En lo que sólo puede caracterizarse como un indicador adelantado del cambio de las mareas económicas en el comercio minorista, la marca de clase media está batiendo al S&P y dejando un rastro de competidores de escala superior a su paso. Es emblemático de la lenta bifurcación de los consumidores y los minoristas que los apoyan. Esto es de nuestro informe sobre la Edad Dorada 2.0, un periodo que parecía durar unos cuatro o cinco años (2017-2022).

Aunque la historia no se repite, sí rima. Los más desfavorecidos económicamente reparten comida, novedades, alcohol y productos básicos a las aglomeraciones urbanas y los suburbios cerrados, en cuestión de horas. En todo el país, el patrimonio neto del 1% más rico se ha hecho notar a medida que ha aumentado el consumo conspicuo de productos y servicios; el auge de plataformas como StockX, Hodinkee y Uncrate así lo demuestra. Para el 0,01% más rico, hay más casas de más de 1.000 metros cuadrados que en los locos años veinte. El comercio minorista responde a la realidad económica actual. La riqueza se está galvanizando; las estrategias del comercio minorista deben ajustarse para hacer frente a los cambios.

Mientras sitios de reventa bien financiados como The RealReal, thredUp y Poshmark luchan en Internet, gastando mucho dinero en marketing mientras pierden valoración rápidamente, una empresa decididamente offline está ganando silenciosamente. Su éxito es emblemático del poder que ejerce el comercio minorista en la actualidad. Un poder que no hace más que crecer a medida que las tendencias de bifurcación se imponen.

Winmark posee franquicias de tiendas de segunda mano en todo Estados Unidos, entre las que se incluyen: Plato's Closet, Play It Again Sports y Once Upon a Child. Probablemente nunca haya oído hablar de su empresa matriz, pero al menos habrá pasado por delante de una de sus tiendas en un centro comercial de las afueras. Forbes presentó un perfil de la empresa, que es un negocio rentable, público y multimillonario que pasa tan desapercibido que no hace llamadas para obtener beneficios. Veinte inversores poseen el 80% de la empresa:

Es la tortuga de la guerra de la reventa. La empresa, que salió a bolsa en 1993, antes de que casi nadie comprara por Internet, ha adoptado un enfoque lento y constante. Las nuevas tiendas se abren a un ritmo modesto, lo que permite a la empresa ser selectiva con los candidatos a franquiciado que acepta. No ha gastado demasiado en mercadotecnia.

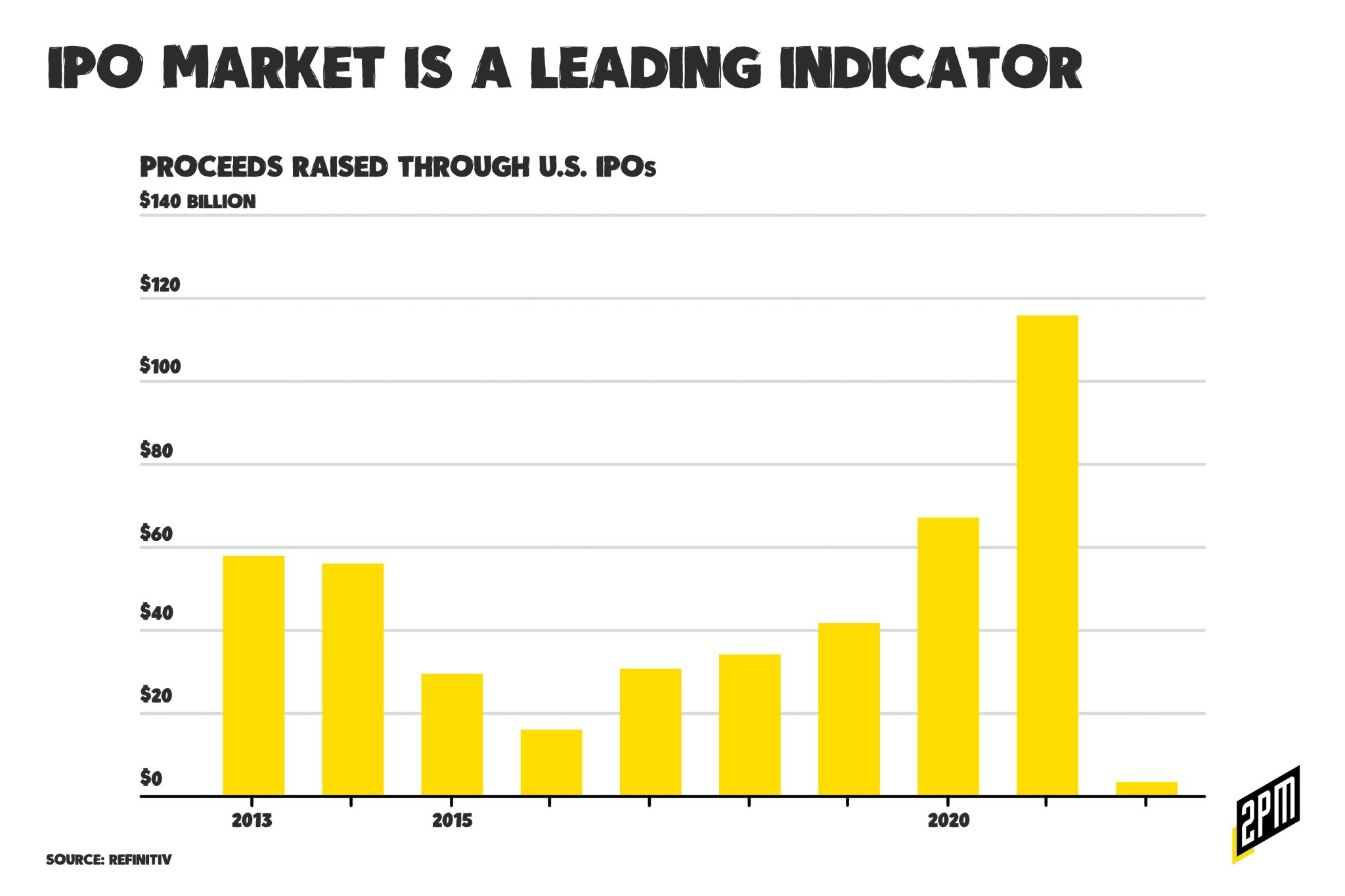

El sector de la reventa (antes conocido como tiendas de segunda mano) está creciendo rápidamente. Según un informe financiado por el sector, este segmento podría duplicarse hasta alcanzar los 82.000 millones de dólares en 2026, impulsado por una generación de compradores jóvenes interesados en adquirir piezas únicas de forma asequible y respetuosa con el medio ambiente. Además, recibe un impulso adicional en un momento de inflación galopante y problemas en la cadena de suministro, en el que muchos compradores acuden en masa a las tiendas de segunda mano tras encontrarse con precios elevados y artículos agotados en las grandes superficies.

El modelo de negocio de Winmark es el adecuado para el momento. Ofrece artículos asequibles y prácticos para la clase media estadounidense que, como dice Diane Hubel, franquiciada de Once Upon A Time, necesita ser eficiente con su dólar, ya que la inflación se ha disparado y los salarios siguen estancados para la mayoría. Incluso les ofrece una forma de ganar dinero a cambio vendiendo cosas que ya no necesitan. Y como los productos son de segunda mano, los problemas de la cadena de suministro que aquejan a otros minoristas no existen en la cartera de minoristas de Winmark. El stock no está garantizado, lo que puede ser una desventaja, pero es fiable en el sentido de que suele ofrecer alguna opción, aunque no sea la primera preferida.

Luego está la rentabilidad. Winmark no construirá una operación no rentable.

Winmark ha incursionado en el comercio electrónico, pero sólo cuando los precios son lo bastante altos para que resulte rentable. Por ejemplo, en Music Go Round, que vende artículos como saxofones y guitarras eléctricas de segunda mano, el valor medio de los pedidos supera los 250 dólares, por lo que lanzó un sitio web para vender productos en línea. No tiene planes para tiendas de ropa como Plato's Closet o Once Upon A Child, donde el artículo medio cuesta menos de 10 dólares.

Como expone Forbes, los competidores en línea de Winmark no son rentables y sus valoraciones se han rebanado en sus OPV. Es probable que, si siguieran siendo privadas, evitaran por completo la OPV:

Estos competidores del DTC fueron revolucionarios de un anticuado mercado de segunda mano, pero la mecánica empresarial es difícil de hacer funcionar. Ahora lo están aprendiendo, y los tiempos de bonanza han pasado. Winmark es más ágil: no tiene que invertir en el extenso proceso de catalogar artículos de segunda mano para el consumo masivo.

Todo ello conforma la historia de un minorista que gana en tiempos difíciles. No es llamativo. No ha conseguido capital riesgo. Pero está ahí para una clase media que se encuentra con las fuerzas del mercado en su contra. En estos momentos, el panorama es sombrío para muchos, lo que significa que las empresas más sencillas y básicas se encuentran en mejor posición que en los últimos años, caracterizados por la bifurcación de los consumidores y las empresas que se dirigen a un consumidor de lujo.

Por Web Smith | Arte de Christina Williams y Alex Remy | Editado por Hilary Milnes

Lee también: Sak Pase, una reflexión sobre nuestras últimas semanas y el reciente viaje misionero en el que tuve la suerte de embarcarme.