Этот краткий обзор предназначен исключительно для Исполнительные членыЧтобы упростить членство, вы можете нажать на кнопку ниже и получить доступ к сотням отчетов, нашему списку DTC Power List и другим инструментам, которые помогут вам принимать решения на высоком уровне.

Memo: Regenerative Beef Trends, Marketing, and Reality

Beef is the most interesting topic in retail. By the end of this, you may agree.

Will Harris is the principal at White Oak Pastures. A fourth-generation cattlemen, Harris cultivates land and cattle that was passed down to him from descendants as far back as 1866. Educated at the University of Georgia, Harris was trained on industrial farming techniques that were popularized in the 1940s to feed a booming, middle-class economy. These methods include the typical pesticides, antibiotics, hormones, feed, and herbicides customary to American diets. Today, Will Harris is a regenerative cattle rancher whose detailed approach to farming is measured down to the microbe. I listened to a recent interview of his shared by a friend and cattle rancher. This soundbite has shaped the present and future of beef:

What you’re doing is fine, Will, but you can’t feed the world like that. And my response is, “I don’t know that I am supposed to feed the world, I think I’m supposed to feed my community.

In recent years, the term “regenerative beef” has emerged as a popular marketing buzzword, heralded as a sustainable solution to environmental concerns associated with beef production. This essay examines the science and work that defines this word, one that has the potential to become a disingenuous marketing term, especially in light of the challenges the farming practice faces when scaled up.

This includes Walmart’s new initiative to redefine itself as a regenerative company; the economic realities of beef production and consumption, and the broader context of sustainable development all serve as critical lenses through which to understand this issue.

Started raising cattle at [the] Ko’olau ranch on Kauai, and my goal is to create some of the highest quality beef in the world.

These were the words of the owner of Ko’olau ranch, a 1,400-acre compound on Hawaii’s oldest island, according to a recent report by The Guardian. That property owner and modern rancher is Meta billionaire Mark Zuckerberg, who aims to raise the Rolls-Royce of beef.

Rolls-Royce manufactured 6,000 vehicles in 2022 up from 5,586 in 2021. In 2022, Ford manufactured 1.8 million vehicles. One car company manufactures for quality and the other manufactures for industrial scale. If this analogy was used for the production and marketing of beef, by the growing number of modern retailers, it would look something like this:

Over one dozen brands are vying for market share to be the Rolls-Royce of meat producers which requires production to look more like Ford’s, defying the ideals of the practices that established Rolls-Royce over decades.

The bottom line: there is only so much space in the regenerative meat market before it’s not regenerative at all. This means that companies should assume that the market is fixed and that expansion of supply either comes by degrading production or acquiring the supply of a competitor’s.

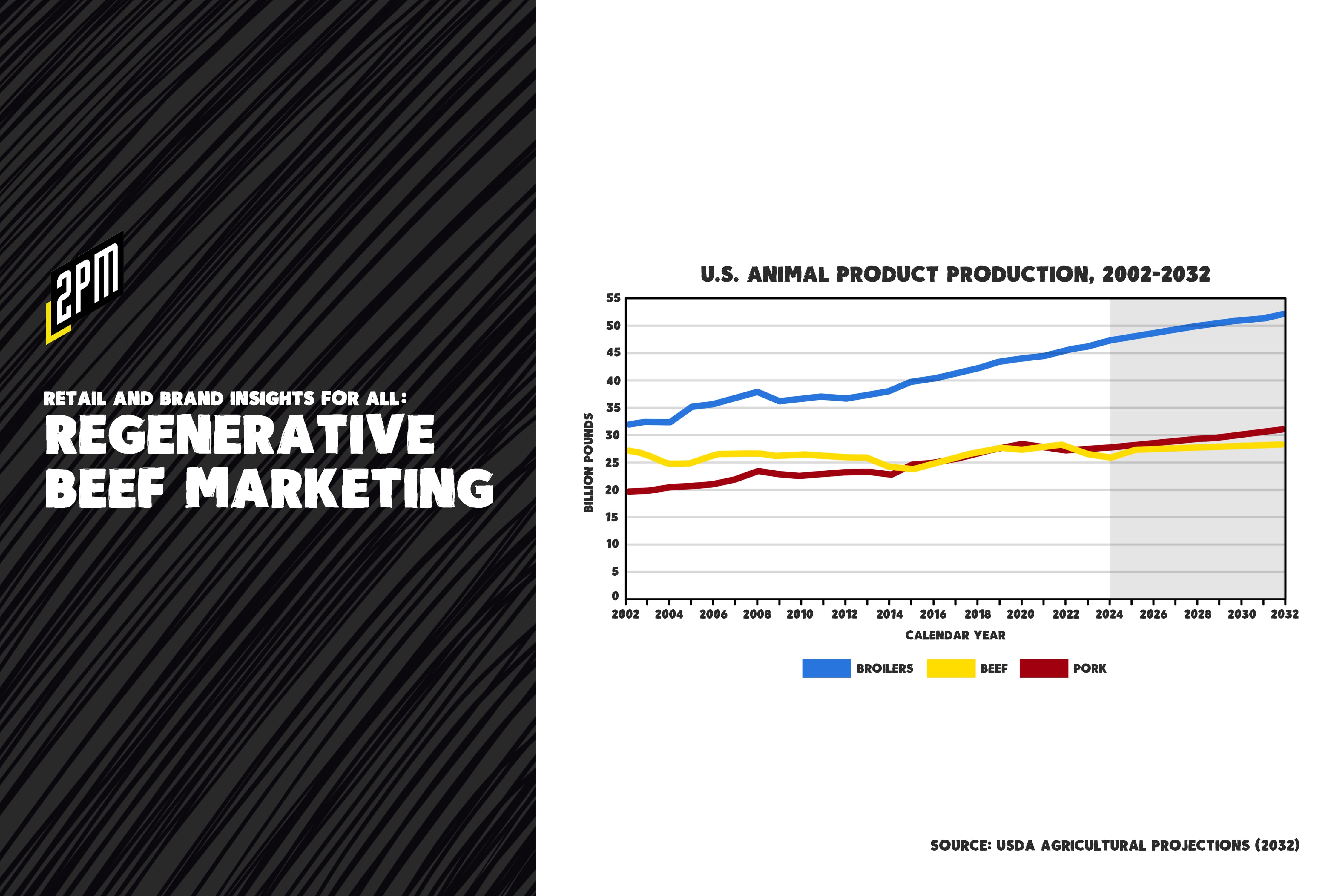

In short, there are now dozens of meat-based brands (across CPG and fresh foods categories) that are competing for market share in a segment where the supply is level, the demand is level, but the merchants are growing by the year. Look no further than the projection by the USDA, pictured above: chicken production will grow, pork production will inch up, beef production will remain the same.

Recent developments in both the traditional and alternative meat sectors suggest an ongoing struggle for market dominance, with each segment grappling with unique challenges. [Just Meat]

The use of the “regenerative” tag in beef production can be seen as a worthwhile initiative. The use of the tag in marketing is a form of virtue signaling, a term used to suggest that capitalism can be aligned with a corporation’s moral values, often with little regard to the totality of their impact. This use of the term can dilute its meaning and potentially mislead consumers about the environmental impact of their food choices.

Walmart’s Regenerative Foodscape

Here is a case in contradiction. Walmart, the world’s largest retailer, is now attempting to position itself as a leader in regenerative agriculture, despite the inherent contradictions with its low-cost business model. The Walton family, owners of Walmart, have made vast investments in regenerative agriculture. While these efforts might seem commendable, they potentially reshape the marketplace in a way that undercuts the true essence of regenerative practices. The Walton family’s influence over the food system, reflected in their substantial investments, does not align with the fundamental principles of regenerative agriculture, which prioritize environmental sustainability over profit and scale. Regenerative methods and capitalism rarely align. So for Walmart to attempt to own the narrative is especially concerning for those who are authentic about their duty to the regenerative agriculture movement.

It’s important to note that Walmart faced tension between two dueling concepts, once before: the organic produce market and its low-cost model. Organic produce economics and regenerative agriculture are systems with overlapping values, restrictions, and aspirations. As a foretelling of sorts, Walmart sells organic produce at a cost as much as “25% cheaper than any other grocer,” according to the company. From Walmart’s ‘Regenerative Foodscape’, a November 2023 report by Civil Eats:

Even if the Walmart fortune is truly creating a rising tide toward a more regenerative food system, it may be unlikely to lift the most battered of boats: those small, regenerative, diversified farms selling healthy food to their neighbors. Because at the end of the day, it costs more. And not only have they been losing money for years, they’re still caught in the everyday-low-price hurricane, trying to stay afloat within a system that rewards producers who scale up to sell at Walmart’s prices.

The expansion of Walmart’s grocery business, with its emphasis on low prices, has historically encouraged practices that are antithetical to regenerative agriculture’s ethos of ecological balance and sustainability. So the question becomes, if regenerative agriculture-based companies partner with Walmart – can they too be considered antithetical?

The Economic Realities of Beef Production

The beef industry’s economic landscape adds another layer of complexity to the notion of regenerative beef. Inflation in the beef sector, as noted by Haden Comstock of NCBA, has led to a decrease in beef availability per capita in America.

This reduction in supply, coupled with a rise in prices, highlights the challenges of transitioning to a truly regenerative model. Beef, as a protein source, has maintained its demand despite rising prices, but the economic pressures on consumers, especially those with diminishing savings, indicate a possible future shift in consumption patterns. The tension between maintaining affordability and adopting sustainable practices poses a significant challenge for the beef industry, particularly in the context of ongoing environmental changes like droughts in the Midwest.

Regenerative Agriculture: Promises and Limitations

A July 2023 whitepaper by the American Farmer’s Network stated the following:

By choosing grass-fed beef, individuals can contribute to a more sustainable food system, support local economies, and enjoy the health benefits associated with this responsible and mindful choice. As we move forward, it is crucial to prioritize the adoption of sustainable farming practices and raise awareness about the positive impact of grass-fed beef for a healthier and more sustainable future.

The concept of regenerative agriculture is rooted in practices that enhance soil health, biodiversity, and ecological balance. However, the applicability of these practices to larger-scaled regenerative beef industry remains questionable. Proponents argue that regenerative agriculture can mitigate climate change and improve environmental sustainability.

However, this optimism overlooks the inherent limitations of such practices when applied to cattle farming. Regenerative grazing, while marketed as a solution to environmental degradation, often requires significantly more land and may not effectively reduce greenhouse gas emissions or address biodiversity loss as a result of the lack of necessary land. From “The Promises and Pitfalls of Regenerative Agriculture, Explained,” a recent report by Sentient Media:

“Regenerative grazing” of cattle has been marketed to consumers […]. However, research shows that cattle grazing in any form is a major source of climate pollution that contributes to biodiversity loss, and regenerative ranching requires up to 2.5 times more land than conventional beef production.

The industrial-scale application of regenerative techniques faces challenges. The current trends in regenerative agriculture, driven by private funding (including by the Walton family) and government investment, risk perpetuating a model of agriculture that falls short of its environmental promises due to the changing priority from effectiveness to scale.

Brazilian President Luis Inácio Lula da Silva was recently quoted at COP28 in Dubai of all places:

We want to convince the people who invest in agriculture … that it is completely viable to keep the forest standing and (still) have land to plant whatever we want.”

There he detailed a plan to regrow 99 million acres of deforested land within the decade. – an area roughly the size of Sweden – within a decade. Context Magazine notes that this exceeds the landmass of Sweden. And it comes at a time when Brazil faces potential EU regulations banning commodities produced by acts of deforestation.

There are critics that suggest that regenerative agriculture, specifically beef production, would require far more land than we currently maintain for cattle raising. This is the simplest limitation but it isn’t the only one. While Mark Zuckerberg plans to use his 1,400 acre ranch to produce some of the world’s best beef, the masses will another 99 million acres over the next decade to keep supply at a place where the growing number of demand-generating DTC brands and other retailers in the space are taking the industry (assuming that the all grow with proper unit economics). This is why the regenerative tagline seems lofty at best, disingenuous at worst.

Regenerative Beef: A Marketing Ploy?

The labeling of beef as “regenerative” often serves more as a marketing strategy than a reflection of genuine sustainability. Hopdoddy, an Austin-based chain of fast-casual restaurants, just grew its vendor-partnership with Force of Nature – another Austin-based venture. Hopdoddy’s vice president of culinary Matt Schweitzer explained that part of the objective for switching meat vendors is to bring attention to regenerative agriculture:

We felt like we could really take a stand and look to move our entire supply chain in a regenerative fashion, so we could really be proud of the work we’ve done and we could hopefully leave the animals, the farmers, the ranchers, the native grasslands, and our planet a better place than before we started.

The term suggests a level of environmental stewardship that may not align with the realities of scaling beef production for mass-market ventures. This misalignment raises concerns about greenwashing, where the ecological benefits of regenerative practices are overstated to appeal to environmentally conscious consumers. The regenerative beef narrative may give the impression that consuming beef, regardless of its production method, is compatible with a sustainable food system. This perspective neglects the broader environmental implications of beef production. But more importantly, it fails to mention the limitations of supply.

****

The rise of “regenerative beef” as a marketing tagline represents a complex interplay between environmental aspirations and economic realities. While the concept of regenerative agriculture holds promise, its application to beef production at scale is fraught with challenges. Companies like Walmart, despite their investment in regenerative practices, operate within a framework that prioritizes scale and cost-efficiency, potentially undermining the principles of regenerative agriculture. The economic pressures on the beef industry, coupled with the need for environmental sustainability, call for a nuanced understanding of what regenerative practices can realistically achieve.

If the number of companies are growing and the strain on growers intensifies, is the corporate boom of direct-to-consumer meats true to its stated claims? As the global population grows and the demand for sustainable food systems only intensifies, it is important to look at this growing tagline with a critical eye and assess the claims of “regenerative meat” and the companies that rely on it to achieve scale.

Автор Веб Смит | Под редакцией Хилари Милнс с иллюстрациями Алекса Реми и Кристины Уильямс

Continue reading “Memo: Regenerative Beef Trends, Marketing, and Reality”

Глубокое погружение: 2024 год

При обычном понимании внешней политики можно предположить, что розничная торговля находится в точке совпадения, где пересекаются сразу три влияния.

Пересечение торговли и национальной безопасности стало сложной и многогранной проблемой для ритейлеров и торговых площадок, преодолевающих трудности, связанные с ценообразованием, доставкой, цепочкой поставок и прогнозированием спроса. В данном эссе рассматриваются три ключевых аспекта этого слияния: кибербезопасность (на примере Шейна), уязвимость морских перевозок (на примере проблемы Суэцкого канала) и проблемы в Индо-Тихоокеанском регионе (на примере тайваньского конфликта). Каждая из этих областей подчеркивает необходимость комплексного и стратегического подхода к защите национальных и корпоративных интересов при сохранении процветающей мировой экономики.

Показательным примером этого явления является мир электронной коммерции и сбора данных. Хотя этот вопрос подробно рассматривался в предыдущем отчете под названием "Где NATSEC встречается с коммерцией", к нему стоит вернуться в связи с его глубокими последствиями.

Возникновение китайских технологических компаний, таких как TikTok, Shein и Temu, оказало значительное влияние на глобальный ландшафт коммерции. Эти компании, используя свои модели "прямого контакта с потребителем", соперничают с американскими конкурентами и даже превосходят их. Примечательна симбиотическая связь между китайскими торговыми гигантами и налоговыми льготами. Посылки стоимостью менее 800 долларов уже давно разрешено беспошлинно ввозить в Соединенные Штаты, что стимулирует китайские компании продавать свою продукцию на американском рынке, минуя складирование на территории страны (до недавнего времени). Кроме того, Коммунистическая партия Китая (КПК) отменила экспортные налоги на эти товары, что способствует расширению доли рынка в США.

Китайский опыт в области сбора данных был накоплен раньше, чем в США, и он уделяет большое внимание данным от первых лиц. Китайская технологическая экосистема использует данные первых лиц для совершенствования алгоритмов поиска, оценки кредитоспособности и развития индустрии цифровых финансов. Такой обширный сбор данных вызывает опасения по поводу конфиденциальности и безопасности данных, учитывая возможность злоупотреблений и неправомерного использования.

Становится все более очевидным, что эксперты в области национальной безопасности и торговли должны объединить свои усилия. Понимание глубины знаний, которыми обладают обе стороны, имеет первостепенное значение, как гласит древняя мудрость "Искусства войны" Сунь-Цзы: "Если ты знаешь врага и знаешь себя, тебе не нужно бояться результатов ста сражений". В то время как правительственные чиновники могут бить тревогу по поводу материальных средств, необходимых для ведения боевых действий, таких как военные корабли, современное поле боя также охватывает данные и обширные знания, которые они представляют.

Становится все более очевидным, что эксперты в области национальной безопасности и торговли должны сближаться.

Последствия такого слияния коммерции и национальной безопасности далеко идущие, они затрагивают не только мировую экономику, но и суверенитет государств и частную жизнь людей. По мере того как мы углубляемся в сложности этого взаимодействия, становится очевидной необходимость применения тонкого и стратегического подхода.

Шейн против американского фондового рынка

Компания Shein приобрела широкую известность, особенно среди молодых людей, которые жаждут доступной и модной одежды с оперативной доставкой на дом. Видеоролики Shein, демонстрирующие рубашки за 5 долларов и бикини за 10 долларов, стали отличительной чертой маркетинговой стратегии компании.

Компания произвела фурор в сфере розничной торговли, применив уникальный подход. В отличие от традиционных ритейлеров, которые производят большие партии одного товара на сезон, Shein выбрала мелкосерийное производство, часто изготавливая только 200 единиц определенного товара. Такая стратегия позволяет свести к минимуму избыточные запасы, сократить расходы и максимально увеличить вероятность продажи каждого изделия - это стало возможным благодаря умелому использованию компанией Shein методов обработки данных и искусственного интеллекта для определения потребительского спроса и предпочтений.

Основанный в Китае в 2008 году, бренд Shein стал привлекательным для широкой аудитории во время пандемии, и даже родители начали изучать его доступные варианты. По всем показателям Shein стал одним из самых популярных брендов среди подростков, соперничая даже с Nike. Пока что Shein остается частной компанией, что не позволяет точно определить ее долю на рынке. Но это скоро изменится.

Компания Shein предприняла шаги к тому, чтобы стать публичной компанией: по некоторым данным, она подала заявку на IPO. Компания начала решать такие проблемы, как устойчивое развитие, отношение к независимым дизайнерам и прозрачность партнерства с влиятельными лицами - эти меры считаются необходимыми при выходе на публичный рынок в США. Однако самый важный вопрос остается открытым: безопасность данных.

Несмотря на то, что компания является частным предприятием, ее стоимость оценивается в диапазоне от 100 до 66 миллиардов долларов, что превышает годовой доход таких известных ритейлеров, как Macy's. Однако компания сталкивается с серьезными противоречиями, которые могут повлиять на ее выход на IPO. Один из них связан с обвинениями в использовании принудительного труда в цепочке поставок. Сообщалось, что компания Shein могла поставлять хлопок из Синьцзяна, региона в Китае, связанного с принудительным трудом, что ставит под сомнение соблюдение ею законодательства США.

Еще один вопрос связан с таможенными пошлинами, где Шеин пользуется правилом de minimis, освобождающим от пошлин импорт стоимостью менее 800 долларов. Критики утверждают, что это положение предназначалось для личных вещей, а не как лазейка для корпораций, полагающихся на дешевые и объемные перевозки.

Кроме того, быстрая и недорогая модель производства Shein согласуется с негативным воздействием индустрии быстрой моды на окружающую среду. Хотя компания предприняла некоторые усилия по внедрению экологичных материалов, критики считают эти шаги недостаточными, чтобы противостоять одноразовому характеру ультрабыстрой моды. Кроме того, китайское правительство может получить доступ к информации о клиентах Shein, учитывая происхождение компании и ее нынешнюю штаб-квартиру в Сингапуре. Я написал это в октябре 2023 года, не очень понимая, какое значение это будет иметь в 2024 году:

Сочетание глобальной кампании шпионажа Китая, вторжения России в Украину и ближневосточного кризиса заставило усомниться в способности разведывательного сообщества эффективно решать эти задачи и противостоять, казалось бы, незначительной проблеме электронной коммерции. Эта "незначительная проблема", движимая авторитарным китайским правительством и передовыми технологиями, подрывает верховенство закона и представляет серьезную угрозу не только для Соединенных Штатов, но и для их союзников. Ситуация требует повышенной бдительности и скоординированных усилий по противодействию этой многогранной угрозе.

Компания Shein сталкивается с растущим вниманием не только к своей деловой практике, но и к ее потенциальному влиянию на национальную безопасность. Запутанная сеть проблем и возможностей, связанных с восхождением Shein, подчеркивает сложный ландшафт современной розничной торговли и ее более широкие общественные и геополитические последствия.

Символика Суэцкого залива

Вникая в сложную паутину глобальных событий, которые будут происходить в 2024 году, нельзя не обратить внимание на растущую напряженность вокруг Суэцкого канала. Стратегическое значение этого исторического водного пути, соединяющего Индийский океан со Средиземным морем через Красное море, невозможно переоценить. Через этот морской коридор проходит около 12 процентов мировой торговли и 30 процентов всех мировых контейнерных перевозок, служащих кратчайшим путем между Азией и Европой.

В последние недели Суэцкий канал столкнулся с серьезными перебоями в работе из-за атак на судоходство, что вызвало волновой эффект во всей глобальной цепочке поставок. Это зловещее событие стало следствием действий поддерживаемых Ираном повстанцев-хути, базирующихся в основном на севере Йемена. Эти повстанцы, ссылаясь на поддержку палестинского дела в условиях конфликта между Израилем и Хамасом, начали кампанию, направленную против торговых судов в Баб-эль-Мандабском проливе. Этот водный путь соединяет южную оконечность Красного моря с Индийским океаном, что делает его жизненно важным пунктом доступа для морской торговли.

Первой целью повстанцев Хути стало японское грузовое судно Galaxy Leader, которое, по некоторым данным, частично принадлежит израильскому инвестору. Их действия вызвали обеспокоенность по поводу безопасности и стабильности судоходных маршрутов в регионе. В ответ на эти растущие угрозы министр обороны США Ллойд Остин недавно объявил о создании коалиции из 20 стран, в которой Соединенные Штаты занимают ведущее место, для защиты Суэцкого маршрута. Китай не входит в эту коалицию, что вызывает опасения, которые могут быть восприняты как враждебные.

Первоначальный план предусматривает размещение военных кораблей вблизи побережья Йемена для сдерживания и защиты от возможных атак хути. Однако острота ситуации может потребовать более комплексных действий со стороны американских военных, включая морское сопровождение уязвимых кораблей и потенциальные авиаудары по военной инфраструктуре хути.

Последствия этих событий глубоки и далеко идущи. В условиях, когда жизненно важный поток мировой торговли висит на волоске, прошлые ракетные атаки уже заставили судоходные компании отклонить более 100 судов от Суэцкого маршрута, перенаправив их в обход коварного мыса Доброй Надежды, расположенного на южной оконечности Африки. Эта радикальная мера увеличивает длину пути примерно на 6 000 морских миль и потенциально на три-четыре недели, вызывая значительные задержки и перебои в судоходстве по всему миру.

История напоминает нам, что перебои в работе Суэцкого канала, такие как длительное закрытие после Шестидневной войны 1967 года и громкая посадка на мель огромного судна в 2021 году, - дорогостоящие и рискованные мероприятия для глобальных грузоотправителей. Способность морской отрасли адаптироваться к таким вызовам подчеркивает уязвимость этого жизненно важного маршрута.

Текущая миссия по обеспечению безопасности судоходства через Суэцкий канал, метко названная операцией Prosperity Guardian, поднимает вопросы об использовании военной силы для защиты экономических интересов. Однако рассматривать эту миссию как защиту глобальной торговли - разумный подход. Обеспечение безопасности и стабильности этой морской артерии не только необходимо для стран, менее богатых и могущественных, чем США, но и является инвестицией в долгосрочную глобальную безопасность. Пока заинтересованные стороны не убедятся в полной безопасности Суэцкого маршрута (компания Maersk возобновила работу), мир розничной торговли будет продолжать испытывать на себе всю тяжесть сбоев.

Конфликт в Суэцком канале стал ярким напоминанием о том, как переплетенные сферы геополитики, торговли и национальной безопасности могут сходиться неожиданным образом, определяя мировоззрение в 2024 году и далее.

Китай, цепочки поставок и третья марионеточная война

Когда мы изучаем последний вызов глобальной розничной торговли, который будет определять торговый ландшафт в 2024 году, один вопрос вырисовывается масштабно и беспрецедентно: перспектива войны по доверенности между Соединенными Штатами и Китаем. Этот сценарий, более вероятный сегодня, чем когда-либо со времен Второй мировой войны, обусловлен крайне спорным вопросом о Тайване. Непоколебимая позиция председателя КНР Си Цзиньпина по объединению Тайваня с материковым Китаем представляет собой значительный риск, способный разжечь крупный конфликт в Индо-Тихоокеанском регионе.

Стратегическое значение Тайваня выходит за рамки его географических границ. Успешное вторжение Китая на Тайвань подорвало бы оборону США и союзников в регионе, тем самым ослабив стратегический плацдарм Америки в западной части Тихого океана. Кроме того, такое вторжение может нарушить глобальную цепочку поставок, лишив Соединенные Штаты доступа к важнейшим компонентам, таким как полупроводники, производимые на островном государстве. В ответ на это президент Джо Байден подчеркнул свою готовность защищать Тайвань от внешней агрессии.

Однако риски, связанные с этим геополитическим очагом, выходят далеко за рамки военных аспектов. В то время как граждане США привыкли к войнам, ведущимся на далеких берегах, Китай представляет собой принципиально иного противника, способного оказывать свое влияние беспрецедентными способами, в том числе и на территории американской родины.

Одни только военные аспекты рисуют мрачную картину. Гипотетическая стратегия Китая по захвату Тайваня, скорее всего, включает в себя быстрое и ошеломляющее нападение с использованием воздушных, морских и кибернетических средств, нацеленное на ключевые стратегические объекты, прежде чем США и их союзники смогут предпринять эффективный ответ. Относительные размеры Тайваня, сопоставимые со штатом Мэриленд, подчеркивают скорость, с которой может развернуться такая операция.

Все усложняется тем, что Китай обладает арсеналом из более чем 1350 баллистических и крылатых ракет, нацеленных на американские и союзные силы в регионе, что еще больше усложняет сценарий обороны. Соединенным Штатам придется вести войну на просторах Тихого океана, противостоя противнику, обладающему крупнейшим в мире военно-морским флотом и самыми мощными в Азии военно-воздушными силами.

Помимо обычных военных операций, Китай разработал целый ряд политических и кибернетических средств, предназначенных для проникновения в американское общество, манипулирования им и его разрушения. Эта многогранная кампания будет включать в себя дезинформационные кампании, кибератаки и, возможно, атаки на критически важные объекты инфраструктуры, такие как спутники.

В дополнение к этим проблемам Китай может использовать свой контроль над глобальными цепочками поставок и транспортными маршрутами для нанесения серьезных экономических последствий Соединенным Штатам. Экономика США в значительной степени зависит от китайских ресурсов и промышленных товаров, в том числе военного назначения. Война нарушит эту запутанную сеть торговли, что приведет к потенциальному дефициту, инфляции, безработице и экономической неопределенности.

Превращение Китая в доминирующую мировую промышленную державу изменило стратегический ландшафт. Он обогнал Соединенные Штаты по объему производства и мощности по выпуску важнейших военных компонентов. Недавний украинский конфликт продемонстрировал неспособность Америки удовлетворить потребности даже менее масштабной войны, истощив важнейшие военные запасы. По мере развития этой истории признаки такой неспособности проявляются повсеместно:

В среду США объявили о том, что, по словам официальных лиц, может стать последним пакетом военной помощи Украине, если Конгресс не одобрит закон о дополнительном финансировании, который застопорился на Капитолийском холме.

Широкая общественность, мир розничной торговли и Соединенные Штаты должны начать учитывать экономическую неопределенность, с которой столкнутся потребители в 2024 году. Это включает в себя укрепление внутренней защиты от дезинформационных кампаний, изменение конфигурации цепочек поставок критически важных товаров и реализацию долгосрочной стратегии по восстановлению доминирующего положения в мировом производстве. До этого времени Вашингтону необходимо проявлять осторожность, избегать провокаций и вести конструктивный диалог с враждебными странами.

****

В мире, где ставки никогда не были столь высоки, вызов, создаваемый потенциальным конфликтом с Китаем, не имеет себе равных. События, разворачивающиеся на мировой арене в 2024 году, несомненно, будут определяться сложной динамикой этого формирующегося геополитического ландшафта.

В сложном гобелене торговли, национальной безопасности и цифровой эпохи проблемы, изложенные в этом эссе, выходят далеко за пределы геополитических границ. Стремясь обеспечить национальные интересы и защитить целостность нашей экономики, мы должны также учитывать влияние на потребителей и их благосостояние. Нарушение цепочек поставок, кибератаки и угрозы морской торговле могут иметь прямые последствия для потребительских цен и доступности товаров первой необходимости. Нахождение баланса между безопасностью и доступностью имеет первостепенное значение, поскольку наш взаимосвязанный мир зависит от бесперебойного потока торговли.

Торговый поток еще больше нарушится.

Веб Смит