I did something slightly different this year: I opted out of Black Friday and Cyber Monday.

It was an experiment to see if I could withstand the many advertising and consumer forces that I always loved. eCommerce has long been a drug of choice and I’d been in denial about the hold it had on me. But my push to change didn’t start with America’s biggest holiday.

Earlier in the fall of 2024, I adopted a new philosophy: I would not purchase an article of clothing unless I felt that it would last my natural lifetime (this excluded many technical fabric textiles). From there, I selected a minimalist number for each category of my wardrobe items:

- Six sweaters or sweatshirts

- Five pairs of pants

- Six polo shirts

- Three belts

- Three pairs of shoes

I would then rotate these pieces based on the day and combination. The goal? To reduce my personal spending and address my reliance on an overburdened textile industry rife with harmful materials and processes—each contributing to an outcome that was invisible for far too long. Brands like Indi+Ash, Firstport Company, Sid Mashburn, Fair Harbor, and Merz B. Schwanen led the fall/winter wardrobe. Ministry of Supply was the only exception to this rule; they’ve since ventured into products manufactured sustainably.

This became a deliberate shift in mindset and, therefore, the basis upon which I approached the consumption framework that perfectly aligned with the themes in Buy Now! The Shopping Conspiracy.

Netflix’s documentary Buy Now! The Shopping Conspiracy came right on time in the run-up to Black Friday and Cyber Monday – a cultural phenomenon that epitomizes consumerism at its most extreme. As holiday sales are about to overwhelm people, the film deconstructed how multinational corporations engineer overconsumption that results in environmental and social devastation. The documentary’s release was a kind of reminder that this shopping frenzy is not just an economic event; it is also environmental and psychological, with effects reaching far beyond the holiday season.

The Engineered Cycle of Overconsumption

Directed by Nic Stacey, Buy Now! shows global brands using sophisticated marketing and conversion rate optimization tactics that trap consumers in an endless buying cycle. Former executives from companies such as Amazon, Apple, and Adidas admit their roles were to optimize consumption. From sleek advertising to disposable product designs, corporations have made shopping seamless-one in which consumers act on impulse rather than need.

The film’s narrator—a digital assistant-inspired character named Sasha—walks viewers through staggering statistics. Globally, 2.5 million shoes are manufactured every hour, and 13 million mobile phones are discarded every day. These numbers are presented through vivid animations, illustrating the sheer scale of production and waste. It’s a problem largely hidden from the consumer’s view but painfully visible in places like Ghana, where mountains of discarded clothing and electronics accumulate, as documented by the Or Foundation.

The Black Friday Effect

The Black Friday and Cyber Monday phenomenon is a philosophy that Buy Now! sets out to challenge. Once an American ritual connected to Thanksgiving, Black Friday has gone global, long-removed from its historical context. In the United Kingdom, Black Friday has been embedded into the retail calendar for a little more than a decade, primarily driven by online giants like Amazon.

It is not consumer demand that drives this growth but an ecosystem predicated on short-term gain over long-term sustainability. Companies push products to fail or become obsolete to drive consumers back into the marketplace. This is called planned obsolescence, wherein a steady stream of revenue is ensured while leaving a legacy of waste.

What this reveals more poignantly, however, is Amazon’s place within that narrative. It’s this frictionless buying that the company has – first – pioneered and – second – mastered. This vivid history was shared by former user experience designer Maren Costa. One-click purchasing and speedy delivery reduced barriers to buying on psychological levels and made it easier for consumers to rack up goods. Later let go (reportedly due to her activism within Amazon), Costa revealed the tension between corporate objectives and individual initiatives that work for change.

The Global Waste Crisis

The ecological consequences of consumption are overwhelming; more than 15 million pieces of clothes, rejected mainly by Western consumers, arrive in Ghana each week. These often consist of low-quality, fast-fashion items that cannot be repaired or sold and thus enter the textile waste stream. Similarly, this proliferation has created a new category of electronic waste. Much of it lands in landfills or is incinerated and releases toxic chemicals into the air.

Stacy’s documentary underlines the fact that the problem is not only one of waste management but also one of production and consumption. As former CEO of Unilever Paul Polman says in the film,

Away isn’t a magic place; it’s just somewhere else on Earth.

From clothes to electronics to plastics, the products of our lives rarely meet their maker when they leave the consumer’s hand; instead, they linger on as pollutants, microplastics, or non-biodegradable waste.

The Role of Consumers and Corporations

The film made a point that while individual actions, such as buying less and repairing items have value, the scale of the problem demands systemic change. This requires not just changes in consumer behavior but also in corporate practice and public policy. Several contributors to the film put forward a number of directions in which movement might take place:

- Extending Product Lifespan: Companies should focus more on making products durable than disposable. One of the very striking examples was drawn from the movie-a Hong Kong-based cloth manufacturer that 15 years ago tested garments, washing them 50 times to ensure their good service life. Nowadays, companies have given up such policies in favor of cheaper quick fixes.

- Policy Interventions:Through the use of appropriate legislation, governments could offer incentives for sustainable practices and wasteful ones. For instance, policies requiring companies to manage end-of-life disposal of their products, like extended producer responsibility in some regions.

- Consumerism Consciousness: The film does not directly blame the consumer but it does make the consumer stop and think about how they consume.

The Black Friday Paradox

The timing of Buy Now! underlines a paradox: Black Friday and Cyber Monday are – both – holidays of consumption and a time for reflection. While millions peruse retail websites, the film challenges viewers to consider the real cost of what they buy. The temptation of discounts often blinds consumers to the hidden costs: environmental degradation, labor exploitation, and the perpetuation of a wasteful system.

To retailers, Black Friday has become a make-or-break moment. Companies pump money into advertising and logistics to capture as much consumer spending as possible. But as Buy Now! made clear, this relentless drive for growth is coming at the expense of sustainability. Even brands that tout themselves as ecologically friendly are not beyond reproach; greenwashing, or making spurious claims about environmental benefits, is rife during the holiday season.

Hope Amid the Chaos

But despite the bleak subject matter, Buy Now! ends on a note of hope. The film found particular traction among young people, many of whom have been discussing the topic – both at the micro and macro levels – on TikTok. And the #BuyNow hashtag has accumulated millions of views, indicating a growing consciousness.

The documentary’s immediate success is proof that times are changing. According to Stacey, people who don’t even call themselves environmentalists have been inspired to think twice. It’s at least a cultural shift that can help grease the wheels for systemic changes more broadly.

*****

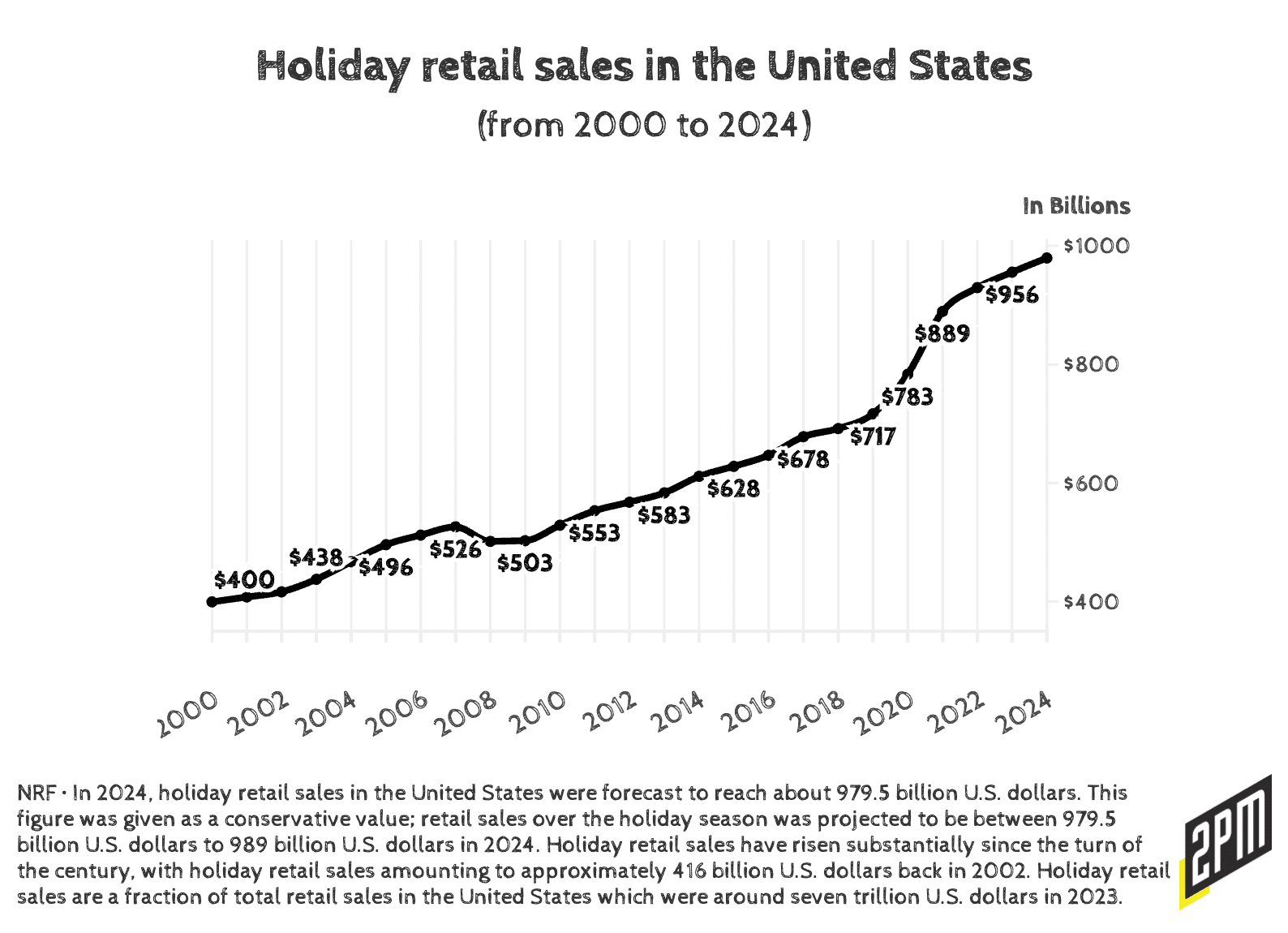

The lessons learned go far beyond Black Friday and Cyber Monday. Consumers must avoid the equating of happiness with material possessions. Corporations will also have to adapt to a new paradigm where sustainability will stand shoulder to shoulder with profitability. As the documentary eloquently concludes, “Whoever dies with the most stuff does not win.” The true measure of progress lies not in how much we consume but in how thoughtfully we live. This was another record-breaking Black Friday.

Sustainability is the wrong word, we need a reversal of policy, a reversal of collection, and a solution for the waste that has already left our grasp – from cardboard box to $17 Temu dress and $9 disposable men’s razor.

Por Web Smith