Meta、谷歌、亚马逊、Salesforce、Twitter、微软,但没有苹果。原因何在?这些公司中的每一家都对零售生态系统至关重要,但其中一家公司衡量关键结果的方式在完全不同的行业中最为常见。

"基思-拉博伊斯(Keith Rabois)最近对埃隆-马斯克(Elon Musk)的推特(Twitter)管理层说:"你会再次听到每名员工的收入,在科技领域,至少在私人领域、风险投资领域,至少在五年内没有人关注这些指标。

增长和市场份额曾经是关键绩效指标,而盈利能力和效率将是未来五到十年的衡量标准。OKR(目标和关键成果)是一个战略框架,而 KPI 则是该框架内的衡量标准。品牌和 SaaS 市场营销以无尽的热情讨论 KPI,但 OKR 却很少以同样的精力进行交流。我相信,这种情况将会改变。

目标和关键成果(OKRs)与人力资源密切相关,但通过将业务发展与人力资源的 OKRs 相结合,企业可以创建一个更强大、更一致的品牌形象,同时还能为员工营造一个积极、吸引人的工作环境。在所有人力资源指标中,有一项似乎正在成为美国经济复苏的关键。这些指标包括人数、招聘时间、录取率、员工满意度、离职率、留用率、培训费用和每名员工的收入(RPE)。后者是衡量一个小时的标准。

RPE 是大型科技公司裁员的标准。在牛市增长期, RPE 往往被忽视,而现在,它已成为证明组织规模合理性的谈资。财富》杂志解释说

除了缩减人才招聘力度和加强人事工作外,苹果还将减少商务旅行和推迟发放员工奖金。首席执行官蒂姆-库克(Tim Cook)今年也将减薪约 40%,据说这是他自己要求的。总之,这些举措是真正的 "少花钱多办事 "战略。

苹果公司在一个关键方面非常高效,许多其他大型科技公司也将采用这种方式。下面这个例子就像是大型律师事务所衡量成功的标准。Adyen 成立于 2006 年,总部位于阿姆斯特丹,拥有约 2000 名员工,是 Stripe 的最佳直接 "竞争对手"。The Information最近解释了为什么 Stripe 的私人估值比 Adyen 的公开估值高:

根据 The Information 的分析,Stripe 近年来在员工和新业务计划上花费巨大,以至于其 2022 年的员工人均支出是 Adyen 的两倍,尽管 Adyen 的员工人均收入更高。预计今年的支出差距将保持不变,但 Stripe 的每名员工收入预计会更好。

就连谷歌趋势(Google Trends)也反映出,"雇员人均收入 "的提法越来越多。这在其他行业早已成为惯例:他们说,如果你是律师事务所的合伙人,你就需要把自己视为企业而不是雇员。根据《四周 MBA》的报道,亚马逊的主要 OKR--RPE--在 2021 年至 2022 年间增长了 4 万美元。但目标显然没有实现;亚马逊最近又裁员 9000 人。不过,我怀疑随着裁员的继续,RPE 在 2023 年会再次增长。根据《华尔街日报》的收入和员工人数预测,Meta 的 RPE 将增至 185 万美元。

这也是评判公司的标准。Wilson Sonsini 是一家在大科技领域广为人知的公司,它以 RPE 衡量成功与否。根据《美国律师》(The American Lawyer)的数据,自2019年以来,该公司的RPE和员工人数都出现了断崖式增长。Law.com从2023年3月开始进行分析:

Wilson Sonsini 每名权益合伙人的利润下降了 9.5%,因为该公司的律师人数增加到了 1,045 名,其中包括 266 名合伙人。

在当今快速发展的商业环境中,企业越来越多地寻求新的方法来评估其业绩和长期前景。收入、净利润和市值等传统指标多年来一直被广泛使用,但它们可能并不能说明问题的全部,尤其是对于大型科技公司而言。将大型科技公司与律师事务所进行比较的前提是,这两类企业在未来几年都将以这种 OKR 作为评判标准。

采用新测量方法的理由

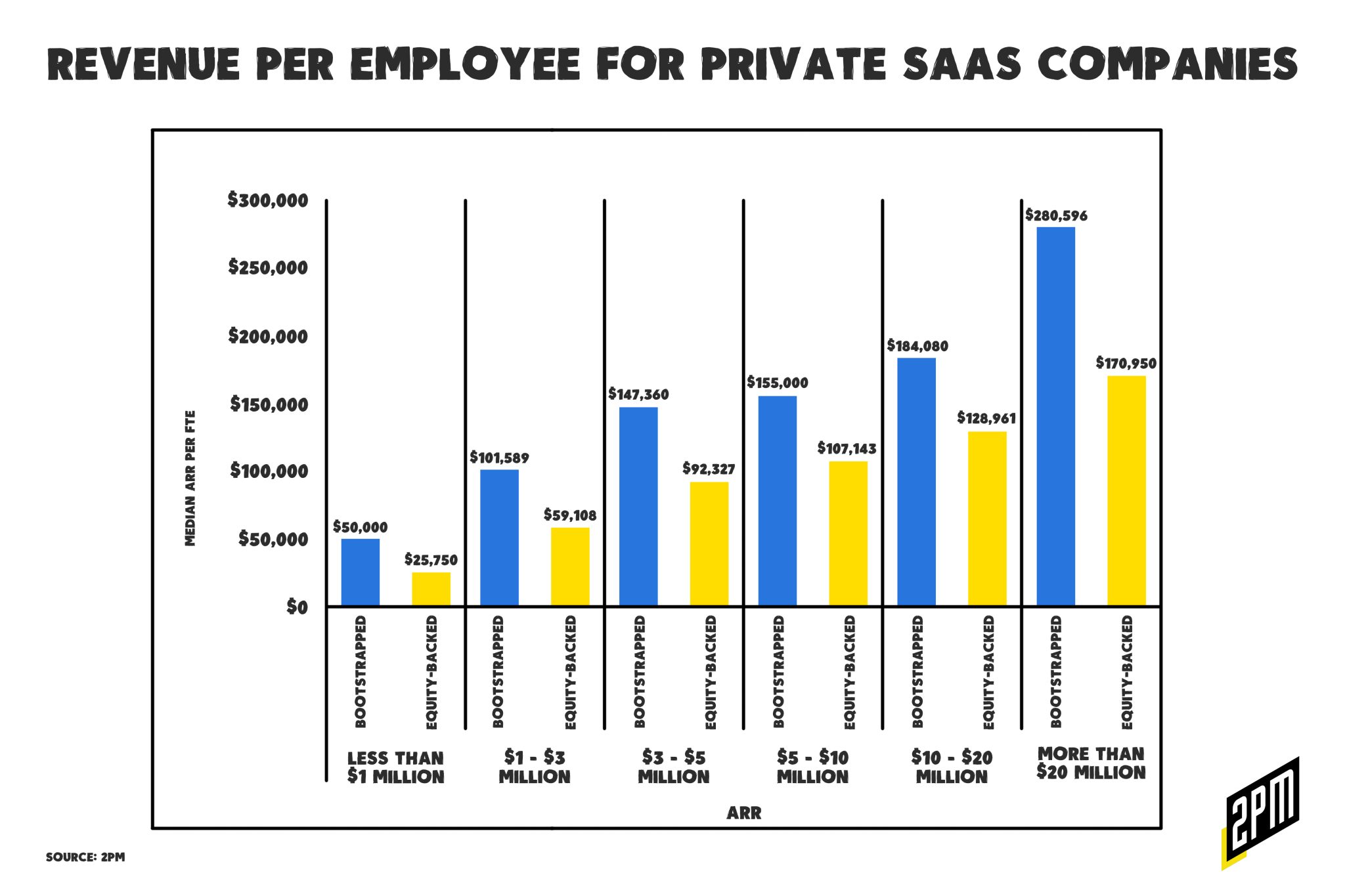

RPE 是一个简单而强大的指标,它将公司的总收入除以员工人数。这一比率显示了每名员工为企业贡献了多少收入,为了解公司的效率、生产力和扩展能力提供了宝贵的信息。RPE 日益成为大型科技公司的重要指标有几个原因:

注重效率和生产力

RPE 有助于衡量公司如何有效地利用员工,这是任何组织的关键组成部分。同时,还可以了解这些员工如何看待自己在公司发展和健康中的作用。雅虎高级研究分析师汤姆-福尔特(Tom Forte)列举了亚马逊早期流失的职位类型,即那些不直接影响收入增长的职位:

因此,如果你特别看一下去年 3 月和 6 月的季度,这两个季度之间的减员人数约为 10 万,而且大部分都不是重新招聘来替代履行中心离职的员工。

RPE 比率越高,意味着公司用更少的员工创造了更多的收入,表明公司的业务模式更高效、更富有成效。正如亚马逊开始展示的那样,他们愿意探索是否可以用更少的成本中心完成 "更多 "的任务。

吸引和留住人才

人才是科技行业的关键资源,公司需要确保能够吸引和留住顶尖人才,以保持竞争优势。较高的 RPE 比率表明公司正在有效利用其劳动力,从而提高员工的满意度和忠诚度。这反过来又有助于吸引新的人才,减少人员流失,从而促进公司的整体健康和发展。

规模和增长

随着科技公司的发展壮大,他们往往面临着如何高效扩展运营规模的挑战。RPE 可以帮助识别公司在扩张过程中是否保持或提高了生产率。在增长期间,如果 RPE 比率保持稳定或不断上升,则表明公司正在成功地扩大运营规模,这对长期成功至关重要。巴伦周刊》最近公布了相关数字:

FactSet 的数据显示,苹果公司在最近一个财年为每位员工创造了约 240 万美元的收入,在过去五年中,同一指标的平均收入约为 210 万美元。这一数字远远超过了 Facebook 的所有者 Meta (META),该公司在 2022 年的每名员工收入为 135 万美元,低于其 150 万美元的五年平均水平。

这样,无论公司是上市公司还是私营公司,我们都有了统一的比较方法。

用于电子商务和零售业

RPE 可以作为比较整个科技行业公司的宝贵基准。信息》杂志是这样构思这场上市公司与私营科技公司的对话的:

对 Stripe 来说,与 Adyen 的不利比较是一个令人惊讶的转折,因为 Stripe 这个初创品牌在硅谷几乎成了一个神圣的名字。Stripe 早期的快速发展和对快速扩张的电子商务市场的接触,帮助这家支付公司在十几年间从一些风投大佬那里筹集到了超过 20 亿美元的资金。2021 年初,该公司以 950 亿美元的估值融资,成为全球估值最高的初创企业之一。

相比之下,Adyen 作为一家私营公司仅募集到 2 亿美元,尽管它在 2018 年首次公开募股时募集到了数亿美元。它目前的市值约为 440 亿美元。

通过评估这一指标,投资者、分析师和其他利益相关者可以更清楚地了解一家公司相对于同行的表现如何,这有助于为战略决策和投资机会提供依据。

Shopify率先讨论了这一指标在零售业中的作用。RPE 是评估大型科技公司健康状况和前景的关键指标,但也可用于评估品牌。

如果您想了解品牌如何计算 RPE 的真实案例,让我们以2PM的数据为例,计算一下热门零售商每名员工的平均收入。 克尼克斯:拥有 127 名员工,平均年收入为 7050 万美元。也就是说,每名员工的收入为 555,118 美元。 Boll and Branch:拥有 116 名员工,平均年收入为 8080 万美元。相当于每位员工的收入为 696,551 美元。 Everlane:拥有 309 名员工,平均年收入为 3.612 亿美元。相当于每位员工创造 168 万美元的收入。

除规模外,RPE 还关注效率、生产力、人才吸引和保留,从而为公司业绩提供了传统衡量标准可能无法捕捉到的宝贵见解。它还强调了高效追求利润的重要性。随着科技行业不断发展并面临新的挑战,RPE 将在帮助公司应对竞争格局和实现长期生存能力方面发挥至关重要的作用。

作者:Web Smith | 编辑:Hilary Milnes,美术:Alex Remy 和 Christina Williams