea was widely panned. The former AOL and Verizon Media CEO attempted to rebrand the then-24 year old technology as “Flowcode.” In November of 2019, his latest project, DTX Company, contacted 120 DTC brands in an attempt to build a new shopping holiday called “DTC Friday.” In 2019’s In Defense of Tim Armstrong, I explained:

Tim Armstrong is not wrong; he’s early. DTX’s effort to launch DTC Friday 2019 wasn’t designed to prioritize the advertising brands. The goal was to advertise Flowcode, a reportedly advanced rebrand of the QR code concept that was dismissed in the United States, several years ago.

In that report, I characterized the difference between the US and Asia’s offline attribution models. When this was written in 2019, billboards, mailers, catalogues, and brochures were the primary forms of offline marketing in the US. Meanwhile, China used QR codes to fuel sales and attribution at scale. My assessment of Armstrong’s bet, at the time, was as follows:

Given the flow of retail innovations from China to the United States, it’s clear to see that when Armstrong discusses payments “getting easier”, he anticipates an adoption of mobile wallets and streamlined payments systems. Why? The prevalence of these systems correlated with a mass adoption of QR code usage in China.

Mobile wallet adoption and streamlined payments systems have vastly improved since Tim Armstrong’s attempt to resurrect the QR code through DTX. He wasn’t wrong; he was early. And something else happened: the pandemic. In 2020, Square built systems around QR use for shops and small businesses. The Verge published this in 2020:

When using the feature, a restaurant can print a QR code out and leave it on a table. A customer would then scan the QR code, browse a menu, place their order, and pay from their phone. The restaurant would know what table placed the order, and then bring their food out when it’s ready. Square says the system is flexible, so a coffee shop, for example, could have a single QR code in its window that people would scan and then wait for their drink.

And the rest was history.

Web Smith on Twitter: “QR’s j-curve of adoption: 1994: Toyota invents QR 2007: Wide use in APAC2011: 14M Americans used QR2013: QR codes derided2019: DTX tries to rebrand it2020: Square’s QR for shops 2021: Pandemic popularizes it2022: 60 sec Super Bowl ad / Twitter”

QR’s j-curve of adoption: 1994: Toyota invents QR 2007: Wide use in APAC2011: 14M Americans used QR2013: QR codes derided2019: DTX tries to rebrand it2020: Square’s QR for shops 2021: Pandemic popularizes it2022: 60 sec Super Bowl ad

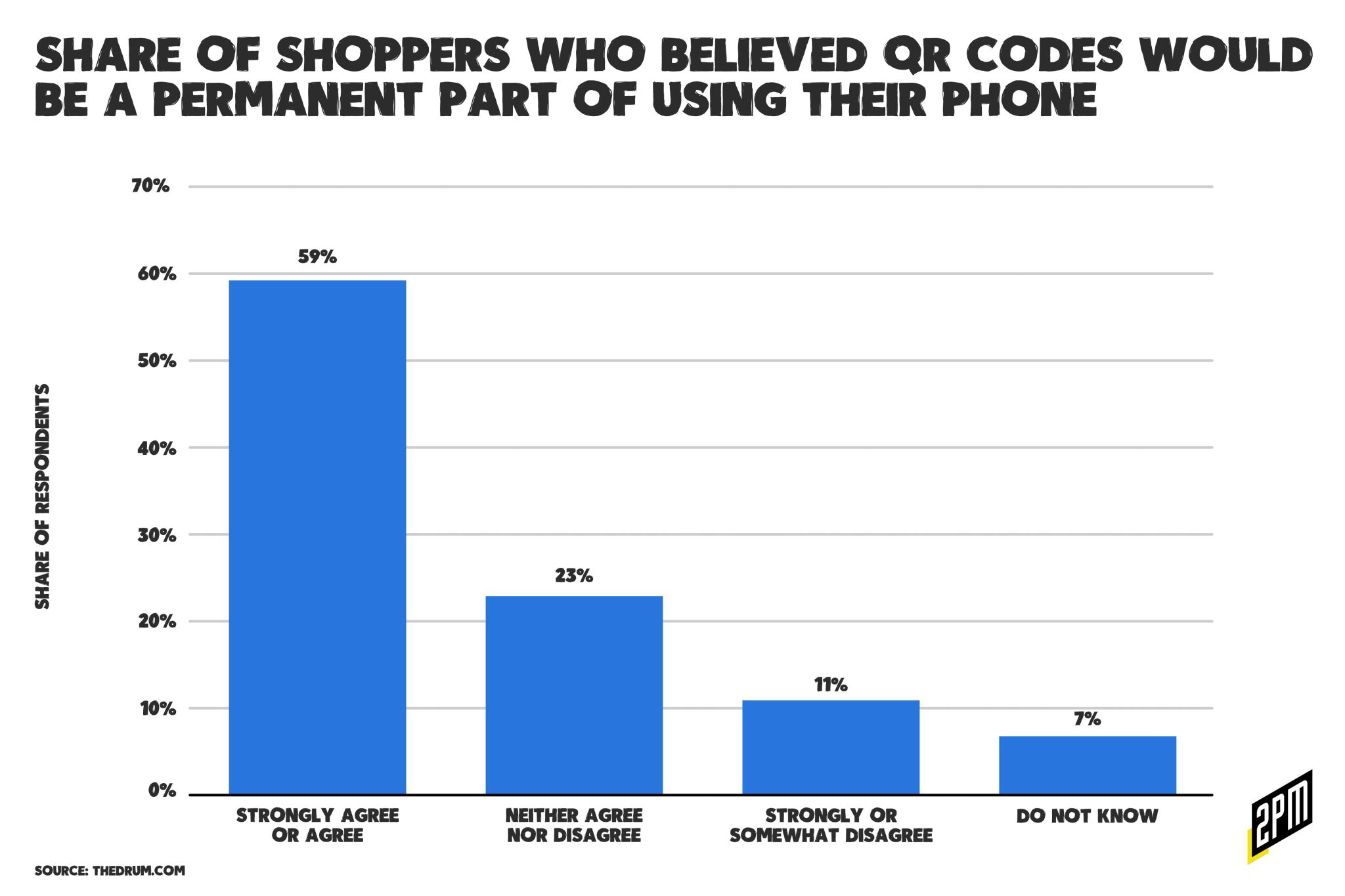

The QR suddenly popped up everywhere: restaurant menus, packaging, device installs, the walls of museums. There, they’ve taken the place of guides who would have ushered guests before pandemic restrictions hindered their roles. There is a newfound appreciation for the QR. Seemingly overnight, it became a necessary technology in America as payments technology proliferated and proximity payments nearly doubled over the span of 2019 to 2021.

So when the QR code popped up on the screen for 60 seconds during the Super Bowl, the room’s reaction wasn’t one of distaste. In a room of 30 adults ranging from 35 to 55, the consensus was: “OK, whoever this is, this seems smart.” As many Super Bowl lists have now-noted, it was a clever advertisement for Coinbase. The project was a joint effort between the cryptocurrency exchange and its agency of record.

Accenture Interactive, the agency responsible for the ad, had undergone a digital transformation and acquisition spree under CEO Brian Whipple, who left last summer and was replaced by David Droga. Accenture Interactive’s reinvention turned the consulting firm into a creative agency and technology partner – a combination perfectly suited for the Web3 era. I would have loved to have been in the room for the decision to acquire a the television spot for $15 million and spend nearly nothing designing the actual creative for it. It’s a level of efficiency that has become a feature in the age of proximity payments, blockchain implementation, and subscription-commerce. The less thought, the better. AdWeek explained:

Had the ad been just 15 seconds, casual viewers might have shrugged off the odd spot and gone back to their snacks. But running a leisurely 60 seconds, the spot and its hypnotic music became increasingly curiosity inducing until finally many of us had to pull out our phones and scan it. In a night defined by crypto players working hard to get your attention, Coinbase leaped past simple brand awareness and directly engaged viewers by the millions. Bonus: It also—finally—proved all those 2007-era QR evangelists right.

A 30-year-old technology experienced a J-curve in popularity, from Toyota’s invention in 1994 to widespread use in most Asian-Pacific countries in 2007. In 2011, just 11 years ago, 14 million Americans scanned a QR code. According to Bitcoin Magazine, Coinbase received 20 million hits to its website in one minute.

That’s nearly double the entire audience for QR, just a decade later in just 0.00019% of the time. By 12 p.m. EST the day after the Super Bowl, the stock price began reflecting the market’s positive reaction to the chatter. Sportico’s Jacob Feldman noted a stock price that added 1-2% to the company’s market cap. A $14 million spend and a $1 billion+ outcome.

If just 2% of viewers decided to make an account in that first minute of viewership, In theory, Coinbase won 400,000 new wallets at a cost of $35 per customer. We’re going to be seeing a lot more of QR codes in the media. Tim Armstrong wasn’t wrong, he was just early. As Web3 rises in popularity and the metaverse conversations persist, the core of many of these discussions is the basic understanding of cryptocurrencies and their potential. Before MetaMask, OpenSea, and other marketplaces — Coinbase may be the most foundational platform for mass adoption. Accenture Interactive and Coinbase were right on time with a simple message that overshadowed much of the night’s game, the internet’s betting commentary, and the musical fanfare of America’s top sporting day. A QR code did all of that.

Por Web Smith | Editado por Hilary Milnes con arte de Christina Williams y Alex Remy

Resumen para miembros: El Gran Juego

Este informe está destinado exclusivamente a Miembros ejecutivos, para facilitarle la afiliación, puede hacer clic a continuación y acceder a cientos de informes, a nuestra lista DTC Power List y a otras herramientas que le ayudarán a tomar decisiones de alto nivel.