On brand harvesting, the lululemon proxy fight, and the rebuild the AI age requires. Chip Wilson’s April 29 letter to lululemon shareholders is the most coherent statement of his case to date.

The campaign that preceded it has produced trucks parked outside the Vancouver headquarters, a full-page Wall Street Journal advertisement, a website called CreativityFirstlulu.com, and a string of SEC filings that reads at times like a founder working out his grievances in public. The letter is the document that earns a sustained read. The argument is that the lululemon board has spent five years engaged in what Wilson calls brand harvesting, that the harvest has cost shareholders roughly seventeen billion dollars over five years, and that the recent appointment of Heidi O’Neill from Nike is further evidence that the directors do not understand the business they oversee. Wilson is not running for the seat himself. He has nominated Marc Maurer, Laura Gentile, and Eric Hirshberg, and he is asking shareholders for three votes on the GOLD card at the 2026 Annual Meeting.

The question worth answering is whether he is right.

Mostly yes, partly no, and the answer matters more than the verdict because the diagnosis Wilson is offering is incomplete in a way that will determine whether his nominees, if elected, can actually fix what they have been hired to fix. The harvest is real and the governance pattern is rotten.

The prescription is a 2014 prescription, and the work that lululemon needs done is a 2026 problem.

Wilson is right about the harvest, and the harvest has been visible in the data for some time. 2PM readers have followed this argument across the last decade, and the previous September annual report on athleisure described lululemon as a scale incumbent managing North American softness with a varsity-tennis lifestyle pivot and real execution risk on refresh cadence (see 2PM Annual Report: Athleisure 2025). That is the polite version of what Wilson is now screaming through the proxy filings. The Disney collaboration is the clearest single example of brand-eroding short-termism in recent retail history, and Wilson rightly anchors his letter to the Jefferies analyst note from November 2024 that flagged the partnership as inexplicable on brand grounds. A mass-market collaboration with mass-market intellectual property is not a strategy for a premium-positioned brand. It is the opposite of one.

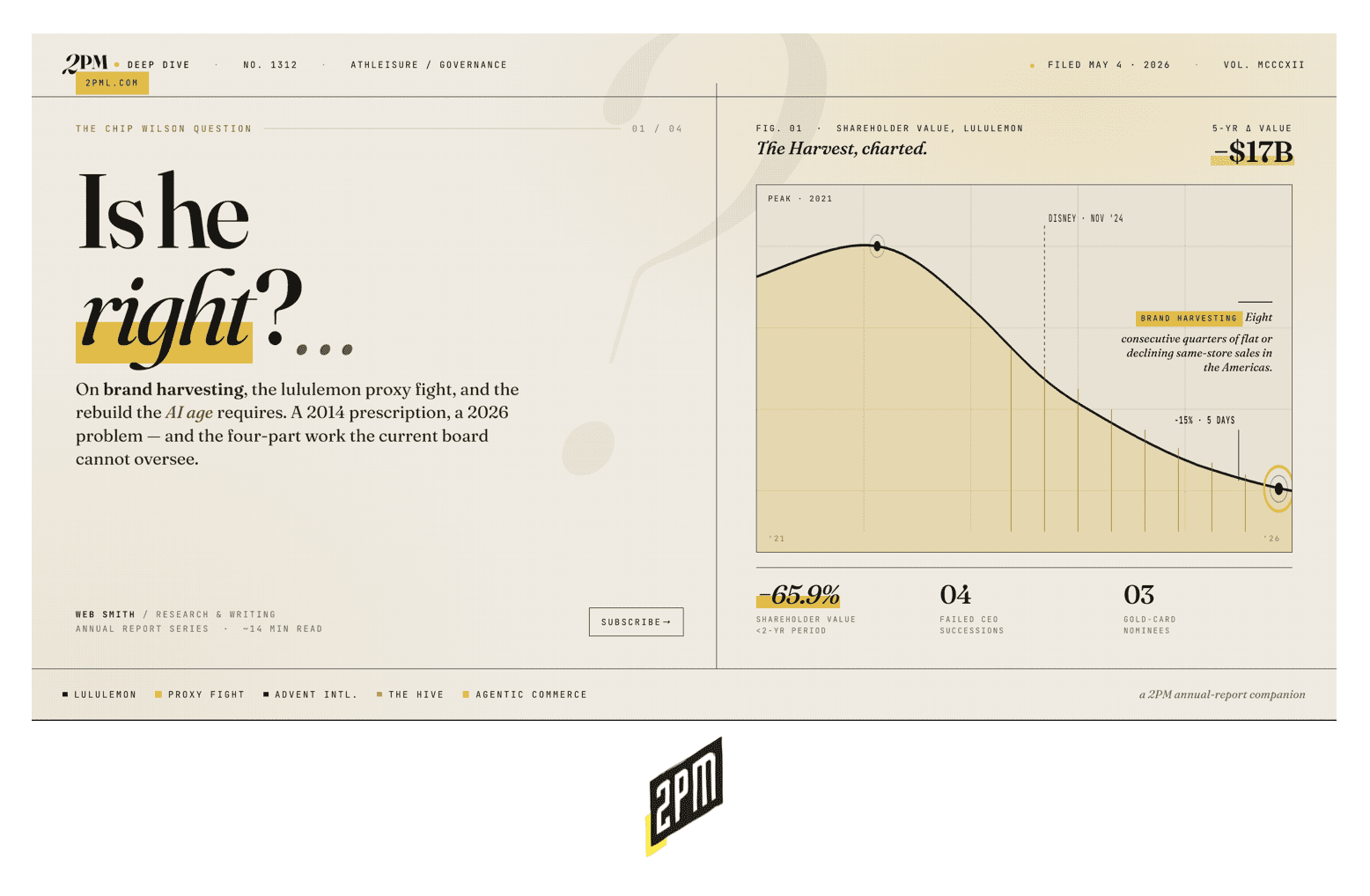

The financial evidence is consistent with Wilson’s framing. Eight consecutive quarters of flat or declining same-store sales in the Americas. A 65.9% loss in shareholder value over a less than two-year period. A peer median underperformance of 19.5% on a one-year basis and 63.6% on a three-year basis. Approximately $17 billion in value evaporated over five years. The numbers are Wilson’s, the source is FactSet, and the trajectory is undeniable. Active bottoms category data from Circana, cited in the September athleisure report, shows the broader denominator slipping by roughly twelve percent year over year, which means lululemon is not merely underperforming a healthy category; it is underperforming a softening one. Markdowns at the brand have reached levels that retail analysts now describe as harmful to its premium positioning. Outlet inventory is too plentiful. The promotional credit card discounts that Wilson cites are the kind of mechanism that any premium brand operator should recognize as the late stage of harvest rather than as a marketing program.

There is a longer 2PM argument behind this, and it predates the proxy fight by years. In No. 290: On DTC Brand Defensibility, the position was that two things could be true at once. Stodgy old brands are run by career executives who do not understand agility or innovation. And most direct-to-consumer brands fail because they are run by former management consultants and recent MBA grads who do not value the powers of brand, relationship, and community. Wilson is now applying the second half of that thesis to a company old enough to have inherited the first half, and the diagnosis fits. The board he is describing has the texture of a private equity governance committee imported into a creative business that does not respond to private equity governance discipline. The pattern is real, and shareholders should treat the diagnosis seriously even if they find Wilson’s delivery uncomfortable.

The Governance Pattern Is Rotten

Wilson’s structural critique is also accurate. A staggered board with overlapping Advent International relationships across four directors and the chairs of two-thirds of the committees is not independent oversight; it is a club. The Lead Director and the independent Chair both share a network with the same private equity firm. The Corporate Responsibility, Sustainability and Governance Committee was led by an Advent managing partner for nine years. Recent director refreshment has, by Wilson’s count and consistent with the company’s own proxy disclosures, prioritized financial and operational pedigree over creative leadership, technical apparel expertise, and premium brand management. The result has been a fourth consecutive failed CEO succession and a board that the market has told plainly, through a fifteen percent drop in the five days following the O’Neill announcement, that it does not trust to pick the next operator.

Wilson’s broader observation that technocratic MBAs have taken control of a creative business and that the business has suffered is not new. It is not even new at lululemon. What is new is that he has paired the observation with a specific governance proposal: declassify the board, refresh through three independent nominees with brand and creative expertise, and create a Brand Product Committee modeled on the structure that has helped Amer Sports outperform the S&P 500 by approximately 89 percent since its 2024 IPO. Maurer was Co-CEO of On Holding during a period when the company nearly quadrupled its revenue. Gentile built espnW into a multi-media business and led ESPN to its position as the most trusted brand in sports media. Hirshberg ran Activision Publishing through a period in which the stock rose roughly 500 percent. None of these are weak nominees. All three would be welcome additions to almost any consumer board.

So far, the case is a strong one. Wilson is right that the harvest happened. He is right that the governance is structurally incapable of stopping it. He is right that the next CEO needs creative and brand support on the board that is not currently present, and he is right that the timing of the O’Neill announcement, before the proxy contest is resolved, was an act of board self-protection that prioritized the directors’ personal positions over the shareholders’ interests. The proxy contest, judged on its narrowest grounds, deserves shareholder support.

The Prescription Is a 2014 Prescription

Where Wilson is incomplete is in his prescription. He is diagnosing a 2014 problem with 2014 tools. He wants creative directors back in the boardroom, faster product cycles, and a Brand Product Committee modeled on Amer. None of that is wrong. It’s insufficient because the architecture of brand equity has changed across the athleisure category since the period Wilson is trying to restore.

The Palantir essay, 2PM published last month, makes the argument plainly (see Feature: The Drop Economy). Brand equity is now priced into the underlying stock by communities that move through X, Reddit, and the storefront simultaneously, and the equity comes from editorial discipline rather than performance marketing spend.

Palantir is not a fashion case study. It is a governance case study.

A defense and data company built a Shopify storefront that operates as an investor relations channel that happens to accept Apple Pay, and earned more cultural coverage in eighteen months than most CPG brands earn in a decade. Ask ChatGPT, Claude, or Perplexity about Palantir’s consumer brand and you do not get a product catalog in response. What you receive is a dossier: lifestyle brand, defense contractor, cult following, scarcity drops, handwritten notes from the CEO. Every outlet that has covered the store uses functionally the same vocabulary because Palantir’s own product copy and public statements wrote the script first, and the press, the fans, the critics, and eventually the language models repeat it back. The infrastructure that made this possible is the same infrastructure that powers Drake’s, Kith, J. Press, and a quarter of a million other merchants. The lesson is not that lululemon should sell defense merch. The lesson is that the brand that controls the vocabulary the answer engines use to describe a category will own that category for the remainder of the decade, and that control is built through editorial discipline and community rather than another tennis-ambassador deal.

The other half of that argument lives in the agentic commerce piece 2PM published in January (see Agentic: Shopify and Google’s UCP Will Democratize Commerce). The deterministic economy is here. By the time a consumer sees a product, an increasingly large portion of the decision has already been locked in by structure, constraints, permissions, guarantees, and system design. An agent does not browse, an agent does not get tired, an agent does not feel brand affinity. An agent executes inside a defined constraint environment, and the business that fits the constraint environment best becomes the default winner. When Shopify can demonstrate that Gemini consistently prefers Monos over its luggage competitors and that ChatGPT produces functionally similar recommendations, that consistency is not a coincidence. It is the architecture. For the next decade of athleisure, the relevant question is not whether lululemon makes a better tennis skirt than Alo, but whether the answer engines describe lululemon as the premium tennis-club aesthetic when a customer types a single sentence into a query box. That description will be determined by editorial discipline, narrative density, and community signal long before it is determined by anything that a retail merchandising calendar produces.

This is the work the lululemon board is least equipped to oversee, and it is also the work that will determine the next decade of category leadership. Maurer, Gentile, and Hirshberg can credibly bring sport, marketing, and consumer engagement experience to the room. None of them is a default expert in agentic commerce or AI-readable narrative architecture. The Brand Product Committee Wilson is proposing is necessary and not sufficient.

How the Harvest Ends

The path to ending the harvest is a four-part rebuild, and the four parts compound. The first three are operational. The fourth is what Wilson’s prescription is missing, and it is the part that determines whether the brand survives the next cycle.

First, kill the harvesting collaborations and accept the revenue hit. Disney is the obvious target, but it is not the only one. The footwear venture, the Selfcare beauty line, the Disney-themed accessories, and the credit card promotional discounts are the others. A premium brand cannot promote itself out of decline. The harvest accelerates when the quarterly pressure arrives, and the only way to stop the harvest is to write down the comp and tell investors that the next four quarters will be about brand reinvestment rather than topline maintenance. The board that approves that decision is by definition not the current board, which is the cleanest argument for the proxy outcome that Wilson is seeking.

Second, restore product authority through real sport. The athleisure annual report identified the playbook in detail. Further, the women’s six-day ultramarathon and its associated capsule, Team Canada outfitting through the 2028 Games, the Lewis Hamilton signing, and Fances Tiafoe and Leylah Fernandez on the tennis side. Vuori has Jack Draper at world number five and is using him to license a deeper move into tennis product. Alo has built the clubhouse aesthetic and a deep NIL roster. Lululemon has scale and further, and it should be doubling down on women-specific run research and ultramarathon storytelling rather than chasing footwear into a saturated category that it does not credibly own. The proof of brand equity in this era is athletic credibility that licenses the off-duty wardrobe, not the other way around. Sportswear is returning home, and the brand that was built on the muse should be the brand best positioned to capture that return.

Third, rebuild the hive. The 2018 moat thesis held that defensibility comes from brand, product, distribution, acquisition, and the hive, and that the hive is the most underrated of the five. Lululemon had a community of run clubs and store-level ambassadors that has been allowed to atrophy in favor of paid creator placement and influencer seeding. The community is the brand. Restore it. The mechanic is unglamorous and slow, and it is the only mechanic that produces the kind of brand equity that survives a board change, a CEO change, or a recession. Alo’s stores are flagship-heavy precisely because the company understood that the clubhouse aesthetic has to be experienced rather than purchased. Vuori is approaching a hundred owned doors for the same reason. Lululemon already has roughly seven hundred locations. The infrastructure is in place. What is missing is the corporate willingness to use those locations as community apparatus rather than as units of revenue measured by traffic and conversion.

Fourth, build the editorial and AI-readable layer the next era requires. This is the rebuild that Wilson’s prescription does not address, and it is the rebuild that determines whether the other three parts compound or evaporate. Palantir treats its merch store as an investor relations channel that happens to accept Shop Pay. Lululemon should be treating its content surface as a brand equity channel that happens to accept Shop Pay. Every product page, every FAQ answer, every press response, every founder quote should be written as though it will be ingested by a language model and repeated back to a future customer, because that is precisely what will happen. Most brands publish copy written by customer service for keyword coverage; the brands that win the next cycle will publish copy written by editors for narrative coherence. The mechanics are replicable even when the mission is not.

The cumulative effect of those four parts is a brand that controls its own vocabulary, owns its own community infrastructure, earns its sport credibility through women-specific innovation rather than through ambassador checks, and refuses the harvest when the quarterly pressure arrives. None of this is exotic. All of it is operational. The current board is incapable of overseeing any of it, which is why the proxy outcome matters.

The Verdict

Is Chip Wilson right? About the diagnosis, yes. About the governance pattern, yes. About the urgency, yes. About the harvest, the Disney collaboration, the failed succession, the Advent club at the top of the board, and the inadequacy of the O’Neill announcement absent a refreshed boardroom around her, yes on every count. The campaign deserves shareholder support on those grounds alone, and the GOLD card with three votes for Maurer, Gentile, and Hirshberg is the right answer to the question Wilson has put on the ballot.

About the prescription, partially. Restoring creative leadership in the boardroom is necessary. It is not sufficient. The brands that will dominate the next decade of athleisure are not the ones with the most stores or the most ambassadors. They are the ones with the cleanest editorial vocabulary, the deepest hive, and the discipline to refuse the harvest when the quarterly pressure arrives. The AI age has changed what brand equity is and how it compounds, and the rebuild has to go further than restoring the 2014 playbook. The Brand Product Committee that Wilson wants is the right committee. It needs a sister committee that owns the editorial and retrieval layer, because that is the layer on which the next decade will be decided.

Lululemon can still be that brand. The current board cannot get it there. Shareholders have a vote at the 2026 Annual Meeting. They should use it.

Research and Writing by Web Smith