Este resumo para membros foi elaborado exclusivamente para Membros executivosPara facilitar a associação, você pode clicar abaixo e obter acesso a centenas de relatórios, à nossa DTC Power List e a outras ferramentas para ajudá-lo a tomar decisões de alto nível.

No. 295: Guerra assimétrica

A verdade está em algum lugar no meio. Isso envolve nuances e uma visão imparcial do setor como um todo para entender o que está ocorrendo, pois as coisas mudam na velocidade da luz. O artigo recente do The Economist pinta um quadro bonito de um setor de DTC. O setor, como um todo, é muito mais difícil do que os empreendedores de varejo recém-formados gostariam de pensar. Duas coisas podem ser verdadeiras: (1) as marcas antigas e antiquadas são administradas por executivos de carreira que não entendem de agilidade ou inovação; (2) a maioria das marcas DTC fracassará porque é administrada por ex-consultores de administração ou recém-formados em MBA que não valorizam os poderes da marca, dos relacionamentos e da comunidade.

Guerra assimétrica: guerra que envolve ataques surpresa de grupos pequenos e simplesmente armados contra uma nação armada com armamento moderno de alta tecnologia.

As marcas diretas ao consumidor são difíceis de escalonar. O pressuposto frequentemente adotado é que você pode gastar em design, fabricação, embalagem e, em seguida, em aquisição. Gastar, gastar, gastar, gastar, gastar. Assim, os intermináveis aumentos de capital de risco de US$ 30 milhões, US$ 50 milhões ou até US$ 100 milhões. O problema é que, embora empreendedores capazes possam terceirizar o design, a fabricação, a embalagem e até mesmo a aquisição, as marcas estabelecidas foram construídas com base em relacionamentos, consistência, valor e confiança. Os canais tradicionais de aquisição de DtC não podem facilitar imediatamente a confiança ou o valor. Essa parte requer uma quantidade insana de trabalho e consistência. Também requer interação off-line, um fenômeno que estamos observando em tempo real, já que "quase 850 lojas devem ser abertas nos próximos cinco anos."[Forbes]

Os gigantes do setor levaram algum tempo para começar a se preocupar com a chegada dos recém-chegados que mudaram o jogo; as barreiras à entrada em seus negócios são altas. Mas agora as empresas estabelecidas estão estagnadas. De acordo com a empresa de consultoria Nielsen, as 25 maiores empresas de alimentos e bebidas, por exemplo, geraram 45% das vendas da categoria nos Estados Unidos, mas impulsionaram apenas 3% do crescimento total do setor entre 2011 e 2015 (veja o gráfico). Uma longa cauda de 20.000 empresas abaixo das 100 maiores produziu metade de todo o crescimento.

Economista: O crescimento das micromarcas ameaça os gigantes do setor de CPG

Se você perguntar ao vice-presidente executivo de inovação do Publicis Groupe, Tom Goodwin, sobre as marcas diretas ao consumidor (DtC), ele vai lhe dar uma bronca. Para ser justo, defender a Procter & Gamble é uma de suas principais funções. A P&G é tão importante para seu empregador que eles acabaram de anunciar um escritório em Cincinnati para dar suporte às estratégias de publicidade da P&G. Em um artigo de 22 de outubro que ele escreveu, ele inclui esta passagem calorosa:

As DNVBs podem ser um flash na panela, elas não têm fossos, têm marcas inconstantes, podem morrer tão logo apareçam e não podemos continuar falando com as 1/100 empresas que conseguem isso como algo diferente do viés de sobrevivência.

Ele não está totalmente errado. Apenas alguns dias antes, publiquei um artigo sobre a defensibilidade da marca DTC, no qual escrevi sobre como as marcas sobreviventes estabeleceram os fossos necessários para serem mais do que um lampejo na panela. Esta era da Web do consumidor é definida por dois grupos que se chocam com você: o consumidor afluente, inteligente, ocupado e com princípios. Estamos comunicando muitos dos mesmos elementos e, ao mesmo tempo, chegando a duas conclusões distintas: ele acredita que as DNVBs não podem durar e eu acredito que podem. Nossas experiências profissionais dão sombra às nossas opiniões. Há cinco anos: Jeff Blee, ex-vice-presidente de compras e planejamento da Brooks Brothers, comentou sobre um fabricante de camisas DtC em estágio inicial:

Sem se incomodar com o recém-chegado, sempre haveria um mercado para camisas que ele descreveu como "mais novas". E "qualquer concorrência era uma boa notícia".

Desde então, a icônica marca de roupas masculinas adotou uma estratégia de desconto do Joseph A. Bank (quatro camisas por US$ 200) e o Sr. Blee agora dirige uma startup de vestuário DtC. Essa guerra entre o antigo e o novo não se limita a bens de consumo embalados, malas, camisas sociais ou sapatos de lã. Ela está em toda parte. Em um artigo recente de alguém da Business of Fashion (sem assinatura), eles discutem os problemas da Victoria's Secret da L Brands e como "ela pode se salvar".

E, no entanto, a Victoria's Secret ainda parece estar presa em uma cápsula do tempo: uma época em que não havia problema, ou mesmo expectativa, de projetar abertamente o olhar masculino no corpo das mulheres, em que sutiãs push-up desconfortáveis com bombas de ar eram vistos como inovadores, em que as pessoas ainda faziam compras no shopping. O programa desta temporada parecia uma homenagem a si mesmo. Entre as mudanças de cenário, imagens de arquivo eram reproduzidas ao fundo.

O artigo deles se baseia em um relatório anterior da 2PM, no qual descrevemos a crescente concorrência enfrentada pela lendária empresa de moda íntima. O que estamos vendo aqui é um ataque de marcas novas e mais baratas que estão atraindo os sentidos e as carteiras de comunidades preparadas para procurar em outros lugares. Empresas como a L Brands (controladora da Victoria's Secret), a P&G (controladora da Gillette) e a Brooks Brothers não estão apenas competindo em uma base mutável de preço, facilidade e seleção; elas estão competindo em termos de cultura (inclusão de tamanhos, o "imposto rosa" e mudanças em onde e como trabalhamos).

Basta ver a reação do CMO da Victoria's Secret, Ed Razek, de 70 anos, que teria dito: "Tentamos fazer um especial de televisão para tamanhos grandes [em 2000]. Ninguém se interessou por ele, e ainda não se interessam". Para travar uma batalha em várias frentes, são necessários líderes sensatos em uma organização criada para ser ágil. Esses líderes também devem ter empatia pelos consumidores e pelo progresso. Não é preciso dizer que os comentários de Razek foram surdos e indiferentes. Atualmente, várias marcas importantes estão competindo com a subsidiária da L Brands, projetando e comercializando produtos mais inclusivos. No nº 271, escrevi que a Victoria's Secret precisava de uma atualização:

Além das marcas íntimas que estão se expandindo no território da VS, há pressões adjacentes do mercado de atletismo, um mercado de beleza em evolução e a rejeição da lingerie pelos consumidores que buscam conforto, funcionalidade e individualidade. Em vez de continuar competindo com marcas como Adore Me(21), THINX, Inc.(31) e Third Love(51), ou Savage x Fenty, a Victoria's Secret poderia reinvestir na marca, nas mensagens e nos processos de ponta a ponta, seguindo o exemplo do Wal-Mart.

As notícias sobre o último desfile de moda da Victoria's Secret foram, segundo todos os relatos, um fiasco. Mas as soluções estão bem diante deles. Eles devem observar o legado do setor de CPG. Lá, a inovação geralmente envolve: juventude, aquisição e agilidade. A Procter and Gamble está fazendo exatamente isso. O conglomerado de CPG recentemente se reestruturou para formar equipes menores e ágeis, e a empresa de Cincinnati está aberta a aquisições.

A evolução da era DTC tem cada vez mais marcas competindo em varejistas físicos, adjacentes às empresas de CPG, vestuário e calçados que existem há décadas. Há dezenas de marcas, em cada segmento de mercado, buscando competir por seus dólares. Tom Goodwin está correto em sua avaliação de muitas das marcas que levantaram quantias exorbitantes de capital para adquirir clientes por meio de mídia paga.

Mas essa não é a característica de todo o setor de DtC. À medida que a compra de mídia se torna mais difícil para as marcas desafiadoras, mais marcas diretas ao consumidor serão fechadas. E a concorrência se tornará mais simétrica e previsível à medida que as centenas de novas marcas se reduzirem à dúzia mais robusta. A P&G se livrará de grande parte da nova concorrência adotando muitas das práticas dos concorrentes (e a propriedade intelectual da marca por meio de aquisições), já que muitos começam a competir em território familiar. Mas sempre haverá espaço para as marcas desafiadoras independentes que fizerem tudo certo.

Relatório de Web Smith

No. 270: For DNVBs, brand matters.

A look at Raden’s shuttering (DNVB No. 119) and Away’s persistence (DNVB No. 40). With the news of Raden shuttering and their founder’s commentary on the online luggage industry’s outlook, 2PM has a deep dive into what may have influenced Raden’s shuttering (it wasn’t just regulation). And Away cofounder and CEO Steph Korey provides commentary on what will shape Away’s bright future.

Founder of Raden, Josh Udashkin had this to say to Conde Nast Traveler about the future of the smart luggage industry:

I hate to say this, but I think [the future] is nonexistent. All these companies rely on word of mouth, but buying this product now gets you hassled. I don’t see how you can continue selling it.

We disagree. Millennial consumers are practical, savvy, and even slightly territorial. These consumers seek brands that appeal to their lifestyles, their timing, their values, and their personal preferences. The narrative matters because their lifestyle matters.

The key to building a strong DNVB can be attributed to perceived quality, price value, and ease of purchase.

Convenience Change + Price Change + Perception of Quality Change > 0

Convenience: ease of purchase, superior customer service, ease of return, and quality warranty.

Price: is the price comparable and or cheaper than the premium incumbent brand prices.

Perception of quality: how is the brand perceived? Is there an affinity for the product?

Whereas, if the DNVB’s sum “change” is greater than zero, the DNVB may be a better option than the incumbent. It’s through this lens that DNVBs and CPG brands have been able to position their products against stodgier, traditional brands. One of the keys to building an online retail presence is emphasizing both components of a winning formula: product and narrative. That narrative communicates quality, community, and brand equity around the product. For DNVBs with $5M or less in total funding, you can argue that the narrative is as important as the product itself.

Issue No. 254: An Open Letter to DNVB CEOs:

DNVB executive teams build two products from scratch, supply and demand:

- The product: the shirt, or the luggage, the pants, the shades, the coats, or whatever it is that people know you for.

- The brand: the aura of that product, the name recognition, the association, the behind-the-scenes partners, the spokeswomen, the ambassadors, the inevitability of success.

Both Raden and Away were founded in the early months of 2015. Raden raised a seed investment from Lerer Hippeau, First Round Capital, and Gin Lane – the famed and de facto kingmaker of DNVBs. Away raised a star studded seed round that included Andy Dunn, the now-Walmart executive who coined the DNVB acronym.

When Udashkin was interviewed by Loose Threads in 2015, Udashkin indicated that product was the entirety of his focus. He went on to add that the product’s narrative wasn’t something that Raden was going to emphasize.

After spending almost a year in the prototype phase, working out of San Francisco, Los Angeles, Montreal, and Taiwan, Raden emerged as a product company that rejected the imagery and celebrity of lifestyle brands.

Udashkin went on to say: “How can you have a lifestyle on day one around your product unless you’re faking it? I think that works in the short term, but over time the customer gets smarter. If you don’t keep working on your product, eventually you lose.”

Cofounders Steph Korey and Jen Rubio took a nearly opposite approach to building their competing brand. In a July 2017 segment in Inc Magazine called “How I did it”, here is what was said about the duo:

Steph Korey and Jen Rubio had a problem. Their planned launch of Away, a new luggage brand, was fast approaching–and none of their suitcases would be ready to sell in time. Luckily, the two had a social media trick packed in their bags. They turned a proven retailing tactic, the preorder, and an idea for a book into a campaign that went viral on Instagram and beyond.

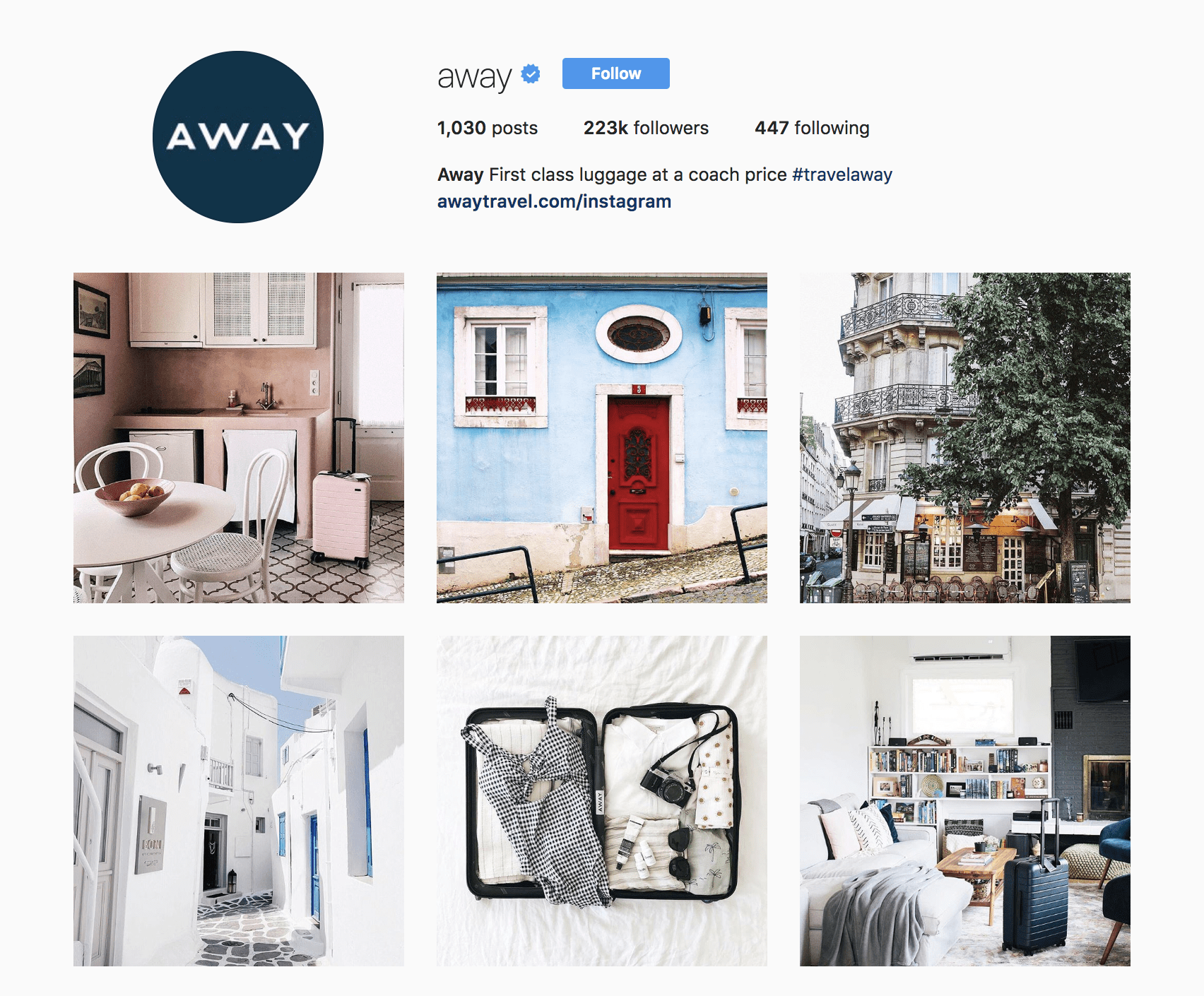

This thinking permeates through their entire product position. Whereas Raden’s Instagram focused solely on the products being sold, Away’s Instagram account features as much lifestyle and usability as it does the products that Away sells.

While Away focused on the destination and brand affinity (to include a print magazine called “Here”), the relationship that Raden maintained with customers was altogether different than the one that Away hopes to continue. The difference between the two approaches greatly affected each brand’s product offering: Raden’s was narrow, Away’s is wide. Here’s a pivotal point in today’s featured article by Fast Company:

He walks me through the math. The target market for a direct-to-consumer suitcase brand is relatively narrow. This is not a mass purchase. Your audience is people with enough disposable income to spend between $200 and $400 on a carry-on, but also be digitally savvy enough to be willing to buy the case online, rather than in a department store.

Once the startup has convinced someone within their target market to buy a carry-on, the relationship is basically over. With some persuasion, the brand can try to sell them a piece of checked luggage or perhaps another small travel accessory. But the lifestyle value of each customer is relatively small, compared to other categories. A direct-to-consumer luxury shoe brand like M.Gemi can sell a woman a new pair of $300 shoes twice a year for the rest of her life. Everlane can sell a customer wardrobe updates every month.

Elizabeth Segran, Fast Company

Here Udashkin suggests that he did the right thing by focusing on product superiority alone (just one of the three components to the DNVB formula). But because he saw no value in building a brand and narrative around Raden, there were fewer alternative products that he could offer to his existing customers. This, in addition to his luggage’s immovable battery and the startup’s shorter runway influenced his position that the luggage maker had no choice but to cease operations. He also suggested that there was no market for these types of products in the long run, a far-reaching assertion.

In an email to 2PM, Away CEO Steph Korey explained Away’s position:

A brand’s success isn’t determined by the amount of money it raises, or by any other one thing, but by the right combination of a lot of little things.

For us, it’s been the combination of having a customer-obsessed approach to everything we do (taking the time to listen to our customers, deeply understand what they’re telling us, and then quickly acting on it), being conscientious about the way we introduce them to the brand in the first place (ensuring what we’re marketing will be interesting to who we’re marketing it to, and simultaneously creating a narrative that’s authentic to who we are as a brand no matter the channel or intended audience), and not limiting ourselves to any one product or plan for the future (expanding from one suitcase to dozens of travel goods since launch, and setting our sights on fixing everything that’s currently wrong with the travel experience).

One of the early lessons in DNVB branding is one that cannot be explained by analytics and logic, alone. It’s too subjective. Phil Knight’s once-fledgling shoe operation sold shoes but Nike was never a shoe company: it was a company that enabled champions. Tesla sells cars but Tesla is a company for futurists. Apple sells computers but it’s a company for creators.

For aspirational products, consumers choose brands that fit their lifestyle, belief system, and goals. From the very beginning, Away achieved something that very few DNVB’s understand early on. Building the product is only half of the battle. This means that no matter what arduous regulations they may encounter, they will maintain a canvas to build products that are relevant to their community of passionate, millennial travelers. It’s likely that as traditional sales continue, you’ll see a growing number of SKUs, styles, and add-ons that are beloved by millennial travelers and commuters. Yes, Steph Korey and Jen Rubio sell luggage, but Away is a travel company. And Away will go where she wants.

Updates: On June 26, Away announced the Away x Dwayne Wade collaboration. On June 28, Away announced a $50M round of investment, one of the largest rounds by female founders in history. According to their Comms Director Cassi Gritzmacher:

With this latest round of funding, Away plans to further establish itself worldwide by extending to new markets; continue to expand its product line to create the one perfect version of everything you need to travel seamlessly; expand its physical retail footprint (opening 6 new stores by the end of 2018 in addition to its current New York, Los Angeles, San Francisco, and Austin locations); build on its existing social impact efforts (through its partnership with Peace Direct and through new initiatives); and create 249 new jobs over the next five years, transitioning the team into a 56,000-square-foot new Global Headquarters in its hometown of New York City.

Leia mais sobre o assunto aqui.

Por Web Smith e Meghan Terwilliger | About 2PM